July 21, 2026

The Midstream Problem That Has Held India's Clean Energy Ambitions Back

The global transition to clean energy has created an unexpected chokepoint, one that sits not in wind fields or battery chemistry laboratories, but in a narrow band of industrial processing infrastructure that most nations have never bothered to build. Rare earth permanent magnets, the invisible workhorses inside electric vehicle motors and wind turbine generators, require a manufacturing chain so technically demanding and capital-intensive that fewer than a handful of countries have successfully established it at commercial scale. China controls roughly 85-90% of global rare earth magnet production, a dominance built over decades of deliberate industrial policy, leaving technology-importing nations like India in a position of profound structural vulnerability.

For India, this vulnerability carries particular weight. The country has set ambitious targets across electric mobility, offshore and onshore wind energy, defence modernisation, and consumer electronics manufacturing. Every one of these sectors depends on a reliable supply of high-performance permanent magnets. Yet India currently imports virtually all of its finished magnet requirements, overwhelmingly from Chinese supply chains, creating a single point of failure across multiple strategic industries simultaneously. The announcement by critical minerals company Lohum on June 5, 2026, of a phased investment of up to ₹3,000 crore to establish the Lohum rare earth magnet plant in Uttar Pradesh marks a substantive attempt to address this vulnerability at its structural root.

Understanding why this matters requires examining not just the financial figures, but the technical architecture of what is being built, the industrial logic behind it, and the considerable challenges that still lie ahead.

When big ASX news breaks, our subscribers know first

Why India's Rare Earth Magnet Dependency Is Structurally Different From Other Import Risks

The Nature of the Dependency

India's reliance on imported rare earth permanent magnets differs fundamentally from typical commodity import dependencies, and this distinction is critical for understanding both the scale of the problem and the difficulty of solving it.

Most commodity dependencies can be partially mitigated through supplier diversification, strategic stockpiling, or demand-side efficiency improvements. Rare earth magnet dependency resists all three of these conventional responses. No commercially viable substitute currently exists for neodymium-iron-boron (NdFeB) magnets in high-performance electric motors and direct-drive wind generators. The physics of these applications demand specific magnetic flux densities and thermal stability characteristics that only rare earth permanent magnets can reliably deliver at the required performance thresholds.

The manufacturing process itself compounds this challenge. Furthermore, producing finished NdFeB magnets requires executing an integrated sequence of technically demanding stages, which touches on broader rare earth supply chains that remain highly concentrated:

-

Rare earth ore extraction and initial concentration

-

Oxide separation via solvent extraction (removing individual rare earth elements from mixed concentrates)

-

Reduction to rare earth metals under controlled atmospheric conditions

-

Alloy preparation combining neodymium, iron, and boron in precise proportions

-

Powder processing through hydrogen decrepitation and jet milling

-

Sintering or bonding at temperatures between 1,000-1,100°C under vacuum conditions

-

Post-sintering heat treatment to optimise magnetic properties

-

Magnetisation and finishing

Each of these stages requires distinct specialised infrastructure, process expertise, and quality control systems. India has historically possessed the raw material base for step one but lacked the integrated industrial infrastructure for steps two through eight. The result is that Indian manufacturers have been purchasing the finished product at the end of this chain rather than participating in any of its value-creating stages.

The Heavy Rare Earth Complication

A dimension of this dependency that receives insufficient attention is India's specific vulnerability around heavy rare earth elements, particularly dysprosium and terbium. These elements are added to NdFeB magnets in small quantities, typically 1-5% by weight, but they perform a critical function: they dramatically increase the magnet's coercivity, or resistance to demagnetisation at elevated temperatures. Without dysprosium additions, NdFeB magnets can lose their magnetisation in the operating temperature ranges experienced by electric vehicle motors under heavy load conditions.

Heavy rare earth elements like dysprosium are far scarcer than light rare earth elements such as neodymium, are geographically concentrated in specific deposit types, and are produced in significantly smaller quantities. China's dominance in heavy rare earth processing is even more pronounced than its dominance in light rare earth processing, creating a compounded dependency risk for high-performance magnet applications.

