June 18, 2026

The Geology of Scarcity: Why Billion-Tonne Copper Deposits Are Worth Fighting For

The mining industry operates on a fundamental geological reality that rarely surfaces in mainstream financial commentary: truly large, high-quality copper deposits are not just valuable, they are vanishing. The average grade of newly discovered copper porphyry systems has declined steadily over the past four decades, and the number of discoveries exceeding one billion tonnes of resource has become extraordinarily rare. When one of these deposits surfaces through a competitive sovereign auction, the strategic calculus for major copper producers changes entirely. The Southern Copper Michiquillay property bid, concluded in February 2018, represents precisely this type of inflection point, one where geological endowment, corporate strategy, and sovereign resource monetisation converge in a single transaction.

Understanding why this acquisition matters requires stepping back from the deal mechanics and examining the broader forces shaping copper supply over the coming decades.

When big ASX news breaks, our subscribers know first

Peru's Cajamarca Region and the Global Copper Supply Equation

A Structural Deficit Written in the Ground

Copper sits at the intersection of nearly every major industrial and technological transition underway globally. Electric vehicles require roughly three to four times more copper than internal combustion equivalents. Grid-scale battery storage, offshore wind infrastructure, and solar installations each demand substantial copper inputs across cabling, transformers, and inverter systems. The International Copper Study Group and various independent research bodies have consistently highlighted a growing divergence between projected demand trajectories and the existing development pipeline's ability to satisfy them.

The challenge is compounded by geology. Porphyry copper systems, the geological class to which Michiquillay belongs, typically form in ancient volcanic arcs where magmatic fluids deposit copper mineralisation across enormous volumes of rock. These systems can extend over several kilometres in both depth and lateral extent, which is precisely what makes them commercially viable at scale. However, the easily accessible, near-surface, high-grade variants of these systems have largely already been discovered and developed.

What remains in the undeveloped pipeline tends to be deeper, lower grade, more complex to permit, or located in jurisdictions carrying elevated social and political risk. Consequently, the copper supply crunch facing the global industry is not simply a question of demand outpacing investment — it is a geological reality embedded in the declining quality of the remaining undeveloped resource base.

Northern Peru's Geological Endowment

The Cajamarca region sits within one of South America's most productive copper metallogenic belts. This belt runs parallel to the Andes cordillera and has produced some of the world's most significant copper operations, including Cerro Verde in the south and the contested Las Bambas project further along the arc. The geological architecture of northern Peru reflects a long history of subduction-related magmatism that created ideal conditions for large-scale copper-molybdenum-gold porphyry emplacement.

Peru consistently ranks among the world's top two copper-producing nations by volume, and the Cajamarca region's porphyry copper systems represent some of the last large-scale undeveloped assets available through competitive sovereign tender processes.

What makes Cajamarca particularly interesting from a technical perspective is the polymetallic nature of its deposits. Unlike some copper provinces where the resource is essentially mono-metallic, the Cajamarca systems frequently carry meaningful molybdenum, gold, and silver credits. These by-product contributions are not trivial. At sufficient production scale, molybdenum and gold revenues can materially reduce the net cash cost per pound of copper produced, effectively improving the economic resilience of the operation across commodity price cycles.

