June 5, 2026

When Supply Chain Fragility Meets Geological Fortune

The global race to secure heavy rare earth supply outside Chinese jurisdiction has shifted from a policy discussion into an active capital deployment event. Across Washington, Tokyo, and Brussels, governments and industrial procurement offices are no longer simply expressing concern about rare earth dependency; they are writing cheques, signing offtake agreements, and restructuring defence procurement frameworks to accelerate the emergence of alternative supply. For investors tracking this dynamic, the critical question is not whether demand for non-Chinese heavy rare earths will grow, but which projects carry the geological and economic profile to actually satisfy it.

That question brings the Sovereign Metals Kasiya project rare earth upside into sharp analytical focus. What began as a compelling rutile-graphite development story has evolved into something structurally more significant: a tri-commodity project where the newest revenue layer requires no additional mining capital, sits inside pits already scheduled for Year 1 production, and carries a rare earth compositional profile that has no equivalent among currently operating producers outside China. Furthermore, the broader rare earth supply chain context makes this development all the more compelling for investors seeking exposure to strategic minerals.

When big ASX news breaks, our subscribers know first

The Economics That Existed Before the Rare Earth Discovery

A DFS That Sets a New Scale Benchmark

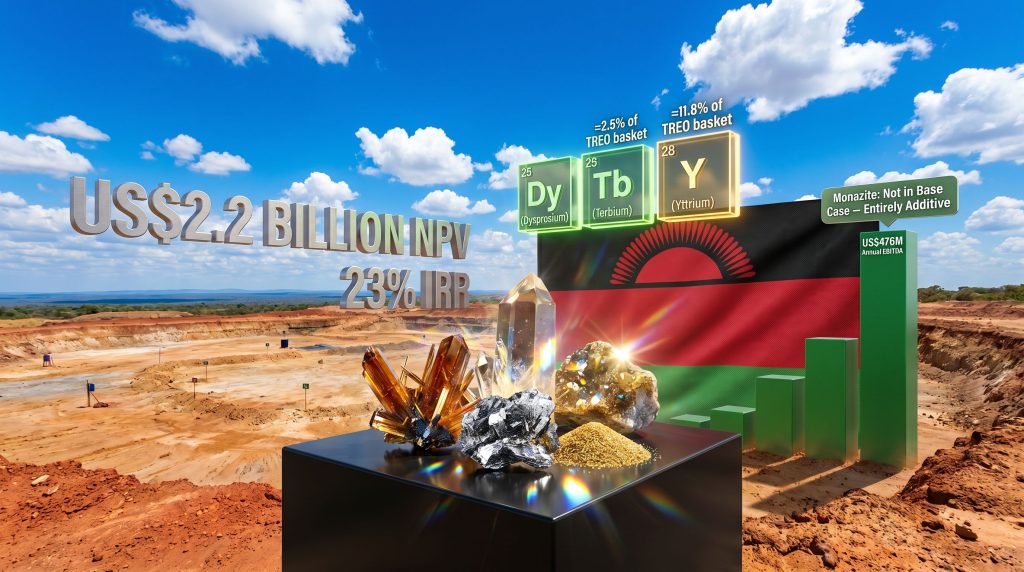

Before evaluating the Sovereign Metals Kasiya project rare earth upside, it is worth establishing what the project already is without a single tonne of monazite in the revenue model. The Kasiya Definitive Feasibility Study (DFS) delivers a pre-tax net present value of US$2.2 billion at an 8% discount rate, alongside an internal rate of return of 23% and projected annual EBITDA of US$476 million across a 25-year mine life.

Production ramps in two phases:

- Phase 1: A single southern processing plant treats 12 million tonnes per annum, operational at commissioning.

- Phase 2: A northern plant addition brings throughput to 24 million tonnes per annum from Year 5 onward.

Annual free cash flow at full production capacity is projected to exceed US$400 million, and the commodity price assumptions underpinning those numbers are demonstrably conservative.

Why the Base-Case Pricing Creates Embedded Asymmetry

The DFS uses independently supplied price assumptions that sit below current Western market references in key areas. The table below illustrates the gap between base-case inputs and observable market conditions:

| Commodity | DFS Base-Case Price | Current Market Reference | Upside Signal |

|---|---|---|---|

| Rutile | ~US$1,670/tonne | Defence procurement premiums rising | Conservative vs. constrained supply |

| Graphite (jumbo flake) | ~US$1,288/tonne | US market ~US$2,000-US$2,200/tonne | ~55-70% below spot |

| Monazite (60% TREO) | Not modelled | US$16,000-US$19,000/tonne (independent forecast) | Entirely additive to NPV |

The graphite pricing gap alone is significant. At approximately US$2,000-US$2,200 per tonne for jumbo flake in the US market, the DFS input of US$1,288 per tonne represents a discount of between 55% and 70%. Any normalisation of graphite pricing toward current market levels would flow directly into project economics without any operational adjustment required.

