June 14, 2026

The Metal That Could Redraw the Global Industrial Map

Few commodity markets reveal the fragility of Western industrial supply chains more starkly than tungsten. While lithium and rare earth elements have dominated critical minerals headlines for years, tungsten has quietly accumulated a set of strategic characteristics that arguably make it more irreplaceable than either. It has the highest melting point of any metal at approximately 3,422 degrees Celsius, exceptional density, and a hardness profile that no synthetic alternative has convincingly matched in high-stress applications. Furthermore, these physical properties are not merely interesting engineering facts — they are the reason the Kazakhstan tungsten deal and China critical minerals supply chain has become a defining geopolitical flashpoint across defence manufacturing, semiconductor fabrication, aerospace engineering, and electric vehicle production simultaneously.

Understanding why this deal has captured the attention of Washington, Beijing, and global commodity markets requires starting not with the transaction itself, but with the structural architecture of a market that has been quietly building toward a breaking point for years. Tungsten's strategic importance is now impossible to ignore, and what follows explains precisely why.

When big ASX news breaks, our subscribers know first

Why Tungsten's Supply Concentration Rivals Any Strategic Commodity on Earth

The degree to which China controls global tungsten supply is frequently underestimated outside specialist circles. Estimates consistently place China's share of global tungsten mine production between 75% and 85%, a concentration that rivals or exceeds China's dominance over rare earth elements. More importantly, China's control extends well beyond the mining stage. Chinese entities hold a disproportionately large share of downstream processing and refining infrastructure, meaning that even tungsten ore mined outside China often depends on Chinese facilities to reach usable industrial form.

China's national tungsten reserve base is estimated at approximately 2.4 million tonnes, the largest single-country concentration on earth. However, the strategic leverage this creates goes beyond raw tonnage. Vertical integration across the entire value chain — from ore extraction through intermediate processing to finished tungsten carbide and other manufactured products — amplifies China's market influence far beyond what reserve figures alone suggest.

How Does Tungsten Compare to Other Critical Minerals in Strategic Vulnerability?

| Critical Mineral | Primary Strategic Use | China's Estimated Supply Share | Substitutability |

|---|---|---|---|

| Tungsten | Defence, semiconductors, EVs | 75–85% of production | Very Low |

| Rare Earth Elements | Electronics, defence systems | 60%+ of mining | Low to Moderate |

| Lithium | EV batteries, energy storage | 60%+ of processing | Low |

| Cobalt | Batteries, aerospace alloys | 70%+ of refining | Low |

Critical Insight: Tungsten's supply concentration is comparable to or greater than rare earth elements, yet it attracts a fraction of the investor and policy attention. This represents one of the most underappreciated structural vulnerabilities in Western industrial strategy — and one that China's export restriction policy has now forced into the open.

The growing role of tungsten in defence and aerospace applications further elevates the urgency of diversifying supply away from a single dominant producer. In addition, the broader critical minerals demand surge has made the case for alternative supply development more compelling than ever before.

China's Export Controls and the APT Price Explosion

In February 2025, China implemented formal export controls on tungsten, triggering an immediate and severe market disruption. The controls arrived alongside tightening of Chinese domestic mining quotas and the compounding effect of declining ore grades at established Chinese operations. The convergence of these factors produced what Fastmarkets described as a perfect storm for tungsten supply tightness, with quota restrictions, grade deterioration, and surging industrial demand reinforcing one another simultaneously.

The price impact was dramatic. Benchmark ammonium paratungstate, or APT, is the primary internationally traded tungsten intermediate product and the standard pricing reference for the global market. APT prices moved from approximately $400 per metric tonne unit (MTU) during the 2025 baseline period to over $3,000 per MTU by April 2026, according to market data. Some tungsten chemical products reportedly recorded price increases exceeding 200% within just a few months.

Reuters reported that global tungsten inventories remained extremely tight throughout this period, as international buyers scrambled to source alternative supplies that simply did not exist at sufficient scale. Industry estimates suggest global tungsten export volumes declined by approximately 40% as the full effect of China's restrictions took hold.

