June 5, 2026

Strategic Manufacturing Transformation Through Advanced Materials

Industrial nations worldwide face unprecedented challenges in securing advanced materials for next-generation technologies. The convergence of defence modernisation, renewable energy expansion, and semiconductor innovation has created acute demand for specialised magnetic components that power everything from precision guidance systems to electric vehicle motors. This materials dependency has emerged as a critical vulnerability in global supply chains, prompting strategic responses across multiple sectors and government levels through domestic rare earth magnet production initiatives.

The rare earth permanent magnet sector represents one of the most concentrated and strategically sensitive segments within advanced materials manufacturing. Two primary magnet families dominate high-performance applications: neodymium-iron-boron (NdFeB) compositions that deliver exceptional magnetic strength-to-weight ratios, and samarium-cobalt (SmCo) variants that maintain performance under extreme temperature conditions. These materials enable technologies ranging from semiconductor fabrication equipment to missile guidance systems and lightweight aerospace components.

Understanding how domestic rare earth magnet production capabilities are reshaping industrial strategy requires examining the intersection of manufacturing capacity, supply chain resilience, and technological sovereignty. Furthermore, the mining industry evolution demonstrates how current developments suggest a fundamental shift from import-dependent procurement toward vertically integrated domestic production systems that span mining through finished component manufacturing.

When big ASX news breaks, our subscribers know first

Understanding the Strategic Foundation

Domestic rare earth magnet production encompasses a complex ecosystem of mining, separation, alloy production, magnet manufacturing, and precision assembly capabilities. Unlike conventional commodity materials, rare earth magnets require specialised processing techniques, advanced metallurgy, and stringent quality control protocols that make supply chain substitution extremely difficult once production relationships are established.

Critical applications driving demand extend far beyond traditional industrial uses. Defence systems rely on rare earth magnets for radar arrays, electronic warfare systems, and precision-guided munitions where performance reliability directly impacts mission success. Additionally, the importance of defence-critical minerals has become increasingly apparent as nations seek to secure supply chains for essential military technologies.

Renewable energy infrastructure depends on these materials for wind turbine generators and energy storage systems that must operate reliably for decades. Meanwhile, automotive electrification programmes require magnetic materials that maintain performance across temperature extremes whilst meeting cost targets for mass production.

The strategic importance of domestic production extends beyond traditional supply chain risk management. Manufacturing capability provides technology development advantages, quality control certainty, and supply surge capacity during periods of heightened demand. Companies developing integrated domestic operations can optimise material properties for specific applications whilst maintaining intellectual property protection around proprietary alloy compositions and manufacturing processes.

Barbara Humpton, Chief Executive Officer of USA Rare Earth, has emphasised that domestic production strengthens capabilities to deliver American-made magnet solutions at both scale and precision. This positioning reflects industry recognition that achieving supply chain independence requires not merely alternative sourcing arrangements, but fundamental manufacturing capabilities that support innovation and customisation for demanding applications.

Current Production Landscape Assessment

Manufacturing capacity distribution across domestic facilities reveals an emerging network of specialised production nodes, each developing particular strengths in materials processing, magnet manufacturing, or precision assembly. Moreover, the integration of data-driven operations has become crucial for optimising production efficiency and quality control across these facilities.

Technology readiness levels vary significantly across different magnet types, with NdFeB production generally more mature than SmCo manufacturing due to broader commercial applications and larger investment flows. Quality certification standards represent critical differentiators for defence and aerospace applications, where materials must meet stringent performance specifications under extreme operating conditions.

Key Production Capabilities:

- NdFeB magnet manufacturing: Higher volume, commercial applications focus

- SmCo specialised production: Lower volume, extreme environment applications

- Precision assembly operations: Custom configurations for specific applications

- Quality certification programmes: Defence and aerospace standards compliance

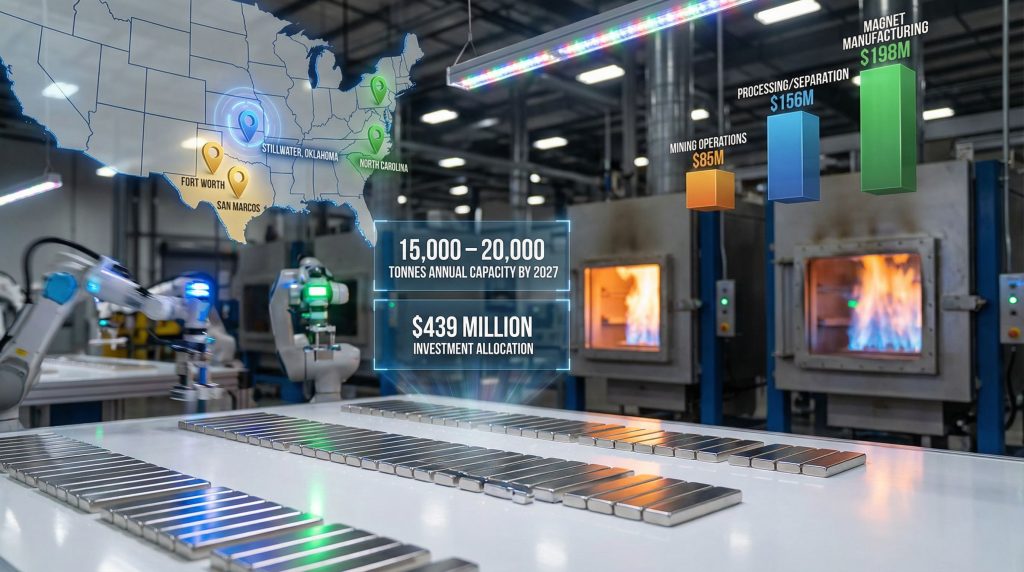

Current domestic production capacity meets approximately 10 to 15 percent of U.S. rare earth magnet demand, indicating substantial expansion requirements to achieve meaningful supply chain independence. This production gap represents both challenge and opportunity for manufacturers developing scaled operations.

Key Production Facilities Driving Domestic Capabilities

Oklahoma Innovation Centers

USA Rare Earth operates magnet manufacturing capacity in Stillwater, Oklahoma, representing a core element of domestic production infrastructure. The Oklahoma facility demonstrates the transition from laboratory-scale research to commercial manufacturing, with operations focused on NdFeB magnet production using domestic feedstock materials.

The Stillwater operations exemplify the integration challenges facing domestic manufacturers. As Barbara Humpton noted, the company is producing magnets in Oklahoma and rapidly expanding that capability as part of an integrated global value chain. This expansion occurs within the context of broader supply chain assembly, including processing, separation, metal-making, and alloy production capabilities through ownership of Less Common Metals Ltd.

Research and development capabilities at Oklahoma facilities support next-generation materials development, with ongoing work to optimise magnet performance for specific applications whilst reducing dependency on critical rare earth elements that face particular supply constraints. Furthermore, partnership networks with academic institutions provide access to advanced materials research whilst supporting workforce development for specialised manufacturing roles.

The Oklahoma manufacturing hub demonstrates how domestic rare earth magnet production requires coordination across multiple processing stages, from refined rare earth oxides through alloy production to finished magnet manufacturing and quality certification. This vertical integration approach contrasts with traditional manufacturing models that rely on specialised suppliers for each production stage.

Manufacturing Technology Platforms

Domestic facilities employ advanced powder metallurgy techniques optimised for consistent magnetic properties across production batches. These manufacturing processes require precise control of atmospheric conditions, temperature profiles, and mechanical processing parameters to achieve the magnetic performance characteristics demanded by aerospace and defence applications.

Quality control protocols extend beyond traditional materials testing to include magnetic property verification, environmental stress testing, and long-term stability assessment. These comprehensive testing programmes support certification for critical applications whilst providing data for continuous process improvement initiatives.

Manufacturing Process Elements:

- Powder preparation: Particle size optimisation and composition control

- Pressing operations: Density uniformisation and dimensional accuracy

- Sintering processes: Temperature and atmosphere control for optimal magnetic properties

- Finishing operations: Surface treatment and dimensional precision

- Quality verification: Magnetic property testing and certification

Government Investment Strategies and Production Scale Impact

Federal investment strategies targeting domestic rare earth magnet production reflect recognition that market forces alone cannot address supply chain vulnerabilities in strategically critical materials. The development of a comprehensive critical minerals strategy has become essential for coordinating these investment approaches, which span direct financial support, research and development funding, and procurement policies that provide market certainty for domestic manufacturers.

