May 12, 2026

Silver's Industrial Renaissance and the Case for Domestic Primary Production

The global silver market is undergoing a structural transformation that few commodity cycles can match. Unlike gold, which derives the vast majority of its demand from jewellery and investment flows, silver's dual role sits at the intersection of monetary history and modern industrial necessity. Solar photovoltaic manufacturing, electric vehicle systems, advanced electronics, and defence applications are collectively reshaping what it means to hold silver in a portfolio. Yet despite this demand surge, the supply side of the equation has remained stubbornly constrained.

Most silver produced globally arrives as a by-product of base metal mining, meaning primary silver production capacity has not kept pace with the evolution of end-use markets. Against this backdrop, the emergence of a large-scale, high-grade primary silver development in the United States carries significance that extends well beyond a single corporate fundraising event. The Sunshine Silver IPO Idaho mine return to production is precisely the kind of structural supply response that analysts have flagged as overdue.

When big ASX news breaks, our subscribers know first

What the Sunshine Silver IPO Signals for North American Supply Chains

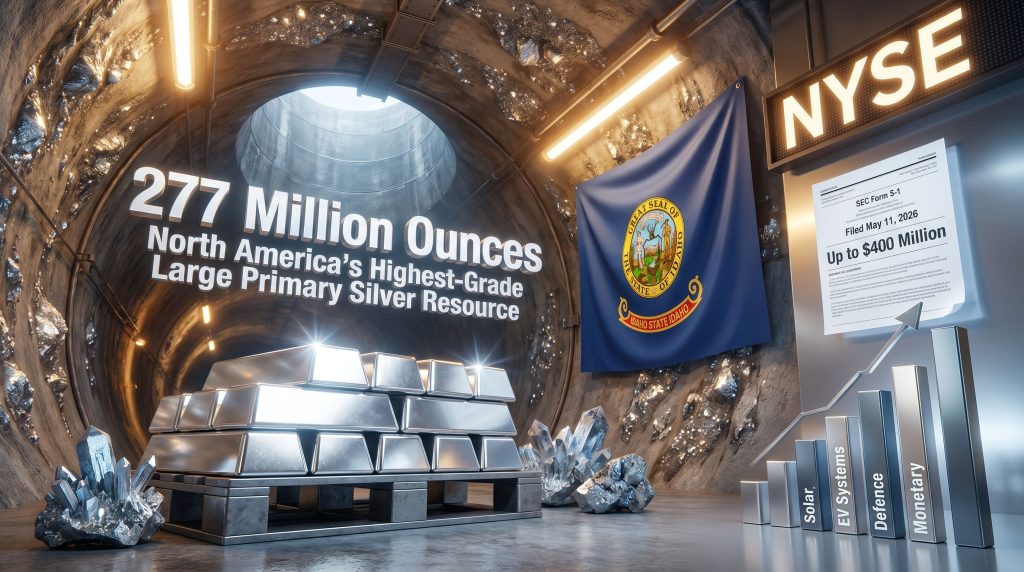

Sunshine Silver Mining and Refining Company, known as SSMRC, filed a registration statement with the U.S. Securities and Exchange Commission on May 11, 2026, marking a pivotal transition from privately held development asset to publicly listed mining company. The company is targeting a listing on the New York Stock Exchange and is seeking to raise up to an estimated $400 million through the public offering of its common stock, according to reporting by Mining Weekly.

The scale of this proposed raise is notable in the context of recent precious metals capital markets activity. Primary silver producers have been conspicuously absent from U.S. IPO pipelines for years, with most silver-focused equity listings concentrated on the Toronto Stock Exchange or Australian Securities Exchange. A NYSE-targeted raise of this magnitude signals a deliberate strategy to attract institutional generalist investors alongside specialist mining funds, broadening the potential ownership base considerably.

Furthermore, what makes this offering structurally different from exploration-stage listings is the combination of a defined production target, substantial pre-IPO capital deployment, and a vertically integrated operational platform that already includes permitted processing infrastructure. Investors are not being asked to fund geological discovery but rather to finance the final phase of transitioning a known, high-grade asset into active production.

Understanding the Form S-1 and What It Means for Investors

A Form S-1 is the primary registration statement used by companies seeking to conduct a public offering of securities in the United States. Filing this document with the SEC initiates a review process during which the company must disclose material information about its business, financial condition, risk factors, and use of proceeds. Until the SEC completes its review and the offering is declared effective, neither the number of shares nor the offering price is finalised.