The APT Price Timeline: A Market Under Structural Stress

| Period | APT Benchmark Price | Primary Driver |

|---|---|---|

| 2025 Baseline | ~$400/MTU | Normal supply conditions |

| Early 2026 | Rising sharply | Export restriction announcement |

| April 2026 Peak | Over $3,000/MTU | Supply panic and inventory depletion |

Market analysts now model the global tungsten supply-demand gap exceeding 17% between 2026 and 2028, with structural undersupply conditions forecast to persist until at least 2027. The underlying reason for this extended timeframe is not merely a short-term export policy decision. New tungsten mines outside China require multi-year development cycles, meaning the pipeline of alternative supply cannot respond quickly regardless of price signals. This creates the kind of persistent supply deficit that historically generates sustained commodity price elevation rather than a brief spike followed by normalisation.

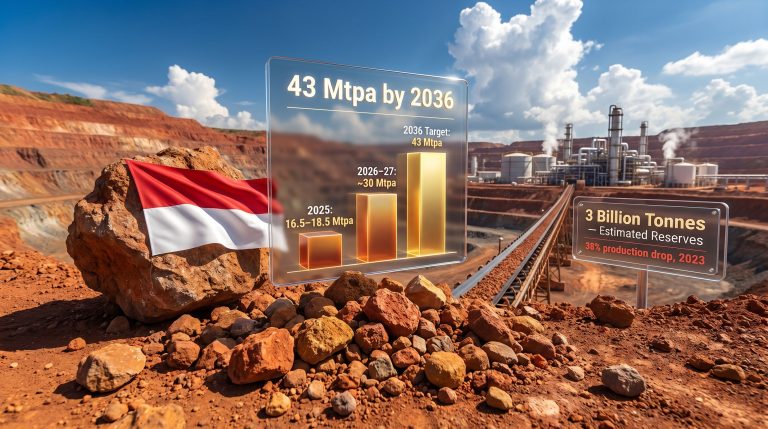

Kazakhstan's Severniy Katpar Project: Scale, Geology, and Strategic Positioning

The Severniy Katpar tungsten deposit in northeastern Kazakhstan carries resource estimates of approximately 1.4 million tonnes of tungsten. To contextualise that figure: it represents more than 58% of China's entire estimated national reserve base of 2.4 million tonnes, concentrated within a single deposit. Combined with the adjacent Upper Kairakty project, projected annual production capacity from full development could reach approximately 12,000 metric tonnes per year, which would represent roughly 15% of current total global tungsten supply.

Very few mineral projects anywhere outside China possess the reserve scale necessary to materially shift global supply balances. Severniy Katpar sits in a rare category occupied by only a handful of deposits worldwide, which explains why it has attracted the level of capital and geopolitical attention it has.

Kazakhstan's first tungsten processing facility opened in November 2024 as a joint venture with Jiaxin International Resources Investment, with a processing capacity of 3.3 million tonnes of ore annually. The country completed its first commercial tungsten concentrate exports in 2025, with a shipment of approximately 3,700 tonnes valued at $71 million delivered to China via existing rail infrastructure. This transaction demonstrated that Kazakhstani tungsten operations can generate meaningful commercial volumes, even if the ultimate destination highlighted the complexity of routing decisions that will define the project's long-term strategic value.

Kazakhstan's Tungsten Production Trajectory

| Year | Estimated Output | Key Development Milestone |

|---|---|---|

| Pre-2024 | Negligible | No commercial tungsten exports |

| 2025 | ~2,400 tonnes | First commercial exports ($71M, China-bound) |

| 2026 onwards | Scaling | Severniy Katpar development advancing |

| 2030 (projected) | Potentially 12,000+ tonnes/year | Full project development scenario |

Kazakhstan is already projected to rank among the top three global tungsten producers in 2025, behind only China and Vietnam. This trajectory suggests Central Asia could emerge as a decisive swing region for global tungsten supply within a decade, provided development timelines and financing commitments are sustained.

Three Scenarios for the Project's Real-World Impact on China's Critical Minerals Grip

The Kazakhstan tungsten deal and China critical minerals supply chain dynamics do not have a single predetermined outcome. The ultimate impact depends on a set of interacting variables spanning financing, logistics, geopolitics, and development execution. Modelling three distinct scenarios reveals both the potential and the risk embedded in this investment thesis.