Manufacturing capability expansion programmes typically address specific bottlenecks in domestic production capacity whilst supporting technology development initiatives that improve performance and reduce costs. These programmes recognise that achieving competitive domestic production requires sustained investment over multiple years as facilities scale operations and optimise manufacturing processes.

Risk mitigation strategies embedded in government investment programmes focus on supply surge capability during crisis periods, technology preservation for national security applications, and maintaining competitive alternatives to concentrated international supply chains. Additionally, establishing a robust critical minerals reserve provides strategic buffer capacity during supply disruptions.

The effectiveness of government investment programmes depends on private sector response patterns, including leveraged investment commitments, technology development partnerships, and market expansion initiatives. Successful programmes typically combine direct financial support with regulatory frameworks that provide long-term market certainty for domestic manufacturers.

Commercial Sector Integration Patterns

Private investment leveraging government support has emerged through various partnership structures, from joint venture formations to technology licensing agreements that enable rapid capability transfer. These arrangements typically balance risk sharing with intellectual property protection whilst accelerating deployment of proven manufacturing technologies.

The USA Rare Earth and Arnold Magnetic Technologies distribution agreement exemplifies commercial sector integration strategies that expand market access without requiring shared ownership structures. Under this non-exclusive arrangement, each company markets the other's products whilst maintaining independent operations and product liability responsibilities.

Matt Blake, CEO of Arnold Magnetic Technologies, has observed that combining USA Rare Earth's magnet manufacturing platform with Arnold's precision manufacturing expertise positions both companies to serve critical markets that demand performance, reliability, and compliance. This partnership model enables expanded capabilities without the complexity of joint venture management structures.

Arnold Magnetic Technologies brings over 130 years of operating history as a manufacturer of engineered magnetic assemblies, high-performance permanent magnets, and precision components. Operating from facilities in the United States, United Kingdom, Switzerland, Thailand, and China, Arnold serves more than 2,000 customers worldwide across aerospace and defence, general industrial, motorsport, oil and gas, medical, and energy markets.

Production Volume Projections and Manufacturing Efficiency

Realistic production volume achievement by 2027 depends on successful coordination across multiple expansion projects, workforce development initiatives, and supply chain integration efforts. Manufacturing efficiency improvements during scale-up phases require addressing learning curve effects, quality consistency challenges, and specialised workforce development requirements.

Capacity expansion scenarios must account for the complex interdependencies between feedstock availability, processing capacity, magnet manufacturing capability, and finished product assembly operations. Bottlenecks at any stage can constrain overall system throughput, making coordinated expansion planning essential for achieving production targets.

The timeline for achieving meaningful domestic production scale reflects the capital-intensive nature of rare earth processing and the specialised equipment requirements for high-performance magnet manufacturing. Facilities typically require 18 to 36 months from construction initiation to commercial production, with additional time needed to achieve full capacity utilisation and quality certification for demanding applications.

Production Scaling Factors:

- Feedstock availability: Domestic mining and processing capacity constraints

- Manufacturing equipment: Specialised machinery procurement and installation timelines

- Workforce development: Technical training for specialised manufacturing roles

- Quality certification: Testing and validation for aerospace and defence applications

- Market integration: Customer qualification and supply agreement development

The next major ASX story will hit our subscribers first

Distribution Networks and Market Access Evolution

Strategic partnership models enabling expanded market access have evolved beyond traditional distributor relationships toward integrated capability sharing arrangements. Cross-marketing agreements between manufacturers create synergies that leverage complementary strengths whilst maintaining operational independence.

The USA Rare Earth and Arnold Magnetic Technologies agreement demonstrates this evolution, with each company marketing the other's magnet products to expand domestic distribution channels. USA Rare Earth offers Arnold's finished permanent magnets made from SmCo and NdFeB materials, whilst Arnold provides access to USA Rare Earth's processed NdFeB feedstock and finished magnets.

Risk sharing through non-exclusive distribution arrangements enables manufacturers to expand market coverage without exclusive dependency relationships. This approach provides flexibility for both parties whilst creating redundant pathways to market that enhance supply chain resilience for end customers.

Market access strategies must address the distinct requirements of defence contractors versus commercial customers. Defence applications typically require extensive supplier qualification processes, security clearances, and specialised testing protocols that create barriers to entry whilst providing competitive advantages once achieved.