Michiquillay: Technical Profile of a Generational Copper Asset

Resource Scale and Deposit Characteristics

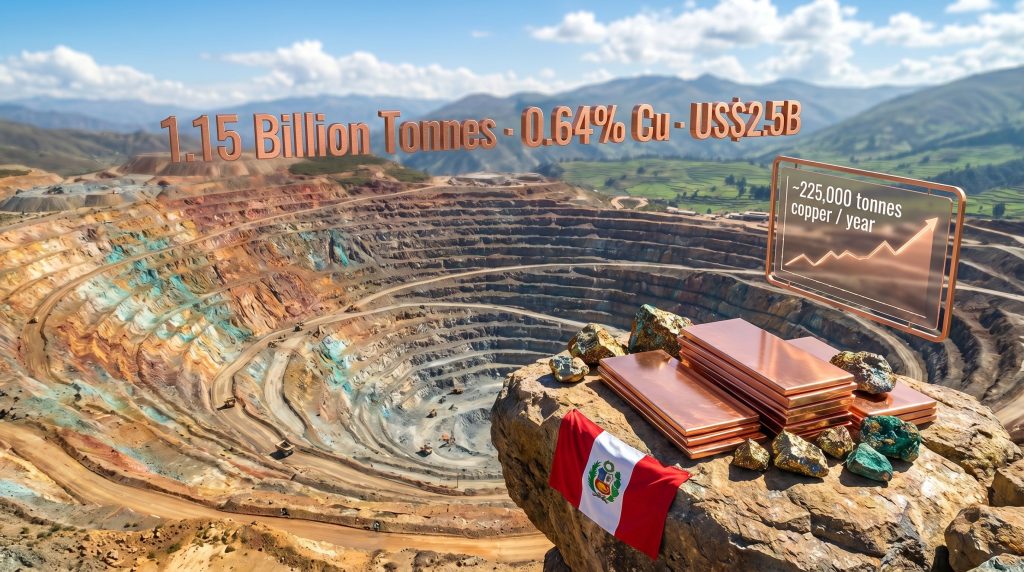

The Michiquillay copper deposit sits in the northern Cajamarca region and carries a resource estimate that places it firmly in the upper tier of undeveloped copper assets globally. The key technical parameters reported at the time of the 2018 auction are summarised below.

| Metric | Estimated Figure |

|---|---|

| Total Resource Tonnage | ~1.15 billion tonnes |

| Average Copper Grade | 0.64% Cu |

| Estimated Annual Production | ~225,000 tonnes copper |

| Capital Development Cost | US$2.0 to US$2.5 billion |

| By-Products | Molybdenum, gold, silver |

One critical caveat must be noted: the resource estimate disclosed at auction time was not compliant with NI 43-101 standards, the internationally recognised framework for reporting mineral resources and reserves. This means the figures should be treated as historically indicative rather than independently verified. Investors and analysts should apply appropriate scepticism and await updated compliant resource estimates as the project progresses through its development lifecycle.

Why 0.64% Cu Matters More Than It Appears

A copper grade of 0.64% may appear modest to those unfamiliar with porphyry economics, but contextualising this figure within the broader development pipeline is instructive. Many recently proposed large-scale copper projects carry grades below 0.5%, and some advanced-stage deposits are being developed at grades closer to 0.3% to 0.4%. At 0.64%, Michiquillay sits above the industry average for new porphyry developments, providing a meaningful operating cost advantage on a per-tonne-of-copper-produced basis once in operation.

The polymetallic credit structure adds further economic depth. Molybdenum, a by-product common to many Andean porphyry systems, is a high-value steel-hardening agent that commands significant market pricing. Gold and silver credits, even at modest concentrations, contribute meaningfully to the project's all-in sustaining cost calculations, potentially allowing Michiquillay to operate competitively through copper price downturns that would strand lower-quality assets. Understanding the broader copper price drivers at play is therefore essential context for evaluating this asset's long-term commercial position.

Tier-1 Classification: What It Actually Means

The term tier-1 asset is frequently misused in mining commentary, but it carries a specific technical and commercial meaning. A genuinely tier-1 copper asset is characterised by:

- A resource base capable of supporting a mine life exceeding 20 to 25 years at commercial production rates

- Operating costs in the lower half of the global cost curve, meaning the asset remains cash-generative across most commodity price environments

- A resource scale large enough to justify the capital intensity of a modern processing facility

- Jurisdictional accessibility sufficient to attract institutional capital and major operator involvement

Michiquillay satisfies the first three criteria comfortably. At 225,000 tonnes of annual copper production from a 1.15 billion tonne resource base, the implied mine life at reasonable recovery assumptions extends well beyond three decades, a characteristic that distinguishes generational assets from shorter-lived operations.

