July 10, 2026

The World's Most Irreplaceable Energy Corridor Is Under Pressure Again

Every few years, global energy markets are reminded of a structural vulnerability they cannot engineer their way out of: the Strait of Hormuz. Unlike supply disruptions caused by weather events, equipment failures, or policy shifts, a Hormuz disruption is uniquely resistant to rapid mitigation. There is no pipeline large enough, no alternative route cheap enough, and no strategic reserve deep enough to fully absorb a prolonged closure. This is what makes the cautious return of LNG tankers to the Strait of Hormuz in July 2026 both a relief and a warning.

The situation is not simply about ships turning around and then turning back. It is about what this cycle of withdrawal and hesitant re-entry reveals regarding the fragility of the LNG supply outlook, the decision-making calculus of commercial shipping operators under live threat conditions, and the long-term structural consequences for energy importers whose entire industrial and residential energy systems depend on uninterrupted seaborne gas deliveries.

When big ASX news breaks, our subscribers know first

Why the Strait of Hormuz Has No Real Substitute

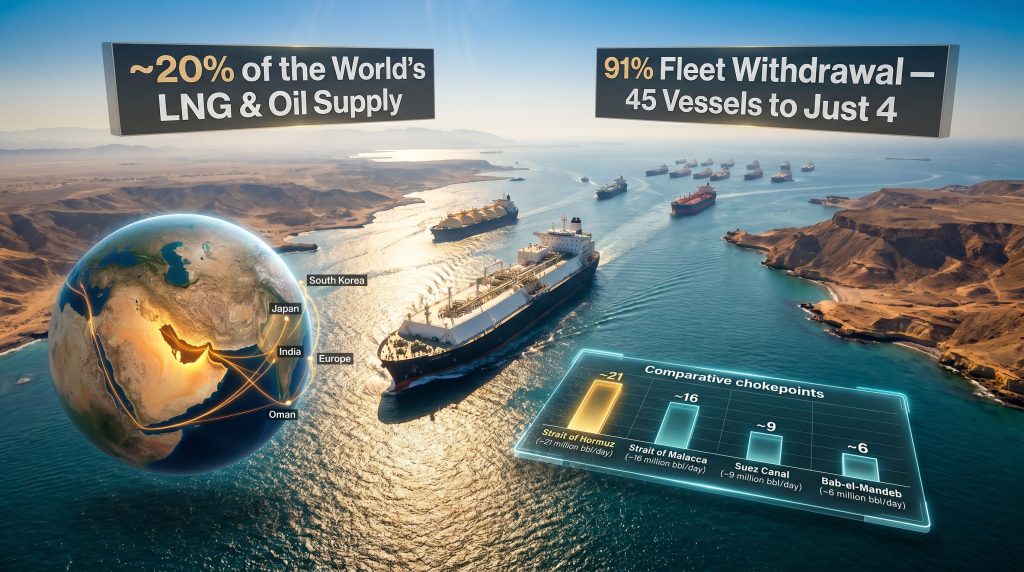

Geography has given the Strait of Hormuz an energy significance that no other maritime passage can match. Connecting the Persian Gulf to the Gulf of Oman and ultimately to the Indian Ocean and global trade lanes, the strait handles approximately 20% of the world's total LNG and crude oil supply on an annual basis. Qatar's Ras Laffan terminal, the largest LNG export facility on the planet, depends entirely on this corridor for outbound cargo movements.

What separates the Strait of Hormuz from other chokepoints is the near-total absence of a workable bypass for LNG carriers. The comparison below illustrates the structural difference in substitutability across the world's major energy chokepoints:

| Chokepoint | Daily Energy Volume (approx.) | Practical Alternate Route | Effective Bypass for LNG? |

|---|---|---|---|

| Strait of Hormuz | ~21 million bbl/day oil equivalent | Abu Dhabi Crude Oil Pipeline (crude only) | No |

| Strait of Malacca | ~16 million bbl/day oil equivalent | Lombok or Sunda Strait | Partial |

| Suez Canal | ~9 million bbl/day oil equivalent | Cape of Good Hope | Yes (costly) |

| Bab-el-Mandeb | ~6 million bbl/day oil equivalent | Cape of Good Hope | Yes (costly) |

The Abu Dhabi Crude Oil Pipeline can redirect a portion of crude oil production away from the Gulf, but it handles crude only. LNG carriers, given their size, specialised cargo containment systems, and operational constraints, have no equivalent rerouting option. This makes the economics of any Hormuz closure uniquely punishing for gas-dependent economies.