Scenario A: Full Western Reorientation (Optimistic)

- U.S. Export-Import Bank financing of up to $900 million materialises alongside $700 million from the International Development Finance Corporation

- Westward transit corridors through the Caspian Sea route become fully operational

- Kazakhstan achieves top-three global producer status and supplies Western defence and semiconductor industries directly

- China's pricing power over tungsten markets is materially reduced within five to seven years

Scenario B: Partial Development with Continued China Dependency (Base Case)

- Financing is secured but logistics constraints limit efficient throughput to Western end markets

- Kazakhstan exports a significant share of output to China via existing rail infrastructure, as it did with its inaugural shipment

- Global supply volumes increase, but China retains processing dominance and strategic market influence

Scenario C: Geopolitical Stall (Downside)

- Transit route disputes with Russia and China constrain westward mineral shipments effectively

- Project financing encounters sustained political headwinds or execution delays

- Kazakhstan's tungsten remains regionally constrained, and Western supply vulnerability persists through the late 2020s

Scenario Warning: The single most important variable separating Scenario A from Scenario B is not financing. It is logistics. Kazakhstan is landlocked, and the existing rail infrastructure most naturally routes toward China. Without a fully operational Caspian transit corridor, Western capital may inadvertently subsidise a supply chain that continues feeding Chinese industrial production.

The U.S. Financing Commitment and the Logic of Friend-Shoring

The potential financial architecture supporting Severniy Katpar's development is substantial by any measure. The U.S. Export-Import Bank issued a Letter of Interest for up to $900 million in project financing, while the International Development Finance Corporation expressed interest in a further $700 million, bringing the combined potential federal interest to $1.6 billion. Private investment from Cove Kaz Capital Group adds at least $1.1 billion in committed capital, creating a total financing framework running into multiple billions.

This level of interest from U.S. federal financing institutions advances the broader framework established through the U.S.-Kazakhstan Memorandum of Understanding on Critical Minerals Cooperation, signed in November 2025. According to reporting by the Financial Times, the MOU formalised Kazakhstan's role as a partner nation within the broader US critical minerals strategy, an approach commonly described as friend-shoring. This US critical minerals strategy reflects Washington's determination to reduce dependence on Chinese-controlled supply chains across a range of critical inputs.

Friend-shoring in critical minerals refers to the deliberate redirection of supply chains toward nations that share sufficiently aligned geopolitical interests with the United States, even when those nations are not formal military allies. Kazakhstan's geographic position, sandwiched between Russia and China with whom it maintains active economic relationships, makes it a more complex friend-shoring candidate than, for example, Australia. The U.S.-Australia critical minerals alliance, valued at $3.5 billion, involves a formal Five Eyes intelligence partner with straightforward export route access. Kazakhstan, however, requires a more nuanced strategic calculation.

The next major ASX story will hit our subscribers first

The Transit Problem: Geography as the Project's Most Underappreciated Risk

Kazakhstan's landlocked geography creates fundamental export route dependencies that no amount of financing can resolve on its own. Understanding the realistic logistics options is essential for evaluating whether Western capital invested in Severniy Katpar will actually deliver supply security for Western industries.

What Are the Realistic Logistics Routes for Kazakhstani Tungsten?

| Export Route | Access to Western Markets | Political Risk Level | Infrastructure Status | Western Supply Viability |

|---|---|---|---|---|

| Via China (rail) | Efficient to Asia only | High (strategic conflict) | Excellent | Low |

| Via Russia | Moderate distance | High (sanctions environment) | Good | Very Low |

| Via Caspian Sea / Azerbaijan | Viable but longer | Moderate | Developing | Medium-High |

| Via Afghanistan | Extremely long | Very High | Poor | Negligible |

The Caspian Sea corridor, routing through Kazakhstan's Kuryk port and onward through Azerbaijan, represents the most strategically viable westward route. However, it requires significant infrastructure investment, multi-modal coordination across rail, sea, and road networks, and sustained political cooperation from transit nations. This is not an insurmountable challenge, but it is a multi-year infrastructure development programme in its own right, layered on top of an already multi-year mine development timeline.

Consequently, the strategic mineral supply risks associated with landlocked deposits are consistently underestimated in market commentary that focuses primarily on reserve scale and financing commitments.

China's Countermove Inside Kazakhstan

A dimension of the Kazakhstan tungsten story that receives insufficient analytical attention is the extent to which Chinese-backed entities have simultaneously advanced their own interests within the country's tungsten sector. The Bakuta open-pit tungsten mine, located near the Chinese border, has been brought into commercial production with Jiangxi Copper overseeing operations and technology management.

