July 8, 2026

Why the World's Central Banks Are Hoarding Gold Again

The international monetary system is undergoing a quiet but consequential transformation. Since 2022, central banks collectively have purchased gold at rates not seen since the post-Bretton Woods era, with emerging market institutions leading the charge. This is not simply a reaction to inflation or short-term currency stress. It reflects a deeper structural anxiety: that dollar-denominated reserves held in foreign custodial accounts carry geopolitical risk that physical gold does not.

When sovereign assets held in Western financial infrastructure were frozen in response to geopolitical conflicts, the message reverberated through every finance ministry in the developing world. Gold, by contrast, cannot be sanctioned. It cannot be frozen by a correspondent bank. It does not default. For nations sitting outside the architecture of Western financial alliances, physical bullion has re-emerged not as a relic of the past but as the most credible reserve instrument available.

Tanzania's approach to building its Tanzania gold reserves over the past 18 months represents one of the most disciplined and structurally coherent applications of this logic anywhere on the continent. Furthermore, this approach is deeply connected to broader shifts in the global monetary system and how nations are reassessing what truly constitutes a sovereign reserve asset.

When big ASX news breaks, our subscribers know first

Tanzania's Structural Advantage: A Gold Producer That Keeps Its Own Gold

Most nations accumulating gold reserves must purchase it on open markets, competing with other central banks and institutional buyers at spot prices that have remained firmly above $3,000 per ounce through much of 2025 and 2026. Tanzania occupies a different position entirely.

As one of Africa's top four gold producers by annual output, Tanzania generates substantial domestic supply that can be redirected into sovereign holdings before it ever reaches international markets. This upstream access is an advantage almost no non-producing economy can replicate. Consequently, Tanzania benefits from a structural edge that dramatically lowers the cost and complexity of reserve accumulation compared with peer nations.

Africa's Major Gold Producers: Where Tanzania Sits

| Country | Approximate Annual Output | Notable Characteristic |

|---|---|---|

| Ghana | ~130 tonnes | Largest sub-Saharan producer |

| Mali | ~70 tonnes | Artisanal and industrial mix |

| Burkina Faso | ~60 tonnes | Rapidly expanding capacity |

| Tanzania | ~50 tonnes | Active domestic reserve accumulation |

| DRC | ~40 tonnes | Predominantly informal sector |

Tanzania's mining sector holds an estimated 10 million ounces in total gold reserves across operating and development-stage projects, with major international operators including AngloGold Ashanti and Barrick Gold Corporation holding significant production footprints in the country. The presence of these global majors, ironically, became central to the government's reserve-building strategy.

How 28 Metric Tonnes of Gold Became a $3.68 Billion Reserve Asset

The Accumulation Timeline

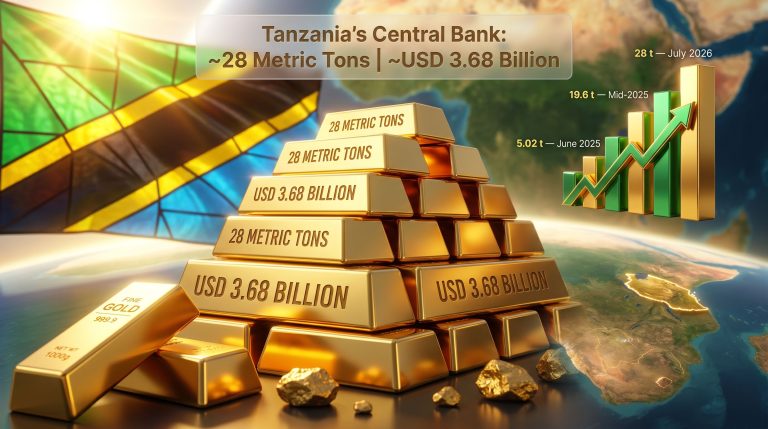

Between approximately January 2025 and July 2026, the Bank of Tanzania acquired more than 28 metric tonnes of physical gold through its domestic purchasing program. The financial progression of that accumulation tells a striking story:

- By the close of 2025, the central bank's bullion holdings were valued at approximately 3.3 trillion Tanzanian shillings, equivalent to roughly $1.3 billion

- By July 2026, that same stockpile had appreciated to a valuation of approximately $3.68 billion

- The increase reflects both continued physical procurement and gold's sustained price strength above $3,000 per ounce during the period

Bank of Tanzania Governor Emmanuel Tutuba disclosed the current valuation at an IMF-World Bank conference held in The Gambia in July 2026, confirming that gold has become a central pillar of the country's reserve management framework. At the time of that announcement, Tanzania held approximately $6 billion in total foreign exchange reserves, providing 4.3 months of import cover, a figure that sits comfortably above the IMF's conventional adequacy threshold of three months.

Key Insight: Gold now accounts for well over half of Tanzania's total foreign exchange reserve position. This concentration in a non-dollar, physical asset is deliberate, not incidental, and represents a fundamental philosophical shift in how the central bank views reserve composition.

The 20% Mandatory Offtake Rule: How the Policy Works

The engine of Tanzania's accumulation program is a regulatory mechanism introduced in June 2025, which requires large-scale gold exporters to direct a minimum of 20% of their production to the Bank of Tanzania at prevailing market prices. The mechanics operate as follows:

- Large-scale mining operators extract and process gold at their Tanzanian operations

- A minimum 20% volume is ring-fenced and made unavailable for direct export

- The Bank of Tanzania purchases this volume at current spot prices, taking physical delivery

- The remaining 80% of production may proceed through standard export licensing channels

- The central bank revalues its accumulated holdings periodically against current market prices

This design is sophisticated from a policy architecture standpoint. By framing the mechanism as a domestic purchase obligation rather than a production levy or export tax, Tanzania reduced the legal friction that typically accompanies resource nationalism measures while achieving comparable sovereign accumulation outcomes. Mining companies receive market prices for the offtake, limiting grounds for investment treaty challenges, while the state captures physical gold directly onto its balance sheet.

The policy directly targets major industrial operators. Barrick Gold, the world's second-largest gold producer by output, operates the North Mara and Bulyanhulu mines in Tanzania. AngloGold Ashanti maintains the Geita gold mine, one of Africa's largest single-site gold operations. These are not marginal producers, and the volumes flowing through the mandatory offtake mechanism are consequently material. For instance, the Buckreef gold project illustrates just how significant Tanzania's broader gold production landscape has become in attracting international attention.

Comparing Regional Gold Reserve Strategies

Tanzania is not the only African nation pursuing domestic gold accumulation, but it has moved faster and more decisively than most. The table below maps the evolving landscape of sovereign gold strategies across the continent.

| Country | Mechanism | Status as of 2026 |

|---|---|---|

| Tanzania | Mandatory 20% offtake from large-scale miners | Active, $3.68B accumulated |

| Ghana | Domestic Gold Purchase Programme (royalty-in-kind) | Active since 2023 |

| Zimbabwe | Gold-backed ZiG currency as monetary anchor | Operational since 2024 |

| Uganda | Central bank domestic gold purchasing program | Launched March 2026 |

Ghana's Domestic Gold Purchase Programme represents the longest-running precedent in sub-Saharan Africa and offers a useful performance benchmark. Zimbabwe's approach is the most aggressive, monetizing gold directly as currency backing rather than holding it as a reserve buffer. Uganda's program, announced in March 2026, signals that the regional momentum behind this model is building rather than plateauing.

However, what makes Tanzania's position particularly noteworthy is how it connects to the broader global phenomenon of central bank gold demand reshaping international reserve management.

Regional Pattern: The convergence of multiple African central banks toward domestic gold accumulation within the same 36-month window is not coincidental. It reflects shared exposure to dollar volatility, declining aid flows, and a reassessment of what constitutes a genuinely sovereign reserve asset.

