June 7, 2026

Structural Market Forces Reshaping Queensland's Resource Economy

Queensland's resource sector operates within a complex web of global demand cycles, technological shifts, and fiscal policy frameworks that extend far beyond traditional commodity price movements. The coal royalties impact on Queensland economy reflects broader economic principles of resource extraction taxation, where government revenue systems attempt to capture economic rent while maintaining industry competitiveness.

The intersection of international supply chains, environmental regulations, and technological advancement creates multiple pressure points across Queensland's resource economy. These forces compound through regional employment networks, infrastructure dependencies, and capital allocation decisions that ripple through both urban centres and remote mining communities.

When big ASX news breaks, our subscribers know first

Understanding Queensland's Progressive Fiscal Framework

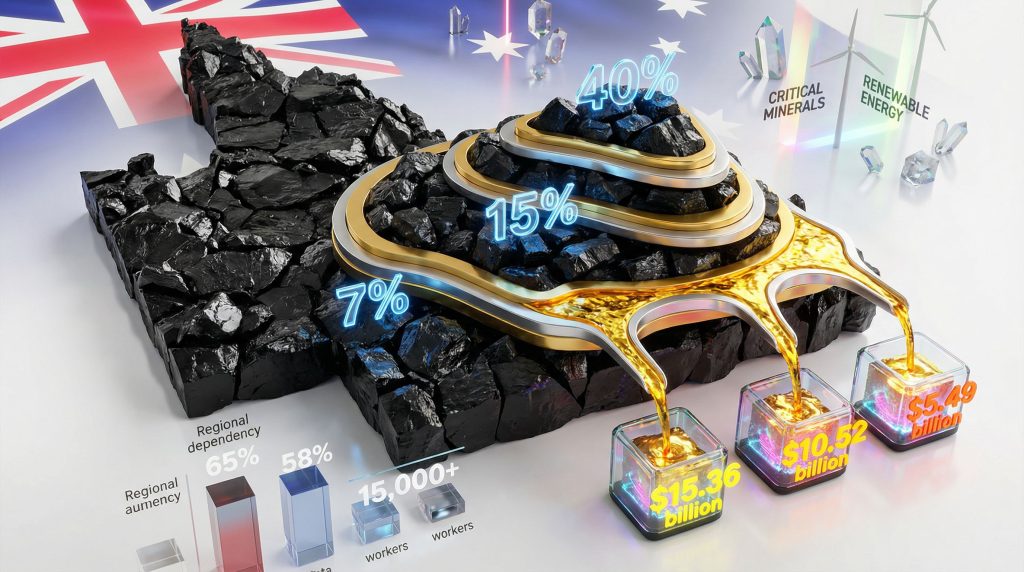

Queensland's royalty architecture operates through a sophisticated tiered mechanism designed to automatically adjust government revenue capture based on commodity price cycles. The structure begins with a base rate of 7% for coal priced below $100 per tonne, escalating progressively to reach 40% for prices exceeding $300 per tonne.

This progressive framework functions as an economic stabiliser during commodity supercycles, though recent Queensland Treasury data reveals significant volatility in actual revenue collection. The 2024-25 mid-year budget update documented royalty revenue expectations of $7.984 billion, representing a substantial $4.787 billion decline (37.5%) from the previous financial year.

Furthermore, understanding these industry evolution trends becomes essential when evaluating how Queensland's fiscal policies adapt to changing market conditions.

Revenue Collection Dynamics Across Price Tiers

The tiered structure creates distinct operational environments for mining companies depending on prevailing market conditions. During peak pricing periods experienced in 2021-2023, many operations faced effective royalty rates reaching the upper tiers of 30-40%, fundamentally altering project economics and investment return calculations.

