July 10, 2026

The Hidden Architecture of Global Oil Risk: How a 21-Mile Chokepoint Controls Energy Markets

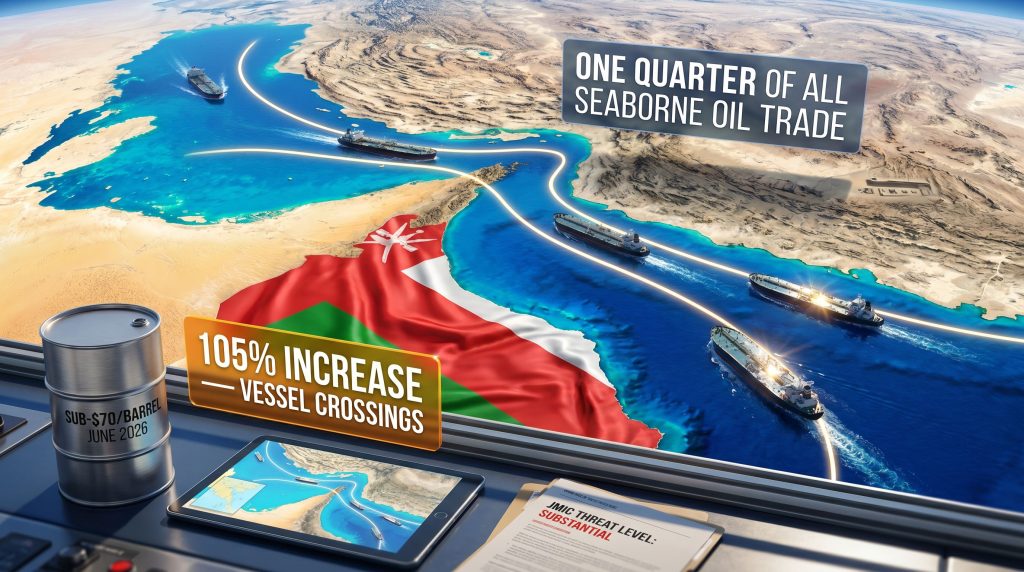

Every decade or so, the energy world is reminded that the physical geography of commodity trade matters more than any spreadsheet model can capture. The Strait of Hormuz is the clearest example of this reality. Stretching just 21 miles at its narrowest navigable point, this sliver of water between Iran and Oman functions as the single most consequential pressure valve in the global hydrocarbon system. When conditions through this corridor deteriorate, the consequences ripple outward with remarkable speed, touching crude benchmarks, freight rates, insurance markets, and downstream fuel prices simultaneously.

What makes the current Strait of Hormuz tensions and Oman shipping corridor situation particularly significant is not simply that conflict has returned to the region. It is that the nature of the dispute has fundamentally changed, shifting from a binary threat of physical closure to something far more complex: a contest over operational authority, routing jurisdiction, and the legal governance of one of the world's most critical maritime lanes.

When big ASX news breaks, our subscribers know first

Why the Strait of Hormuz Cannot Be Replicated or Bypassed

Understanding why markets respond so acutely to Hormuz developments requires appreciating what the waterway actually carries and what alternatives realistically exist. Furthermore, the crude oil price trends that have emerged in 2025 and into 2026 have made this question more pressing than ever.

Approximately one quarter of all globally seaborne oil trade transits the Strait on an annual basis. This figure encompasses not only crude oil but also liquefied petroleum gas, liquefied natural gas, and a substantial volume of refined petroleum products destined predominantly for Asian import markets. The countries whose export infrastructure depends almost entirely on this corridor include Saudi Arabia, Iraq, Kuwait, the United Arab Emirates, and Iran itself.

Unlike the Suez Canal or the Strait of Malacca, no genuinely equivalent bypass route exists at comparable throughput scale. The closest partial alternative for Saudi crude is the East-West Pipeline, which terminates at Yanbu on the Red Sea coast and can carry roughly 5 million barrels per day at full capacity. That represents meaningful relief for Saudi volumes but does nothing to address Iraqi, Kuwaiti, or UAE export exposure. The UAE's Abu Dhabi Crude Oil Pipeline provides limited additional bypass capacity toward Fujairah. Neither option approaches the full scale of what transits Hormuz on a given day.

The Strait's navigable shipping lanes are also structurally exposed in ways that other chokepoints are not. The waterway is shallow in parts, mine-susceptible, and militarily observable from both coastlines. These physical characteristics mean that even partial disruption or elevated threat perception carries outsized consequences for tanker operators, insurers, and flag states.