Beyond Reserve Building: The Financial Inclusion Dividend

One of the less-discussed dimensions of Tanzania's gold reserve program is its downstream effect on financial sector formalisation. Since the initiative began, nearly 4,000 new bank accounts have been opened by mineral dealers and small-scale artisanal miners who previously operated entirely outside the regulated financial system.

This matters for several reasons beyond the headline reserve figures:

- Formally banked operators become visible to tax authorities, broadening the fiscal base

- AML and KYC compliance improves across the mineral trading supply chain

- Previously unbanked miners gain access to credit, insurance, and formal payment infrastructure

- The central bank develops better real-time data on domestic gold flows, improving monetary policy inputs

The integration of artisanal and small-scale mining (ASM) operators into the banking system is a policy outcome that development economists have sought for decades across sub-Saharan Africa with limited success. Tanzania's reserve-building mechanism achieved it as an indirect consequence of commodity policy rather than through direct financial inclusion initiatives.

Tanzania's Gold Summary: Key Statistics

| Metric | Figure |

|---|---|

| Gold accumulated over 18 months | 28+ metric tonnes |

| Reserve valuation (July 2026) | ~$3.68 billion |

| Reserve valuation (end-2025) | |

| Total foreign exchange reserves | ~$6 billion |

| Import cover | 4.3 months |

| Estimated mining-sector gold reserves | ~10 million ounces |

| Mandatory domestic offtake requirement | 20% of large-scale production |

| New bank accounts (sector formalization) | ~4,000 |

The next major ASX story will hit our subscribers first

The Partial Sale Decision: Infrastructure Financing or Reserve Erosion?

In February 2026, President Samia Suluhu Hassan directed the Bank of Tanzania to proceed with a partial liquidation of its gold holdings to finance domestic infrastructure development. Minister of State Kitila Mkumbo confirmed the decision, citing roads, power generation capacity, and port infrastructure as the primary targets for capital deployment. The underlying context was a material contraction in foreign donor funding and development aid flows, forcing the government to mobilise domestic assets rather than rely on external financing.

What remains conspicuously absent from the public record is any quantification of the planned sale. Tanzania's decision to sell part of its reserve has drawn considerable international attention given how rapidly those holdings were built up.

| Parameter | Status |

|---|---|

| Decision authority | President Samia Suluhu Hassan |

| Ministerial confirmation | Minister of State Kitila Mkumbo |

| Volume to be sold | Not publicly disclosed |

| Timeline for liquidation | Not publicly disclosed |

| Stated end uses | Roads, power plants, port upgrades |

| Triggering factor | Sharp contraction in donor funding |

The absence of volume and timeline disclosures creates a credibility gap that sits awkwardly alongside the central bank's reserve-building narrative. Survey data from late 2025 indicated that more than 60% of Tanzanians expressed concern that the country's natural resources were not being managed transparently in the public interest. When a government accumulates gold through a high-profile program and then announces partial sales without quantifying the drawdown, it amplifies rather than resolves those concerns.

Governance Consideration: Sovereign wealth frameworks in more transparent jurisdictions, such as Norway's Government Pension Fund, operate under legislated disclosure requirements that specify drawdown triggers, volume limits, and parliamentary reporting obligations. Tanzania's program currently lacks equivalent accountability architecture, which creates governance risk that investors and multilateral partners are likely to price.

Infrastructure Financing via Reserve Liquidation: Modelling the Tradeoffs

If Tanzania were to sell approximately 20% of its current gold position, that would represent roughly $736 million in proceeds at current valuations. To contextualise what that capital could deploy in infrastructure terms using regional construction cost benchmarks:

- Approximately 1,500 to 2,000 kilometres of paved highway

- Approximately 400 to 600 MW of grid-scale power generation capacity

- Partial modernisation of Dar es Salaam port infrastructure

The critical analytical question is whether the productivity returns generated by that infrastructure over a 20 to 30-year horizon exceed the opportunity cost of holding the equivalent gold position. If gold prices continue appreciating, the cost of selling early compounds over time. If infrastructure investment generates measurable GDP growth and reduces logistics costs across the economy, the conversion may prove rational.