Current market conditions demonstrate the system's volatility challenges. The Queensland Resources Council notes that numerous companies continue paying premium royalty rates while absorbing elevated operational costs. This dual pressure constrains sector growth prospects and affects regional employment stability.

| Price Threshold | Royalty Rate | Market Impact |

|---|---|---|

| Below $100/tonne | 7% | Minimal fiscal burden during downturns |

| $100-175/tonne | 15% | Moderate revenue generation |

| $175-250/tonne | 20% | Increased government revenue capture |

| Above $250/tonne | 30-40% | Maximum extraction during boom periods |

Economic Multiplier Effects and Regional Employment Networks

The coal sector's economic footprint extends substantially beyond direct mining operations, creating cascading effects throughout Queensland's regional economies. Verified data indicates the coal sector contributed $76 billion to Queensland's economy while supporting more than 363,000 local jobs during 2024-25.

These employment figures represent direct positions within coal operations. However, broader economic impact assessments suggest additional indirect employment through service industries, equipment suppliers, and regional business networks. The Queensland resources sector overall contributed $115.2 billion and supported close to 555,000 jobs, indicating coal's dominant position within the state's resource economy.

Regional Economic Concentration Patterns

Central Queensland and coastal regions demonstrate the highest economic dependency ratios on coal-related activities. These areas experience amplified effects during both boom and downturn cycles, with employment volatility creating significant social and economic challenges for regional communities.

Recent analysis indicates direct spending in regional Queensland fell by $3.44 billion, reflecting the immediate impact of reduced coal sector activity on local economies. This decline affects everything from housing markets to retail spending, demonstrating the broad economic multiplier effects of resource sector performance.

Moreover, Coal royalty revenue underpins Queensland's economic foundations, though the system faces increasing scrutiny regarding its long-term sustainability.

Key Employment Metrics:

- Direct coal employment: 363,000+ workers across Queensland

- Total resources sector employment: 555,000+ positions

- Economic contribution ratio: Coal represents approximately 66% of total resources sector contribution

- Regional spending decline: $3.44 billion reduction in direct regional expenditure

Investment Capital Allocation Under Royalty Pressure

The progressive royalty structure creates complex investment decision frameworks that influence long-term capital deployment across Queensland's coal sector. During elevated price periods, effective royalty rates substantially increase project cost structures, requiring higher return thresholds to justify new investments.

Industry leadership acknowledges that many operations currently face royalty burdens at the 30-40% tiers while simultaneously managing increased operational costs. This combination constrains sector expansion and limits new project development, with implications for employment growth and regional economic development.

Consequently, the commodity prices impact on Queensland's coal sector becomes increasingly complex when viewed through the lens of progressive royalty structures.

Capital Investment Decision Matrices

High Price Scenarios ($250+ per tonne):

- Royalty burden reaches 30-40% of revenue

- Projects require significantly higher return thresholds

- Capital allocation favours brownfield expansions over greenfield developments

- Risk tolerance decreases due to elevated government take

Moderate Price Scenarios ($150-250 per tonne):

- Royalty burden ranges 15-25% of revenue

- Standard investment criteria remain applicable

- Balanced capital allocation between expansion and new projects

- Moderate risk tolerance for development projects

Low Price Scenarios (Below $150 per tonne):

- Royalty burden minimised to 7-15% of revenue

- Lower hurdle rates enable marginal project consideration

- Focus shifts to operational efficiency and cost reduction

- Emphasis on preserving existing operations rather than expansion

Structural Revenue Volatility and Fiscal Planning Challenges

Queensland's fiscal planning confronts inherent challenges due to coal royalty volatility, with revenue fluctuations creating budgetary uncertainty that affects state government spending capacity and regional investment planning. The dramatic revenue decline documented in the 2024-25 budget update illustrates these challenges.

The $4.787 billion year-over-year decline in royalty revenue stems from multiple factors, including lower export volumes and faster-than-anticipated declines in hard coking coal prices. These factors were partially offset by a weaker Australian dollar, though the net impact remains substantially negative for state revenue.

Furthermore, those developing their investment strategy 2025 must account for this revenue volatility when considering Queensland's resource sector exposure.

