May 19, 2026

Understanding the Strategic Chokepoint Risk Framework

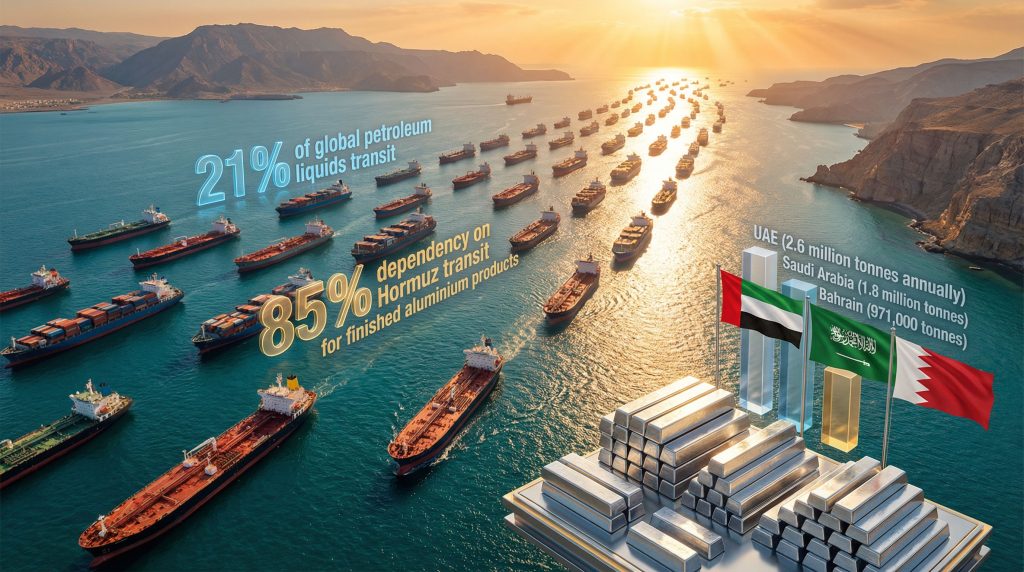

The strait of Hormuz tensions and aluminium supply disruption represents a critical vulnerability in modern commodity supply chains, where military positioning intersects with commercial shipping routes. Furthermore, this narrow waterway connecting the Persian Gulf to the Gulf of Oman facilitates approximately one-fifth of global petroleum product movements, making it irreplaceable for energy security across multiple continents.

Geographic Vulnerability Assessment of Critical Maritime Routes

The 34-kilometre channel creates an unavoidable transit point for vessels carrying crude oil, refined products, and manufactured goods from Gulf Cooperation Council nations to international markets. Maritime traffic through this corridor reached a virtual standstill following escalating tensions between Iran and Israel beginning February 28, 2026.

Although Iranian authorities have not formally announced any closure, shipping companies interpreted the security environment as presenting unacceptable risk levels for commercial operations. This de facto suspension demonstrates how perceived threats can create supply disruptions even without official blockade declarations.

The waterway's strategic importance extends beyond petroleum flows. Container shipping routes carrying manufactured aluminium products from Gulf states traverse these same waters, creating dual exposure for regional producers who import raw materials and export finished goods through identical maritime corridors. Consequently, these developments highlight the interconnected nature of trade war oil markets and their broader implications.

Geopolitical Escalation Scenarios and Market Response Patterns

Market participants responded immediately to escalating regional tensions through commodity price adjustments and operational modifications. West Texas Intermediate crude oil surged 7.76% to $72.19 per barrel on March 2, 2026, reflecting traders' assessment of potential supply disruption risks.

This price movement established the foundation for subsequent freight rate calculations across multiple commodity sectors. Insurance markets demonstrated heightened risk perception through elevated marine coverage premiums, with underwriters reluctant to provide coverage for vessels transiting through waters where military assets maintained strategic positioning.

The timeline of market responses reveals how quickly geopolitical uncertainty translates into commercial decision-making. Major shipping lines implemented operational changes within 72 hours of initial tension escalation, suggesting that contingency planning protocols recognise the waterway's vulnerability to rapid closure scenarios. For instance, the US–China trade war impact demonstrates similar rapid market adjustments during geopolitical tensions.

When big ASX news breaks, our subscribers know first

What Makes Middle Eastern Aluminium Production Uniquely Vulnerable?

GCC Smelting Capacity and Export Dependencies

Gulf Cooperation Council nations operate substantial aluminium smelting facilities that collectively represent a significant portion of global primary production capacity. These operations concentrate in the UAE, Saudi Arabia, and Bahrain, creating regional clusters that share common logistics infrastructure and export routes.

The geographic positioning of these facilities creates inherent dependency on maritime transit through strategic chokepoints. Regional producers have already notified customers of anticipated delays and logistics disruptions following the March 2026 tension escalation.