China's Belt and Road Initiative has established deep infrastructure and investment relationships throughout Kazakhstan over many years, creating embedded economic dependencies that cannot be unwound quickly even if political will exists to do so. The result is a dual-dependency dynamic in which Kazakhstan is simultaneously courted by Washington and Beijing for its mineral resources. Astana is strategically positioned to leverage this competition to extract maximum economic benefit, which may mean continuing to route portions of its tungsten output toward China regardless of Western preferences — at least until alternative infrastructure is in place and offering comparable commercial terms. As The Diplomat has noted, the China-US clash over critical minerals presents Kazakhstan with a genuine strategic opportunity, though one that must be navigated carefully.

Long-Term Demand Drivers and Market Growth Projections

The investment thesis for tungsten extends well beyond the current supply shock. Long-term structural demand growth is supported by multiple converging industrial megatrends that are largely independent of short-term price cycles.

Fortune Business Insights estimates the global tungsten market was valued at approximately $5.43 billion in 2025 and projects growth to approximately $9.19 billion by 2034. Research Nester offers a more aggressive projection, forecasting the market could surpass $11 billion by 2035, driven by semiconductor expansion, electrification, and advanced manufacturing growth.

The seven demand drivers most consistently cited across industry forecasts include:

- Aerospace production expansion driven by rising commercial and military aircraft orders globally

- Defence spending acceleration as NATO nations increase procurement of tungsten-dependent munitions and systems

- Semiconductor fabrication growth where tungsten plays a critical role in deposition and interconnect manufacturing processes

- Electric vehicle scale-up with tungsten used in braking systems and drivetrain components

- Renewable energy infrastructure where tungsten-tipped tooling is incorporated into wind and solar installation equipment

- Industrial automation advancement requiring precision tungsten carbide cutting tools across automated manufacturing environments

- AI hardware manufacturing where server and data centre components increasingly incorporate tungsten-based materials

Investor Reframing: Tungsten is undergoing the same fundamental reclassification that lithium experienced between 2015 and 2020, transitioning from a niche industrial input to a technology-critical metal commanding premium valuations and sustained strategic government attention. The difference is that tungsten has no credible substitute in many of its highest-value applications, creating a more durable demand floor than most battery metals.

What a Functioning Western Tungsten Supply Chain Would Actually Require

Building genuine supply chain independence from China in tungsten is not a single transaction outcome. It is a multi-step industrial programme that requires execution across the entire value chain simultaneously.

- Secure mine development financing at the scale required to develop Severniy Katpar to full production capacity

- Establish processing infrastructure outside Chinese control, capable of converting raw tungsten concentrate into intermediate and finished products

- Build viable Caspian transit corridors with the infrastructure investment and multi-nation coordination that requires

- Develop downstream refining and manufacturing capacity in allied nations capable of absorbing large volumes of non-Chinese tungsten

- Create long-term offtake agreements with Western defence contractors, semiconductor manufacturers, and technology hardware producers

- Establish strategic tungsten stockpiles in allied nations as a buffer against future supply disruptions or export restriction escalations

Each of these steps involves multi-year timelines. The uncomfortable reality is that even under the most optimistic development scenario, a fully functional Western tungsten supply chain anchored by Kazakhstani production is a mid-2030s outcome, not a near-term solution to current supply tightness.

The Broader Strategic Picture: From Oil Dependency to Metal Dependency

The structural parallel between 20th-century petroleum geopolitics and 21st-century critical mineral competition is not merely rhetorical. Access to tungsten, rare earths, and battery metals is becoming as strategically consequential as petroleum access once was. However, there is one important difference: oil had liquid global markets with many producing nations, while critical minerals like tungsten have production concentrated in one or two countries with the ability to exercise supply leverage far more decisively than most oil exporters ever could.

The Kazakhstan tungsten deal and China critical minerals supply chain competition represent a test case for whether Western economies can construct credible alternative supply chains at the speed and scale required — before the supply gap becomes an industrial and defence emergency rather than a policy priority. The scale of the Severniy Katpar reserve base gives reason for measured optimism. The logistics complexity, the competing Chinese presence within Kazakhstan, and the multi-year development timelines, however, give reason for strategic patience rather than premature confidence.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Forecasts, market projections, and scenario analyses referenced herein involve inherent uncertainty. Past commodity price movements are not indicative of future performance. Readers should conduct their own due diligence before making any investment decisions.

Want to Stay Ahead of the Next Major Critical Minerals Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across tungsten, rare earths, and over 30 other commodities — converting complex data into clear, actionable opportunities before the broader market reacts. Explore how historic mineral discoveries have generated extraordinary returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the next major find.