Budget Planning Under Resource Revenue Uncertainty

Government budget processes must account for significant revenue volatility when coal royalties represent a substantial portion of total state income. The current forecast of $5.4 billion in coal royalties for the financial year demonstrates the ongoing importance of this revenue stream despite recent declines.

Revenue Decline Analysis:

- 2024-25 Budget Forecast: Originally higher than current $7.984 billion

- Actual Mid-Year Update: $7.984 billion (revised downward)

- Coal-Specific Forecast: $5.4 billion for current financial year

- Primary Decline Factors: Export volume reductions, price deterioration

This volatility necessitates sophisticated fiscal management strategies, including conservative revenue assumptions and potential stabilisation mechanisms to smooth spending capacity during commodity cycles.

Operational Cost Dynamics and Industry Sustainability

Rising operational costs compound the pressure created by high royalty rates, creating margin compression that affects industry sustainability and employment stability. Industry representatives emphasise that companies face dual pressures from both elevated government royalty takes and increased production costs.

The Queensland Resources Council has highlighted that operational cost increases affect companies across all commodity price tiers, reducing the sector's ability to absorb high royalty rates during market downturns. This cost pressure influences employment decisions and investment allocation across regional operations.

Cost Structure Pressures

Primary Cost Escalation Factors:

- Labour and skilled workforce: Wage inflation affecting regional mining communities

- Equipment and maintenance: Supply chain pressures increasing machinery costs

- Regulatory compliance: Environmental and safety requirement costs

- Energy and fuel: Transportation and processing cost increases

- Infrastructure maintenance: Port and rail network cost escalation

These cost pressures create challenges for maintaining employment levels during periods of reduced commodity prices, particularly when combined with high royalty obligations that cannot be easily adjusted based on operational profitability.

The next major ASX story will hit our subscribers first

Regional Economic Dependencies and Policy Constraints

Regional Queensland's economic structure creates significant political and policy constraints around royalty adjustments, as many communities derive substantial portions of their economic activity from coal operations. The interconnected nature of regional economies means royalty policy decisions affect employment, business activity, and community sustainability across multiple sectors.

The $3.44 billion decline in direct regional spending demonstrates the immediate impact of reduced coal sector activity on communities that have developed around mining operations. These effects extend beyond direct employment to affect local businesses, service providers, and infrastructure utilisation.

In addition, Queensland coal mining industry faces new regulatory pressures as the state government balances economic needs with environmental concerns.

Community Economic Dependency Analysis

Regional centres across Central Queensland and the Mackay region demonstrate high dependency ratios on coal-related economic activity. These communities face particular vulnerability during industry downturns, with limited economic diversification to offset reduced mining activity.

The Queensland Resources Council leadership anticipates continued challenges for regional Queensland, including potential job losses and reduced royalty flows back to regional communities. This outlook reflects the structural economic dependencies that constrain policy flexibility around royalty adjustments.

Regional Impact Factors:

- Employment concentration: High percentages of regional workforce in coal-related positions

- Business network effects: Service industries dependent on mining sector spending

- Infrastructure utilisation: Transport and port facilities designed for resource exports

- Community sustainability: Local government revenue and service capacity linked to mining activity

Global Market Positioning and Competitive Dynamics

Queensland's position within international coal markets influences the state's ability to maintain elevated royalty rates without compromising market share or investment attractiveness. The interaction between global supply dynamics, environmental policies in importing nations, and competing supply sources affects optimal royalty policy settings.

The recent faster-than-expected decline in hard coking coal prices reflects broader global market pressures, including demand shifts in major importing countries and increased competition from alternative suppliers. These factors constrain Queensland's pricing power and affect the effectiveness of progressive royalty structures.

For instance, examining the global mining landscape reveals how Queensland competes with other major coal-producing regions worldwide.