From Ceasefire Optimism to Renewed Crisis: The 2026 Escalation Timeline

To understand the present situation, it helps to trace how rapidly market confidence collapsed following what appeared, briefly, to be a workable diplomatic framework.

A Memorandum of Understanding between the United States and Iran had temporarily restored transit confidence through mid-2026. Crude oil prices responded accordingly, falling below $70 per barrel in June 2026 as market participants priced out the geopolitical risk premium that had accumulated during earlier conflict phases. For energy traders, this represented a textbook case of risk repricing: the physical supply threat appeared contained, and prices adjusted.

That adjustment proved premature. The sequence of events that followed unfolded quickly:

-

An Iranian attack on a commercial vessel near the Strait triggered the immediate crisis phase.

-

US President Donald Trump characterised the incident as a direct violation of the existing ceasefire framework.

-

The Joint Maritime Information Center (JMIC), operating under US Navy oversight, formally raised the threat classification in the Strait to "substantial" — a designation carrying significant implications for vessel routing decisions and insurance obligations.

-

US military forces conducted airstrikes against Iranian missile installations, drone infrastructure, and radar facilities positioned near the Strait.

-

Iran's Islamic Revolutionary Guard Corps (IRGC) responded with retaliatory strikes against US military positions in the region.

The speed of this deterioration is itself instructive. Energy markets that had taken weeks to price out Hormuz risk saw that confidence evaporate within days. This asymmetry between how slowly stability builds and how quickly it collapses is a defining feature of geopolitical oil risks in commodity markets.

The Toll Dispute: A Structural Fault Line That Markets Underestimated

Beneath the military exchanges lies a legal and administrative dispute that may prove more durable than any single incident. The question of transit fees through the Strait has emerged as a fundamental point of conflict between Tehran and Washington.

| Position | US Stance | Iranian Stance |

|---|---|---|

| Transit Fees | Permanent toll-free passage required | Right to charge navigation and environmental service fees |

| Timeline | No fee window — open passage at all times | 60-day toll-free window, after which fees apply |

| Legal Basis | International maritime law and freedom of navigation | Sovereign territorial claim over passage management |

| Current Status | Active dispute — unresolved | IRGC asserting operational control over vessel routing |

This dispute is significant because it recasts the entire risk framework. Previous Hormuz crises centred on whether the Strait would be physically closed, a dramatic but ultimately unlikely outcome given its economic importance to Iran itself. The current dynamic involves something more subtle and potentially more persistent: a contest over who exercises operational authority over vessels transiting the waterway, through which lanes, and under whose administrative oversight.

What Is the Oman Shipping Corridor and How Did It Emerge?

With the primary Traffic Separation Scheme rendered operationally unusable due to active security threats, including reports of dozens of uncleared mines remaining in the central waterway, a practical solution was urgently needed. The humanitarian dimension was acute: more than 11,000 sailors were effectively stranded in the Gulf due to the conflict, unable to transit safely through established lanes.

Oman and Iran held talks to ease maritime passage as tensions escalated. Consequently, Oman stepped into this vacuum in coordination with the International Maritime Organization (IMO), establishing two temporary maritime routes flanking the primary shipping lane through its Maritime Security Centre and naval assets.

How the Corridor Routes Are Structured

-

Northern temporary route — positioned above the primary Traffic Separation Scheme lane, providing an alternative track for inbound vessels.

-

Southern temporary route — positioned below the primary lane, accommodating outbound vessel movements.

-

Both routes were confirmed as toll-free by Omani authorities, with no transit fees imposed on commercial vessels regardless of flag state or cargo type.

-

Vessel crossings through the Oman-facilitated corridors reportedly increased by 105% following the corridor's establishment, reflecting the acute demand for a viable alternative routing option.

The commercial logic was straightforward: operators needed to move cargo, sailors needed to reach port, and the Omani corridors provided a functional pathway when the primary lane could not.

Iran's Rejection and the 7 July Attacks

Iran's IRGC publicly characterised Oman's corridors as unacceptable and potentially dangerous, stating that all commercial vessels must use only IRGC-approved routes and establish direct contact with the IRGC Navy prior to transit. Iran warned ships of a forceful response to vessels using US-backed alternative routing frameworks.

This rejection transformed a logistical emergency solution into a geopolitical flashpoint. On 7 July 2026, vessels using the Omani alternative routes were attacked, representing a significant escalation in Iran's willingness to enforce its routing authority through direct maritime interdiction rather than diplomatic protest alone.