Critical structural point: The Strait of Hormuz is not just important because of the volume of energy it carries. It is important because it is genuinely irreplaceable for LNG logistics at any commercially viable cost. This asymmetry between risk and substitutability is what gives Iran significant geopolitical leverage over global energy markets.

Reconstructing the July 2026 Disruption: What Actually Happened

The Sequence That Triggered the Retreat

On Tuesday, July 8, 2026, Iranian missile activity in the region caused damage to a Qatari-flagged LNG tanker and a Saudi-flagged crude oil carrier operating near the strait. Maritime threat classifications were immediately escalated to "severe", the highest operational risk designation used by commercial shipping risk assessors.

The response from vessel operators was swift and telling. Three QatarEnergy LNG carriers — the Al Ghariya, Duhail, and Al Ruwais — reversed their inbound courses while travelling empty toward Ras Laffan to collect cargo. An Indian-flagged very large crude carrier, the Lila Vadinar, which had been transporting Kuwaiti crude oil, executed a course reversal off the tip of Oman on Wednesday, July 9, further confirming the breadth of the shipping community's response.

By Friday, July 10, 2026, ship-tracking data from Kpler and LSEG indicated that at least five ballast LNG carriers had re-entered the strait. This represented a cautious resumption rather than a normalisation, with operators prioritising empty vessel transits to assess conditions before committing laden cargo ships.

Japan's Fleet Withdrawal: A Metric Worth Understanding

Perhaps no single data point captures the severity of the disruption more precisely than the dramatic contraction in Japan-linked shipping activity. According to the Japanese Shipowners' Association, the Gulf presence of Japanese-affiliated vessels dropped from 45 ships carrying approximately 1,100 crew members at the onset of hostilities to just 4 vessels with roughly 100 crew members by early July 2026.

That represents a reduction of more than 91% in vessel count and a near-equivalent contraction in crew exposure, achieved within days of the initial incident.

This scale of withdrawal by a single major maritime nation within such a compressed timeframe is highly unusual and reflects just how seriously Japanese shipping operators assessed the live threat environment. It will almost certainly become a reference benchmark for industry-wide crew evacuation thresholds in future conflict scenarios.

How Shipping Operators Are Making Transit Decisions Under Threat

The Multi-Variable Risk Framework Governing Each Voyage Decision

Commercial shipping operators are not making simple binary decisions about whether to transit or avoid the strait. Each voyage decision involves layered risk assessments across at least five distinct variables:

-

Vessel load status (laden vs. ballast): An empty carrier still exposes hull and crew to missile or drone attack, but eliminates the financial catastrophe of cargo loss aboard a laden LNG vessel carrying potentially tens of millions of dollars in cargo.

-

Proximity to Iranian-controlled territorial waters: Iran has issued navigational directives requiring commercial vessels to adhere to specific corridors near its coastline, creating implicit compliance costs even for vessels that ultimately do transit.

-

Charter party and contractual obligations: Shipping operators face meaningful financial penalties for non-delivery under long-term supply contracts. This creates a financial pull toward resuming transits even when threat levels remain elevated.

-

War risk insurance premium escalation: Surcharges applied to Gulf-transiting vessels have surged significantly during the disruption period, materially altering the voyage economics calculation for every operator considering a transit.

-

Flag state guidance and formal advisories: Japan, South Korea, and India have each issued formal guidance to their flagged and affiliated vessels, creating a compliance layer on top of commercial risk assessments.

What the Ballast-First Re-Entry Strategy Signals

The deliberate sequencing of ballast (empty) transits before any resumption of laden cargo movements is not accidental. It reflects a structured operational protocol that the industry informally describes as route stress-testing under live conditions. Operators are, in effect, sending vessels with reduced financial exposure through the corridor first to validate that the threat level has declined sufficiently to justify committing high-value LNG cargoes.

A cluster of empty LNG carriers observed gathering in waters near Ras Laffan during this period confirms that significant export capacity is staged and ready to move. The constraint is not logistics or cargo availability. It is operator confidence in the security environment. Furthermore, more LNG tankers have gradually slipped through the strait as conditions have shown tentative signs of stabilising.

Mapping Import Dependency: Which Countries Face the Greatest Exposure

| Country | Estimated LNG Import Share via Hormuz | Primary Supplier Exposure | Approximate Strategic Reserve Buffer |

|---|---|---|---|

| Japan | ~25-30% | QatarEnergy, Abu Dhabi | ~90-100 days |

| South Korea | ~20-25% | QatarEnergy | ~60-80 days |

| India | ~15-20% | QatarEnergy, Oman LNG | ~30-45 days |

| China | ~10-15% | QatarEnergy | Variable |

| European Union | ~8-12% | QatarEnergy (via re-export) | ~60-90 days |

Why Japan's Structural Vulnerability Is Categorically Different

Japan occupies a uniquely exposed position among major LNG importers. With virtually no domestic oil or gas production at commercial scale, every disruption to seaborne LNG supply translates almost immediately into procurement stress for utilities and industrial users. There is no domestic backstop, no pipeline connection to continental supply networks, and no meaningful indigenous energy buffer.