The containerised nature of aluminium exports from Middle Eastern facilities creates specific vulnerability compared to bulk commodity movements. Unlike dry bulk carriers that might utilise alternative routing, container shipping requires specialised port infrastructure and vessel capacity that cannot be easily substituted.

Export logistics from Gulf states typically involve twenty-foot equivalent unit containers carrying approximately 20 tonnes of P1020 aluminium ingot per container. This packaging approach, whilst efficient for inventory management and customer delivery, creates dependency on container shipping lines that have demonstrated willingness to suspend Middle Eastern operations during periods of elevated security risk.

Raw Material Import Vulnerabilities

Middle Eastern aluminium smelters operate under a dual logistics exposure model where both input materials and output products transit through identical maritime corridors. Alumina feedstock arrives via bulk carriers through the same waterways that later carry containerised aluminium products to international markets.

This creates compound risk where production facilities face simultaneous disruption potential on supply and distribution channels. The 1.9 tonnes of alumina required per tonne of aluminium production represents a continuous import requirement that cannot be easily substituted through alternative supply sources.

Regional smelters typically maintain 3-4 week stockpile buffers, meaning that extended maritime disruptions could force production curtailments within a month of initial supply interruption. However, effective market volatility hedging strategies can help mitigate some of these risks.

Alternative import routes through Red Sea corridors or overland transportation networks face significant capacity constraints. Industry participants noted that trucking sufficient raw materials to maintain current production levels would require several trucks per minute operating continuously, competing with essential goods transportation for limited infrastructure capacity.

How Do Freight Rate Dynamics Amplify Supply Chain Stress?

War Risk Surcharge Implementation Across Shipping Lines

Major container shipping companies implemented comprehensive service suspensions and surcharge structures within days of regional tension escalation. The speed and scope of these responses demonstrate how quickly perceived security risks translate into operational cost increases for commodity shippers.

| Shipping Line | War Risk Surcharge | Effective Date | Geographic Scope |

|---|---|---|---|

| Hapag-Lloyd | $1,500 per TEU | March 2, 2026 | All GCC ports |

| Maersk | Suspended bookings | March 1, 2026 | UAE, Oman, Iraq, Kuwait, Qatar, Bahrain, Saudi Arabia |

| MSC | Complete suspension | March 1, 2026 | Worldwide cargo to Middle East |

The Hapag-Lloyd War Risk Surcharge applies retroactively to bookings already issued and cargo currently on vessels. For aluminium exporters shipping 20 tonnes of P1020 ingot in a standard twenty-foot container, this surcharge translates to an additional $75 per tonne in logistics costs.

Mediterranean Shipping Company's complete suspension of worldwide cargo bookings to Middle Eastern destinations represents the most comprehensive response. Maersk's selective suspension focuses on refrigerated and dangerous goods categories whilst maintaining some general cargo capacity, though with significant geographic restrictions.

Crude Oil Price Correlation and Transportation Cost Multipliers

Rising crude oil prices create multiplicative effects on maritime transportation costs through direct fuel cost increases and indirect insurance premium escalations. The 7.76% crude price surge established new baseline costs for vessel operators, who typically pass fuel cost adjustments through to shippers via surcharge mechanisms.

Fuel cost pass-through structures in maritime contracts create automatic escalation mechanisms that amplify crude oil price movements into commodity shipping expenses. These contractual arrangements ensure that energy price volatility translates directly into logistics cost inflation for commodity exporters and importers.

Secondary cost escalations emerge through increased marine insurance premiums, vessel routing modifications, and port congestion effects. Market participants reported insurance coverage reluctance from underwriters, forcing shippers to accept higher premium rates or extended coverage exclusions for Middle Eastern transit routes. Moreover, understanding tariff market impact becomes crucial when evaluating these cost structures.

What Alternative Supply Strategies Could Mitigate Regional Disruptions?

European Premium Market Adjustments

European aluminium markets immediately reflected Middle Eastern supply concerns through premium adjustments that signal anticipated supply tightening. Rotterdam P1020A premiums increased from $280-320 per tonne on February 27 to $300-340 per tonne on March 2, representing a $20-40 per tonne increase within three trading days.

This premium escalation indicates that European consumers began adjusting procurement strategies to account for potential Middle Eastern supply disruptions. The speed of market response suggests that industrial buyers maintain contingency supplier relationships and can activate alternative sourcing arrangements relatively quickly when primary supply routes face uncertainty.

European storage facilities and distribution networks likely began strategic inventory positioning to buffer potential supply gaps from Gulf region producers. Whilst specific volume data remains proprietary, the premium increases suggest material demand shifting toward non-Gulf suppliers serving European markets.

