July 10, 2026

How Silver-Rich Geology and Phased Mine Design Position a Sinaloa District for Redevelopment

Few dynamics in gold mining generate as much investor attention as the redevelopment of historically productive districts using modern engineering. Across Latin America, some of the most capital-efficient projects of the past two decades have not been greenfield discoveries but rather the systematic application of contemporary metallurgy and mine planning to districts that sustained extraction activity for centuries. The Sinaloa region of Mexico fits this archetype with unusual precision, and the Torex Gold Los Reyes project production framework released in July 2026 offers a detailed window into how that value thesis is being translated into financial and operational reality.

Understanding the Los Reyes opportunity requires more than reading headline numbers. It demands an appreciation of how grade management, processing circuit selection, tailings engineering, and phased capital deployment interact to shape the risk-adjusted return profile of a long-life precious metals asset.

When big ASX news breaks, our subscribers know first

A District With Centuries of Proof: The Geological Foundation of Los Reyes

The Los Reyes asset in the Sinaloa district is not new to industrial-scale extraction. Historical production estimates suggest the area yielded approximately 1 million oz of gold and 60 million oz of silver between 1770 and 1990, a track record spanning more than two centuries of continuous or intermittent mining activity. This legacy matters in ways that go beyond narrative appeal.

For geologists and mine planners, a multi-century production history creates a body of empirical evidence about ore continuity, structural controls, and metallurgical behaviour that no amount of modern drilling can fully replicate. The fact that historical operators consistently returned to this district across vastly different economic and technological eras suggests robust geological endowment rather than episodic, structurally isolated mineralisation.

The modern resource base, as defined under NI 43-101 standards, reflects that geological confidence. The current indicated mineral resource stands at 1.5 million oz Au and 54 million oz Ag, with inferred resources adding a further 538,000 oz Au and 21.6 million oz Ag. Critically, the silver-to-gold ratio embedded in the resource, roughly 36 oz Ag for every 1 oz Au in the indicated category, has profound implications for project economics that only become apparent when by-product cost accounting is applied.

Why the Silver-Gold Ratio Is a Hidden Value Driver

Most gold project analyses default to co-product cost metrics, which can obscure the economic contribution of silver in polymetallic deposits. Furthermore, silver's dual role as both a precious and industrial metal means its pricing dynamics are distinct from gold. At Los Reyes, the distinction between co-product and by-product accounting is dramatic:

| Cost Metric | Co-Product Basis | By-Product Basis |

|---|---|---|

| Total Cash Cost (TCC) | US$1,299/oz AuEq sold | US$279/oz Au sold |

| Mine-Site AISC | US$1,617/oz AuEq sold | US$738/oz Au sold |

The US$1,338/oz difference in AISC between the two accounting methods is almost entirely attributable to silver revenue credits. At life-of-mine average production of approximately 3 million oz Ag per year, silver becomes far more than a secondary commodity at this project. It functions as a structural cost offset that, under constructive silver pricing, positions Los Reyes among the lower-cost quartile of global gold producers on a by-product basis.

This dynamic is not widely understood by generalist investors who screen projects on headline AISC figures without distinguishing co-product from by-product methodologies. For investors with a view on silver prices, the by-product AISC of US$738/oz gold at a US$50/oz silver assumption carries meaningful upside optionality if silver outperforms that base case. In addition, ongoing silver supply deficits could further strengthen the case for elevated silver pricing across the mine life.

The PEA Financial Architecture: What the Numbers Actually Reveal

The Torex Gold Los Reyes project production economics, as outlined in the July 2026 Preliminary Economic Assessment, present a compelling capital efficiency case. However, interpreting those numbers requires understanding the assumptions and structural choices embedded within them.