Japan's government has long maintained deliberate supply diversification architecture across three primary corridors: Qatari and UAE volumes via the Gulf, Australian LNG from the Pacific Basin, and US LNG from the Gulf of Mexico. However, even with this diversification strategy, the Strait of Hormuz still accounts for a material share of Japan's total LNG import mix, making any prolonged disruption a direct threat to energy security.

Three Scenarios for How This Disruption Resolves

Scenario 1: Controlled Re-Opening (Base Case)

Diplomatic channels reduce the intensity of active hostilities within two to four weeks. LNG traffic resumes incrementally, with outbound laden cargoes from Ras Laffan being prioritised. A short-term LNG spot price premium in the range of 10-20% dissipates over 30 to 45 days as supply flows normalise. Japanese and South Korean utilities draw on strategic reserves to bridge the gap without triggering emergency procurement.

Scenario 2: Prolonged Disruption (Elevated Risk Case)

Hostilities persist for six to twelve weeks, with periodic vessel incidents sustaining the severe threat classification. QatarEnergy is compelled to invoke force majeure on a portion of contracted LNG deliveries. European importers compete aggressively for Atlantic Basin supply, pushing spot prices sharply higher. The oil market disruption compounds these pressures, as non-Gulf shipping routes experience freight rate surges and vessels are redirected across multiple commodity classes, further straining global trade war impacts on already fragile energy supply chains.

Scenario 3: Full Strait Closure (Tail Risk)

A deliberate Iranian blockade or sustained mining operation closes the strait to all commercial traffic. Global LNG markets face a supply shock potentially affecting 4-5% of total traded volumes. Emergency coordination mechanisms through the International Energy Agency are activated alongside strategic petroleum reserve releases. This scenario would likely serve as a long-term catalyst for accelerated LNG import infrastructure investment entirely outside the Gulf corridor.

Investor and analyst note: Even if Scenario 1 prevails, the downstream consequences for long-term LNG contract structuring, fleet positioning protocols, and supply diversification investment will be lasting. The July 2026 disruption cycle has already altered how LNG buyers think about counterparty risk in Gulf-dependent supply chains.

The next major ASX story will hit our subscribers first

Iran's Calibrated Use of Maritime Pressure as Geopolitical Leverage

The Pattern Behind the Incident

The July 2026 events did not occur in isolation. Iran has periodically leveraged its geographic control over the northern shore of the Strait of Hormuz as a strategic tool, with documented incidents of vessel seizures, drone attacks, and navigational interference across multiple periods of heightened regional tension. The issuance of directives requiring commercial vessels to use specific transit corridors near Iranian waters functions as a form of soft blockade, imposing compliance costs and war risk premium burdens on operators without formally closing the strait.

This approach is deliberately calibrated. A full closure of the strait would invite unified international military response and severe economic consequences for Iran itself, which also depends on Gulf waters for portions of its own energy export activity. The more strategically useful instrument is controlled threat escalation: maintaining uncertainty at a level that forces shipping operators to price in risk, raises global energy costs, and creates diplomatic leverage without crossing the threshold that would trigger an overwhelming military response.

The US Military Dimension

The US Fifth Fleet, operating out of Bahrain, maintains a continuous naval presence in the Persian Gulf specifically designed to deter interference with commercial shipping. US retaliatory strikes on Iranian targets following vessel attacks represent a significant escalation threshold — one that all commercial shipping operators must factor into their forward risk models. The dynamic interaction between US military posture and Iranian responses creates a security environment that is structurally difficult to price into long-term shipping contracts or LNG supply agreements.

Long-Term Structural Consequences: Supply Chain Diversification Accelerates

The Alternative Supply Corridors Gaining Strategic Importance

The July 2026 disruption adds measurable urgency to a supply diversification trend that was already underway across major LNG importing nations. Three alternative supply corridors are positioned to benefit from accelerated long-term contracting activity:

-

US LNG (Gulf of Mexico corridor): Terminals including Sabine Pass, Corpus Christi, and the emerging Plaquemines LNG facility represent the most significant structural alternative to Middle Eastern supply for Asian buyers. US LNG carries no Hormuz transit exposure and benefits from a fundamentally different geopolitical risk profile.