Market Positioning Considerations

Competitive Advantages:

- Geographic proximity: Reduced transportation costs to Asian markets

- Infrastructure networks: Established port and rail systems

- Operational reliability: Consistent supply chain performance

- Resource quality: Coal specifications meeting international demand requirements

Market Challenges:

- Environmental policy shifts: Importing country policies affecting demand

- Alternative supply development: Competing regions expanding production capacity

- Technology transitions: Long-term demand uncertainty due to energy transitions

- Price volatility: Global supply-demand imbalances affecting pricing stability

Economic Transition Strategies and Diversification Planning

Queensland's long-term economic planning increasingly emphasises diversification away from traditional coal dependence while maintaining the sector's substantial contribution during transition periods. This approach requires careful balance between supporting existing industries and developing alternative economic foundations.

The Queensland Resources Council emphasises the sector's potential role in addressing economic challenges, provided appropriate policy settings attract continued investment. This perspective highlights the importance of maintaining industry viability during transition periods while developing alternative economic activities.

However, US tariffs and inflation trends may also influence Queensland's export competitiveness in global markets.

Transition Investment Framework

Immediate Development Priorities (2025-2027):

- Critical minerals processing: Developing downstream processing capabilities

- Renewable energy infrastructure: Solar and wind project development

- Port diversification: Expanding facility capabilities beyond coal exports

- Workforce development: Retraining programmes for transitioning workers

Medium-term Objectives (2027-2030):

- Advanced manufacturing: Technology-intensive production facilities

- Regional economic diversification: Tourism and agricultural value-adding

- Infrastructure modernisation: Transport networks supporting multiple industries

- Innovation ecosystem development: Research and development capabilities

Long-term Vision (2030+):

- Hydrogen production and export: Clean energy industry development

- Carbon management technologies: Storage and utilisation capabilities

- Circular economy initiatives: Waste reduction and resource efficiency

- Knowledge economy expansion: Service and technology sector growth

Policy Implications and Economic Outlook

Queensland's coal royalty system requires careful calibration to balance revenue maximisation with industry sustainability, particularly during commodity price downturns when both government revenue and industry profitability face pressure. The current environment demonstrates these competing priorities.

Industry representatives emphasise the importance of policy settings that attract investment while recognising government fiscal requirements during challenging economic periods. This balance becomes particularly critical when royalty revenues decline substantially, as demonstrated in the current budget cycle.

The coal royalties impact on Queensland economy remains a complex issue requiring ongoing evaluation and adjustment to maintain the state's competitive position while ensuring sustainable revenue generation.

Strategic Considerations for Policy Development

Fiscal Policy Balance:

- Revenue optimisation: Maximising government income without compromising industry viability

- Investment attraction: Maintaining competitive investment environment

- Regional support: Ensuring policy settings support affected communities

- Transition facilitation: Enabling economic diversification while maintaining current contributions

Economic Sustainability Factors:

- Employment stability: Protecting regional job markets during transition periods

- Infrastructure utilisation: Maintaining asset productivity across economic cycles

- Community resilience: Supporting regional economies through industry changes

- Competitive positioning: Preserving Queensland's market advantages in global markets

The state's economic future depends on successfully managing the transition from resource dependence while preserving the substantial benefits that coal extraction provides to Queensland's prosperity and Australia's export earnings. This transition requires sophisticated policy coordination across multiple government levels and industry sectors.

Disclaimer: This analysis is based on publicly available information and should not be considered as financial or investment advice. Coal royalties impact on Queensland economy involves complex factors that may change rapidly based on global market conditions, policy decisions, and economic circumstances. Readers should consult appropriate professional advisors for specific investment or policy guidance.

Looking for Early-Stage Queensland Resource Investment Opportunities?

Discovery Alert's proprietary Discovery IQ model monitors ASX mineral discovery announcements in real-time, including emerging opportunities from Queensland's dynamic resource sector. With significant royalty revenue shifts affecting established operations, identifying breakthrough discoveries before market recognition could position investors ahead of major structural changes across Australia's mining landscape.