This technical reality means that India's rare earth magnet supply chain vulnerability is layered: dependency on imported finished magnets sits on top of a deeper dependency on imported heavy rare earth processing capability. China's export controls have further highlighted how this layered dependency can be weaponised, making any domestic magnet manufacturing initiative that addresses both layers essential for genuine supply chain resilience.

What the Lohum Rare Earth Magnet Plant in Uttar Pradesh Is Actually Building

Facility Specifications and Operational Scope

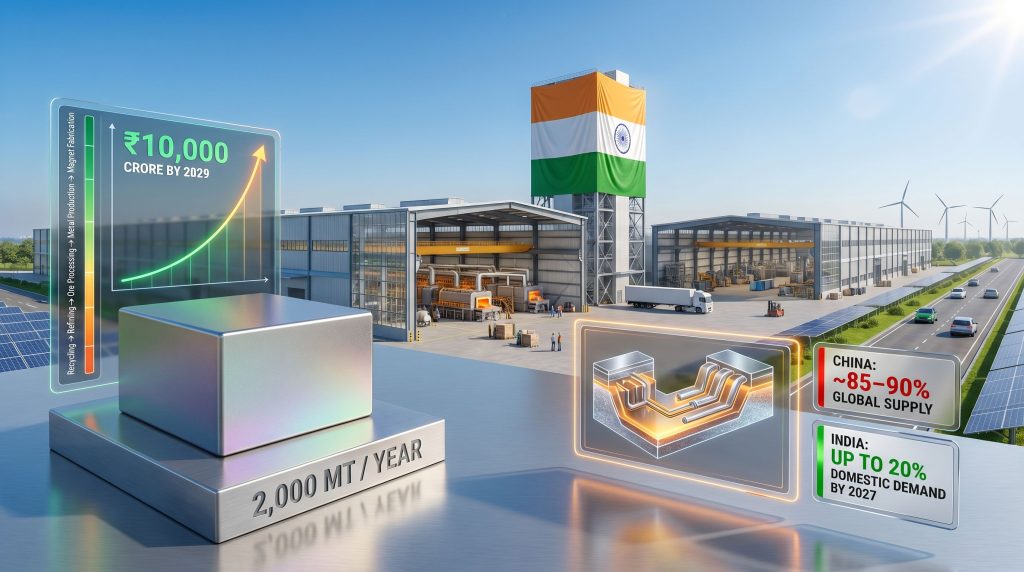

The Lohum rare earth magnet plant in Uttar Pradesh, situated on a 50-acre plot in Meerut allotted by the state government, is designed from the ground up as an end-to-end integrated processing and manufacturing hub rather than a partial-chain assembly operation. According to the official announcement reported by ET EnergyWorld, the facility is planned for an annual production capacity of 2,000 metric tonnes of rare earth magnets, with total investment of ₹2,500-3,000 crore to be deployed in phases through 2029.

| Parameter | Detail |

|---|---|

| Location | Meerut, Uttar Pradesh |

| Site Area | 50 acres |

| Annual Production Target | 2,000 metric tonnes |

| Total Planned Investment | ₹2,500-3,000 crore (phased to 2029) |

| Initial Capital Deployment | ₹500 crore |

| Revenue Target by 2029 | ₹10,000 crore |

| Projected Demand Coverage | Up to 20% of India's magnet demand by 2027 |

The facility's operational scope, as described by Lohum Founder and CEO Rajat Verma, spans the processing of rare earth ores, oxides, and scrap through to the production of rare earth metals and finished magnets. This full-chain integration is the defining characteristic that distinguishes the Meerut plant from previous Indian attempts at rare earth processing, which have typically addressed isolated segments of the value chain rather than the complete manufacturing sequence.