Dissecting the Auction: How Southern Copper Secured Michiquillay

Peru's Proinversión Tender Mechanism

Proinversión functions as Peru's primary state agency for structuring and executing competitive investment tenders across infrastructure and resource sectors. Unlike open-market mergers and acquisitions where price discovery occurs through negotiation between willing buyers and sellers, sovereign tender processes involve the state setting the structural parameters of the deal while competing bidders optimise their proposals within those constraints.

For Michiquillay, the bid evaluation framework incorporated three primary components: an upfront cash payment to the Peruvian state, a committed royalty rate on future production revenues, and social investment obligations tied to community development in the surrounding Cajamarca region. This structure reflects Peru's experience with large mining project development and the government's objective of front-loading revenue capture while sharing long-term upside through royalty streams.

The Winning Bid Structure

Southern Copper's successful tender submission combined a US$400 million upfront payment with a committed 3% royalty on production revenues. The full development capital requirement is separately estimated at US$2.0 to US$2.5 billion, representing the cost of constructing the mine, processing plant, tailings facilities, and associated infrastructure required to bring Michiquillay into production.

| Bid Component | Value |

|---|---|

| Upfront Government Transfer | US$400 million |

| Production Royalty Rate | 3% |

| Competing Bidders | 2 total |

| Total Development Capex Estimate | US$2.0 to US$2.5 billion |

A particularly telling detail is that only two companies submitted bids in the final tender round. This limited participation is not unusual for projects of this capital complexity, but it does reflect the high barriers to entry in large-scale Peruvian copper development. Assembling the financing capacity, technical expertise, and regulatory experience required to credibly develop a multi-billion dollar project in Cajamarca narrows the competitive field considerably.

Grupo Mexico's Strategic Logic

Southern Copper operates as a subsidiary of Grupo Mexico, one of Latin America's largest diversified mining and infrastructure conglomerates. This ownership structure is strategically significant in the context of the Michiquillay acquisition.

For a vertically integrated mining conglomerate with Grupo Mexico's balance sheet capacity, acquiring a billion-tonne copper deposit through a sovereign tender process rather than purchasing a listed junior explorer eliminates the takeover premium and provides direct engagement with the host government on development terms from the outset.

This distinction is worth emphasising. When a major miner acquires a junior company holding a copper project, it typically pays a premium above the net asset value to compensate existing shareholders for the optionality and exploration success embedded in the asset. Sovereign tenders bypass this premium entirely, replacing it with a negotiated upfront payment and royalty obligation that, in many scenarios, represents a lower total cost of entry on a per-tonne-of-resource basis. At US$400 million for 1.15 billion tonnes, Southern Copper's entry cost equates to roughly US$0.35 per tonne of in-situ resource, a figure that compares favourably against many market-based copper acquisition transactions during the same period.

Capital Intensity and Development Realities

Benchmarking the US$2.5 Billion Capex Estimate

The US$2.5 billion development cost estimate for Michiquillay places its capital intensity at approximately US$11,000 per tonne of annual copper production capacity, based on the projected 225,000 tonne output figure. This compares reasonably with peer-group porphyry copper developments in the Andean region, though the industry's experience with projects like Las Bambas and Quellaveco highlights the tendency for large Peruvian copper developments to experience cost escalation during construction.

A typical capital expenditure breakdown for a project of this nature would allocate resources across the following categories:

- Open pit mine development including pre-stripping and haul road construction

- Concentrator plant incorporating crushing, grinding, flotation, and dewatering circuits

- Tailings storage facility designed for multi-decade operational capacity

- Water management infrastructure covering fresh water supply and process water recycling

- Power supply either through grid connection or dedicated generation capacity

- Camp facilities and logistics including access road upgrades and port arrangements if required

Each of these categories carries its own escalation risk in the Peruvian Andes, where altitude, remote access, and logistical complexity routinely push costs above initial estimates.