Base Case and Upside Scenario Comparison

| Financial Metric | Base Case | +10% Metal Price Scenario |

|---|---|---|

| Gold Price Assumption | US$3,600/oz | US$3,960/oz |

| Silver Price Assumption | US$50/oz | US$55/oz |

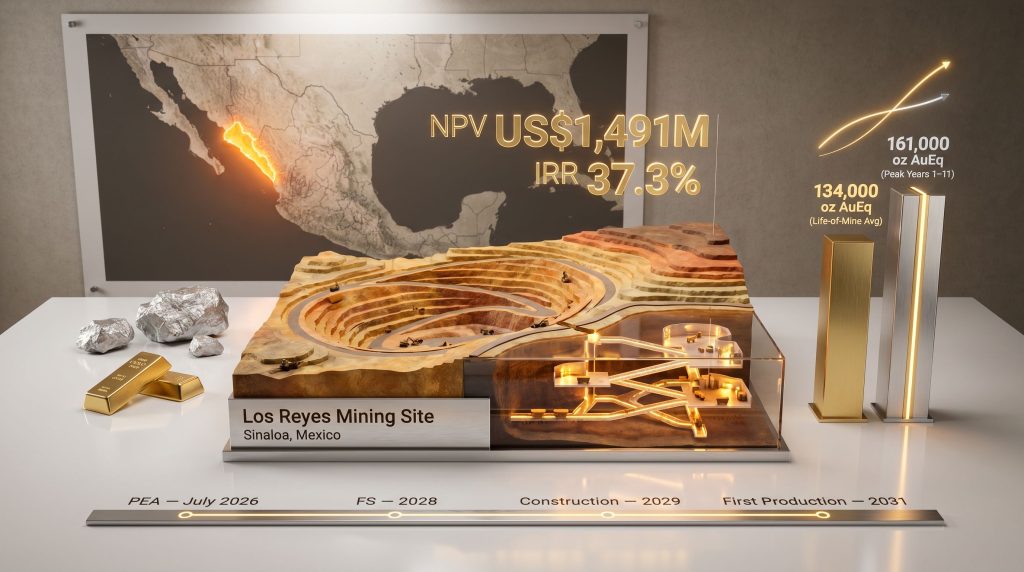

| After-Tax NPV (5% discount) | US$1,491 million | US$1,816 million |

| After-Tax IRR | 37.3% | 42.7% |

| Initial CAPEX | US$515 million | US$515 million |

| Profitability Index | 2.9x | N/A |

| Payback Period | 1.9 years | N/A |

The 2.9x profitability index is particularly instructive. In capital allocation terms, this means each dollar of initial capital deployed is projected to return approximately $2.90 in net present value terms, a threshold that would attract serious attention from institutional investors evaluating competing uses of mining capital.

The 1.9-year payback period against a 14.4-year mine life is equally significant. In project finance terms, recovering initial capital in under two years from a 14-year asset creates an extended period of essentially unencumbered cash generation. This front-loaded return structure is directly attributable to the grade management and mine sequencing strategy discussed below.

The 325 basis point IRR expansion between base case and upside scenario (+37.3% to +42.7%) confirms meaningful leverage to gold and silver price appreciation, an important characteristic given elevated precious metals pricing environments in recent years. That same sensitivity applies symmetrically downward, which investors should factor into downside scenario modelling.

The Full Capital Picture: Initial and Sustaining Costs

A common analytical error in mining project evaluation is focusing exclusively on initial capital while underweighting sustaining capital obligations. At Los Reyes, sustaining capital of US$579 million over the mine life actually exceeds initial CAPEX of US$515 million, a characteristic typical of long-life underground operations.

Initial Capital Breakdown (US$515 million):

- Process plant construction: US$113 million

- Underground mining development: US$77 million

- On-site and off-site infrastructure: US$71 million

- Contingency allocation: US$103 million (~20% of pre-contingency CAPEX)

Sustaining Capital Over Mine Life (US$579 million):

- Underground mining sustaining capital: US$340 million

- Open-pit sustaining capital: US$75 million

- Fleet lease payments: US$301 million

- Closure cost provision: US$35 million

The US$301 million in fleet lease payments is worth highlighting as a distinct financial structure. Rather than purchasing mining equipment outright, the project model incorporates lease financing for mobile fleet, which preserves capital flexibility but creates a recurring fixed cost obligation that sits within sustaining capital rather than initial CAPEX. This is an increasingly common approach in mid-tier gold development but one that can be misread in cost comparisons if not properly categorised.

Production Architecture: How Grade Management Drives NPV

The Phased Sequencing Logic

The Torex Gold Los Reyes project production profile is not simply a function of resource grade. It is the result of a deliberate sequencing strategy designed to concentrate high-value ounces in the earliest possible cash flow periods, a technique sometimes called grade management or high-grading optimisation. Factors such as grade and permitting complexity are, consequently, central to how the project's financial outcomes will ultimately be realised.

The execution logic proceeds in three distinct phases:

-

Ramp-up (Year 1): Open-pit mining commences 12 months ahead of underground development. This sequencing ensures the 5,000 t/d processing plant has a reliable ore feed during the highest-risk operational period, without depending on underground production that typically requires longer development timelines to stabilise.

-

Peak production (Years 1 to 11): Open-pit and underground extraction operate concurrently, with both sources feeding the processing plant with the highest-grade material available. Lower-grade open-pit material is stockpiled rather than blended into the mill feed, preserving mill head grades and maximising metal output per tonne processed.