End Market Targeting

The Meerut facility is designed to serve five primary demand segments, each with distinct technical requirements. The surge in critical minerals demand across these sectors makes the timing of this investment particularly strategic:

-

Electric vehicles: Traction motors in passenger EVs, electric two-wheelers, and commercial electric vehicles represent the highest-volume growth opportunity, driven by India's accelerating EV adoption curve

-

Wind energy: Permanent magnet generators used in direct-drive offshore and onshore turbines, where magnet performance directly determines energy yield and maintenance intervals

-

Defence and aerospace: Guidance systems, precision actuators, electronic warfare equipment, and compact motor applications where supply sovereignty carries strategic importance

-

Consumer electronics: Hard disk drives, acoustic components, sensors, and miniaturised motors in devices where magnetic performance directly affects product quality

-

Energy storage systems: Auxiliary motor applications within grid-scale and distributed storage infrastructure, a segment expected to grow substantially as India's grid modernisation programme expands

The breadth of this end market targeting provides important revenue diversification, reducing dependence on any single sector's growth trajectory while positioning the facility to benefit from multiple simultaneous tailwinds in India's industrial development.

How Lohum's Recycling Heritage Creates a Structural Competitive Advantage

The Strategic Logic of Starting With Recycling

One of the less immediately obvious dimensions of Lohum's competitive positioning involves the strategic relationship between its existing battery recycling operations and its new rare earth magnet manufacturing ambitions. The company currently operates a battery recycling capacity of 25,000 metric tonnes annually, making it one of India's most significant processors of end-of-life lithium-ion batteries and electronics.

This recycling infrastructure creates a competitive advantage in magnet manufacturing that pure-play primary processors cannot easily replicate. The battery recycling process Lohum has developed enables recovery of rare earth materials — including spent NdFeB magnets that retain their rare earth content regardless of magnetic performance degradation. These secondary feedstocks can supplement primary ore inputs, providing a cost-effective and domestically sourced raw material stream that reduces exposure to volatile primary rare earth prices.

The company's planned expansion of refining operations across lithium, cobalt, nickel, aluminium, and copper reflects a broader strategic vision of becoming a comprehensive critical minerals processor rather than a single-material specialist. This multi-mineral approach creates operational synergies, as the chemical processing infrastructure required for rare earth separation shares fundamental engineering principles with the hydrometallurgical processing used in battery material refining.

The Five-Pillar Business Architecture

Lohum's transformation from battery recycling specialist to integrated critical minerals company follows a deliberate sequential logic:

-

Battery recycling (established core competency, 25,000 MT annual capacity)

-

Critical mineral refining (lithium, cobalt, nickel, aluminium, copper from recycled streams)

-

Rare earth ore and oxide processing (primary feedstock processing capability)

-

Rare earth metal production (reduction and alloy preparation)

-

Advanced magnet manufacturing (sintered and bonded magnet fabrication)

Each pillar builds on the technical and infrastructure foundations established by the preceding ones. The recycling operations provide both feedstock materials and hydrometallurgical processing expertise. The critical mineral refining capability develops the chemical separation skills transferable to rare earth oxide processing. The progression from oxide processing to metal production to finished magnets then follows a logical industrial scaling sequence.

This dual-input model, combining virgin rare earth ores and oxides with recycled magnet scrap as co-feedstocks, gives the Meerut facility a raw material flexibility that single-source processors cannot match. In volatile rare earth markets, this flexibility translates directly into cost resilience and supply continuity advantages.

The Policy Framework Enabling This Investment

India's National Critical Mineral Mission

India's National Critical Mineral Mission identifies rare earth elements as strategically essential inputs requiring domestic production capability. The policy framework supporting rare earth magnet manufacturing encompasses multiple instruments, including production-linked incentive frameworks for advanced materials, the Ministry of Heavy Industries' dedicated magnet production support scheme, and state-level industrial policy incentives.

It is important to note that while these policy frameworks create an enabling environment for investments of this nature, the specific government support received by Lohum for the Meerut project extends to land allocation by the Uttar Pradesh government, as confirmed in the official announcement. Investors and analysts should not assume that broader policy frameworks automatically translate into project-specific financial or regulatory support beyond what has been explicitly disclosed.

