June 21, 2026

Precious Metals at a Crossroads: Understanding the Forces Shaping Bullion in 2026

Commodity markets have long operated on the premise that geopolitical risk is temporary while monetary fundamentals are structural. That assumption is being tested in mid-2026 as the US Iran negotiations impact on bullion emerges not as a simple binary risk event, but as a multi-layered force interacting simultaneously with dollar dynamics, energy markets, and central bank policy expectations. For gold and silver investors, the current environment demands a more sophisticated analytical framework than headline-watching alone can provide.

When big ASX news breaks, our subscribers know first

Why Geopolitical Diplomacy Has Displaced Monetary Policy as Bullion's Primary Near-Term Driver

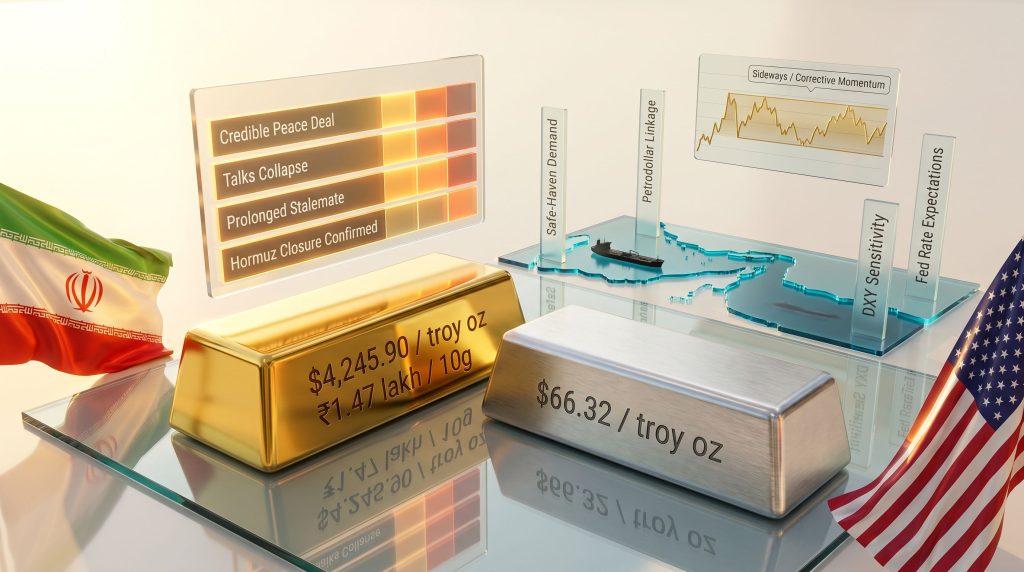

For most of the post-2008 era, gold pricing was predominantly anchored to real interest rates and US dollar strength. Central bank decisions in Washington, Frankfurt, and Tokyo were the primary variables that commodity desks monitored. That calculus has shifted materially in 2026. The resumption of formal US-Iran diplomatic engagement, culminating in a framework agreement and a subsequent round of technical talks scheduled in Burgenstock, Switzerland, has elevated geopolitical risk assessment to the front of the analytical queue.

This shift is not arbitrary. The framework agreement established a 60-day deadline for negotiators to resolve technical details, creating a defined window of elevated uncertainty across commodity markets. Unlike diffuse geopolitical risks such as trade tensions or sanctions disputes, a time-bounded negotiation with explicit milestones generates structured volatility patterns that commodity traders can anticipate and position around.

What makes the current situation particularly complex is that diplomatic progress and precious metals performance do not move in a simple inverse relationship. Instead, the US-Iran negotiations interact with bullion pricing through four distinct transmission channels, each capable of producing contradictory price signals at the same time.

The Four Transmission Channels: How Diplomacy Moves Gold and Silver

Channel 1: Safe-Haven Demand and Risk Sentiment

The most intuitive channel is also the one most frequently oversimplified. When geopolitical tensions rise, institutional and retail investors historically increase allocations to gold as a store of value outside the financial system. The key nuance, however, is that silver's dual identity as both a monetary and industrial metal creates a different sensitivity profile.

Gold safe-haven demand functions almost purely as a monetary hedge during risk-off episodes. Silver, by contrast, carries significant industrial demand from electronics, solar panel manufacturing, and chemical processing sectors. When geopolitical uncertainty suppresses global growth expectations, industrial silver demand comes under pressure at the same time that monetary silver demand rises, creating a net dampening effect relative to gold's safe-haven response.

Channel 2: Petrodollar and Energy Price Dynamics

Iran's position as a significant oil and gas producer means that any shift in the diplomatic relationship between Washington and Tehran carries immediate implications for global energy supply expectations. Falling crude oil prices, which typically follow credible de-escalation signals, reduce inflation expectations across major economies. Lower inflation expectations erode gold's appeal as an inflation hedge in the short term, creating a temporary headwind even in a scenario where the dollar simultaneously weakens.