-

Tail phase (Years 11 to 14.4): After primary mining concludes, the accumulated lower-grade stockpile is systematically processed to sustain mill utilisation. This avoids stranded processing capacity and maintains revenue generation through the project's final years.

| Production Metric | Life-of-Mine Average | Peak Period (Years 1 to 11) |

|---|---|---|

| Annual AuEq Production | 134,000 oz | 161,000 oz |

| Annual Gold Production | ~93,000 oz | 111,000 oz |

| Annual Silver Production | ~2,992,000 oz | 3,594,000 oz |

| Mine Life | 14.4 years | N/A |

| Total Mineralized Material | 26.07 Mt | N/A |

| Head Grade (Au) | 1.68 g/t | Higher during peak |

| Head Grade (Ag) | 63.4 g/t | Higher during peak |

"The decision to defer lower-grade open-pit material rather than blend it into early mill feed is a technically sound NPV optimisation technique. By concentrating high-grade feed in the early years when discounting has the least erosive effect on present value, the project captures disproportionately more value from the same total mineral inventory."

Mining Methods: Open Pit and Underground in Context

The open-pit component extracts 11.25 Mt of mineralized material against 76.03 Mt of waste, producing an average strip ratio of 6.8:1. While this ratio is not unusually high by industry standards for precious metals open-pit operations, it underscores that the underground component carrying 14.82 Mt represents the operational backbone, contributing approximately 57% of total processed tonnes.

Underground extraction uses long-hole open stoping with paste backfill, a method well-suited to the steeply dipping, high-grade vein systems typically found in silver-gold districts like Sinaloa. Long-hole open stoping allows large volumes of ore to be blasted efficiently from ring-drilled holes, while paste backfill, made partly from processed tailings, provides structural support for excavated voids. This backfill approach also serves an environmental function by redirecting approximately 38% of total tailings underground rather than to surface storage.

Processing Technology and Tailings Engineering

Why Merrill-Crowe Was Chosen Over Carbon-in-Leach

The metallurgical circuit selection at Los Reyes, specifically the use of Merrill-Crowe precipitation rather than carbon-in-leach (CIL) or carbon-in-pulp (CIP) recovery, reflects a technically informed decision based on the deposit's silver-rich character.

The Merrill-Crowe process works by clarifying pregnant leach solution and then precipitating dissolved gold and silver by adding zinc dust under vacuum. It is particularly effective for high-silver ores because silver recovery through activated carbon can be less efficient at elevated silver concentrations. The process delivers life-of-mine metallurgical recoveries of 94.8% for gold and 81.1% for silver, figures that compare favourably with industry benchmarks for similar deposit types.

The processing circuit flows as follows:

- Three-stage crushing reduces run-of-mine ore to mill feed size.

- Single ball mill grinding achieves target particle size for leaching.

- Whole-ore cyanide leaching dissolves gold and silver into solution.

- Merrill-Crowe precipitation recovers gold and silver as a sponge product.

- Smelting produces doré bars for sale or further refining.

Dry-Stack Tailings: An Engineering Choice With Environmental and Financial Dimensions

Approximately 62% of tailings are filtered and placed in a dry-stack tailings storage facility, while the remaining 38% is converted into cemented paste backfill for underground void management. This hybrid approach reduces the surface footprint of wet tailings storage, lowers closure cost obligations, and improves geotechnical stability, all material considerations in Mexico's evolving environmental permitting landscape.

Power infrastructure for the project will be supplied via a dedicated 138 kV transmission line connecting the site to an existing hydroelectric grid north of Cosala. This standalone power solution reduces diesel dependency and associated fuel cost volatility, while the hydroelectric source lowers the project's scope 2 carbon intensity relative to diesel or coal-fired grid alternatives.

Development Timeline and the Critical Path to First Production

| Development Milestone | Target Timing |

|---|---|

| 20,000m Resource Conversion Drilling | Commenced May 2026 |

| Preliminary Economic Assessment Release | July 2026 |

| Prefeasibility Study Initiation | 2H 2026 |

| Feasibility Study Completion | 2028 |

| Construction Commencement | 2029 |

| First Commercial Production | 2031 |

The 20,000m drilling program targeting the Guadalupe, Z-T, and Central zones is the near-term value driver most directly within Torex's operational control. Converting inferred resources to indicated classification is not merely a bureaucratic category upgrade. Under NI 43-101 standards, inferred resources carry too much geological uncertainty for inclusion in feasibility-level mine plans or bank financing calculations. Successful conversion through this program is therefore a prerequisite for both the prefeasibility study and any future debt financing discussions.

