August 4, 2026

Strategic Reserve Rebalancing in an Era of Monetary Uncertainty

Global monetary authorities face unprecedented challenges as traditional reserve management frameworks confront structural inflation pressures, geopolitical fragmentation, and fiscal sustainability concerns. The institutional response has been decisive: a fundamental shift toward physical asset accumulation that represents the most sustained period of central bank gold buying in modern financial history.

This transformation extends beyond tactical allocation decisions. Central banks worldwide are actively reconstructing reserve portfolios to address systematic vulnerabilities embedded within post-Bretton Woods monetary architecture, where unlimited currency creation creates persistent debasement pressures against finite physical assets.

When big ASX news breaks, our subscribers know first

Institutional Gold Accumulation Reaches Historic Proportions

Central bank gold buying has achieved remarkable consistency, with monetary authorities maintaining net purchase positions for 16 consecutive years through 2025. This institutional behaviour reverses a three-decade selling trend that characterised central bank activity from the 1980s through 2000s.

The scale of accumulation demonstrates systematic rather than opportunistic positioning. Furthermore, recent gold price forecast analyses suggest this institutional demand continues to support market fundamentals.

Annual Purchase Volumes (2020-2025)

| Year | Net Purchases (Tonnes) | Year-over-Year Change | Leading Buyers |

|---|---|---|---|

| 2020 | 273 | -59% | Turkey, India, Uzbekistan |

| 2021 | 463 | +70% | Thailand, Brazil, Hungary |

| 2022 | 1,082 | +134% | Turkey, China, Egypt |

| 2023 | 1,037 | -4% | Singapore, China, Poland |

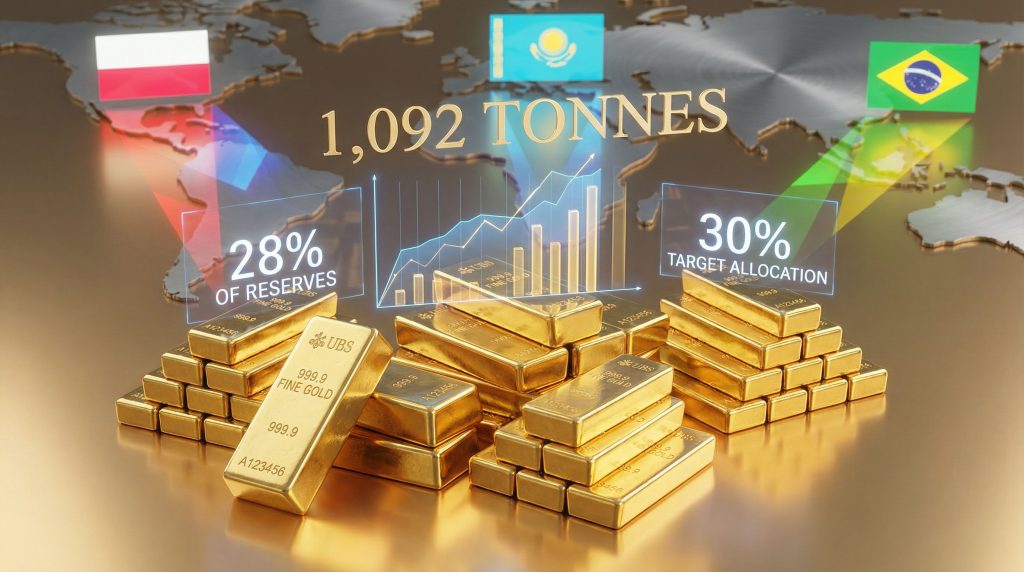

| 2024 | 1,092 | +5% | Poland, India, Kazakhstan |

| 2025 | 863 | -21% | Poland, Brazil, Czech Republic |

Source: World Gold Council Gold Demand Trends Reports

Mathematical Supply Constraints Create Structural Price Support

Central bank gold buying now represents 25-35% of annual global demand against mine production of approximately 3,200 tonnes yearly. This mathematical relationship creates structural supply constraints that must be resolved through either:

- Recycling expansion: Increased scrap metal recovery and processing

- Investment liquidation: Retail and institutional selling to satisfy institutional demand

- Price appreciation: Market clearing mechanisms that balance supply and demand

With institutional buyers demonstrating consistent accumulation regardless of price levels, the burden of adjustment falls primarily on other market participants. In addition, the historic gold surge demonstrates how sustained demand can drive exceptional price performance.