The attacks on vessels transiting the Oman corridor signal a critical shift: Iran is not merely disputing the legal basis of alternative routing frameworks — it is actively enforcing its position through force, creating an environment where no routing option can be considered genuinely safe without Iranian acquiescence.

How Freight Markets and Crude Pricing Are Responding

The return of active hostilities has produced measurable stress across multiple interconnected market layers.

Crude Oil Price Dynamics

The sub-$70 per barrel environment of June 2026 reflected a market that had largely priced out Hormuz disruption risk following the initial ceasefire. The renewed escalation has reintroduced a geopolitical risk premium into crude benchmarks, with Middle East Gulf crude streams facing the most direct exposure to transit uncertainty. For a broader view of the current environment, the crude market overview provides useful context on where prices stood before this escalation cycle began.

A particularly important and underappreciated dynamic is that crude price responses to Hormuz tensions are not linear. Markets tend to overprice immediate disruption risk during acute escalation phases and then underprice the structural residual risk during temporary stability windows, as June 2026 demonstrated. This volatility pattern creates both risk and opportunity for energy market participants.

Freight Market Stress Indicators

| Risk Category | Pre-Escalation | Post-Escalation |

|---|---|---|

| War Risk Premium (% of vessel value) | Low / minimal | Elevated — voyage-specific assessment |

| VLCC Charter Rate Premium (Gulf routes) | Normalised | Significantly elevated |

| Crew Risk Allowances | Standard | Enhanced danger pay applicable |

| Cargo Insurance Loading | Minimal | Substantial uplift |

Shipping operators now face a binary routing dilemma with no clean answer:

-

Use IRGC-endorsed lanes and implicitly accept Iranian operational authority over the transit.

-

Use the Oman corridors and accept the demonstrated attack risk that materialised on 7 July.

War risk insurance has re-entered the Joint War Committee's Listed Areas framework for the Strait of Hormuz, triggering mandatory additional premium clauses. Critically, insurers have shifted from blanket annual premium structures to voyage-specific risk assessments, reflecting a structural change in how Gulf transit exposure is priced rather than a temporary adjustment.

LPG, LNG, and Refined Products: The Overlooked Exposure

Media coverage of Hormuz tensions typically focuses on crude oil, but the exposure profile extends significantly further. The Strait is the primary transit corridor for Gulf LPG and LNG exports, with Asian importers carrying the most concentrated demand exposure. In addition, these oil price impacts extend well beyond the crude benchmark into downstream energy costs across Asian economies.

Countries facing acute supply chain vulnerability if transit volumes contract meaningfully include:

-

South Korea — heavily reliant on Gulf LPG for petrochemical feedstocks.

-

Japan — dependent on Gulf LNG streams with limited near-term diversification capacity.

-

India — a major LPG import market with growing Gulf dependency.

-

China — the world's largest LNG importer, with significant Gulf stream exposure.

Jet fuel and gasoil markets, already under upward pressure from regional conflict dynamics, face additional cost inflation if product tanker movements through the Strait are constrained.

Oman's Diplomatic Role: A Fulcrum Under Pressure

Oman's intervention in establishing the alternative corridors is not merely a logistical act. The Sultanate has historically served as a discreet back-channel between Iran and Western governments, a role it has now extended explicitly into the maritime governance domain.

By working through the IMO framework, Oman has positioned itself as a legitimate international actor in Strait management, creating a direct institutional challenge to Iran's unilateral authority claims. The corridors are not simply an emergency shipping measure; they represent a competing governance model for the waterway. Understanding the broader context of OPEC market influence is equally important here, as Gulf producers' export capacity underpins the urgency of resolving this impasse.

Whether Oman's traditional neutrality can withstand Iranian pressure following the 7 July vessel attacks is one of the most consequential near-term variables in the crisis. If Oman is forced to withdraw its facilitation role, the practical alternatives for commercial vessels diminish sharply.

The next major ASX story will hit our subscribers first

Three Scenarios for the Strait: Pathways and Probabilities

Scenario 1 — Negotiated Stabilisation (Lower Probability, Near-Term)

A revised agreement is reached, incorporating compromise language on routing protocols and the transit fee dispute. Vessel traffic normalises through the primary lane; the Oman corridors are wound back as emergency measures. Crude prices return toward the $65-70 per barrel range as the geopolitical premium dissipates.

