May 12, 2026

Global energy markets operate within an intricate web of dependencies where single transit routes can determine economic stability across continents. Maritime chokepoints represent critical vulnerabilities in international trade architecture, with disruptions capable of triggering cascading effects through manufacturing supply chains, financial markets, and geopolitical relationships. When these strategic waterways face prolonged instability, nations must rapidly reconfigure decades-old trade patterns while managing economic pressures from volatile energy costs and supply uncertainties.

The interconnected nature of modern economies means that energy transit disruptions extend far beyond immediate fuel shortages, penetrating deep into industrial production systems, consumer markets, and strategic planning frameworks across multiple sectors.

Understanding Strategic Energy Transit Vulnerabilities in China's Trade Network

China's economic architecture demonstrates significant exposure to maritime energy transit disruptions, particularly through critical waterways that handle substantial portions of global crude oil movements. The Strait of Hormuz crisis impacts China trade through multiple transmission mechanisms that extend beyond immediate energy supply constraints.

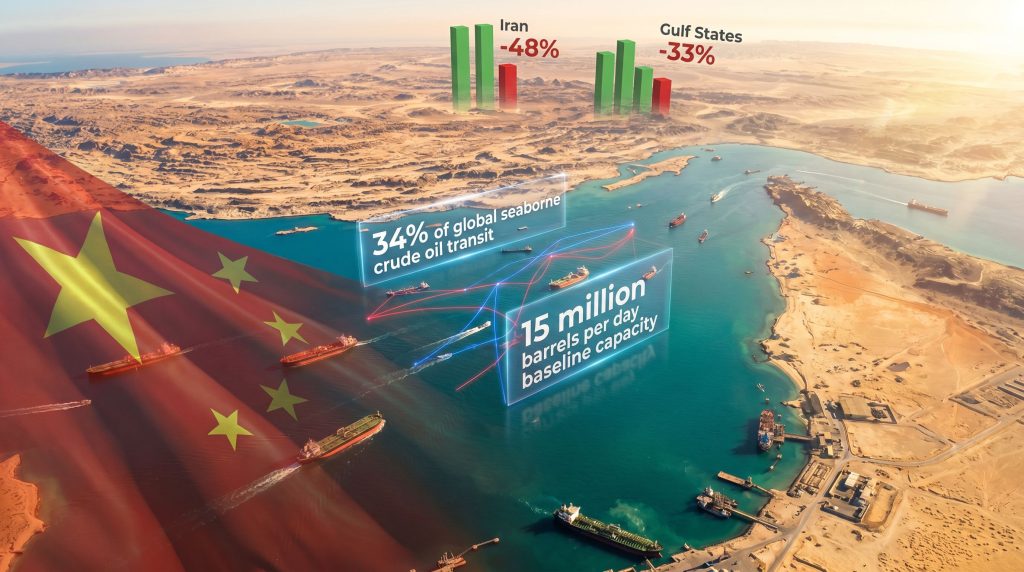

Recent data from Chinese customs authorities reveals the magnitude of trade flow disruptions during March 2026, when restrictions on the Strait of Hormuz intensified. Imports from Iran declined 48 percent year-over-year, while exports to Iran dropped 90 percent during this period. The broader Persian Gulf region experienced similar disruptions, with exports to eight Gulf economies falling 57 percent and imports declining 33 percent.

The strait's strategic importance stems from its role as a conduit for approximately 20 percent of global oil transit, creating bottleneck conditions where any operational disruption generates outsized international impacts. Chinese energy security faces particular vulnerability given the concentration of Middle Eastern suppliers, with oil imports from Gulf countries dropping 25 percent year-over-year during the March crisis period.

Alternative supply arrangements have provided partial mitigation, with increased shipments from Russia, Malaysia, and Indonesia helping offset some shortfalls. However, these alternatives operate within capacity constraints and face their own geopolitical and logistical limitations that prevent complete substitution of Gulf supplies.

Geographic Constraints and Capacity Limitations

The narrow configuration of the Strait of Hormuz creates inherent vulnerability for global energy flows. At its narrowest point in international waters, the strait spans approximately 21 nautical miles, forcing large tanker traffic through concentrated shipping lanes. Daily throughput typically reaches 15 million barrels under normal conditions, representing aggregated movement of vessels carrying between 2 million and 3 million barrels per tanker.

