June 19, 2026

The global mining industry operates within predictable cycles of expansion and contraction, yet some declines transcend normal market rhythms to signal fundamental structural breakdown. When exploration investment collapses across multiple commodity sectors simultaneously, the implications extend far beyond temporary market adjustments to threaten the entire foundation of a resource-dependent economy.

Mining exploration represents the critical pathway from geological potential to economic production, typically requiring 15-20 years from initial discovery through mine development. This extended timeline means current exploration decisions determine production capacity two decades hence, creating a delayed but inevitable link between today's investment patterns and future economic output.

Understanding this temporal disconnect becomes essential when analysing resource economies experiencing systematic exploration decline. The consequences of reduced exploration investment remain hidden for years before manifesting as production shortfalls, employment losses, and reduced export revenues that can devastate national economic stability.

The Mechanics Behind South Africa's Exploration Collapse

South african mining exploration decline represents more than cyclical downturn patterns observed in commodity markets. The systematic reduction in exploration investment reflects fundamental breakdowns in the institutional framework supporting long-term resource development.

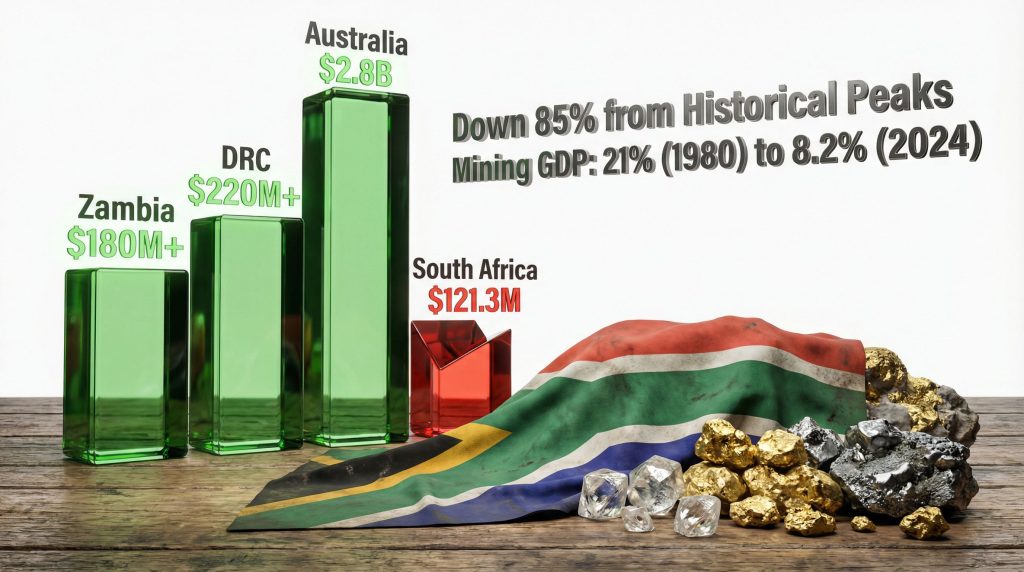

Investment in mineral prospecting has contracted more than 85% over three decades, with exploration spending declining 5.3% to 738 million rand ($43.9 million) in 2025 according to government statistics. This sustained reduction positions South Africa's exploration investment below 1% of global spending, representing a dramatic fall from historical leadership positions.

Critical Investment Decline Indicators:

• Exploration spending: 85% reduction over 30 years

• Annual decline rate: 5.3% in 2025 alone

• Global market share: Below 1% from previous leadership position

• Investment timeline: Seven consecutive years of decline

The regulatory environment creates particular challenges for junior exploration companies that historically drive early-stage project development. These smaller companies lack capital reserves necessary to navigate extended permitting challenges or maintain operations during policy uncertainty periods. Their systematic withdrawal from South African markets eliminates the exploration pipeline that feeds larger mining operations.

Infrastructure deterioration compounds exploration investment challenges. Power supply reliability issues affect exploration camps, drilling operations, and sample processing facilities. Transportation network limitations increase costs for equipment mobilisation and sample transport to analytical laboratories. These operational constraints multiply exploration costs while reducing project viability assessments.

Economic Research Southern Africa identifies underdeveloped junior mining sectors as creating effective collapse of project pipelines. This institutional assessment suggests the problem extends beyond current investment levels to encompass the systematic destruction of exploration infrastructure and expertise networks that generate future mine development opportunities.

When big ASX news breaks, our subscribers know first

Comparative Analysis: South Africa Versus Global Mining Jurisdictions

South african mining exploration decline contrasts sharply with investment patterns observed in competing resource economies. While South Africa experiences sustained capital flight, neighbouring African countries capture increasing shares of continental exploration budgets.

