July 26, 2026

When Shareholder Rights Meet Carbon Accountability: A Legal Reckoning for South African Mining

Corporate governance frameworks are built on an implicit assumption: that the rights of shareholders evolve in step with the risks they carry. For most of the twentieth century, those risks were relatively legible — operational, financial, reputational. Today, a different category of risk has entered the boardroom with increasing urgency, and it is one that existing legal frameworks were never explicitly designed to accommodate.

Climate-related financial exposure has become material enough that institutional investors and activist shareholders are no longer content to raise concerns informally. They are going to court. The Thungela shareholder climate disclosure lawsuit, currently before the Gauteng High Court, represents one of the most consequential corporate governance cases in South African legal history.

It does not ask the court to shut down a coal mine or mandate a corporate pivot to renewables. It asks something far simpler — and arguably far more difficult for the respondent to resist: does South African law give shareholders the right to formally request climate risk disclosure from the companies they own? The answer could reshape the governance landscape for every JSE-listed company with significant carbon exposure.

When big ASX news breaks, our subscribers know first

The Three Parties, the Three Years, and the Statute at the Centre of It All

The applicants in this matter are Aeon Investment Management, Fossil Free South Africa, and Just Share NPC — a non-profit shareholder activist organisation. Together, they have spent three consecutive annual general meeting cycles attempting to table a resolution requesting that Thungela Resources adopt and publish greenhouse gas emission reduction targets aligned with the Paris Agreement's 1.5 degrees Celsius pathway.

The resolution covers Thungela's full value chain of emissions across global operations, with a net-zero commitment by 2050. The resolution is, by design, non-binding. It does not instruct the board to take operational action. It requests disclosure.

In each of 2023, 2024, and 2025, the Thungela board refused to table the resolution. In 2025, the company went a step further, stating that the applicants hold no legal right to propose such resolutions at all — and signalling that it would reject all future attempts of this nature. That escalation forced the matter to court.

| Year | Action by Applicants | Thungela's Response |

|---|---|---|

| 2023 | Climate resolution submitted ahead of AGM | Rejected by the board |

| 2024 | Resolution resubmitted | Rejected by the board |

| 2025 | Resolution resubmitted | Rejected; legal right to propose denied |

| Late 2025 | Gauteng High Court application filed | Declaratory order sought |

Before approaching the High Court, the applicants lodged a formal complaint with the Companies and Intellectual Property Commission (CIPC). That referral initiated an alternative dispute resolution process through the Companies Tribunal. No resolution was reached, which cleared the procedural path for litigation — and, critically, strengthened the applicants' standing by demonstrating that all available pre-litigation remedies had been exhausted.

What Does the Legal Challenge Actually Claim?

Business Day's reporting on this legal action confirms the applicants argue that Thungela's repeated refusals constitute a breach of shareholder rights under South African company law. Furthermore, Mining Weekly's coverage of Thungela's response reveals the company intends to vigorously oppose the action, characterising the application as an overreach into board authority.