Definitive feasibility studies represent a critical gateway before construction capital can be committed, and Los Reyes must navigate this process rigorously before the 2029 construction start can be confirmed. It is also worth noting that drilling at Los Reyes was suspended during 2025 due to security-related concerns in the Sinaloa region before resuming in May 2026. This suspension, while resolved, illustrates a genuine operational risk variable that project scheduling must actively accommodate. Sinaloa has experienced periods of elevated security complexity related to organised crime activity, and this factor warrants ongoing investor attention as a potential source of timeline disruption.

"A preliminary economic assessment is a conceptual-level study. Financial projections at this stage are based partly on inferred mineral resources that are considered too speculative for economic inclusion under standard reporting frameworks. The figures presented will be subject to material revision as geological confidence increases through the prefeasibility and feasibility study phases."

The next major ASX story will hit our subscribers first

Strategic Fit: What Los Reyes Means for Torex's Corporate Trajectory

Torex Gold's existing production base at the Morelos Complex in Guerrero state delivered 452,523 oz of gold in 2025, anchored by the Media Luna and ELG mines. While this is a substantial and well-established operation, it represents a single-asset concentration that institutional investors in mid-tier gold producers typically view as a structural risk premium.

Los Reyes directly addresses that risk by adding a geographically distinct, standalone production centre within the same national operating environment. The strategic logic is reinforced by Torex's track record in Mexico, which encompasses permitting expertise, community engagement protocols, security management systems, and an established local talent pool. These capabilities, developed over years at Morelos, are transferable to Sinaloa and represent a genuine operational advantage over an external party attempting to develop the same asset from scratch.

At peak production of 161,000 oz AuEq per year, Los Reyes would represent approximately a 35% production increment relative to Morelos 2025 output. A combined portfolio operating at those levels would place Torex in the 550,000 to 600,000+ oz AuEq per year range during Los Reyes' peak phase, approaching the production scale threshold that institutional investors often associate with reclassification from mid-tier to near-senior gold producer status. This distinction matters because institutional mandates for senior gold exposure are typically broader and more liquid than those for mid-tier names, potentially expanding the investor base and compressing valuation multiples.

Key Risk Factors Investors Should Model Independently

- PEA study limitations: The conceptual nature of a preliminary economic assessment means financial projections can shift materially as geological and engineering confidence increases through subsequent study phases.

- Security environment: The 2025 drilling suspension demonstrates that Sinaloa's security conditions represent an active, not merely theoretical, operational risk.

- Permitting timeline uncertainty: Mexico's mining permitting framework has grown increasingly complex in recent years, introducing potential delays between feasibility completion in 2028 and construction start in 2029.

- Metal price symmetry: The same leverage that generates a 325 basis point IRR improvement under a +10% price scenario applies proportionally to downside outcomes.

- Underground execution dependency: With 14.82 Mt of the total feed sourced from underground operations, long-hole open stoping performance and paste backfill quality are critical operational variables.

- Sustaining capital intensity: Total sustaining capital of US$579 million exceeding initial CAPEX of US$515 million requires investors to model free cash flow carefully across the full mine life rather than anchoring on early payback metrics alone.

Frequently Asked Questions: Torex Gold Los Reyes Project Production

When will Los Reyes begin producing gold?

First commercial production is targeted for 2031, following construction commencement planned for 2029. The project is currently progressing through resource conversion drilling and study phase activities, with a prefeasibility study planned for the second half of 2026 and a full feasibility study targeted for 2028.

What is the average annual gold production forecast?

The PEA projects average annual production of 134,000 oz AuEq across the 14.4-year mine life. During the first 11 years of primary mining, annual production is expected to average 161,000 oz AuEq, comprising approximately 111,000 oz Au and 3.59 million oz Ag.

How does silver production affect the project's cost profile?

Silver production of approximately 3 million oz per year creates substantial by-product revenue credits that reduce the effective cost of gold production. On a by-product basis, the mine-site AISC falls to US$738/oz gold sold, compared to US$1,617/oz AuEq on a co-product basis. The difference reflects the economic materiality of silver at this deposit.

What is the NPV of the Los Reyes project?

Under base case assumptions of US$3,600/oz Au and US$50/oz Ag, the after-tax NPV at a 5% discount rate is estimated at US$1,491 million. A scenario assuming 10% higher metal prices produces an after-tax NPV of US$1,816 million.

What is the initial capital cost to build the mine?

Initial capital expenditure is estimated at US$515 million, inclusive of US$113 million for the process plant, US$77 million for underground development, US$71 million for infrastructure, and US$103 million in contingencies. Life-of-mine sustaining capital adds a further US$579 million.

Want to Track the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex geological and financial data into actionable investment insights for both short-term traders and long-term investors — explore Discovery Alert's dedicated discoveries page to see how historic finds have generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the broader market.