When transit restrictions occur, tankers face several routing alternatives, each involving significant cost and timing penalties:

- Cape of Good Hope routing adds 8-10 days transit time and substantial fuel costs

- Pipeline alternatives through Central Asia operate near capacity limits

- Regional transshipment hubs in Malaysia and Singapore require additional handling operations

Economic Transmission Mechanisms

Energy supply disruptions transmit through China's economy via interconnected pathways that amplify initial impacts. Manufacturing sectors face immediate input cost pressures as petroleum-derived materials become more expensive and less readily available. Transportation costs increase across all import categories, not merely energy products, as fuel expenses rise for shipping, trucking, and logistics operations.

Working capital requirements intensify as companies maintain larger inventories to buffer against supply uncertainties. Regional economic variations emerge based on proximity to alternative supply sources and industrial composition, with coastal manufacturing centres potentially adapting more rapidly than inland production facilities.

When big ASX news breaks, our subscribers know first

Quantifying Trade Disruption Impacts Across Key Relationships

The March 2026 crisis provided concrete data on how energy transit restrictions translate into measurable trade impacts across China's key Middle Eastern relationships. Analysis of customs data reveals differentiated impacts across trading partners, reflecting varying degrees of economic integration and alternative pathway availability.

| Trading Partner | Import Change (YoY) | Export Change (YoY) | Primary Impact Sectors |

|---|---|---|---|

| Iran | -48% | -90% | Crude oil, petrochemicals |

| Gulf States (aggregate) | -33% | -57% | LNG, refined products |

| Saudi Arabia | -25% | -60% | Crude oil, chemicals |

| Qatar | -30% | -55% | LNG, fertilisers |

These figures demonstrate asymmetric impacts between import and export flows, with Chinese exports to the region declining more severely than imports. This pattern suggests that while alternative energy suppliers can partially substitute for Gulf crude oil, Chinese manufactured goods face greater difficulty accessing Middle Eastern markets during transit disruptions.

Commodity-Specific Impact Analysis

Petroleum products experienced the most severe disruptions, with crude oil flows contributing significantly to the overall trade decline. Liquefied natural gas (LNG) imports from Qatar faced similar pressures, though existing contracts and alternative suppliers provided some stability. Petrochemical imports, essential for China's manufacturing base, encountered both volume reductions and price premiums as suppliers diverted products to spot markets.

Non-energy commodities also faced disruption through increased shipping costs and insurance premiums. Fertiliser imports from the Gulf region declined as agricultural input costs rose, potentially affecting China's domestic food production capacity during critical planting seasons.

Alternative Supply Activation

Russia emerged as a primary alternative supplier during the crisis, though infrastructure constraints limited expansion capacity. Malaysian and Indonesian shipments increased to partially offset Gulf shortfalls, demonstrating the importance of regional energy partnerships in crisis mitigation.

However, these alternatives operate within finite parameters:

- Russian pipelines approach capacity limits during peak demand periods

- Southeast Asian suppliers face their own domestic energy requirements

- Central Asian routes require significant lead times for capacity expansion

Manufacturing Sector Resilience Under Energy Supply Stress

China's industrial base demonstrated varying levels of resilience during the March 2026 energy supply disruptions, with certain sectors proving more adaptable to alternative input sources than others. Manufacturing industries with high petroleum dependency faced immediate operational challenges, while those with diversified supply chains or domestic input alternatives maintained higher production levels.

Petrochemical Industry Vulnerability

The petrochemical sector experienced the most severe operational constraints, given its direct dependency on crude oil and natural gas feedstocks. Processing facilities designed for specific crude oil grades faced technical challenges when switching to alternative suppliers, as different crude types require adjusted refining parameters and may produce varying output quality.

Key vulnerability factors include:

- Feedstock compatibility requirements limiting supplier flexibility

- Process optimisation delays when switching between crude oil types

- Quality control challenges maintaining product specifications with alternative inputs

- Contract fulfilment pressures from downstream customers expecting consistent supply

Steel Production Adaptation Strategies

China's steel industry, while less directly dependent on Gulf energy supplies, faced cost pressures through increased coking coal and energy expenses. Steel producers implemented several adaptation strategies, including production scheduling modifications to optimise energy consumption during lower-cost periods and supplier diversification to reduce dependency on any single energy source.

Some facilities temporarily adjusted product mix toward less energy-intensive steel grades, while others accelerated planned maintenance schedules to coincide with high energy cost periods. These operational modifications helped maintain production volumes while managing increased input costs.

Automotive Sector Supply Chain Adjustments

China's automotive manufacturing sector, producing approximately 25-30 million vehicles annually, encountered disruptions through petroleum-derived component supply chains. Plastic components, synthetic rubber, and specialised lubricants all experienced price increases and delivery delays.

