June 23, 2026

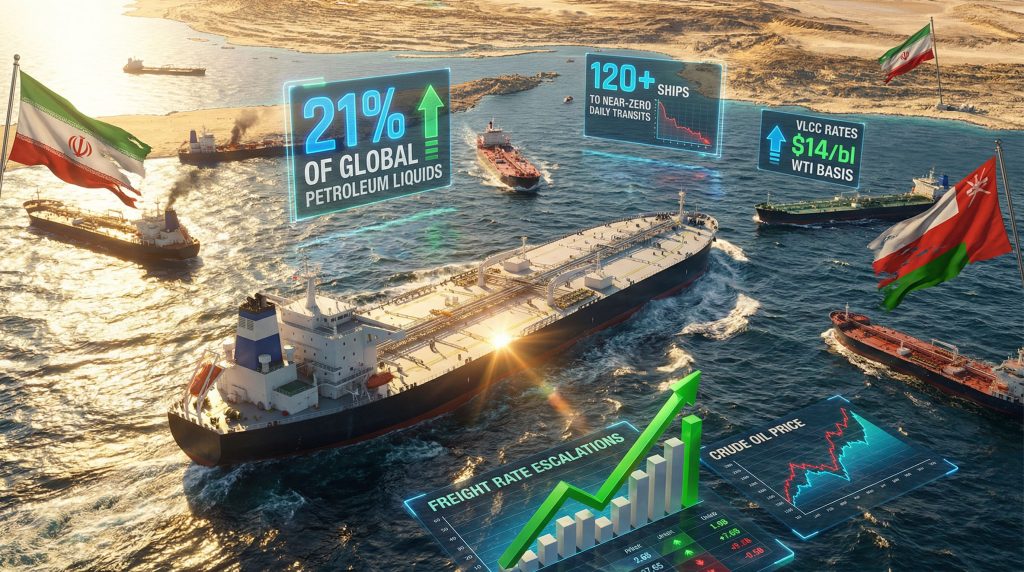

The strait of hormuz squeeze lifts us crude freight rates to unprecedented levels as global energy markets grapple with supply chain disruptions that have fundamentally altered transportation economics. When approximately 21% of global petroleum liquids become inaccessible through traditional routing, market participants face immediate rebalancing pressures that create both opportunities and constraints across the energy sector. Furthermore, these disruptions reveal underlying structural vulnerabilities while simultaneously highlighting the resilience mechanisms built into global commodity trading systems.

Maritime transportation systems for crude oil have evolved around predictable routing patterns developed over decades. However, geopolitical events can instantly transform established trade flows, forcing market participants to navigate unfamiliar supply chain configurations under extreme time pressure. Understanding these dynamics becomes essential for comprehending how energy markets respond to systemic shocks and oil price movements during crisis periods.

Critical Chokepoint Economics: Understanding Maritime Disruption Mechanics

Maritime chokepoints represent single points of failure in global energy supply chains, where geographic constraints concentrate massive commodity flows through narrow passages. When the Strait of Hormuz becomes restricted, its closure creates immediate supply rebalancing pressures across alternative routes and crude oil sources, triggering cascading effects throughout the global energy system.

Immediate Infrastructure Impact Assessment

The disruption metrics reveal the scope of market dislocation across multiple dimensions. According to Argus Media's latest market analysis, the strait of hormuz squeeze lifts us crude freight rates to historic highs as traditional shipping patterns collapse entirely.

The immediate infrastructure impact includes:

- Daily vessel transits: Collapsed from 120+ ships to near-zero operations

- VLCC fleet impact: Approximately 8% of global very large crude carriers trapped in restricted zones

- Container capacity affected: 0.6% of global fleet (roughly 100 vessels) repositioned

- Regional crude flows disrupted: 277,000 barrels per day from Middle East Gulf to US Gulf Coast eliminated

These figures demonstrate how chokepoint closures create bottlenecks that extend far beyond the immediate geographic area. Market intelligence platform Vortexa tracked these specific flow disruptions from November 2025 to February 2026, highlighting the sustained nature of supply chain reconfigurations during extended crisis periods.

Strategic Supply Route Alternatives

When traditional routing becomes unavailable, energy traders must identify alternative supply corridors within days rather than months. The trade war impact on oil markets compounds these challenges by creating additional political constraints on available alternatives.