Supply Chain Resilience Mechanisms

Redundant supplier relationships have become essential for customers seeking supply security in critical applications. The development of multiple domestic sources enables risk diversification whilst supporting competitive dynamics that benefit end users through improved service and pricing competition.

Strategic inventory management practices are evolving to balance cost efficiency with supply security, particularly for materials with long procurement cycles and specialised manufacturing requirements. Emergency production surge capabilities require maintained excess capacity that adds costs during normal operations but provides critical flexibility during supply disruptions.

Quality assurance across distributed manufacturing networks requires standardised testing protocols, shared certification processes, and coordinated technical support capabilities. These systems enable customers to qualify multiple suppliers whilst maintaining consistent performance standards across different sourcing options.

Competitive Dynamics Against International Suppliers

Cost structure analysis reveals that domestic rare earth magnet production operates with significant cost premiums compared to established international suppliers, particularly for high-volume commercial applications. However, government procurement preferences and specialised application requirements can justify these premiums, whilst commercial market penetration requires demonstrated value beyond supply security.

Quality and performance differentiation opportunities exist in specialised applications where domestic manufacturers can provide customisation, rapid response, and integrated support services that international suppliers struggle to match. Innovation advantages in next-generation magnet technologies may provide competitive positioning as performance requirements continue advancing.

Long-term cost reduction pathways through scale economies and manufacturing efficiency improvements require sustained investment and market development over multiple years. Furthermore, according to recent industry analysis by CNBC, rare earth magnet manufacturers are experiencing increased demand and market opportunities, suggesting favourable conditions for domestic expansion.

Competitive Positioning Elements:

| Factor | Domestic Advantage | International Challenge | Strategic Response |

|---|---|---|---|

| Supply Security | High reliability, surge capacity | Established cost structures | Value-based positioning for critical applications |

| Quality Control | Customisable specifications | Proven manufacturing processes | Innovation focus and specialised capabilities |

| Delivery Speed | Regional proximity, responsiveness | Global scale efficiencies | Agile manufacturing and customer integration |

| Technical Support | Direct engineering access | Established customer relationships | Integrated solution development |

Technology Innovations Driving Production Efficiency

Advanced manufacturing techniques are reducing material waste whilst improving consistency in magnetic properties across production batches. Powder metallurgy improvements enable better particle size distribution control and composition uniformity, resulting in enhanced magnetic performance and reduced rejected material rates.

Automation integration addresses both quality consistency requirements and workforce constraints in specialised manufacturing operations. Automated systems provide precise control of critical processing parameters whilst reducing human exposure to hazardous materials used in rare earth processing and magnet manufacturing.

Recycling technologies for sustainable production have emerged as both environmental and economic necessities, given the high value and limited availability of rare earth materials. End-of-life magnet recovery and reprocessing capabilities reduce feedstock requirements whilst providing cost advantages for domestic manufacturers.

Process Innovation Areas:

- Powder preparation optimisation: Enhanced particle size control and composition uniformity

- Sintering process improvements: Temperature profile optimisation and atmosphere control

- Surface treatment advances: Corrosion resistance and performance enhancement

- Recycling integration: End-of-life material recovery and reprocessing

- Quality automation: Real-time monitoring and process adjustment capabilities

Material Science Breakthroughs

Alternative rare earth compositions that reduce dependency on the most constrained elements represent critical research areas for domestic manufacturers. Research institutions such as CSIRO have provided valuable insights into rare earth processing and applications, helping inform substitution strategies that must balance performance requirements against material availability whilst maintaining cost competitiveness for target applications.

Coating technologies that extend magnet lifespan in demanding environments provide value differentiation opportunities for domestic manufacturers serving aerospace and defence markets. Advanced surface treatments can significantly improve corrosion resistance and thermal stability, justifying premium pricing for critical applications.

Performance optimisation for specific applications enables domestic manufacturers to compete through customisation rather than purely on cost basis. Tailored magnetic properties, specialised geometries, and integrated assembly capabilities create value propositions that commodity suppliers cannot easily replicate.

Market Applications Influencing Production Strategies

Defence and aerospace requirements drive production protocols that emphasise reliability, traceability, and performance consistency over cost minimisation. Qualification standards for these applications require extensive testing, documentation, and supplier certification processes that create competitive barriers whilst ensuring material performance under extreme conditions.