The 2025 Production Target: A Realistic Assessment

Southern Copper indicated a production commencement target of approximately 2025 at the time of the bid award in early 2018. Achieving this timeline would require successfully completing environmental impact assessments, obtaining construction permits, completing detailed engineering, and executing a multi-year construction programme — all while maintaining community acceptance in what has historically been one of Peru's most contested mining jurisdictions.

The track record of comparable Peruvian copper developments suggests that even well-funded, technically capable operators routinely encounter timeline extensions driven by regulatory sequencing and community negotiation processes. Anglo American's Quellaveco project, a similarly scaled copper development in Peru, took over two decades from initial discovery to first production. This context is essential for calibrating expectations around Michiquillay's development timeline.

Social Licence: The Variable That Overrides Everything Else

Cajamarca's Contested Mining History

No analysis of the Michiquillay acquisition is complete without examining the social and political dynamics of Cajamarca province. The region carries a significant legacy of mining-community conflict that has directly affected multi-billion dollar copper project timelines in the past. The most prominent example is the Conga gold-copper project operated by Newmont, which was effectively suspended following prolonged community protests and political opposition despite having received formal government approvals.

The Conga impasse cost Newmont years of development time and ultimately contributed to a fundamental restructuring of the project's development approach. Cajamarca's community dynamics are shaped by a combination of factors that distinguish it from more straightforward mining jurisdictions:

- High-altitude water sources, including lakes and wetlands, that local communities depend on for agricultural and domestic use

- A well-organised civil society with demonstrated capacity to mobilise sustained opposition to mining projects

- Historical grievances related to environmental impacts from legacy mining operations in the region

- Political actors at both local and national levels who have leveraged anti-mining sentiment for electoral purposes

Why Social Licence Is the Critical Path Item

Technical feasibility and financial capacity are necessary conditions for developing Michiquillay, but they are insufficient on their own. The project's ultimate development timeline will be determined primarily by Southern Copper's ability to build genuine acceptance among affected communities in Cajamarca, a process that cannot be compressed through capital deployment alone.

Any credible development timeline for Michiquillay must account for the social and political complexity that has historically extended permitting processes in Cajamarca by years, not months. The technical and financial case for the project is straightforward; the human and political case requires sustained, transparent engagement that demonstrates material benefit to local communities.

Effective social licence strategies for large Andean copper projects typically involve co-investment in local water infrastructure, guaranteed employment quotas for community members, transparent revenue-sharing arrangements, and ongoing independent monitoring of environmental parameters. Southern Copper's track record at its existing Peruvian operations will be scrutinised closely by Cajamarca communities and advocacy groups as the development process advances.

The next major ASX story will hit our subscribers first

Southern Copper's Broader Peru Strategy

Portfolio Context and Production Growth

Southern Copper was already a significant copper producer in Peru prior to the Michiquillay acquisition, with established operations contributing meaningfully to the country's national copper output. The addition of a potential 225,000 tonne per year copper producer represents a substantial incremental contribution to both Southern Copper's global production profile and Peru's national output.

Furthermore, Peru's copper production has grown substantially over the past decade, driven by expansions at Cerro Verde and the commissioning of Las Bambas. Michiquillay's eventual production would add further volume to an already significant national output base. In this context, understanding how Michiquillay fits within the landscape of the largest copper mines globally helps illustrate the asset's long-term strategic significance.

The Reserve Depletion Imperative

For established copper majors, the strategic calculus around large undeveloped deposits is driven as much by reserve replacement as by pure production growth. Every tonne of copper extracted from existing operations depletes the reserve base, and unless new resources are added through exploration or acquisition, the long-term production profile inevitably declines. Securing Michiquillay gives Southern Copper a generational asset capable of anchoring its Peruvian production portfolio well into the second half of the 21st century.

This reserve replacement dynamic is one of the lesser-understood drivers of sovereign tender participation by major miners. The internal rate of return analysis on a project like Michiquillay must be viewed alongside the opportunity cost of not securing the asset, particularly given the scarcity of comparable undeveloped resources available through any acquisition pathway. In addition, the growing emphasis on copper exploration importance underscores why securing known, large-scale deposits through sovereign tenders has become an increasingly rational strategy for majors facing depleting reserve bases.