This distinction matters for prospective investors. The $400 million figure represents an estimated ceiling disclosed in the filing, not a fixed capital raise. Final proceeds will depend on market conditions, investor demand during the roadshow process, and the pricing outcome agreed between the company and its underwriting banks.

The Sunshine Complex: Geology, Scale, and the Coeur d'Alene Legacy

The Sunshine Complex occupies a position within Idaho's Silver Valley that is difficult to replicate. The Coeur d'Alene Mining District, where the complex is situated, has been one of the most productive silver-producing regions in North American history, with recorded production spanning well over a century. The district's geology is characterised by structurally controlled silver-lead-zinc veins hosted in the Belt Supergroup metasedimentary sequence, a geological setting that has historically delivered some of the highest-grade silver mineralisation on the continent.

The current resource base at the Sunshine Complex reflects decades of exploration and development:

| Resource Category | Silver (Million Ounces) |

|---|---|

| Indicated | 112 |

| Inferred | 165 |

| Total Combined | 277 |

The company describes this as North America's highest-grade large primary silver resource, a claim that reflects both the absolute size of the resource and the grade characteristics of the mineralisation. In the context of global silver deposits, grade is a critical differentiator. High-grade primary silver resources reduce the volume of material that must be processed to produce each ounce, directly improving operating cost profiles and capital efficiency.

The Vertical Integration Advantage: Mine, Mill, and Refinery Under One Roof

One of the most strategically significant characteristics of the Sunshine Complex is its vertically integrated structure. The asset encompasses:

- An underground mine within a historically productive district

- An on-site processing mill capable of handling ore from mine output

- A silver refinery that is already permitted, capable of producing finished silver product

This configuration is rare in the global silver industry. Most development-stage silver projects must either construct new processing facilities from scratch or rely on third-party smelter and refinery arrangements, both of which introduce cost, timeline, and counterparty risk. The fact that the Sunshine Complex carries a pre-permitted refinery eliminates a significant regulatory and capital hurdle that has delayed comparable projects in other jurisdictions.

The practical implication is that IPO proceeds can be directed toward mine development, infrastructure upgrades, and working capital rather than duplicating processing capacity that has already been approved and partially established.

Fifteen Years of Private Capital: What $180 Million Has Built

SSMRC's parent entity, Electrum Group, acquired the Sunshine Complex in 2010 and has since committed more than $180 million to the project prior to any public market fundraising. This level of pre-IPO investment is substantial and carries meaningful implications for how investors should assess the project's risk profile.

The capital deployed over this 15-year private ownership period has funded:

- Land consolidation across the Silver Valley district, securing the largest mineral rights position within the Coeur d'Alene Mining District

- Infrastructure rehabilitation, modernising aging plant and equipment to meet contemporary operational and safety standards

- Resource delineation drilling, expanding and upgrading the geological confidence of the 277-million-ounce resource

- Feasibility preparation, advancing technical studies toward the bankable feasibility stage required for project financing

The transition from 15 years of private capital deployment to a public equity offering suggests that the development team has now reached the stage where the capital requirements exceed the practical limits of private funding alone. This is a common inflection point in mine development cycles and typically signals that a project has achieved sufficient technical maturity to withstand public market scrutiny.

From an investor psychology perspective, the sunk capital argument is worth examining carefully. While $180 million of pre-IPO investment does reduce certain early-stage risks, it does not eliminate execution risk associated with the 2028 production restart timeline. Feasibility studies, equipment procurement, labour mobilisation, and commissioning all carry inherent uncertainties that must be evaluated independently of historical capital expenditure.

Antimony: The Critical Mineral Dimension That Changes the Investment Thesis

Silver is the headline commodity at the Sunshine Complex, however antimony's strategic uses as a by-product potential embedded within the deposit add a layer of strategic significance that is not immediately apparent from a precious metals framing alone.