Risk Management Frameworks Drive Institutional Demand

Counterparty Risk Elimination Through Physical Assets

Modern central bank risk management explicitly distinguishes between:

Credit Risk Assets

- Government bonds carrying issuer default probability

- Currency holdings dependent on sovereign policy decisions

- Digital assets subject to technological or institutional failure

Zero-Counterparty Risk Assets

- Physical gold held in allocated storage arrangements

- Specific bars maintained in segregated vault systems

- Direct ownership eliminating institutional dependencies

The Bank for International Settlements research confirms that central bank gold buying reflects institutional recognition that physical assets provide unique risk characteristics unavailable through financial instruments.

Geopolitical Insurance Against Financial System Fragmentation

Recent precedents demonstrate how political decisions can freeze access to reserve assets:

- Russian reserves: $300+ billion frozen through SWIFT restrictions (2022)

- Venezuelan gold: Bank of England custody disputes (2019-present)

- Iranian assets: Blocked through international payment systems

These cases illustrate systematic vulnerability within digital financial infrastructure, where assets exist as database entries subject to jurisdictional control rather than physical possession.

Central bank gold buying provides insurance against such scenarios through assets that cannot be digitally frozen, sanctioned, or seized through financial networks. Consequently, the central banks' gold reserves data shows increasing emphasis on domestic storage arrangements.

Portfolio Diversification Beyond Dollar Dependency

Measured Reserve Recomposition Strategy

IMF Currency Composition of Official Foreign Exchange Reserves (COFER) data documents systematic diversification:

- 2017: Dollar share approximately 65% of global reserves

- 2025: Dollar share below 57% of global reserves

- Net reallocation: 8-9 percentage points across $12-13 trillion reserve base

- Capital flow: Estimated $840-910 billion redirected toward alternative assets

This diversification occurs through gradual rebalancing rather than wholesale abandonment, with gold serving as a primary alternative allocation target. Moreover, US economic challenges contribute to this strategic rebalancing as institutions seek protection from dollar dependency.

Multi-Asset Reserve Architecture Development

Contemporary central banks construct reserves across multiple asset categories:

Operational Liquidity (40-50%)

- Short-term government securities for immediate market intervention

- Currency swap arrangements for international payment obligations

- Money market instruments providing daily liquidity management

Strategic Diversification (30-40%)

- Physical gold eliminating counterparty exposure

- Non-dollar currency holdings reducing concentration risk

- Special Drawing Rights (SDRs) providing multilateral alternatives

Yield Enhancement (10-20%)

- Longer-duration securities generating portfolio returns

- Equity positions in select jurisdictions

- Alternative investments approved under reserve management mandates

This architecture balances immediate operational needs with long-term wealth preservation objectives.

Regional Accumulation Patterns Reflect Geopolitical Positioning

Eastern European Leadership in Gold Allocation

Poland exemplifies aggressive institutional accumulation, purchasing 90 tonnes in 2024 and maintaining consistent buying through 2025. Polish central bank authorities updated their gold reserve target from 20% to 30% of total reserves in October 2025, representing one of the most explicit institutional commitments to gold allocation globally.

This target reflects geographic proximity to geopolitical instability and explicit hedging against regional conflicts that could disrupt traditional financial relationships.

Hungary maintains 94.5 tonnes representing 33% of reserves, the highest allocation percentage among major central banks. This positioning demonstrates institutional willingness to prioritise wealth preservation over yield generation.

Asian Strategic Accumulation Patterns

Kazakhstan holds 387 tonnes (15% of reserves) with consistent annual additions regardless of market pricing. As the world's eighth-largest gold producer, Kazakhstan retains domestic production for reserves rather than international sales, creating structural demand independent of market conditions.

India maintains 822 tonnes (approximately 8% of reserves) through steady institutional buying across multiple price cycles. This approach reflects long-term reserve diversification strategy that operates independently of short-term market timing considerations.

China reports 2,264 tonnes but likely understates actual holdings due to strategic disclosure policies. Chinese accumulation occurs through both official central bank purchases and state-controlled entity acquisitions that may not appear in public statistics.