Zambia and Democratic Republic of Congo attract greater shares of exploration capital allocated to African markets, representing a fundamental redistribution of investment from South Africa toward competing regional jurisdictions. This capital migration reflects investor perceptions of improved regulatory stability and operational predictability in alternative locations.

Regional Exploration Investment Comparison:

| Jurisdiction | Investment Trend | Policy Stability | Infrastructure Rating |

|---|---|---|---|

| South Africa | Declining 7 years | Uncertain | Deteriorating |

| Zambia | Increasing | Improving | Moderate |

| DRC | Volatile growth | Mixed | Developing |

| Ghana | Stable growth | Stable | Improving |

The Department of Mineral and Petroleum Resources published strategies targeting restoration of South Africa's global exploration share to 5%, representing a five-fold increase from current levels. However, this recovery goal requires addressing fundamental policy and infrastructure constraints that created the initial decline.

International mining companies increasingly view South Africa as a higher-risk jurisdiction compared to alternative African investment destinations. This risk premium affects capital allocation decisions across the exploration-to-production timeline, creating competitive disadvantages that compound over multiple investment cycles.

Australia maintains exploration investment levels exceeding $2.8 billion annually through consistent regulatory frameworks and transparent permitting processes. Understanding the mineral exploration impact on economic development highlights the policy stability requirements necessary to maintain competitive exploration investment attraction in global markets.

Economic Multiplier Effects of Exploration Investment Collapse

Mining exploration decline creates cascading economic impacts extending throughout resource-dependent regional economies. The employment effects manifest across multiple sectors beyond direct mining operations, affecting transportation, engineering services, equipment supply, and consumer spending in mining-dependent communities.

Current mining sector employment decreased to 468,898 workers in the fourth quarter of 2024, declining by 3,180 positions quarter-on-quarter. This employment contraction reflects both current production adjustments and reduced hiring for exploration-stage projects that would generate future employment opportunities.

Mining Sector Employment Historical Context:

• Gold sector workforce: Declined from 500,000+ (1988) to 94,000 (2023)

• Total mining employment: 468,898 (Q4 2024), down 3,180 quarterly

• Employment decline rate: Accelerating across multiple commodity sectors

• Secondary employment: Multiplier effects across supporting industries

Production declines compound employment impacts as current mining operations reduce output across multiple commodity types. Recent production data shows mining output declining 2.7% year-on-year, with specific commodities experiencing sharper contractions including coal production down 7.9% and iron ore decreased 7.6%.

The temporal lag between exploration investment and mine development means current employment declines represent only initial manifestations of exploration cuts implemented years earlier. Future employment impacts will accelerate as existing mines exhaust reserves without replacement projects advancing through development pipelines.

Regional economies dependent on mining employment face particular vulnerability from exploration decline. Consumer spending reductions in mining-dependent communities create secondary effects across retail, services, and housing markets that extend economic impacts beyond direct mining sector boundaries.

Despite exploration collapse, total mineral sales increased 7.3% to 861 billion rand, reflecting commodity price appreciation rather than production volume growth. This revenue growth masks underlying production decline trends that will intensify as current operations exhaust reserves without exploration-derived replacement projects.

Commodity-Specific Risk Assessment and Market Implications

Different commodity sectors experience varying degrees of vulnerability from south african mining exploration decline, reflecting unique market dynamics, reserve concentrations, and demand patterns that determine global supply chain implications.

Diamond exploration investment demonstrates the most severe commodity-specific decline, falling from $126.2 million annually during 2006-2008 to $8.3 million in 2022-2024. This 93% reduction over approximately 16 years eliminates South Africa's exploration pipeline for future diamond mining projects despite continued global luxury market demand.

Critical Commodity Exposure Analysis:

• Platinum Group Metals: 70% global reserve concentration creates supply vulnerability

• Diamond: 93% exploration investment decline threatens future production

• Gold: 90% production decline despite record global prices

• Chromium/Manganese: Limited alternative global sources increase supply concentration risk

Platinum group metals face compound challenges from south african mining exploration decline and electric vehicle adoption reducing industrial demand. South Africa's control of approximately 70% of global platinum reserves creates significant supply concentration risk, particularly as exploration investment fails to identify replacement deposits for aging mines.

Gold sector performance illustrates the disconnect between commodity economics and South African production capacity. Despite record global gold prices that typically stimulate exploration investment and production expansion, South African output continues declining due to regulatory barriers and policy uncertainty overriding pure market incentives.

Furthermore, chrome and manganese markets face particular vulnerability from south african mining exploration decline due to limited alternative global sources and critical importance for steel production. Supply concentration increases create potential bottlenecks in global industrial supply chains dependent on these materials.