Antimony is a metalloid with a unique combination of properties that make it indispensable across several high-priority industrial and defence applications:

| Application Sector | Antimony Function |

|---|---|

| Battery technology | Antimony trioxide used in lead-acid battery plates; emerging role in antimony-based energy storage |

| Flame retardants | Antimony trioxide acts as a synergist with halogenated compounds in plastics and textiles |

| Defence materials | Used in tracer bullets, night-vision technology, and infrared components |

| Semiconductor production | Applied in certain semiconductor manufacturing processes |

| Glass manufacturing | Used as a fining agent in specialty glass production |

The geopolitical dimension of antimony supply risks is acute. China has historically accounted for the overwhelming majority of global antimony production, with its share of refined antimony output having represented well over half of global supply for extended periods, according to U.S. Geological Survey mineral commodity data. This concentration creates supply chain vulnerability for Western manufacturers and defence contractors that has attracted increasing policy attention.

A domestic U.S. mine capable of producing both primary silver and antimony as a co-product from a single permitted processing complex represents a supply configuration that is genuinely difficult to replicate under current regulatory and geological conditions. The combination of precious metals revenue and critical minerals optionality in one project is a rare structural feature.

It is important to note that the antimony potential at Sunshine remains characterised as a by-product opportunity at this stage of project development. Investors should seek technical disclosure in the SEC filing regarding specific antimony grades, estimated recovery rates, and the economic contribution of antimony to overall project returns before treating this dimension as a primary investment driver.

Silver Demand Fundamentals: Why the 2028 Production Horizon Is Well-Timed

The timing of SSMRC's planned return to production in 2028 aligns with several structural demand trends that are reshaping global silver consumption patterns. Understanding these dynamics provides context for evaluating why a large-scale primary silver producer entering the market at this point carries significance beyond the company's own financial profile. In addition, the silver supply deficits that have characterised recent years reinforce the strategic importance of new primary production coming online.

| Demand Driver | Outlook |

|---|---|

| Solar photovoltaic manufacturing | Silver paste is used in solar cell contacts; demand has grown significantly with renewable energy deployment |

| Electric vehicle systems | Silver contacts, connectors, and LIDAR components contribute to per-vehicle silver intensity |

| Electronics miniaturisation | Printed circuit boards and advanced semiconductors require high-purity silver |

| Monetary and investment demand | Cyclical but persistent demand linked to macroeconomic uncertainty |

| Industrial applications (antimony-linked) | Growing demand in energy storage and defence sectors |

A critical structural nuance of the silver market that is often overlooked by generalist investors is the by-product production dynamic. The majority of the world's silver is not mined intentionally. It arrives as a secondary output from lead, zinc, copper, and gold mining operations. This means that silver supply is largely inelastic to silver price signals in the short to medium term.

When silver prices rise, primary silver miners benefit directly, but the bulk of global supply does not respond proportionally because it is driven by base metal economics rather than silver economics. A large-scale, high-grade primary silver operation like the Sunshine Complex, consequently, occupies a structurally advantaged position in the supply landscape. Its economics are directly geared to silver prices, and its production decisions are made with silver as the primary revenue driver rather than a secondary consideration.

The next major ASX story will hit our subscribers first

Key Risk Factors Every Investor Should Evaluate

No development-stage mining project is without meaningful execution and market risks. The Sunshine Silver IPO Idaho mine return to production story carries several risk dimensions that warrant careful assessment:

Development and Execution Risks

- Feasibility completion uncertainty: Full bankable feasibility studies are still in progress, meaning capital cost estimates may be subject to revision. Cost overruns are common in mine development projects globally.

- Timeline pressure: The 2028 production target represents a defined milestone, but mine restart projects of this complexity frequently encounter scheduling pressures related to equipment delivery, labour availability, and underground development rates.

- Capital deployment efficiency: Ensuring that $400 million in IPO proceeds is allocated optimally across competing development priorities requires disciplined project management.

Market and Commodity Risks

- Silver price volatility: Project economics are directly sensitive to silver price movements. A sustained decline in silver prices from current levels would compress projected returns.

- Antimony price and market development: If antimony by-product revenues form a material part of the project's economic case, investors must assess the stability and depth of antimony markets.

Structural Mitigating Factors

- Over $180 million in pre-IPO capital has already addressed early-stage infrastructure and land consolidation decisions, reducing the risk of foundational project errors

- The permitted refinery infrastructure avoids a major regulatory bottleneck that routinely delays comparable projects

- The Coeur d'Alene Mining District's established geological data and historical production records provide a strong foundation for resource confidence assessments

- Idaho's established mining regulatory framework provides a relatively predictable permitting environment compared to many other U.S. jurisdictions

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Investing in development-stage mining companies involves significant risk, including the potential loss of capital. Readers should conduct independent due diligence and consult a licensed financial adviser before making any investment decisions.