This tension between gold as a permanent monetary anchor and gold as a deployable development finance instrument is the defining strategic dilemma Tanzania now faces, and it is one that no simple formula resolves.

The Longer Arc: Resource Sovereignty and the Mineral-to-Reserve Conversion Model

Historically, the extractive model in sub-Saharan Africa has followed a predictable sequence: minerals are extracted, exported, and converted into foreign currency revenues that are then held in dollar-denominated instruments managed by foreign custodians. The value capture at each stage of that chain has disproportionately accrued outside the producing nation.

Tanzania's model inverts the terminal step. By intercepting 20% of gold production before it exits the country and converting it directly into sovereign bullion holdings, the government bypasses the foreign currency conversion step entirely. The mineral stays on Tanzanian soil in its highest-value physical form.

This approach also hedges against a risk that dollar-reserve accumulation does not: the depreciation of the dollar itself. As the US fiscal position has expanded and dollar hegemony has faced periodic stress, holding Tanzania gold reserves in a non-sovereign, supply-constrained physical asset provides a form of insurance that bond portfolios cannot. In addition, the gold safe-haven role has become increasingly central to how sovereign treasuries worldwide are thinking about long-term reserve strategy.

Upside Scenarios for Tanzania's Reserve Position

- Continued gold price appreciation above $3,000 per ounce expands reserve value without additional procurement costs

- Expansion of the mandatory offtake threshold beyond 20% could accelerate the accumulation pace

- Successful formalisation of artisanal mining supply chains could bring additional volume into the central bank pipeline

- A transparent partial sale framework, if established, could unlock infrastructure capital while preserving sovereign credibility

Key Risk Factors to Monitor

- Undisclosed reserve liquidation could reduce the accumulated buffer faster than publicly understood

- Regulatory friction with major international operators could affect long-term mining investment appetite

- Gold price volatility introduces mark-to-market fluctuations that affect reported reserve adequacy

- Continued transparency deficits around the sale program carry sovereign credit perception risk

Frequently Asked Questions: Tanzania Gold Reserves

How much gold does Tanzania currently hold in reserve?

As of July 2026, the Bank of Tanzania holds more than 28 metric tonnes of physical gold, with a current market valuation of approximately $3.68 billion. The scale of these central bank gold reserves places Tanzania among the most active accumulating nations relative to its economic size.

Why is Tanzania building gold reserves so aggressively?

The program serves three interconnected purposes: strengthening the overall foreign reserve buffer, providing a non-dollar hedge against currency depreciation pressure on the Tanzanian shilling, and reducing the country's dependence on dollar-denominated reserve instruments that carry geopolitical custodial risk.

How does Tanzania acquire gold for its central bank?

Since June 2025, large-scale mining operators are legally required to sell a minimum of 20% of their production to the Bank of Tanzania at prevailing market prices, providing a steady domestic supply pipeline unavailable to non-producing nations.

Is Tanzania planning to sell its gold reserves?

A partial sale was announced in February 2026 under presidential directive, with proceeds designated for domestic infrastructure investment. Neither the volume to be sold nor the timeline for the transaction has been publicly disclosed.

What share of Tanzania's total reserves does gold represent?

With gold holdings valued at approximately $3.68 billion against total foreign exchange reserves of roughly $6 billion, gold now constitutes the dominant component of Tanzania's reserve position. This concentration is historically unusual and reflects a deliberate policy preference for non-dollar assets — a strategy that mirrors the broader global moment when gold at $3,000 became a psychological and structural turning point for sovereign reserve managers worldwide.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. All valuations referenced are based on market prices prevailing at the time of reporting and are subject to change. Forecasts, scenario projections, and infrastructure cost estimates are illustrative and carry inherent uncertainty. Readers should conduct independent research before making any financial decisions.

Want to Track the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time ASX mineral discovery alerts, turning complex geological and commodity data into clear, actionable insights for investors at every level — explore historic discoveries and their returns to understand the opportunity, then begin your 14-day free trial to position yourself ahead of the broader market.