The Structural Cost Advantage: Free-Dig Mineralogy

Most mining cost analyses focus on operating expenditure per tonne. At Kasiya, the more important structural advantage is what the project does not require. The entire ore body sits within a deep tropical weathering profile on the flat Lilongwe Plain, meaning rutile, monazite, and graphite are all hosted in a laterally extensive blanket above the saprock boundary. There is no drilling, no blasting, and no pre-stripping.

This eliminates the three largest capital and operating cost drivers at hard-rock mining operations. The processing flowsheet begins at a power requirement of just 30 megawatts, scaling to 60 megawatts at full capacity. Crucially, both figures sit within the capacity of Malawi's existing national grid, with infrastructure expansion already underway involving the World Bank, Total, and EDF.

Free-dig mineralogy is not simply a cost advantage; it is a competitive moat. Hard-rock peers cannot replicate a surface-hosted weathering profile, and the low energy intensity of the Kasiya flowsheet is a permanent feature of the geology, not a function of project design choices.

The Monazite Discovery: Dissecting the Rare Earth Composition

Why TREO Basket Composition Matters More Than Volume

A common error in rare earth project analysis is treating total rare earth oxide volume as the primary value driver. In practice, the composition of the TREO basket is what determines both commercial pricing and strategic relevance. Rare earths divide broadly into two groups:

- Light rare earth oxides (LREOs): Cerium, lanthanum, and praseodymium dominate most producing deposits. These elements have relatively limited pricing power and face oversupply conditions in the standard monazite market.

- Heavy rare earth oxides (HREOs): Dysprosium, terbium, and yttrium are present in far smaller quantities globally, face structurally inelastic demand from permanent magnet manufacturing and defence applications, and are the specific elements subject to China's April 2025 export controls.

The Kasiya TREO basket is weighted toward the second group in proportions that have no precedent among producing peers. In addition, the rare earth processing challenges that typically constrain HREO development are considerably less acute at Kasiya given its free-dig mineralogy and existing processing flowsheet.

The Four-Pit Data: What the Numbers Actually Show

Monazite confirmation spans four DFS pits: Babbler, Kingfisher, Sparrow, and Mousebird. All four are scheduled within the early production sequence. The compositional data confirmed across these pits is striking:

| TREO Component | Kasiya 4-Pit Weighted Average | Top 5 Global REE Producers Average | Multiple |

|---|---|---|---|

| Dysprosium + Terbium (DyTb) | ~2.5% of TREO basket | ~0.4% of TREO basket | ~6x higher |

| Yttrium | ~11.8% of TREO basket | ~1.7% of TREO basket | ~7x higher |

| DyTb at 0-6m depth | Up to 3.1% | – | Exceptional surface grade |

| Yttrium at 0-6m depth | Up to 17.2% | – | Exceptional surface grade |

The near-surface depth profile (0 to 6 metres) returning dysprosium-terbium up to 3.1% and yttrium up to 17.2% is particularly relevant. These concentrations appear precisely in the depth range that the free-dig mining method targets, requiring no change whatsoever to the extraction approach.

Zero Incremental Mining Capital: The Key Structural Point

The mechanism by which monazite becomes recoverable is worth explaining precisely, because it is the feature that makes the economics so unusual. Within the existing DFS processing flowsheet, material passes through a series of separation circuits designed to isolate rutile and graphite. What remains is classified as a non-conductor tailings stream. It is this stream, already being processed in the existing flowsheet, that has been confirmed to carry monazite.

The implication is that the capital question for rare earth recovery shifts from conventional mine development economics to a narrower, more tractable question: what does a monazite concentration and separation circuit add to the back end of a flowsheet that is already funded and engineered?

Important caveat: Metallurgical and mineralogical studies are ongoing. Recoverable monazite volumes across the full deposit have not yet been formally quantified, and any formal incorporation of rare earth revenue into project economics is contingent on the completion of that work.

The Geopolitical Dimension: Why Western Capital Is Paying a Premium

The Scale of US Dependency on Chinese Heavy Rare Earths

US Senate testimony delivered on February 24, 2026 by the Assistant Secretary of War for Industrial Base Policy confirmed that China controls approximately 95% of global heavy rare earth output and that the US imports close to 100% of its requirements. Yttrium dependency stands at 100% import reliance. America's only fully integrated domestic rare earth producer carries no measurable dysprosium, terbium, or yttrium. There is, at present, no domestic US equivalent to Kasiya's HREO profile.