Security clearance considerations for personnel working on defence applications add complexity and cost to manufacturing operations whilst providing competitive advantages once achieved. These requirements limit the supplier base whilst creating stable, long-term relationships with qualified manufacturers.

Commercial market segments present different optimisation priorities, with electric vehicle applications emphasising cost efficiency and manufacturing scale, whilst wind energy applications prioritise durability and long-term performance stability. Each segment requires tailored approaches to material specifications and manufacturing processes.

Application-Specific Requirements:

- Defence systems: Maximum reliability, extensive qualification, security protocols

- Aerospace components: Weight optimisation, extreme environment performance, traceability

- Electric vehicle motors: Cost efficiency, high-volume production, consistent quality

- Wind turbine generators: Durability, maintenance minimisation, environmental resistance

- Industrial automation: Precision specifications, specialised configurations, technical support

Emerging Application Areas

Energy storage system components represent growing opportunities for specialised magnet applications, particularly in grid-scale storage systems that require long-term stability and predictable performance characteristics. These applications often justify premium pricing for superior materials and manufacturing quality.

Advanced robotics and automation systems increasingly require high-performance magnets for precision motor applications, sensor systems, and magnetic levitation technologies. These emerging markets provide opportunities for domestic manufacturers to establish positions in growing technology segments.

Medical device applications demanding biocompatible materials and specialised performance characteristics create niche opportunities where customisation capabilities and regulatory compliance provide competitive advantages for domestic manufacturers with appropriate certifications.

Long-term Strategic Implications for U.S. Manufacturing

Supply chain independence scenarios require coordinated development across mining, processing, manufacturing, and assembly capabilities to create truly resilient domestic supply chains. Timeline projections for achieving strategic autonomy suggest decade-long development periods requiring sustained investment and policy support.

Critical dependency reduction across key applications must balance strategic objectives with economic efficiency, recognising that complete supply independence may not be economically justifiable for all applications. Consequently, selective independence in the most critical applications may provide optimal resource allocation whilst maintaining strategic flexibility.

Allied nation collaboration opportunities can extend effective supply chain resilience beyond purely domestic production by creating trusted supplier networks that reduce dependency on potentially hostile sources. These relationships require diplomatic coordination alongside industrial cooperation to achieve sustainable strategic benefits.

Economic impact projections suggest that domestic rare earth magnet production could support thousands of specialised manufacturing jobs whilst creating multiplier effects in related industries including mining, processing, and advanced manufacturing equipment sectors.

Strategic Outcome Indicators:

- Supply independence metrics: Percentage of critical applications served by domestic sources

- Economic impact measures: Employment creation, trade balance improvement, regional development

- Innovation advancement: Technology development, intellectual property creation, competitive positioning

- Allied partnership strength: Collaborative production capabilities, shared technology development

- Crisis response capacity: Supply surge capabilities, strategic stockpile management, emergency production protocols

Investment and Growth Outlook

Private sector confidence in domestic rare earth magnet production continues developing as government policies provide market certainty and investment incentives reduce financial risks. Technology advancement requirements for maintaining competitiveness demand sustained research and development investment alongside manufacturing capacity expansion.

Market expansion opportunities in allied nations could provide additional scale for domestic manufacturers whilst supporting strategic objectives of reducing global dependency on concentrated supply sources. Export potential requires coordination with international partners to develop trusted supplier relationships and compatible technical standards.

Risk management considerations must address geopolitical supply disruption scenarios, environmental compliance requirements, and workforce development challenges that could constrain growth. Successful domestic rare earth magnet production requires addressing these interconnected challenges through comprehensive strategic planning and sustained commitment across both public and private sectors.

Investment Disclaimer: This analysis contains forward-looking projections based on current industry developments and government policies. Actual production capacity, market dynamics, and competitive positioning may differ significantly from projections due to technological, regulatory, or market changes. Investors should conduct independent due diligence and consider multiple scenarios when evaluating opportunities in the rare earth magnet sector.

Seeking Your Next Strategic Investment Opportunity?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why historic discoveries can generate substantial returns by exploring major breakthrough announcements, then begin your 14-day free trial today to position yourself ahead of the market.