Scenario 2 — Sustained Corridor Conflict (Base Case)

Neither side concedes on routing authority. The Oman corridor remains contested, with vessel operators self-selecting routes based on flag state, cargo type, and insurer guidance. Freight rates remain elevated, war risk premiums persist, and crude prices trade with a sustained $5-10 per barrel geopolitical premium baked into benchmarks.

Scenario 3 — Full Strait Disruption (Tail Risk, High Consequence)

Escalating attacks force a de facto collapse of commercially viable transit lanes. The volume of at-risk supply approaches 15-20 million barrels per day. Coordinated IEA strategic petroleum reserve releases are activated across member states, and crude prices spike meaningfully above $100 per barrel as supply shock dynamics dominate market sentiment.

Frequently Asked Questions: Strait of Hormuz Tensions and Oman Shipping Corridor

What is the Oman shipping corridor and why was it created?

Oman established two temporary maritime routes in coordination with the International Maritime Organization to provide safe passage alternatives when the primary Strait of Hormuz Traffic Separation Scheme became operationally unsafe. The immediate humanitarian trigger was the need to evacuate more than 11,000 sailors stranded in the Gulf. Oman's Maritime Security Centre confirmed that no transit fees are charged on either route.

Why is Iran opposed to the Oman shipping corridor?

Iran's IRGC has rejected the Oman-facilitated routes, characterising them as unacceptable. Tehran's position requires all commercial vessels to use IRGC-designated lanes and establish direct communication with the IRGC Navy before transiting. This reflects Iran's broader assertion of sovereign administrative authority over Strait passage management, a position in fundamental tension with the freedom of navigation principles upheld under international maritime law.

How much oil transits the Strait of Hormuz?

Approximately one quarter of all globally traded seaborne oil passes through the Strait annually, covering crude oil, LPG, LNG, and refined petroleum products destined primarily for Asian markets including China, Japan, South Korea, and India.

What happened to oil prices during the temporary ceasefire?

Following the initial restoration of transit stability under the US-Iran agreement, crude oil prices fell below $70 per barrel in June 2026, reflecting markets pricing out the accumulated geopolitical risk premium. The subsequent return of hostilities and vessel attacks has since reintroduced upward pricing pressure.

What is the JMIC threat level for the Strait?

The Joint Maritime Information Center, operating under US Navy oversight, raised the Strait of Hormuz threat classification to "substantial" following commercial vessel attacks. This designation influences vessel routing decisions, insurance requirements, flag state advisories, and crew risk assessments across the global tanker fleet.

Could the Strait be completely closed to commercial traffic?

A full closure represents a low-probability but high-consequence scenario. If sustained attacks rendered all viable transit lanes operationally unsafe, at-risk supply volumes could approach 15-20 million barrels per day, almost certainly triggering coordinated IEA strategic reserve releases and a significant crude price spike above $100 per barrel.

Key Risk Summary: Current Strait of Hormuz Status

| Factor | Current Status | Market Implication |

|---|---|---|

| Strait Transit Status | Contested — primary lane unusable | Supply uncertainty premium in crude |

| Oman Corridor | Operational but under active attack risk | Elevated freight and insurance costs |

| US-Iran MOU | Fragile — actively violated | Geopolitical risk premium sustained |

| JMIC Threat Level | Substantial | Vessel operator caution; route avoidance |

| Toll Dispute | Unresolved | Long-term structural uncertainty |

| LPG/LNG Exposure | Significant | Asian import cost pressures rising |

| Crude Price Direction | Upward bias | Risk premium re-entering benchmarks |

The broader lesson embedded in this crisis is one that energy markets periodically forget and are then forced to relearn: physical geography is not a background variable in commodity pricing. It is the foundational constraint around which all other market dynamics operate. The Strait of Hormuz tensions and Oman shipping corridor developments of 2026 are a pointed reminder that when that geography becomes contested, the entire energy pricing architecture must adjust to accommodate the new reality.

This article is intended for informational and analytical purposes only. It does not constitute financial or investment advice. All scenario projections and probability assessments involve inherent uncertainty and should not be relied upon as predictions of future market conditions. Readers should conduct their own independent analysis before making any commercial or investment decisions.

Want to Capitalise on the Next Major Commodity Discovery Before the Market Catches On?

While geopolitical tensions reshape global energy pricing, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across 30-plus commodities and converting complex data into clear, actionable opportunities — explore historic discoveries and their market returns to see what's possible, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.