China's rare earth export restrictions on dysprosium, terbium, and yttrium, implemented in April 2025, represent a material tightening of Western access to the three elements most critical to permanent magnet manufacturing for electric motors, wind turbines, and military guidance systems. The demand for these elements is structurally inelastic; there is no commercial substitute for dysprosium-enhanced neodymium iron boron magnets in high-temperature, high-torque applications.

Sovereign Metals' Chief Commercial Officer outlined the full scope of US dependency across multiple critical mineral categories, noting that the country currently has zero domestic titanium, zero domestic graphite, and zero domestic heavy rare earths, with each of these supply gaps posing risks to both industrial and defence capability.

The Titanium Dimension: A Compounding Strategic Narrative

Separate from, but strategically compounding, the rare earth thesis is Kasiya's positioning within the Western defence titanium supply chain. Toho Titanium, Japan's most technically demanding titanium producer and the principal supplier of defence-grade titanium to Western procurement programmes following Russia's exclusion post-2022, has confirmed that Kasiya rutile meets full specification across its entire production range.

The US currently produces zero domestic titanium sponge. The defence platforms dependent on uninterrupted titanium supply include:

- The F-35B Lightning II (approximately 35% titanium by weight)

- Virginia-class submarines

- M1 Abrams main battle tanks

- Boeing 787 Dreamliner commercial aircraft

Sovereign Metals' commercial leadership has characterised this dependency explicitly, noting that the functioning of these platforms is contingent on titanium supply, and titanium producers have made clear they cannot deliver without access to high-quality rutile feedstock. Kasiya's rutile qualification therefore creates a direct pathway into Western defence procurement that exists independently of any rare earth considerations. This dynamic also feeds into the broader critical minerals demand surge reshaping Western procurement strategy in 2025 and beyond.

M&A Transactions That Establish a Valuation Reference

Two recent transactions frame the capital market valuation context for Western-aligned rare earth assets:

| Transaction | Date | Value | Key Terms |

|---|---|---|---|

| USA Rare Earth acquisition of Serra Verde Group | April 20, 2026 | ~US$2.8 billion | 15-year offtake; floor prices of US$575/kg dysprosium, US$2,050/kg terbium |

| Energy Fuels acquisition of Australian Strategic Materials | January 20, 2026 | ~US$299 million | Western-aligned rare earth processing capability |

The Serra Verde floor prices contextualise why Kasiya's TREO basket composition commands such a significant premium over standard monazite benchmarks. A basket weighted toward dysprosium and terbium, at government-backed floor prices of US$575 and US$2,050 per kilogram respectively, justifies independent price forecasts for Kasiya's 60% TREO monazite concentrate at US$16,000 per tonne (base case) and US$19,000 per tonne (high case), compared to the April 2026 Shanghai Metals Market standard monazite benchmark of US$6,142 per tonne.

Neither the Serra Verde nor the Australian Strategic Materials assets carry a HREO compositional profile comparable to Kasiya's four-pit weighted average.

Four Milestones Between Now and Full Valuation Recognition

The Re-Rating Pathway

The gap between Kasiya's current US$2.2 billion NPV and a fully integrated tri-commodity valuation runs through four discrete events, each representing an independent catalyst for re-rating:

-

ESIA Completion and Mining Licence Application: The Environmental and Social Impact Assessment is nearing completion. Together with the DFS, it forms the formal mining licence submission. The process applies IFC performance standards, the benchmark recognised by commercial banks, development finance institutions, and government agencies as the threshold for project bankability.

-

IFC Financing Package Advancement: The International Finance Corporation is engaged as a potential co-lead arranger for project debt. The indicative structure targets approximately 60% debt (US$400-US$450 million), with the balance from equity, prepayments, and offtake finance. Mitsui has signed an offtake MOU covering over 50% of Stage 1 rutile production. Traxys of North America has signed an MOU targeting up to 40,000 tonnes per annum of graphite during Phase 1, providing contracted revenue visibility for the debt case.

-

Monazite Volume Quantification Across the Full Deposit: The current confirmation covers four pits. Deposit-wide quantification of recoverable monazite volumes is the critical step that would permit formal incorporation of rare earth revenue into project economics. Completion of metallurgical and mineralogical studies determines whether monazite transitions from optionality to a third modelled revenue stream.