The primary alternatives include:

West African Routes

- Extended voyage distances to Asia-Pacific markets

- Limited spare capacity for rapid deployment

- Higher insurance and operational costs

North American Corridors

- US Gulf Coast production mobilisation

- Alaska North Slope export acceleration

- Trans-Pacific shipping route development

Russian Alternative Pathways

- Constrained by existing geopolitical factors

- Limited flexibility for rapid volume increases

- Complex sanctions navigation requirements

Latin American Routes

- Restricted volumes available for immediate redeployment

- Infrastructure limitations for large-scale expansion

- Geographic disadvantages for Asian markets

When big ASX news breaks, our subscribers know first

US Crude Freight Rate Escalation: Market Mechanisms and Drivers

The transformation of US crude export dynamics during Middle Eastern supply disruptions follows predictable economic patterns, though the magnitude and speed of change often exceed historical precedents. Multiple interconnected factors drive freight rate increases, creating compounding effects across the energy transportation sector.

Demand Substitution Economics

Immediate Buyer Repositioning

When Middle Eastern crude becomes inaccessible, global refiners pivot toward North American alternatives within days. This substitution effect particularly benefits light sweet WTI crude as refiners seek replacements for Middle Eastern grades in Asia-Pacific facilities. A Japanese refiner recently secured 2 million barrels of WTI for June delivery, demonstrating the urgency driving these procurement decisions.

Crude Specification Flexibility

US light sweet WTI has emerged as a substitute for Abu Dhabi's light sour Murban at Asia-Pacific refineries, indicating that specification requirements become more flexible during supply emergencies. Refiners traditionally optimise crude slates for maximum economic returns, but supply security concerns override these considerations during crisis periods.

Vessel Repositioning Dynamics

Fleet Reallocation Mechanics

The effective closure of Hormuz forces tanker operators to redeploy vessels from traditional Middle East-Asia routes to US Gulf-Asia corridors. This repositioning creates temporary capacity constraints on US export routes despite global tanker overcapacity from post-COVID shipbuilding programmes.

VLCC Rate Escalation

US Gulf Coast to China VLCC rates reached approximately $14 per barrel on a WTI basis, representing nearly double week-over-week increases. These rates achieved the highest levels since systematic tracking began in 2012, indicating unprecedented demand for trans-Pacific crude transportation capacity.

Insurance Market Complications

War risk insurance costs for Middle Eastern transits have reached levels that make US crude exports comparatively attractive despite higher freight expenses. The Joint War Committee's ongoing risk assessments continue influencing global shipping calculations, though specific premium escalation data requires insurance market verification.

Comparative Economics

At $14 per barrel freight rates, US Gulf WTI becomes less competitive on a delivered basis, yet Asian refiners must evaluate total supply security rather than purely economic metrics. The calculation involves crude price differentials, freight costs, insurance premiums, and strategic supply diversification benefits.

Regional US Crude Grade Performance Analysis

Different crude grades respond uniquely to supply disruption scenarios based on their specifications and traditional export patterns. Understanding these responses provides insight into refinery substitution preferences and regional supply chain flexibility, particularly as the oil price rally continues gathering momentum.

Gulf Coast Crude Market Dynamics

Mars Crude Premium Surge

Deepwater Mars crude surged to a six-year high premium to WTI, reflecting its direct substitutability with Middle Eastern medium sour grades. Mars specifications closely match the density and sulphur content requirements of refineries traditionally supplied from the Persian Gulf region.

| US Gulf Coast Crude Performance | ||

|---|---|---|

| Crude Grade | Price Impact | Key Market Drivers |

| Mars (Medium Sour) | Six-year premium high to WTI | Direct substitute for Middle Eastern medium sour grades |

| WTI (Light Sweet) | $90+ breakthrough achieved | Asian refiner demand replacing Murban supplies |

| Heavy Louisiana Sweet | Premium expansion noted | European refiner substitution requirements |

WTI Market Breakthrough

April Nymex WTI achieved $90.13 per barrel by 12:00 PM ET on March 6, 2026, representing a $9.12 per barrel increase from the previous day's settlement. This $23 per barrel weekly increase (35% gain) demonstrates the rapid price response to supply constraint scenarios.

Alaska North Slope Market Transformation

Record Price Achievement

Alaska North Slope (ANS) crude delivered prices reached record levels as Asia-Pacific refiners sought medium sour alternatives. Multiple May-arrival cargoes traded around an $8.30 per barrel premium to July ICE Brent on a cost, insurance, and freight (CIF) US west coast basis.

This pricing represents an $8.10 per barrel increase above final April cargoes and marks the highest level since assessment tracking began in January 2018. These transactions occurred at approximately $20.00 per barrel premiums to front-month Dubai assessments on a delivered basis.

Jones Act Fleet Constraints

The specialised US-flagged tanker fleet serving domestic ANS distribution faces competing demands from trans-Pacific export opportunities. This constraint creates domestic supply tightness while supporting higher delivered prices as vessels potentially redirect to Asian markets rather than traditional California and Washington destinations.