Overland Transportation Feasibility Analysis

Alternative export routes through Saudi Arabian ports like Jeddah and Yanbu face significant infrastructure capacity constraints that limit their effectiveness as substitutes for maritime container shipping through traditional routes. Industry analysis indicates that trucking equivalent volumes would require continuous heavy vehicle movement that exceeds current road network capacity.

The logistics mathematics reveal fundamental constraints: transporting 20-tonne container equivalents via trucking requires multiple vehicles per container load due to weight and volume limitations. Scaling this to accommodate typical Middle Eastern aluminium export volumes would demand trucking capacity that competes directly with essential goods transportation.

Port infrastructure at alternative Saudi facilities lacks the container handling capacity and specialised equipment necessary to accommodate sudden volume increases from diverted Gulf exports. Rail transportation alternatives face similar capacity constraints, with existing rail infrastructure designed primarily for domestic and regional passenger service rather than heavy commodity export flows.

Pipeline alternatives remain technically infeasible for finished aluminium products, limiting overland options to trucking and rail systems that cannot readily substitute for maritime container capacity.

How Do Other Critical Minerals Navigate Similar Transit Risks?

Bauxite Supply Chain Resilience from West Africa

Guinea's bauxite exports to China demonstrate successful geographic diversification strategies that bypass Middle Eastern chokepoint risks entirely. Shipping routes from Guinea to Chinese ports utilise the Cape of Good Hope passage around southern Africa, completely avoiding strait of Hormuz tensions and aluminium supply disruption dependencies.

China imported 149.19 million tonnes of bauxite from Guinea in 2025, representing a 35.51% year-on-year increase and accounting for 74% of China's total bauxite import volume. This volume concentration demonstrates how major commodity consumers can achieve supply security through geographic diversification rather than transport route multiplication.

However, even geographically diversified supply chains experienced cost pressures from crude oil price increases. Freight rates for Guinea-to-China shipments increased from $24 per dry metric tonne in January to $26-27 per dmt by late February 2026, representing a 4.2% to 12.5% cost escalation.

Industry sources indicated that continued crude oil price elevation could force temporary shipping delays if Guinean miners cannot secure vessels at economically viable freight rates. This demonstrates how global fuel cost increases can affect even geographically isolated supply chains through maritime transportation cost inflation. Additionally, examining oil price rally insights provides valuable context for these developments.

Zinc and Lead Concentrate Market Adaptations

Iranian zinc and lead concentrate exports to China represent less than 10% of China's total annual concentrate imports, limiting overall market exposure to Middle Eastern supply disruptions. This relatively modest market share provides natural diversification that reduces systemic risk compared to more concentrated supply relationships.

Chinese smelter operations maintained robust inventory positions following winter restocking cycles, creating buffer capacity that reduces immediate procurement urgency. This inventory positioning demonstrates how seasonal demand patterns can provide temporary protection against supply disruptions when facilities maintain strategic stockpiles.

Freight rate increases for zinc and lead concentrates averaged $2-3 per tonne compared to pre-tension baselines, driven primarily by higher fuel costs rather than war risk premiums. Treatment charges remained stable despite logistics cost increases, suggesting that Chinese smelters absorbed transportation cost escalation.

The concentrate market's relative stability compared to finished aluminium products illustrates how bulk commodity transportation can maintain greater operational flexibility during maritime disruptions compared to containerised manufactured goods.

What Investment Implications Emerge from Supply Chain Fragmentation?

Regional Production Capacity Rebalancing Opportunities

Supply chain vulnerability in Middle Eastern aluminium production creates potential investment opportunities in alternative production regions with greater geographic diversification. Facilities located outside traditional chokepoint dependencies may experience enhanced competitive positioning as industrial consumers prioritise supply security over pure cost optimisation.

Capital allocation decisions increasingly incorporate geopolitical risk assessments alongside traditional financial metrics when evaluating production facility investments. This shift suggests that future capacity expansion may favour locations with multiple export route options and reduced dependency on single maritime transit corridors.

Technology transfer acceleration may emerge as companies seek to reduce transportation dependencies through production localisation strategies. Advanced smelting technologies and process optimisation may enable economically viable production in markets previously considered cost-prohibitive compared to Gulf region facilities.

Strategic Metal Stockpiling and Forward Contract Adjustments

Industrial consumers are likely adjusting inventory management strategies to incorporate longer buffer periods and multiple supplier relationships that reduce concentration risk. This strategic stockpiling approach requires additional working capital investment but provides operational insurance against supply disruptions.

Forward contract structures may evolve to incorporate force majeure clauses and alternative delivery mechanisms that provide flexibility during geopolitical disruptions. Financial hedging instruments including freight rate derivatives and currency swaps may become standard risk management tools for companies with concentrated Middle Eastern exposure.

Government strategic reserve policies may expand to include aluminium and other critical industrial metals, creating additional demand sources that support alternative production regions whilst providing national security insurance for strategic materials.