Manufacturers responded by:

- Increasing inventory buffers for critical petroleum-derived components

- Accelerating supplier qualification for alternative material sources

- Adjusting production schedules to optimise component availability

- Implementing cost pass-through mechanisms to manage margin pressures

Geopolitical Risk Assessment and Strategic Response Scenarios

The duration and intensity of energy transit disruptions significantly influence appropriate response strategies, with different crisis timelines requiring distinct adaptation approaches. Short-term disruptions may be manageable through inventory drawdowns and spot market purchases, while extended crises necessitate fundamental supply chain restructuring and alternative infrastructure development.

Short-Term Crisis Management (30-Day Scenario)

During immediate crisis periods, China's strategic petroleum reserves provide crucial buffer capacity. Current reserve levels, while substantial, operate within finite timeframes that require careful management during extended disruptions. Emergency supplier activation protocols focus on maximising throughput from existing alternative relationships rather than developing new partnerships.

Key management strategies include:

- Strategic reserve utilisation at controlled depletion rates

- Spot market purchasing despite premium pricing

- Alternative route acceleration through existing partnerships

- Industry coordination to prevent competitive bidding among importers

Extended Crisis Adaptation (90-Day Scenario)

Longer disruption periods require structural adjustments that extend beyond emergency measures. Supply chain reorganisation becomes necessary as companies establish new supplier relationships and modify logistics networks. Price volatility management shifts from short-term hedging to longer-term contract renegotiation.

Extended adaptation involves:

- Infrastructure investment acceleration in alternative supply routes

- Long-term contract modification to incorporate risk premiums

- Regional partnership deepening with non-Gulf suppliers

- Domestic production capacity expansion where technically feasible

Permanent Security Premium Environment

The transformation of energy transit from operational risk to permanent geopolitical leverage creates lasting changes in trade architecture. Industry analysts have noted how the strait has evolved into a persistent geopolitical tool, suggesting that security premiums will remain embedded in energy and maritime insurance costs even after immediate hostilities cease.

This permanent risk environment requires:

- Diversified supply portfolio development reducing concentration risk

- Enhanced emergency response capabilities for rapid crisis adaptation

- Regional infrastructure investment supporting alternative transit routes

- Financial risk management evolution incorporating persistent geopolitical premiums

Economic Impact Transmission and Multiplier Effects

Energy cost increases propagate through China's economy via multiple transmission mechanisms that amplify initial disruption impacts. Manufacturing margin compression occurs as companies absorb increased input costs while maintaining competitive pricing in export markets. Currency dynamics add additional complexity as energy imports require foreign exchange, potentially affecting the renminbi's value during periods of increased import costs.

Export Competitiveness Dynamics

Rising energy costs directly impact China's export competitiveness through increased production expenses that must either be absorbed by manufacturers or passed through to international customers. Industries with high energy intensity face particular pressure, as competitors from countries with stable energy supplies gain relative cost advantages.

Furthermore, the OPEC production impact on global pricing adds another layer of complexity, as reduced production quotas amplify cost pressures beyond transit disruption effects.

Competitiveness factors include:

- Direct energy cost increases in production processes

- Transportation cost inflation affecting delivered prices

- Currency adjustment pressures from increased import requirements

- Alternative supplier premium costs compared to baseline Gulf supplies

Regional Economic Variations

Different regions within China experience varying impacts based on their industrial composition and proximity to alternative supply sources. Coastal areas with diversified port infrastructure adapt more readily to alternative shipping routes, while inland manufacturing centres dependent on pipeline supplies face greater adjustment challenges.

Regional variation factors:

- Port infrastructure capacity for handling diverted shipments

- Industrial composition determining energy intensity levels

- Alternative supplier proximity affecting transportation costs

- Local supply chain flexibility enabling rapid supplier switching

Employment and Consumer Impact Pathways

Energy supply disruptions eventually transmit to employment markets through reduced industrial production and consumer markets through increased prices for petroleum-derived products. Manufacturing sectors may implement reduced working hours or temporary production slowdowns, affecting regional employment levels in industrial centres.

Consumer price impacts emerge through multiple pathways, including direct fuel cost increases and indirect effects through transportation and manufacturing cost pass-through. These impacts vary by region and income level, with energy-intensive consumption patterns experiencing greater price pressures.

Strategic Response Framework Development

China's response to energy transit vulnerabilities involves both immediate crisis management capabilities and longer-term structural adaptations designed to reduce future exposure. Emergency response systems focus on maintaining critical supplies during disruption periods, while strategic development initiatives aim to diversify supply sources and enhance energy security resilience.