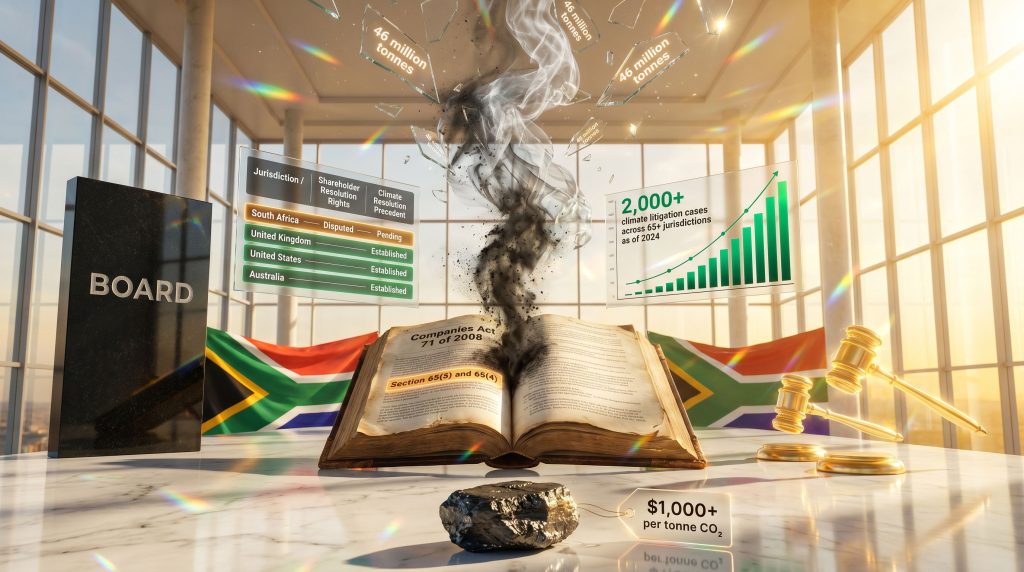

Decoding Section 65: What the Companies Act Actually Provides

The legal battleground is Sections 65(3) and 65(4) of the Companies Act 71 of 2008. The provisions are relatively direct in their language. Section 65(3) provides that any two qualifying shareholders may propose a resolution concerning any matter over which they each hold voting rights. Section 65(4) requires the company to submit that resolution for shareholder consideration at the next general meeting.

The applicants argue that the plain language of these sections is unambiguous. Climate risk disclosure is a matter that materially affects shareholder value, meaning shareholders are entitled to exercise their voting rights over it. Just Share's executive director has characterised the case as being fundamentally about shareholders exercising their rights to act in their own interests with respect to material financial risks — a framing rooted not in activism but in orthodox investment logic.

Thungela's counter-position is more restrictive. Its replying affidavit argues that shareholder voting rights are confined to matters expressly enumerated in the Act or the company's Memorandum of Incorporation. Because the Act vests operational management in the board — requiring directors to manage the business and exercise all company powers unless the Act or the MOI specifies otherwise — the company argues that climate strategy falls exclusively within board authority.

There is a notable gap in Thungela's position, however. The company describes shareholder voting rights as existing within what it calls narrow confines, but its affidavit does not specify which matters shareholders are actually entitled to propose under its interpretation. The restriction is asserted without a positive account of what remains permissible — a logical vulnerability that the Gauteng High Court will need to address.

Thungela also invokes the spectre of unconstrained shareholder interference to illustrate what it believes the applicants' position would permit — including resolutions on geopolitical matters or sporting controversies. Legal commentators have noted that this framing considerably overstates the scope of what is being sought, which is limited to disclosure of quantifiable carbon data within an internationally recognised framework.

The Constitutional Dimension

The applicants do not rely solely on statutory interpretation. Their case incorporates a constitutional overlay grounded in Section 24 of the South African Constitution, which protects every person's right to an environment that is not harmful to health or well-being.

By linking shareholder resolution rights to this constitutional guarantee, the applicants elevate the dispute from a technical question of corporate law to one with broader public interest implications. A court that accepts this framing must weigh whether blocking climate disclosure mechanisms is inconsistent not only with the Companies Act but with constitutional rights that South African courts are obligated to uphold and promote.

The Carbon Numbers Behind the Resolution

To understand why the applicants regard this disclosure as material, it is necessary to engage with the scale of emissions associated with Thungela's operations. Thungela's coal production is associated with approximately 46 million tonnes of carbon dioxide emissions annually. The overwhelming majority of these are Scope 3 emissions — meaning they are produced not at the mine itself but when customers combust the coal that Thungela extracts and sells.

Research cited in the court proceedings, drawing on work from the University of California, estimates the economic damage associated with a single tonne of carbon dioxide at more than $1,000. Applied to Thungela's annual output, that implies a potential environmental damage figure exceeding $46 billion per year — a figure that virtually any financial analyst would classify as a material liability requiring disclosure to investors.

Thungela does have a climate plan. However, according to Fossil Free South Africa's assessment of that plan, it targets only 2% of current emissions for reduction to zero by 2050. The remaining 98% — comprised almost entirely of Scope 3 customer combustion emissions — has no meaningful reduction targets beyond the natural closure of mining operations over time.

This gap is precisely what the proposed resolution is designed to address. A plan that accounts for 2% of a company's total carbon footprint cannot credibly claim alignment with the Paris Agreement's 1.5 degree Celsius temperature pathway. Furthermore, considering the broader context of critical minerals demand and the global energy transition, the pressure on carbon-intensive producers to demonstrate comprehensive disclosure is only intensifying.