Frequently Asked Questions: Southern Copper Michiquillay Property Bid

What did Southern Copper pay for the Michiquillay copper project?

Southern Copper's winning bid comprised a US$400 million upfront cash transfer to the Peruvian government, combined with a committed production royalty of 3%. The separate capital cost required to actually construct and commission the mine is estimated at US$2.0 to US$2.5 billion, which Southern Copper would fund through its own balance sheet and financing arrangements over the development period.

How large is the Michiquillay copper deposit?

The deposit contains an estimated 1.15 billion tonnes of mineralisation grading 0.64% copper, with additional by-product credits from molybdenum, gold, and silver. Importantly, this resource estimate was not reported in compliance with NI 43-101 standards at the time of the 2018 auction and should be treated as historically indicative pending updated compliant reporting.

Who administered the Michiquillay tender process?

Proinversión, Peru's state agency responsible for attracting and structuring private investment in major resource and infrastructure projects, conducted the competitive auction process.

Why did so few companies bid on Michiquillay?

Only two companies participated in the final tender round, reflecting the substantial capital requirements, permitting complexity, and social risk profile associated with developing a multi-billion dollar copper project in Cajamarca. Projects of this scale effectively self-select for a very small cohort of operators with the financial capacity, technical expertise, and risk tolerance required. However, copper project partnerships between majors and junior explorers represent an alternative route through which smaller players can gain exposure to assets of this magnitude without bearing the full capital burden independently.

When is Michiquillay expected to produce copper?

Southern Copper indicated a target production commencement date of approximately 2025 at the time of the 2018 bid award. However, given Cajamarca's historical permitting and community consultation timelines, this target should be understood as aspirational rather than fixed, subject to successful completion of environmental assessments and ongoing community engagement processes.

Key Takeaways: What the Michiquillay Acquisition Reveals About Copper's Strategic Future

The Southern Copper Michiquillay property bid is not merely a transactional event. It is a case study in how sophisticated mining companies secure production capacity in an environment of geological scarcity. Several broader lessons emerge from examining this acquisition in depth, as reported at the time of the bid by industry observers who noted the unusually limited competition for such a significant asset:

- Geological scarcity commands strategic premiums: Billion-tonne copper deposits at economically relevant grades are not being discovered at a rate sufficient to replace consumption, making existing undeveloped tier-1 assets disproportionately valuable

- Sovereign tenders offer structurally different risk profiles compared to open-market M&A, bypassing acquisition premiums while introducing host government relationship dynamics that persist throughout the project lifecycle

- By-product economics fundamentally reshape project viability: Michiquillay's molybdenum, gold, and silver credits are not incidental — they are integral to the asset's economic resilience across copper price cycles

- Social licence is a non-financial risk with entirely financial consequences: Cajamarca's history demonstrates that community opposition can render technically sound, well-funded projects commercially inoperable

- Reserve replacement drives sovereign tender participation as much as pure production growth, a dynamic that is frequently underweighted in conventional deal analysis

- The 0.64% Cu grade advantage is real but not permanent: As Michiquillay ages and mining depths increase, grade profiles may evolve, making early high-grade production periods critical to project economics

Disclaimer: This article is intended for informational and educational purposes only and does not constitute financial or investment advice. Resource estimates cited reflect historical figures available at the time of the 2018 auction and may not comply with current reporting standards. Readers should conduct their own due diligence before making investment decisions. Forward-looking statements regarding production timelines, capital costs, and project development are inherently uncertain and subject to material change.

Want to Track the Next Major Copper Discovery Before the Market Catches On?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries — including copper — and delivering actionable alerts to subscribers ahead of the broader market. Explore historic examples of major discovery returns to understand the opportunity, then begin your 14-day free trial at Discovery Alert to position yourself at the forefront of the next significant find.