The next major ASX story will hit our subscribers first

How Could Extended Disruptions Reshape Global Aluminium Trade Flows?

Scenario Modeling: 30-Day vs 90-Day Closure Impact

Short-term disruptions lasting 30 days would primarily affect inventory depletion at Gulf region smelters whilst creating temporary premium increases in major consuming markets. Existing stockpiles and alternative supplier activation could potentially accommodate this duration without forcing production curtailments at regional facilities.

Extended disruptions lasting 90 days or longer would likely force production curtailments at Middle Eastern smelters due to alumina feedstock depletion. Given typical 3-4 week inventory buffers for raw materials, facilities would face critical supply shortages within the second month of sustained maritime disruption.

Global supply-demand rebalancing would accelerate during extended disruption scenarios, with alternative production regions increasing capacity utilisation to offset Middle Eastern shortfalls. Price premiums would likely escalate substantially as inventory buffers exhaust and consumers compete for alternative supply sources.

The aluminium futures market would likely experience significant volatility during extended disruption scenarios, with backwardation structures emerging as near-term supply concerns outweigh longer-term production capacity considerations.

Long-Term Structural Market Changes

Permanent structural changes may emerge even after disruption resolution, as consumers and producers adjust supply chain strategies to prevent future vulnerability. Investment acceleration in geographically diversified production facilities would likely continue based on demonstrated chokepoint risks rather than reverting to previous concentration patterns.

Trade route diversification strategies would likely become standard practice for major commodity consumers, with portfolio approaches to supplier relationships replacing cost-optimisation-focused procurement strategies. This shift implies higher structural costs but greater supply security for industrial operations.

Technology adoption for supply chain visibility and risk management would likely accelerate, with real-time tracking systems and predictive analytics becoming standard tools for managing geopolitical supply risks across multiple commodity categories.

What Risk Management Frameworks Should Industry Stakeholders Adopt?

Multi-Layered Contingency Planning Models

Early warning indicator systems should incorporate geopolitical tension monitoring alongside traditional market and operational metrics. These systems require integration of political risk analysis with supply chain monitoring to provide advance notice of potential disruption scenarios before they fully develop.

Supplier diversification matrices should evaluate geographic distribution, transportation route variety, and political stability indicators rather than focusing primarily on cost and quality metrics. Qualification processes for alternative suppliers should include scenario testing to ensure operational readiness during emergency activation periods.

Financial hedging instruments should address freight rate volatility, currency exposure, and commodity price risks simultaneously rather than treating these as independent variables. Integrated risk management approaches recognise that geopolitical disruptions typically affect multiple cost components concurrently.

Collaborative Industry Response Mechanisms

Information sharing protocols among market participants can provide collective early warning capabilities that exceed individual company intelligence gathering capacity. Industry associations and commodity exchanges may develop formal information sharing frameworks that improve market-wide preparedness for supply disruption scenarios.

Joint inventory management and allocation systems could provide buffer capacity during disruptions whilst distributing storage costs across multiple industry participants. These collaborative approaches require advance coordination but can provide more efficient risk management than individual company stockpiling strategies.

Regulatory coordination for emergency supply measures may become necessary during extended disruption scenarios, with government agencies and industry participants developing predetermined response protocols that balance strategic material security with market functionality. Furthermore, recent studies on aluminum price jumps in Middle East conflicts demonstrate the importance of proactive risk management.

Strategic scenario planning must incorporate both immediate operational responses and longer-term structural adaptations to address the reality that geopolitical tensions affecting critical maritime chokepoints will likely continue creating periodic supply chain vulnerabilities. The strait of Hormuz tensions and aluminium supply disruption events of March 2026 demonstrate how quickly regional conflicts can translate into global commodity market impacts, requiring sophisticated risk management approaches that balance cost efficiency with supply security across multiple operational timeframes.

Moreover, industry experts note that Middle East tensions continue to affect aluminum supply chains globally, emphasising the need for adaptive strategies that can respond to evolving geopolitical landscapes whilst maintaining operational efficiency.

This analysis is based on market intelligence and strategic assessment methodologies current as of March 2026. Market conditions and geopolitical situations remain subject to rapid change, requiring ongoing monitoring and adaptive strategy adjustments. Investment and operational decisions should incorporate professional risk assessment and consider multiple scenario outcomes.

Ready to Navigate Complex Geopolitical Commodity Risks?

Discovery Alert's proprietary Discovery IQ model provides real-time alerts on significant ASX mineral discoveries, helping investors identify opportunities that may benefit from supply chain disruptions and geopolitical tensions affecting global commodity markets. Start your 14-day free trial today and gain the market intelligence needed to capitalise on strategic mineral discoveries whilst navigating volatile commodity environments.