Why Scope 3 Is the Critical Disclosure Gap for Coal Producers

Scope 3 emissions receive less regulatory attention than Scope 1 and 2, partly because they occur outside the producer's direct operational control. For most industries, Scope 3 is a secondary concern. For thermal coal miners, it is the dominant one.

The business model of a thermal coal producer is essentially defined by Scope 3 output: the product being sold exists specifically to be combusted. A climate plan that excludes the emissions from that combustion is not a climate plan in any meaningful sense — it is an accounting exercise that reassigns responsibility to customers without quantifying the aggregate impact.

Global mining peers have adopted more comprehensive approaches:

| Company | Scope 3 Disclosure | Climate Resolution Stance |

|---|---|---|

| BHP (ASX: BHP) | Full disclosure across value chain | Accepts shareholder climate resolutions |

| Rio Tinto (ASX: RIO) | Full disclosure across value chain | Accepts shareholder climate resolutions |

| Thungela Resources | Partial — limited Scope 1 and 2 targets | Actively blocking resolutions |

| Sasol | Partial | Resistance reported |

| Exxaro Resources | Partial | Resistance reported |

The pattern is instructive. South Africa's fossil fuel-exposed companies are outliers relative to their global peers on both disclosure quality and shareholder engagement practices. Thungela is not an isolated case — similar legal arguments have been deployed by Sasol and Exxaro to block emissions-related resolutions, suggesting a coordinated interpretive posture across the sector rather than company-specific governance choices.

The Board Supremacy Doctrine and Its Limits

Thungela's core legal argument — that the board's exclusive authority to manage company operations precludes shareholder intervention on climate strategy — draws on a well-established principle of corporate law. Directors do carry fiduciary duties that operate independently of majority shareholder wishes.

South African courts have held directors personally liable for corporate failures at companies including Tongaat-Hulett, Steinhoff, EOH, and VBS, demonstrating that board accountability is real and enforceable. The difficulty with applying this doctrine to the Thungela situation is that the applicants are not seeking to override the board's operational authority. They are requesting that the board disclose information about the emissions consequences of its operational decisions to the people who own the company.

There is an important distinction between a resolution that instructs a board to change its strategy and one that asks the board to report on the material risks associated with its existing strategy. The former may reasonably be characterised as an incursion into board authority. The latter is arguably a basic expectation of ownership.

Thungela's spokesperson has framed the application as inappropriate because it encompasses not only Thungela's own coal sales but also the downstream usage of that coal by customers and the broader global environmental impact of climate change. The company regards this breadth as a reason for rejection. The applicants regard it as a reason for disclosure.

What the Gauteng High Court's Ruling Could Establish

The court has been asked to issue a declaratory order confirming that Thungela breached shareholder rights and its legal obligations under the Companies Act by refusing to table the proposed resolutions. Three broad outcome scenarios carry meaningfully different consequences for the South African governance landscape.

Scenario A: The court rules in favour of the applicants

A broad interpretation of Sections 65(3) and 65(4) would confirm that qualifying shareholders hold the right to propose resolutions on material ESG matters. Every JSE-listed company would need to establish clear protocols for receiving and processing shareholder resolutions on climate and other sustainability topics. The ruling would create binding precedent affecting companies well beyond the coal sector.

Scenario B: The court rules in favour of Thungela

A narrow interpretation reinforcing board supremacy would place South Africa's corporate governance framework in divergence from peer jurisdictions in the United Kingdom, United States, and Australia. Institutional investors operating under ESG mandates may interpret this outcome as a governance risk signal, potentially reducing exposure to JSE-listed companies. The constitutional question under Section 24 would remain unresolved and would likely resurface through separate proceedings.

Scenario C: A narrow or procedural ruling

If the court addresses the matter on procedural grounds without resolving the underlying statutory interpretation, legal uncertainty would persist. Similar disputes involving Sasol, Exxaro, and other carbon-exposed companies would continue to generate litigation without clear legislative or judicial guidance.

Regardless of outcome, the case has already accomplished something significant: it has compelled a formal judicial examination of whether South African corporate law adequately protects shareholders' right to engage on material climate risks. The reputational and regulatory consequences of that examination may ultimately prove more influential than the ruling itself.