Why Meerut and Why Uttar Pradesh

The selection of Meerut in Uttar Pradesh as the facility location reflects a convergence of industrial policy and locational logic. The UP government's allotment of a 50-acre plot reflects the state's active industrial attraction strategy, while Meerut's specific geography provides tangible operational advantages:

-

Proximity to the Delhi NCR industrial corridor and its dense network of EV and electronics manufacturers

-

Established road and rail connectivity enabling efficient inbound raw material logistics and outbound distribution

-

Access to a substantial skilled engineering workforce pool from educational institutions across the NCR region

-

Competitive industrial land pricing relative to alternative manufacturing hubs in Maharashtra or Tamil Nadu

India's Raw Material Endowment: The Underutilised Foundation

A critical contextual factor is that India possesses substantial domestic rare earth reserves managed through IREL (India Rare Earths Limited). The country holds approximately 6.9 million tonnes of rare earth oxide equivalent reserves, representing roughly 6% of global resources, concentrated primarily in monazite-bearing coastal placer deposits in Kerala, Tamil Nadu, Odisha, and Andhra Pradesh. These reserves have historically been significantly underutilised due precisely to the absence of midstream processing infrastructure of the type Lohum is now attempting to build.

The Meerut facility, if it successfully establishes ore and oxide processing capability, creates a potential demand anchor for India's upstream rare earth mining sector, potentially catalysing a broader development of the domestic rare earth value chain extending from mine to magnet.

Decoding the ₹10,000 Crore Revenue Target

Financial Architecture and Growth Assumptions

The ₹10,000 crore revenue target by 2029 is a forward-looking projection that deserves careful contextual analysis. At 2,000 metric tonnes of annual production capacity and current global NdFeB magnet pricing of approximately USD 35-45 per kilogram for sintered grades, the production value of a fully utilised facility would be in the range of ₹5,800-7,500 crore annually from magnet sales alone. The ₹10,000 crore target therefore implies either premium product pricing, higher capacity utilisation than the headline figure suggests, or a substantial contribution from the company's broader refining and recycling operations.

This projection should be treated as a management aspiration rather than a financial forecast. Multiple execution risks remain between current status and the 2029 target, including ramp-up timelines, offtake agreement development, technical yield optimisation, and raw material supply chain establishment.

The phased capital deployment structure provides important risk management benefits:

-

Initial ₹500 crore funds foundational facility construction and early-stage production capability

-

Subsequent tranches can be calibrated to actual production ramp-up progress, reducing capital at risk in early phases

-

The 2029 completion timeline allows for iterative technical optimisation as each processing stage is commissioned and refined

Regional Comparison: Contextualising the Investment Scale

| Initiative | Investment Scale | Capacity Focus | Status |

|---|---|---|---|

| Lohum, India (Meerut) | ~USD 300-360M | 2,000 MT/year finished magnets | Announced June 2026 |

| MP Materials, USA | ~USD 700M | NdFeB alloy production | Commissioning phase |

| Lynas Rare Earths, Malaysia | ~AUD 500M+ | Oxide processing | Operational and expanding |

| China (aggregate capacity) | Multi-billion USD | 200,000+ MT/year | Established dominant position |

Note: Figures are approximate and drawn from publicly available industry reporting. Comparisons should account for differing production stages, product types, and cost structures across geographies.

The Meerut investment is modest relative to the capital deployed by established Western rare earth processing initiatives, which reflects both the earlier stage of India's industrial development in this sector and the lower capital cost environment of Indian manufacturing. However, the end-to-end integration ambition of the Meerut facility arguably represents greater strategic value per rupee invested than facilities focused on single-stage processing, because it addresses the complete value chain gap rather than incrementally expanding one segment of it.

The next major ASX story will hit our subscribers first

Technical and Operational Challenges That Will Determine Success

Where the Real Complexity Lies

Several technical and operational challenges will determine whether the Meerut facility achieves its production and revenue targets. Investors and industry observers should monitor these specific risk factors:

Solvent extraction scaling: The separation of individual rare earth elements from mixed oxide concentrates requires solvent extraction circuits that are notoriously difficult to scale and optimise. Achieving consistent separation efficiencies at 2,000 MT annual output will require significant process engineering expertise, likely necessitating technology partnerships with experienced processors.

Heavy rare earth processing capability: Achieving high-coercivity magnet grades suitable for premium EV applications requires successful processing of dysprosium and terbium, which demand more sophisticated separation chemistry than the lighter rare earth elements. The absence of domestic heavy rare earth processing infrastructure in India means this capability will need to be built largely from scratch.