-

Australian LNG (Pacific Basin corridor): Projects including Ichthys, Gorgon, Wheatstone, and the North West Shelf offer a lower geopolitical risk Pacific Basin supply corridor that is structurally advantaged for Japan and South Korea given proximity and existing long-term contract relationships.

-

East African LNG (longer-dated option): Mozambique and Tanzania represent meaningful future supply sources, though infrastructure development timelines push material volume contributions well into the early-to-mid 2030s at the earliest.

Operational Protocols That Are Likely to Change Permanently

Beyond supply diversification at the macro level, the July 2026 disruption is already influencing how shipping operators think about fleet management and risk protocols at the operational level. In addition, crude oil price trends across global benchmarks have responded sharply to the uncertainty, reflecting how deeply interconnected LNG and crude markets remain under conditions of simultaneous supply stress.

-

War risk insurance architecture: Operators are reassessing how war risk coverage triggers are defined and how premium costs are pooled and allocated across fleets operating in geopolitically sensitive regions.

-

Crew safety and evacuation thresholds: The documented reduction in Japanese crew exposure from approximately 1,100 to just 100 individuals within days of the initial incident will likely become an industry reference point for how quickly and at what threat threshold crew evacuation protocols should be activated.

-

Ballast transit staging as standard protocol: The practice of deliberately staging empty vessels outside the strait to assess conditions before committing laden cargo movements may evolve from an improvised crisis response into a formalised pre-transit risk assessment standard.

Frequently Asked Questions

What are ballast LNG carriers and why does their return matter?

A ballast LNG carrier is a tanker travelling empty, without cargo, typically returning to a loading terminal to collect a new shipment. Their significance in the current context is that operators sent these lower-financial-exposure vessels through the strait first, as a deliberate risk-testing strategy before committing laden cargo ships carrying tens of millions of dollars in LNG.

Why can't LNG carriers simply use an alternative route?

LNG carriers are large, specialised vessels with fixed operational constraints. Unlike crude oil, which can partially bypass the Strait of Hormuz via the Abu Dhabi Crude Oil Pipeline, LNG has no equivalent overland bypass infrastructure. The only alternative for LNG would be sourcing supply from non-Gulf producers entirely, which cannot be arranged at short notice given long-term contract structures and infrastructure limitations.

How does a Hormuz disruption affect LNG spot prices?

Supply tightening through the Strait of Hormuz typically generates an immediate premium in LNG spot markets as buyers scramble to secure alternative cargoes. The magnitude and duration of price impact depends on how long the disruption persists, the volume of strategic reserves held by importing nations, and the speed with which Atlantic Basin producers can redirect additional supply toward displaced Asian buyers.

What does force majeure mean in the context of LNG contracts?

Force majeure is a contractual clause that allows a party to suspend delivery obligations when circumstances beyond their reasonable control prevent performance. In the LNG context, a severe Hormuz disruption could allow producers like QatarEnergy to invoke force majeure on contracted deliveries, shifting the cost and procurement burden onto importing utilities without the normal contractual penalty structures applying.

What This Moment Reveals About Global Energy Security

The gradual return of LNG tankers to the Strait of Hormuz following the July 2026 disruption offers a deceptively reassuring signal. Traffic is moving again, but the conditions that created the disruption remain unresolved. Iran retains the geographic and strategic capacity to interfere with commercial shipping. War risk insurance premiums remain elevated. Japanese and other Asian utilities are drawing on strategic reserves rather than relying on normalised supply flows.

The deeper lesson is structural: global LNG supply chains have been constructed around a corridor that cannot be adequately replicated or bypassed at any commercially viable cost. Consequently, global industrial demand patterns across Asia's manufacturing and energy-intensive sectors will remain highly sensitive to any recurrence of Hormuz instability. The geopolitical risk attached to that corridor is not trending downward.

The most durable response available to importing nations is long-term supply diversification combined with deeper strategic reserve investment, not simply hoping that each successive Hormuz disruption resolves quickly enough to avoid lasting economic damage. For investors, energy analysts, and policymakers monitoring LNG tanker movements and strait security conditions, the July 2026 cycle is not an isolated event. It is the latest iteration of a recurring structural vulnerability that will continue to shape global energy security strategy for decades.

Want to Stay Ahead of the Next Major Resource Discovery Triggered by Energy Market Disruption?

When geopolitical shocks like the Strait of Hormuz disruption ripple through global commodity markets, the opportunities for informed investors can emerge rapidly — Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex data into actionable insights so subscribers are never caught flat-footed. Explore historic discoveries and their remarkable returns to understand the scale of opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.