The next major ASX story will hit our subscribers first

South Africa's Climate Disclosure Gap: A Structural Problem

One reason this dispute has reached the High Court is that South Africa lacks a binding climate disclosure mandate for listed companies. The JSE's sustainability disclosure guidelines represent best practice guidance rather than enforceable obligations. This contrasts sharply with the regulatory direction in comparable jurisdictions:

- The European Union has implemented the Corporate Sustainability Reporting Directive (CSRD), making climate disclosure mandatory for large listed entities

- The United Kingdom has adopted mandatory Task Force on Climate-related Financial Disclosures (TCFD) reporting for premium-listed companies

- Australia has enacted mandatory climate disclosure legislation aligned with IFRS S2 standards

- South Africa retains a voluntary framework for listed companies, creating the legal ambiguity at the core of this dispute

The King IV Code on Corporate Governance provides guidance on integrated reporting and ESG considerations, but it operates on an apply-and-explain basis and cannot substitute for legislative clarity on shareholder resolution rights. The absence of mandatory IFRS S2 adoption or equivalent domestic standards leaves investors and companies without a shared reference point for what constitutes adequate climate disclosure.

Legislative reform that explicitly includes material ESG risks within the scope of Section 65 resolution rights, or that mandates climate-related financial disclosure for JSE-listed entities, would resolve the ambiguity that is currently forcing affected parties into court. Until that reform occurs, litigation is likely to remain the primary mechanism through which shareholders can enforce climate disclosure expectations. The evolving geopolitical mining landscape is, furthermore, accelerating pressure on governments worldwide to clarify these obligations.

What This Means for Institutional Investors and Long-Term Portfolios

For investors assessing exposure to JSE-listed companies with significant carbon footprints, the Thungela shareholder climate disclosure lawsuit surfaces several intersecting risk dimensions that extend well beyond the legal question.

Regulatory risk is growing. South Africa's Climate Change Act creates a pathway toward mandatory emissions reduction obligations, and the global trajectory of climate regulation points toward tightening constraints on high-emission industries over the medium term.

Stranded asset risk is already visible in thermal coal valuations globally. Assets that require long payback periods face accelerating devaluation as energy transition timelines compress in major markets. Consequently, safe-haven investing strategies are attracting growing interest from institutional allocators seeking to reduce exposure to stranded asset risk in carbon-intensive sectors.

Financing and insurance risk is becoming operational. Global lenders and insurers are progressively withdrawing coverage and credit facilities from coal operations that cannot demonstrate credible transition planning.

The engagement versus divestment question is directly relevant here. Institutional investors — including large South African pension funds with fiduciary obligations to manage long-term risk — often prefer shareholder engagement through resolutions over divestment, because engagement preserves ownership rights and allows investors to influence corporate behaviour from within.

The Thungela case illustrates what happens when that engagement pathway is legally contested: investors are left with fewer tools, not more accountability. In addition, the broader context of mining sustainability transformation globally suggests that companies resisting disclosure are increasingly at odds with where capital markets, regulators, and their own investors are headed.

A ruling that confirms shareholder resolution rights under Section 65 would preserve the engagement pathway. A ruling that restricts those rights would narrow the options available to long-term institutional capital, potentially accelerating divestment decisions that the board supremacy argument was ostensibly designed to prevent.

However, it is also worth noting that government intervention in mining is increasingly shaping the regulatory environment within which these disputes unfold, with policymakers in multiple jurisdictions signalling an intent to formalise ESG disclosure requirements before the courts are forced to do so repeatedly.

The Thungela shareholder climate disclosure lawsuit is, at its most fundamental level, a dispute about who gets to define what is material in a company's risk profile. That question does not have a purely legal answer — but the Gauteng High Court's ruling will shape how South African corporate law responds to it for years to come.

This article contains forward-looking analysis and scenario modelling for informational purposes only. It does not constitute legal or financial advice. Readers should seek independent professional guidance before making investment or governance decisions based on the matters discussed.

Want to Identify ASX Mineral Discoveries Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex data across more than 30 commodities into clear, actionable insights for both short-term traders and long-term investors — begin your 14-day free trial today and explore how historic discoveries have generated substantial returns for those who acted early.