Sintering yield optimisation: NdFeB magnet sintering is a precision process where small variations in temperature profiles, atmosphere control, and powder preparation can significantly impact magnetic properties and production yields. Achieving commercially viable yields at scale typically requires 12-24 months of process optimisation after initial commissioning.

Workforce development: Rare earth metallurgy is a highly specialised discipline with extremely limited domestic training infrastructure in India. Recruiting and retaining qualified process metallurgists, chemical engineers, and magnet production specialists will represent a sustained operational challenge throughout the ramp-up phase.

Offtake security: Without binding long-term supply agreements with EV manufacturers or wind energy developers, revenue projections remain uncertain regardless of production capability. Establishing commercial relationships with major domestic offtakers will be as critical to the facility's success as its technical performance.

Import dependency during ramp-up: Until domestic ore processing is fully operational, the facility will likely depend on imported rare earth oxides as feedstock, partially replicating the supply chain vulnerability it is designed to address. The timeline for transitioning from imported oxide inputs to domestically processed materials will be a key indicator of genuine supply chain independence.

The Strategic Significance of India's First Integrated Rare Earth Magnet Plant

Closing the Midstream Gap

India's critical minerals challenge has never been fundamentally about resource scarcity. The country possesses meaningful rare earth reserves, and its recycling infrastructure has been growing steadily. The structural problem has always been the absence of midstream processing and manufacturing capability connecting these upstream resources to downstream technology manufacturing demand. The Lohum rare earth magnet plant in Uttar Pradesh represents a targeted intervention at precisely this midstream bottleneck, with significant energy security implications for the country's broader industrial strategy.

If the Meerut facility executes successfully, its effects will extend well beyond its own production volumes. A demonstrated domestic rare earth magnet manufacturing capability creates a reference facility and talent base from which additional capacity can be scaled. It establishes procurement relationships with domestic rare earth miners and oxide processors. It develops a specialised workforce that can support future capacity expansion. Furthermore, it provides EV manufacturers and wind energy developers with proof of concept for domestic sourcing, creating the commercial confidence necessary for long-term offtake commitments.

Implications for India's Clean Energy Sectors

The clean energy sectors most directly affected by domestic magnet supply availability would experience tangible operational benefits if the Meerut facility achieves its targets:

-

EV manufacturers gain partial insulation from international rare earth price cycles, with domestic procurement reducing foreign exchange exposure on a cost component that can represent 8-12% of motor manufacturing costs

-

Wind energy developers gain access to shorter supply chains with reduced lead times, simplifying project planning and reducing inventory carrying requirements for large-scale turbine installations

-

Defence procurement benefits from a sovereign supply source for a component category previously identified in official assessments as a critical strategic vulnerability

India as a Regional Magnet Supplier: A Speculative But Plausible Trajectory

Looking beyond the 2029 target horizon, a successfully operating Meerut facility could serve as the foundation for positioning India as a regional rare earth magnet supplier to Southeast Asian and potentially Middle Eastern markets by the early 2030s. This trajectory would require sustained execution against technical and commercial milestones, continued policy support for the broader critical minerals ecosystem, and the development of competitive cost structures relative to established Asian producers.

This represents a speculative projection that depends on numerous execution assumptions. It is not an established industry forecast and should be interpreted as a potential long-term scenario rather than a probable near-term outcome.

What is less speculative is the structural logic of the attempt. India's combination of raw material reserves, a growing domestic technology manufacturing base, cost-competitive engineering talent, and an increasingly sophisticated policy framework for critical minerals creates legitimate conditions for building genuine rare earth processing capability. The Lohum rare earth magnet plant in Uttar Pradesh is the most ambitious step yet taken to translate these conditions into operational industrial reality.

Disclaimer: This article contains forward-looking statements, financial projections, and speculative assessments that are based on publicly available information and independent analysis. These projections are not investment advice and should not be relied upon as forecasts of actual financial or operational outcomes. Readers should conduct independent due diligence before making any investment decisions related to companies or sectors discussed in this article.

Want To Identify The Next Major Critical Minerals Discovery Before The Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across rare earths, critical minerals, and the commodities powering India's clean energy ambitions — instantly translating complex geological data into actionable investment insights. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.