How This Offering Fits the Broader Mining Capital Markets Environment

The broader precious metals outlook has been notably supportive, with elevated gold prices throughout 2025 and into 2026 providing a positive sentiment backdrop for silver as well, given the two metals' correlated investment demand characteristics. The Sunshine Silver IPO Idaho mine return to production offering arrives during precisely this period of renewed investor attention.

The NYSE listing choice is strategically deliberate. Mining equities on the Toronto Stock Exchange have traditionally attracted specialist resource investors, while NYSE-listed mining companies benefit from access to a broader pool of institutional capital that includes pension funds, sovereign wealth vehicles, and generalist equity managers who are less likely to engage with TSX-listed names. For a company seeking to raise up to $400 million, this access to deeper institutional liquidity is a meaningful structural advantage.

The 2028 production timeline also provides a defined investment horizon that distinguishes this offering from earlier-stage exploration listings. Investors in development-stage companies often face extended periods of pre-production capital requirements without near-term production catalysts. A project targeting mine commissioning within approximately two years of its IPO offers a more visible pathway from equity raise to operational revenue generation, which typically supports a narrower valuation discount relative to net asset value.

Frequently Asked Questions: Sunshine Silver IPO and Idaho Mine Restart

What is the Sunshine Silver IPO?

SSMRC filed a Form S-1 registration statement with the SEC on May 11, 2026, initiating the process for a proposed public offering of its common stock on the NYSE. The company is seeking to raise up to an estimated $400 million to fund the advancement of the Sunshine Complex in Idaho toward its planned 2028 production restart.

What resource does the Sunshine Complex contain?

The complex hosts a combined indicated and inferred silver resource of approximately 277 million ounces, comprising 112 million ounces in the indicated category and 165 million ounces in the inferred category. The company describes this as the highest-grade large primary silver resource in North America.

What is the difference between an indicated and inferred resource?

In mineral resource classification, an indicated resource has sufficient geological evidence and drill data to allow reasonable assumptions about continuity, grade, and density. An inferred resource has lower geological confidence and is based on limited data. Indicated resources carry greater technical confidence and are closer to meeting the standards required for economic mine planning.

When is production expected to begin?

SSMRC has communicated a target production restart date of 2028, subject to the completion of feasibility studies, successful capital deployment from the IPO, and the execution of mine development activities.

What is antimony and why does it matter to this project?

Antimony is a critical mineral with applications spanning battery technology, flame retardants, semiconductor manufacturing, and defence-grade materials. Its significance to the Sunshine Complex lies in its potential as a by-product of silver mining operations at the site, adding a critical minerals dimension to the project's commodity profile at a time when Western supply chain security for antimony has become a priority concern.

Who owns SSMRC?

The company is co-owned by Electrum Group, a private investment firm that acquired the Sunshine Complex in 2010 and has committed more than $180 million to its development over the subsequent 15 years. The IPO represents a significant transition of the asset from private development to public equity markets.

A Convergence of Fundamentals, Geography, and Timing

The Sunshine Silver IPO Idaho mine return to production story is not reducible to a single commodity or a single market moment. It brings together a world-class silver resource in a proven geological district, a vertically integrated permitted processing platform, a critical minerals by-product dimension in antimony, and a production timeline that intersects with structurally expanding silver demand from clean energy and technology manufacturing.

What distinguishes this offering from many mining IPOs is the depth of the pre-existing asset foundation. Fifteen years and over $180 million of private investment has transformed a dormant historic mine into a technically advanced development asset with defined resource boundaries, permitted infrastructure, and a staged path to production. The public equity raise, if completed, would fund the final leg of this journey.

For investors evaluating exposure to primary silver production in a stable U.S. jurisdiction, the Sunshine Complex offers a differentiated platform at a time when supply constraints and demand growth are increasingly misaligned. As with any development-stage mining investment, thorough review of the SEC filings, technical reports, and independent feasibility data remains essential before any investment conclusions are drawn.

Want to Stay Ahead of the Next Major Silver or Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, translating complex geological and commodity data into actionable investment insights for both short-term traders and long-term investors. Explore how historic discoveries have generated substantial returns by visiting Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.