Pacific Basin Supply Tightness

ANS represents one of the readily available medium sour spot grades in the Pacific basin, making additional Asian demand particularly impactful on west coast availability. South Korean and Japanese buyers actively sought alternative supplies to replace Middle Eastern imports effectively cut off by regional conflicts.

VLCC Rate Analysis: Historic Escalation Factors

Very Large Crude Carrier (VLCC) freight rates have reached levels unseen in over a decade of systematic tracking, reflecting fundamental supply-demand imbalances in specialised shipping capacity. These rate increases occur despite theoretical global tanker overcapacity, highlighting how effective capacity differs significantly from total fleet availability.

Capacity Utilisation Paradox

Theoretical vs. Effective Capacity

Despite global tanker overcapacity resulting from post-COVID shipbuilding programmes, effective available capacity has contracted sharply due to:

- Vessel Entrapment: Ships trapped in Persian Gulf requiring complex repositioning operations

- Insurance Restrictions: Coverage limitations reducing operational flexibility for specific routes

- Extended Voyage Distances: Route diversions increasing transit times and reducing vessel turnover

- Crew and Fuel Considerations: Higher operational costs for alternative routing patterns

Rate Structure Analysis

VLCC capacity typically ranges from 280,000-320,000 deadweight tons, with a 2-million-barrel cargo incurring approximately $28 million in freight costs per voyage at current $14 per barrel rates. Voyage times from US Gulf to China span approximately 20-25 days, creating significant capital commitment requirements.

Market Structure Implications

Historical Context

The $14 per barrel freight rate represents the highest level since systematic route tracking commenced in 2012, providing 14 years of comparative data for analysis. Previous rate spikes typically lasted weeks rather than months, but current geopolitical uncertainties suggest potentially extended elevation periods.

Supply Chain Bottlenecks

Freight rate escalation creates compounding effects throughout energy supply chains. Higher transportation costs reduce crude oil competitiveness on delivered bases while simultaneously encouraging supply source diversification to reduce dependency on volatile shipping routes.

Strategic Supply Chain Rebalancing: Long-term Market Evolution

Energy market disruptions often accelerate structural changes that might otherwise develop gradually over years. Current supply chain reconfigurations may establish lasting trade relationships extending beyond immediate crisis periods, fundamentally altering global energy flow patterns as the US oil production decline creates additional market dynamics.

Trans-Pacific Corridor Development

Relationship Acceleration

The crisis accelerates development of US-Asia crude trade relationships through forced market making. Japanese and South Korean refiners establishing direct procurement relationships with US producers create potential for sustained trade flows even after traditional Middle Eastern supplies resume normal operations.

Infrastructure Investment Justification

Sustained high freight rates may justify investments in expanded US export terminal capacity, specialised tanker fleet development for trans-Pacific routes, and alternative pipeline infrastructure reducing maritime transportation dependency.

Strategic Petroleum Reserve Utilisation

Government Intervention Mechanisms

Strategic responses demonstrate the policy dimension of supply security during chokepoint disruptions. South Korea's government initiated discussions regarding Strategic Petroleum Reserve releases and potential oil product export restrictions, indicating coordinated energy security responses.

These interventions reveal how supply disruptions trigger both market-based and policy-based adjustment mechanisms simultaneously, creating complex interaction effects between commercial and strategic considerations.

Risk Assessment Framework: Duration and Severity Scenarios

Energy market participants must evaluate multiple scenario pathways for strategic planning during extended supply disruptions. Different duration assumptions lead to dramatically different investment and operational decisions across the energy sector, particularly as oil prices ease under tariffs in some scenarios.

Short-term Stabilisation Scenario (2-4 weeks)

Market Normalisation Expectations

- Freight rates normalise as alternative routes establish operational efficiency

- Crude price premiums moderate but remain elevated above historical baselines

- Limited permanent supply chain restructuring occurs

- Traditional trade relationships resume with minor modifications

Extended Disruption Scenario (2-6 months)

Structural Adaptation Acceleration

- Permanent supply chain diversification accelerates across multiple regions

- US crude export infrastructure expansion becomes economically justified

- Asian refinery crude slate optimisation shifts toward North American grades

- Strategic alliance formation around alternative supply corridors intensifies

Prolonged Crisis Scenario (6+ months)

Fundamental Market Restructuring

- Complete reshaping of global crude trade flow patterns

- Strategic alliance formation around alternative supply corridors becomes permanent

- Accelerated energy security policy implementations across multiple jurisdictions

- Infrastructure investment programmes targeting supply chain resilience

The next major ASX story will hit our subscribers first

Historical Comparative Analysis: Chokepoint Disruption Patterns

Understanding current market responses requires comparison with previous chokepoint disruptions, though each event contains unique characteristics preventing direct extrapolation. The Suez Canal blockage of 2021 provides the most recent comparable disruption data for evaluating how tanker traffic collapses affect freight costs.