The electric vehicle transition affects different South African commodities in opposing directions. While platinum demand faces reduction from internal combustion engine displacement, lithium and battery metal exploration could provide new opportunities. However, current exploration decline prevents South Africa from participating in emerging commodity demand growth.

Recovery Scenarios and Timeline Analysis

South African mining exploration recovery depends on comprehensive policy reform implementation across multiple institutional frameworks simultaneously. The complexity of required interventions creates significant uncertainty regarding recovery timelines and ultimate success probability.

Government strategies target restoration of global exploration market share to 5% from current levels below 1%, representing ambitious recovery goals requiring sustained policy implementation and infrastructure investment over extended periods. Recent policy changes, including the executive order on permits, demonstrate how regulatory frameworks can rapidly transform investment environments.

Recovery Pathway Requirements:

• Tax rebate systems for exploration companies

• Transparent mining rights database establishment

• Increased geological mapping funding

• Regulatory process streamlining and timeline reduction

• Infrastructure reliability restoration across power and transport networks

Three distinct recovery scenarios emerge from current policy and market conditions, each carrying different probability assessments and timeline implications:

Optimistic Recovery Scenario (5-7 years):

Comprehensive reform implementation with sustained political commitment creates rapid policy clarity restoration. Infrastructure investment programmes address power and transport constraints while regulatory streamlining reduces permitting timelines. International investor confidence returns as policy uncertainty diminishes. Estimated probability: 25%.

Moderate Recovery Scenario (10-15 years):

Gradual policy improvements occur alongside selective infrastructure upgrades, creating partial investor confidence restoration. Recovery proceeds slowly as institutional changes require extended implementation periods. Some exploration investment returns but South Africa remains secondary choice compared to competing jurisdictions. Estimated probability: 45%.

Extended Decline Scenario (17+ years):

Continued policy uncertainty prevents meaningful reform implementation while infrastructure deterioration accelerates. South Africa develops permanent competitive disadvantage as international mining companies establish operations in alternative jurisdictions. Recovery becomes increasingly difficult as expertise networks dissolve and infrastructure decay requires massive capital investment. Estimated probability: 30%.

Economic Research Southern Africa recommends specific technical interventions including establishment of transparent mining claims framework databases and increased geological mapping funding. These evidence-based policy suggestions represent standard international best practices for exploration-stage mining sector development.

The exploration-to-production timeline means recovery benefits require 15-20 years to materialise fully, creating political challenges for sustaining reform commitments across multiple electoral cycles.

Global Supply Chain Vulnerabilities and Market Rebalancing

South african mining exploration decline creates systematic vulnerabilities in global commodity supply chains, particularly for minerals where the country maintains dominant reserve positions or significant production market shares.

Platinum group metals markets face the most severe supply concentration risk, with South Africa controlling approximately 70% of global reserves while exploration investment collapses. This combination creates potential long-term supply constraints as existing mines exhaust reserves without exploration-derived replacement projects advancing through development pipelines.

Global Supply Chain Risk Assessment:

• High Risk: Platinum, palladium, chromium, manganese

• Moderate Risk: Gold, diamond, iron ore

• Emerging Risk: Battery metals if exploration revival fails during energy transition

Chromium and manganese markets demonstrate particular vulnerability due to limited alternative global sources and critical importance for steel production. South african mining exploration decline reduces long-term supply security for these materials essential to global industrial manufacturing processes.

International commodity markets begin pricing South African supply risk premiums into long-term contract structures, reflecting reduced confidence in the country's ability to maintain production levels over extended periods. These risk premiums create competitive advantages for alternative suppliers while disadvantaging South African producers through reduced contract values.

Capital reallocation patterns show exploration investment migrating toward West African gold provinces, Zambian copper belt expansion, and Democratic Republic of Congo critical minerals projects. This geographical redistribution of investment capital creates new supply sources while reducing dependence on South African production. Countries leveraging australian industry advantages in mining technology and regulatory frameworks increasingly attract investment capital.

However, the battery metals transition presents particular challenges for South Africa's commodity mix. While platinum demand faces reduction from electric vehicle adoption, lithium and rare earth element exploration could provide new revenue sources. Current exploration decline prevents South African companies from participating in emerging commodity demand growth associated with energy transition requirements.

Mining services companies adapt to reduced South African activity by establishing operations in alternative African jurisdictions, creating brain drain effects that compound exploration capacity decline through expertise migration to competing markets.

The next major ASX story will hit our subscribers first

Investment Strategy Implications and Risk Management

South african mining exploration decline creates complex investment considerations requiring sophisticated risk assessment frameworks that account for both current production vulnerabilities and long-term supply chain implications across multiple commodity sectors.