Economic Conditions Accelerating Institutional Gold Demand

Real Interest Rate Environment Analysis

When inflation-adjusted yields approach or fall below zero, gold becomes more attractive relative to yield-bearing assets. Current conditions show:

- 10-Year TIPS yields: Fluctuating around real zero

- Inflation expectations: Persistently above 2.5% annually

- Policy rate positioning: Central bank rates lagging inflation in multiple jurisdictions

This environment eliminates gold's traditional opportunity cost (foregone interest income) while maintaining its inflation protection characteristics. However, understanding gold and stock cycles becomes crucial for optimal portfolio allocation timing.

Fiscal Sustainability Concerns Create Debasement Incentives

Rising government debt levels globally create incentives for central bank gold buying as insurance against currency debasement:

Critical Debt Trajectory Indicators

- U.S. federal debt: $36.8 trillion approaching 130% of GDP

- European sovereign debt: Elevated post-COVID levels across major economies

- Emerging market debt: Sustainability questions amid dollar strength cycles

High debt levels constrain monetary policy options, potentially leading to financial repression or currency debasement scenarios where gold provides superior wealth preservation.

The next major ASX story will hit our subscribers first

Storage and Custody Infrastructure Evolution

Domestic Repatriation Movement Gains Momentum

World Gold Council data shows 68% of central banks now store gold domestically, up from approximately 50% in 2020. This shift reflects:

Reduced Dependency Benefits

- Elimination of external custody relationships and associated fees

- Direct physical control during periods of international tension

- Rapid verification and mobilisation capability during crises

Infrastructure Investment Requirements

- Construction of sovereign storage facilities meeting international standards

- Implementation of security systems equivalent to traditional custody centres

- Development of domestic assaying and verification capabilities

Allocated vs. Pool Storage Considerations

Central banks increasingly demand allocated storage arrangements where specific bars are held in segregated accounts rather than unallocated pool arrangements that create counterparty exposure.

Allocated Storage Advantages

- Direct ownership of identifiable physical assets

- Elimination of pooled storage risks where institutions commingle holdings

- Legal clarity regarding ownership claims during institutional stress

Operational Implementation

- Higher storage costs offset by eliminated counterparty risk

- Enhanced audit and verification procedures

- Simplified repatriation processes during geopolitical tensions

Market Structure Implications of Sustained Institutional Buying

Supply-Demand Fundamental Analysis

Annual Supply Sources

- Mine production: ~3,200 tonnes

- Recycling and scrap recovery: ~1,200-1,400 tonnes

- Central bank sales: Minimal (net buyers for 16 years)

- Investment liquidation: Variable based on market conditions

Annual Demand Components

- Central bank gold buying: 800-1,100 tonnes (25-35% of total demand)

- Jewellery fabrication: ~2,000-2,200 tonnes

- Industrial applications: ~300-400 tonnes

- Investment demand: 200-800 tonnes (highly variable)

With institutional demand representing such a substantial portion of annual consumption, central bank gold buying creates mathematical constraints on supply availability for other market participants. For instance, effective gold investment strategies must account for this structural demand component.

Price Discovery and Market Behaviour Implications

Institutional buying occurs through different channels than retail investment:

Central Bank Purchase Methods

- Gradual accumulation through regular small transactions

- Direct producer purchases avoiding spot market impact

- Strategic timing during market corrections for cost averaging

Market Impact Characteristics

- Reduced volatility due to steady institutional demand

- Price floor effects during market corrections

- Sustained support independent of speculative positioning

This institutional approach creates price stability mechanisms that differ from traditional commodity market dynamics.