Immediate Risk Mitigation Capabilities

Strategic petroleum reserve management provides the primary immediate response tool, though reserve capacity operates within finite parameters requiring careful utilisation planning. Emergency supplier activation protocols leverage existing relationships with alternative suppliers, though capacity constraints limit expansion potential during crisis periods.

In addition to traditional supply management, governments and businesses increasingly focus on market volatility hedging strategies that help mitigate price risks during disruption periods.

Additional immediate measures include:

- Shipping route optimisation to minimise transit times and costs

- Port capacity surge activation to handle increased throughput

- Industry coordination mechanisms preventing competitive supply bidding

- Financial market stabilisation through foreign exchange management

Long-Term Security Architecture Evolution

Permanent risk mitigation requires fundamental changes in China's energy trade architecture, emphasising supply source diversification and alternative transit route development. Regional energy partnerships become increasingly important as permanent alternatives to Gulf suppliers, necessitating infrastructure investment and diplomatic relationship strengthening.

Strategic development priorities:

- Alternative supplier relationship deepening with Russia, Central Asia, and Southeast Asia

- Pipeline infrastructure expansion reducing maritime transit dependency

- Renewable energy transition acceleration decreasing overall import requirements

- Regional trade integration enhancement within Asia-Pacific frameworks

Technology Integration for Supply Chain Resilience

Advanced logistics technologies enable more effective crisis response through real-time supply chain monitoring and optimisation capabilities. Predictive analytics help identify potential disruption risks before they materialise, while automated routing systems can rapidly adjust shipping patterns during crisis periods.

Technology applications include:

- Supply chain visibility systems providing real-time disruption alerts

- Predictive risk modelling for early warning capabilities

- Automated logistics optimisation for rapid route adjustment

- Digital trade financing reducing transaction delays during crisis periods

The next major ASX story will hit our subscribers first

Investment and Financial Market Implications

Energy transit disruptions create both immediate financial pressures and longer-term investment opportunities across multiple sectors. Traditional energy sector valuations face volatility from supply uncertainty, while alternative energy infrastructure and logistics optimisation technologies attract increased investment interest.

Crisis-Driven Investment Opportunities

Infrastructure development projects supporting alternative energy supply routes present significant investment potential, particularly in pipeline construction, port facility expansion, and renewable energy generation capacity. Logistics technology companies developing supply chain resilience solutions also benefit from increased demand for risk management capabilities.

However, the broader geopolitical context, including US-China trade war impact considerations, affects investment flows and technology transfer arrangements between countries.

Key investment sectors:

- Alternative energy infrastructure including pipelines and port facilities

- Supply chain technology for disruption monitoring and optimisation

- Strategic materials processing reducing import dependency

- Regional trade facilitation services supporting alternative partnerships

Financial Risk Management Evolution

Energy supply disruptions require sophisticated financial hedging strategies that extend beyond traditional commodity price risk management. Currency hedging becomes crucial as import costs fluctuate, while supply chain financing arrangements must accommodate increased volatility and longer lead times.

Financial adaptation strategies:

- Enhanced commodity hedging incorporating supply disruption risks

- Currency risk management for volatile import cost scenarios

- Supply chain financing flexibility accommodating extended lead times

- Insurance portfolio optimisation balancing coverage with cost constraints

Market Pricing of Long-Term Risks

Financial markets increasingly incorporate permanent geopolitical risk premiums into energy sector valuations, reflecting expectations that transit route vulnerabilities will persist beyond immediate crisis periods. This permanent risk pricing affects capital allocation decisions and investment return requirements across energy-dependent industries.

Market pricing considerations:

- Permanent risk premium integration in energy sector valuations

- Supply chain resilience valuation for companies with diversified sourcing

- Regional diversification premiums for businesses with alternative market access

- Technology solution valuation for crisis management capabilities

Future Trade Architecture Evolution Scenarios

The current energy transit crisis accelerates existing trends toward supply chain diversification and regional trade integration while potentially creating permanent structural changes in global energy markets. Post-crisis trade patterns may reflect permanently higher security premiums and greater emphasis on supply source diversification.

Permanent Supply Chain Diversification Outcomes

Companies that successfully diversify supply sources during crisis periods often maintain these arrangements permanently, reducing future vulnerability while spreading risk across multiple suppliers. This diversification trend creates more complex but more resilient supply networks that can better withstand future disruptions.

Consequently, the recent oil price rally has accelerated corporate decisions to secure alternative supply arrangements, with many companies willing to accept higher costs for greater supply security.