Suez Canal Blockage (2021) vs. Hormuz Closure (2026)

| Comparison Factor | Suez 2021 | Hormuz 2026 |

|---|---|---|

| Disruption Duration | 6 days total | Ongoing (7+ days) |

| Primary Commodity Impact | Containers/General cargo | Crude oil/LNG focus |

| Freight Response Pattern | Temporary spike, quick normalisation | Sustained elevation |

| Strategic Response Focus | Route diversification | Supply source diversification |

| Market Memory Effect | Limited long-term changes | Potential permanent restructuring |

Key Distinctions

The current disruption affects energy commodities directly rather than general cargo, creating more immediate economic impacts across multiple sectors simultaneously. Energy security considerations drive different strategic responses compared to general trade disruptions.

Market Outlook: Freight Rate Sustainability Assessment

Evaluating freight rate sustainability requires balancing fundamental support factors against potential moderating forces. Current market conditions suggest multiple scenarios depending on geopolitical developments and supply chain adaptation speeds.

Fundamental Support Factors

Sustained Elevation Drivers

- Continued Middle East supply uncertainty creating persistent risk premiums

- Asian refiner crude slate diversification establishing new demand patterns

- Strategic stockpiling activities supporting consistent demand levels

- Insurance market risk reassessment maintaining elevated coverage costs

Structural Change Catalysts

The crisis may establish permanent changes in energy trade relationships, creating baseline demand for trans-Pacific crude transportation that persists beyond immediate supply constraints.

Potential Moderating Forces

Rate Normalisation Pressures

- Diplomatic resolution progress reducing geopolitical risk premiums

- Alternative Middle Eastern export route development providing supply alternatives

- Increased US crude production response to sustained high prices

- Strategic petroleum reserve releases dampening spot market tightness

Market Rebalancing Mechanisms

Higher freight costs eventually encourage supply response through increased US production, while demand destruction from elevated energy costs creates natural market balancing forces.

Investment Implications and Strategic Positioning

Current market conditions create distinct winners and losers across energy sector investments, with traditional risk-return relationships temporarily altered by supply chain disruptions. Understanding these dynamics becomes crucial for strategic positioning during extended volatility periods.

Primary Beneficiary Sectors

US Crude Producers with Export Capacity

Companies positioned to increase export volumes benefit directly from elevated pricing and sustained Asian demand. Export terminal capacity becomes a critical competitive advantage during supply shortage periods.

Tanker Operators with Fleet Positioning Flexibility

Shipping companies capable of rapid vessel repositioning capitalise on freight rate premiums while competitors remain constrained by existing commitments or vessel specifications.

Alternative Energy Infrastructure Developers

Projects targeting energy supply diversification receive accelerated investment interest as strategic considerations override purely economic calculations.

Strategic Storage Facility Operators

Both commercial and strategic storage facilities benefit from increased utilisation as market participants seek supply security through inventory building.

Risk Considerations and Constraints

Demand Destruction Scenarios

Sustained high energy costs eventually reduce consumption across multiple sectors, potentially creating oversupply conditions once transportation constraints resolve.

Geopolitical Escalation Risks

Further regional conflict expansion could disrupt additional supply sources while complicating insurance and financing arrangements for energy investments.

Currency and International Trade Impacts

Energy cost inflation affects exchange rates and trade balances, creating secondary effects on international crude oil competitiveness and demand patterns.

Regulatory Response Uncertainties

Government interventions targeting energy security may alter market dynamics unpredictably, affecting investment returns across multiple time horizons.

The strait of hormuz squeeze lifts us crude freight to record levels while creating lasting changes in global energy trade patterns. These developments extend far beyond temporary price adjustments, establishing structural shifts that may persist long after immediate supply constraints resolve. Market participants must navigate both immediate operational challenges and strategic positioning for altered trade relationships in this evolving energy landscape.

Disclaimer: This analysis contains forward-looking statements and market predictions based on current conditions. Energy markets remain subject to significant volatility from geopolitical, economic, and operational factors. Investment decisions should consider comprehensive risk assessments beyond the scope of this analysis. Market data and statistics cited reflect conditions as of the specified dates and may change rapidly during volatile periods.

Looking to Capitalise on Energy Market Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market during volatile energy and commodity cycles. Begin your 14-day free trial today and secure your market-leading advantage while global supply chains reshape investment landscapes.