-

Potential US Equity Listing: A US listing would connect Sovereign's capital structure to the institutional and government capital pools most actively deploying into non-Chinese critical minerals. The company has already engaged with the US State Department, Department of Defense, Office of Strategic Capital, US International Development Finance Corporation (DFC), and US Trade and Development Agency. The DFC's US$565 million mine development finance commitment to Serra Verde establishes a precedent for the scale of US government-backed financing available to qualifying projects.

Furthermore, America's rare earth supply chain vulnerabilities make a US listing an increasingly logical step, given the intensity of capital flows targeting non-Chinese HREO projects in the current policy environment.

Scenario Framework: What Formal Monazite Incorporation Changes

The following scenarios illustrate the valuation progression as the rare earth thesis matures from optionality to formal economics:

-

Scenario A (Current State): NPV of US$2.2 billion from rutile and graphite only. Monazite is compositionally confirmed but not economically modelled. This is the floor, not the ceiling.

-

Scenario B (Partial Quantification): Recoverable monazite volumes confirmed across a subset of the deposit. Rare earth revenue modelled at conservative pricing. NPV uplift determined by recoverable tonnes and separation circuit capital requirements.

-

Scenario C (Full Tri-Commodity Economics): Deposit-wide monazite quantification complete. A 60% TREO concentrate priced at US$16,000 per tonne is formally integrated into the project financing model alongside rutile and graphite. This scenario reflects the full scope of what Kasiya may produce.

The entire rare earth upside thesis exists in the space between Scenario A and Scenario C. Every milestone listed above moves the project one step closer to the formal economic recognition of a mineral that is already present in the ground, already being processed through an existing flowsheet, and already independently valued at a significant premium to the standard market benchmark.

Frequently Asked Questions

What rare earth elements does Kasiya's monazite contain?

Monazite recovered from the DFS non-conductor tailings stream contains all four magnetic rare earth elements, with dysprosium, terbium, and yttrium confirmed in measurable concentrations across all four tested pits. The four-pit weighted average carries approximately 2.5% dysprosium-terbium and 11.8% yttrium within the TREO basket.

Is rare earth revenue included in the US$2.2 billion NPV figure?

No. The base-case NPV of US$2.2 billion at an 8% discount rate is derived entirely from rutile and graphite revenue. Monazite represents potential upside that is entirely additive to the current valuation, contingent on the completion of volume quantification studies.

Why does Kasiya's monazite command a price premium over standard benchmarks?

Standard monazite is dominated by lower-value light rare earths including cerium and lanthanum. Kasiya's basket carries disproportionately elevated concentrations of dysprosium, terbium, and yttrium, the elements subject to Chinese export controls and the highest per-kilogram values in Western government procurement contracts. This compositional distinction supports an independent forecast of US$16,000-US$19,000 per tonne against an April 2026 standard benchmark of US$6,142 per tonne.

Does recovering monazite require new mining or separate infrastructure?

Based on current testwork, monazite reports to the non-conductor tailings stream within the existing flowsheet, requiring no new mining activity or primary processing circuits. A downstream concentration and separation circuit would likely be required, with metallurgical studies ongoing to confirm technical and economic parameters.

The next major ASX story will hit our subscribers first

The Investment Framework: Separating Confirmed Value From Emerging Upside

The analytical discipline required when evaluating the Sovereign Metals Kasiya project rare earth upside is to maintain a clear separation between what is confirmed and what remains contingent. The US$2.2 billion NPV is confirmed, bankable, and supported by conservative commodity pricing. The rare earth thesis is confirmed in compositional terms but not yet quantified in volume or formally modelled in economics.

What distinguishes this rare earth optionality from typical development-stage REE claims is the specificity of each component:

- The mineralisation is present in pits scheduled for Year 1 production, not speculative exploration ground.

- Recovery requires no incremental mining capital, limiting the cost question to downstream processing circuit design.

- The HREO compositional profile is independently benchmarked against producing peers, not projected from geological inference.

- The strategic demand context is documented at the highest levels of US defence and industrial policy, not inferred from broader market trends.

The risk-adjusted framework looks like this: the downside case is a world-class rutile-graphite project with economics that stand independently on conservative assumptions. The upside case adds a third revenue stream carrying HREO ratios that no currently operating peer outside China can match. The path from the downside case to the upside case is defined, sequential, and measurable.

This article is for informational purposes only and does not constitute financial advice. Readers should conduct their own due diligence and consult a licensed financial adviser before making investment decisions. Forward-looking statements and scenario projections involve assumptions that may not be realised.

Want To Track The Next Major Mineral Discovery Before The Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time ASX alerts on significant mineral discoveries — including rare earth, critical mineral, and multi-commodity projects — instantly translating complex data into actionable insights for investors at every level. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.