Investment Framework Lessons for Portfolio Construction

Institutional Allocation Methodologies

Central bank allocation targets provide frameworks for individual portfolio construction:

Conservative Allocation Range (5-15%)

- Reflects established central bank holdings in developed markets

- Prioritises stability over growth potential

- Suitable for wealth preservation objectives

Moderate Allocation Range (10-20%)

- Mirrors active accumulator central bank strategies

- Balances insurance benefits with growth asset allocation

- Appropriate for balanced risk tolerance profiles

Aggressive Allocation Range (20-30%)

- Matches leading central bank targets (Poland, Hungary)

- Emphasises protection against systematic monetary risks

- Suitable for high-concern scenarios regarding currency stability

Risk Management Parallel Applications

Central bank gold buying demonstrates institutional risk management principles applicable to individual portfolios:

Systematic Risk Hedging

- Gold protects against broad financial system stress

- Provides performance during currency debasement periods

- Maintains value during equity market corrections

Geographic Diversification Strategy

- Reduces portfolio dependence on single-country economic performance

- Provides exposure to global rather than domestic monetary conditions

- Creates hedge against home-country specific political risks

Long-Term Wealth Preservation Focus

- Emphasises purchasing power maintenance over yield generation

- Operates independently of short-term market timing decisions

- Provides intergenerational wealth transfer capabilities

Geopolitical Factors Reshaping Reserve Management

Financial System Fragmentation Accelerates

The 2022 freezing of Russian foreign exchange reserves created institutional precedent demonstrating how traditional reserve assets can become inaccessible through political decisions. This event accelerated central bank gold buying among nations concerned about similar vulnerabilities.

Jurisdictional Risk Assessment

- Assets held in foreign financial centres subject to host country legal decisions

- Digital holdings vulnerable to payment system restrictions

- Physical gold stored domestically eliminates jurisdictional exposure

Alternative Payment Infrastructure Development

Bilateral trade agreements increasingly include provisions for non-dollar settlement, with gold serving as neutral collateral or settlement asset:

BRICS Payment System Evolution

- Development of alternatives to SWIFT messaging infrastructure

- Gold-backed settlement mechanisms for international trade

- Reduced dependency on dollar-denominated clearing systems

Regional Currency Integration

- Increased use of local currencies for bilateral trade settlement

- Gold serving as neutral reserve asset across currency systems

- Hedging against single-currency system vulnerabilities

Future Monetary System Architecture Implications

Central Bank Digital Currency Integration

As central banks develop digital currency infrastructure, gold provides unique complementary characteristics:

Physical Anchor Function

- Tangible backing for digital currency systems

- Hedge against technological failures or cyber attacks

- Historical precedent for monetary system confidence

International Settlement Applications

- Neutral asset for cross-border CBDC transfers

- Collateral for international digital payment systems

- Bridge asset between competing digital currency standards

Crisis Liquidity Provision Capabilities

Central banks view gold as ultimate liquidity source mobilisable during extreme financial stress:

Emergency Intervention Tools

- Gold lending facilities during banking system stress

- Collateral for international emergency funding arrangements

- Asset sales capability for fiscal emergency funding

Monetary System Confidence Mechanisms

- Visible reserves supporting currency credibility

- Historical association with monetary system stability

- Public confidence anchor during financial crises

Strategic Portfolio Positioning Insights

Central bank gold buying reflects institutional recognition of converging structural trends that individual investors should consider:

Monetary System Transition Risks

- Post-Bretton Woods dollar system faces structural pressures from high debt levels

- Alternative currency arrangements gaining institutional support

- Physical assets provide hedge against systematic monetary changes

Geopolitical Fragmentation Implications

- International financial system becoming less integrated due to political tensions

- Assets held outside traditional financial centres gain strategic value

- Direct ownership reduces dependency on institutional relationships

Portfolio Optimisation Benefits

- Gold provides uncorrelated returns during equity market stress

- Inflation protection characteristics complement bond allocations

- Crisis performance historically superior to traditional safe haven assets

The 16-year institutional trend toward central bank gold buying represents more than tactical allocation decisions. It signals fundamental reassessment of monetary system stability and the importance of assets that exist outside traditional financial infrastructure.

For individual investors, central bank behaviour offers proven frameworks for long-term wealth preservation and systematic risk management during periods of monetary uncertainty.

Investment Disclaimer: This analysis is provided for educational purposes only and does not constitute investment advice. Past performance does not guarantee future results. Precious metals investments involve risks including price volatility and liquidity considerations. Consult qualified financial advisors before making investment decisions.

Looking to Position Ahead of the Next Major Gold Discovery?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, helping investors capitalise on opportunities before broader market recognition. Explore how historic discoveries have generated exceptional returns and begin your 14-day free trial today to secure your market-leading advantage in the evolving precious metals landscape.