Direct investment in South African mining assets carries elevated policy risk premiums reflecting regulatory uncertainty and infrastructure constraints that may persist despite potential reform efforts. According to Mining Weekly's analysis, investors must evaluate whether current asset valuations adequately reflect these systematic risks or if further downside adjustments remain probable.

Strategic Investment Framework Considerations:

• Policy stability assessment as primary evaluation criterion

• Infrastructure reliability requirements for operational viability

• Regulatory timeline predictability for development project economics

• Currency volatility impact on cost structures and revenue conversion

• Alternative jurisdiction comparison for opportunity cost analysis

Diversified exposure strategies enable investors to maintain commodity market participation while reducing concentration risk from South African production vulnerabilities. These approaches include direct commodity futures exposure, mining companies with geographically diversified operations, and technology companies serving global mining sectors.

Some contrarian investment perspectives identify potential value opportunities in South African mining assets, arguing that current prices reflect maximum pessimism while geological endowment remains world-class. These investment approaches require extended time horizons and acceptance of significant policy implementation risk.

Mining services companies with regional operational flexibility provide alternative exposure to African mining growth while reducing dependence on South African market conditions. These companies benefit from exploration investment migration toward competing African jurisdictions.

The rand depreciation creates potential cost advantages for South African mining operations through reduced labour and operational expenses in dollar terms. However, these currency benefits may prove temporary if exploration decline accelerates production reduction and export revenue contraction.

Risk Mitigation Strategies:

• Portfolio diversification across multiple African mining jurisdictions

• Commodity futures for direct price exposure without operational risk

• Mining technology companies serving global markets

• Currency hedging for South African asset exposure

• Extended investment timelines accounting for policy implementation delays

Professional mining investors emphasise geological endowment quality versus policy framework trade-offs when evaluating South African opportunities. While resource quality remains globally competitive, sustained policy uncertainty creates operational challenges that may offset geological advantages.

Lessons for Resource-Dependent Economic Development

South african mining exploration decline provides critical insights for resource-dependent economies seeking to maintain competitive advantages in global commodity markets. The systematic nature of this decline demonstrates how quickly natural resource endowments can become economically inaccessible through policy mismanagement.

The temporal lag between policy implementation and economic outcomes creates particular challenges for democratic political systems where electoral cycles encourage short-term decision-making over long-term institutional development. Mining exploration requires 15-20 year investment horizons that extend beyond typical political planning frameworks.

International mining investment flows toward jurisdictions offering predictable regulatory environments, transparent permitting processes, and reliable infrastructure networks. These institutional requirements remain consistent across different geological and geographical contexts, suggesting universal principles for resource sector development.

The junior mining company ecosystem plays essential roles in early-stage exploration that larger corporations cannot efficiently perform. Policy frameworks must specifically support these smaller exploration companies through targeted tax incentives, streamlined permitting, and transparent mining rights allocation systems.

Infrastructure reliability emerges as a fundamental requirement for exploration-stage mining operations that cannot justify backup power systems or alternative transportation networks during early development phases. Countries allowing infrastructure decay create systematic barriers to exploration investment regardless of geological potential.

Policy Framework Requirements for Exploration Investment:

• Regulatory predictability across extended investment timelines

• Transparent mining rights databases and allocation processes

• Tax incentive structures supporting early-stage exploration risk

• Infrastructure reliability for power, transport, and communications

• Institutional stability transcending electoral cycles

South Africa's experience demonstrates that geological endowment alone cannot sustain mining sector competitiveness without supporting institutional frameworks. Countries with inferior geological potential but superior policy environments successfully attract exploration capital from traditionally dominant producers.

The exploration-to-production timeline creates irreversible consequences from policy failures that require decades to correct once institutional damage occurs. This temporal dynamic emphasises prevention over remediation in resource sector policy development. Analysis from Engineering News suggests that technological innovation and skills development remain crucial for recovery prospects.

Global commodity markets provide alternative supply sources when traditional producers experience systematic decline, reducing the leverage that resource endowment historically provided to producing countries. This market evolution requires resource-dependent economies to maintain competitive institutional frameworks rather than relying on geological advantages alone.

Investment Disclaimer: This analysis contains forward-looking assessments and probability estimates that involve substantial uncertainty. Mining exploration involves significant risks including policy changes, infrastructure failures, commodity price volatility, and geological uncertainty. Past performance does not guarantee future results, and investors should conduct independent due diligence before making investment decisions. Currency fluctuations may affect international investment returns. Consult qualified financial advisors before making investment commitments.

Want to Capitalise on Major Mineral Discoveries Before the Market Catches Up?

Discovery Alert provides instant notifications on significant ASX mineral discoveries using its proprietary Discovery IQ model, empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why historic discoveries can generate substantial returns by visiting Discovery Alert's dedicated discoveries page and begin your 14-day free trial today to position yourself ahead of the market.