Diversification characteristics:

- Multi-source supplier portfolios reducing single-point-of-failure risks

- Regional supply preference favouring geographically proximate sources

- Flexible contract structures enabling rapid supplier switching

- Enhanced inventory management balancing cost with security

Regional Trade Integration Acceleration

Crisis periods often accelerate regional economic integration as countries seek alternatives to disrupted global supply chains. Enhanced cooperation within Asia-Pacific frameworks becomes more attractive as a permanent alternative to Middle Eastern energy dependency.

Integration developments:

- Bilateral energy agreements with regional suppliers

- Infrastructure connectivity projects supporting alternative trade routes

- Financial system integration facilitating regional trade transactions

- Regulatory harmonisation reducing cross-border transaction costs

Technology-Driven Optimisation

Advanced logistics and supply chain technologies developed during crisis periods often provide permanent efficiency improvements that persist after crisis resolution. Digital trade platforms, predictive analytics, and automated optimisation systems become standard infrastructure supporting more resilient trade networks.

Technology integration:

- Predictive supply chain analytics for early disruption detection

- Automated route optimisation for real-time logistics adjustment

- Digital trade documentation reducing transaction processing delays

- Integrated risk management systems combining multiple risk factors

Risk Management and Preparedness Framework Development

Effective preparation for future energy transit disruptions requires comprehensive risk assessment frameworks that identify vulnerability points and develop corresponding mitigation strategies. Early warning systems enable proactive rather than reactive responses, while diversified partnership networks provide multiple options during crisis periods.

Early Warning System Development

Sophisticated monitoring systems can identify potential disruption risks before they materialise into actual supply interruptions. These systems combine geopolitical intelligence, shipping route monitoring, and supply chain analytics to provide advance warning of developing crisis situations.

Warning system components:

- Geopolitical risk monitoring tracking diplomatic and military developments

- Shipping route surveillance identifying operational disruptions

- Supplier financial monitoring detecting potential supply interruptions

- Market intelligence integration combining multiple information sources

Business Preparedness Strategies

Individual companies can implement preparedness measures that reduce vulnerability to supply disruptions while maintaining operational efficiency during normal periods. These strategies balance security with cost considerations, ensuring resilience without unnecessary expense.

Furthermore, understanding the US oil production decline and its implications helps companies develop more comprehensive contingency planning.

Preparedness elements:

- Supply chain stress testing identifying critical vulnerability points

- Alternative supplier qualification maintaining backup relationships

- Flexible inventory management optimising security with carrying costs

- Crisis response protocols enabling rapid operational adjustment

Regional Cooperation Enhancement

International cooperation frameworks can provide mutual support during crisis periods while sharing the costs of resilience infrastructure development. Regional partnerships distribute risk across multiple countries while creating economies of scale in alternative supply development.

Cooperation mechanisms:

- Joint strategic reserve management for regional crisis response

- Infrastructure cost sharing for alternative route development

- Intelligence sharing agreements for early warning enhancement

- Coordinated diplomatic initiatives addressing crisis resolution

Building Resilient Trade Architecture for Long-Term Stability

The March 2026 Strait of Hormuz crisis demonstrates how single chokepoint vulnerabilities can generate cascading disruptions across entire trade networks. Strait of Hormuz crisis impacts China trade through multiple transmission mechanisms that extend far beyond immediate energy supply constraints, affecting manufacturing operations, export competitiveness, and regional economic development patterns.

Successful adaptation requires balancing immediate crisis response capabilities with longer-term structural changes that reduce future vulnerability. Companies and governments that invest in supply chain diversification, alternative infrastructure development, and advanced risk management systems position themselves for greater resilience during future disruption periods.

The permanent integration of security premiums into energy markets reflects market expectations that geopolitical risks will persist beyond current crisis periods. This reality necessitates fundamental changes in trade architecture that prioritise resilience alongside efficiency, creating more robust but potentially more complex supply networks.

Finally, the Strait of Hormuz crisis impacts China trade patterns demonstrate the critical importance of strategic planning for maritime chokepoint vulnerabilities. As global supply chains become increasingly complex, nations must balance efficiency with security considerations to maintain economic stability during geopolitical disruptions.

Disclaimer: This analysis is based on publicly available information and scenario modelling. Trade disruption impacts, financial market responses, and policy outcomes may vary significantly from projections based on actual crisis developments, government responses, and market conditions. Readers should conduct independent research and consult appropriate professionals before making business or investment decisions based on this analysis.

Looking to Navigate Energy Market Volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, empowering subscribers to identify actionable opportunities ahead of broader market movements in the energy and commodities sectors. Start your 14-day free trial today to position yourself strategically during periods of global supply chain disruption and energy market uncertainty.