The Strait of Hormuz amplifies this dynamic considerably. Approximately 20% of global crude oil supply and substantial volumes of liquefied natural gas transit this narrow waterway. Iran's announcement in June 2026 that the strait had been closed following Israeli strikes in Lebanon generated immediate commodity market turbulence, before the US Central Command confirmed that shipping continued uninterrupted. The episode illustrated a critical market dynamic: information asymmetry around Hormuz creates high-amplitude but short-duration price dislocations in both energy and precious metals markets. Furthermore, the precious metals market pressures arising from these energy disruptions can compound rapidly when multiple risk factors align simultaneously.

Channel 3: US Dollar Index Sensitivity

The inverse relationship between the US Dollar Index (DXY) and gold pricing is one of the most structurally consistent correlations in commodity markets. When the dollar strengthens, gold becomes more expensive for non-US buyers, suppressing global demand. Conversely, a weaker dollar amplifies purchasing power for buyers across Asia, the Middle East, and Europe, providing structural support for gold prices.

The DXY closed the week near 100.60, signalling moderate dollar strength that acted as a direct headwind for international gold buyers. A credible US-Iran agreement has the potential to trigger dollar softening as risk appetite improves and capital rotates away from safe-haven currencies, which would in turn provide a secondary tailwind for gold that could partially or fully offset any war premium compression resulting from the deal itself.

Channel 4: Federal Reserve Rate Expectations

The fourth channel operates through the opportunity cost mechanism. Non-yielding assets like gold become less attractive when interest rates rise because investors can earn meaningful returns from fixed-income alternatives. A hawkish Federal Reserve stance, maintained through June 2026, has been identified by analysts as a persistent headwind for bullion.

Easing geopolitical tensions theoretically reduce inflationary pressure by bringing more Iranian oil supply back to global markets and lowering energy costs. If inflation cools as a result, the Fed's justification for maintaining elevated rates weakens, which could shift rate trajectory expectations in a direction favourable to gold. The interaction between PCE inflation data and geopolitical developments therefore creates a compounding analytical challenge for bullion investors.

Current Market Snapshot: Where Prices Stand

The most recent trading week produced a clear divergence between domestic Indian markets and global benchmarks, a divergence that reveals more about currency dynamics than about underlying demand fundamentals.

| Instrument | Weekly Performance | Closing Level |

|---|---|---|

| MCX Gold Futures | Down 2.2% (₹3,325 per 10g) | ₹1.47 lakh per 10g |

| MCX Silver Futures | Down 5.3% (₹13,001 per kg) | ₹2.33 lakh per kg |

| Comex Gold Futures | Marginally higher | $4,245.90 per troy ounce |

| Comex Silver Futures | Down 2.03% | $66.32 per troy ounce |

| US Dollar Index (DXY) | Moderate strength | ~100.60 |

The domestic MCX declines were materially larger than global price moves because a strengthening Indian rupee reduced the landed cost of imported gold priced in US dollars. This currency effect is frequently misread by retail investors as a signal of deteriorating global gold demand, when in reality it reflects rupee appreciation compressing the domestic price premium. Analysts from LKP Securities noted that gold faced headwinds from falling energy prices, rupee strength, and Federal Reserve hawkishness acting simultaneously during the period.

Precious metals momentum is best characterised as sideways to corrective in the immediate term, with directional clarity most likely to emerge once the negotiation window resolves or Federal Reserve rate guidance shifts materially.

Bullion Scenario Matrix: Mapping Outcomes to Price Direction

| Negotiation Outcome | Oil Price Direction | USD Direction | Gold Price Impact | Silver Price Impact |

|---|---|---|---|---|

| Credible Peace Deal | Bearish | Bearish (weakens) | Mildly Bullish (net) | Neutral to Mildly Bullish |

| Talks Collapse / Escalation | Bullish | Bullish (strengthens) | Mixed (safe-haven vs. rate fears) | Bearish (industrial demand concern) |

| Prolonged Stalemate | Sideways / Volatile | Sideways | Corrective / Range-Bound | Underperformance vs. Gold |

| Confirmed Hormuz Closure | Sharply Bullish | Initially Bearish | Strongly Bullish | Bullish |

| Full Nuclear Deal Revival | Bearish | Bearish | Moderately Bullish | Neutral |

The table above highlights one of the most counterintuitive features of the current environment: a successful peace deal is not necessarily bearish for gold in aggregate. If it simultaneously weakens the dollar and suppresses oil prices, it can produce a net positive for bullion even as the war premium compresses. According to recent market analysis, gold prices have continued to edge higher precisely because investors are weighing these competing factors rather than reacting to diplomatic headlines in isolation.

The Strait of Hormuz: A Physical Chokepoint With Outsized Market Consequences

Few geographic features carry more commodity market significance per square kilometre than the Strait of Hormuz. The waterway connects the Persian Gulf to the Gulf of Oman and serves as the transit corridor for exports from Saudi Arabia, Iraq, the UAE, Kuwait, and Iran. Beyond crude oil, it handles significant LNG volumes destined for South and East Asian import terminals.

A confirmed closure, even for a matter of days, would produce cascading repricing across energy, shipping, and commodity markets globally. For silver specifically, the industrial demand implications would be significant. Manufacturers in electronics and solar sectors, which collectively represent a growing share of annual silver consumption, depend on stable energy costs and uninterrupted supply chains. An energy shock originating from Hormuz disruption would compress industrial margins and reduce silver offtake in key manufacturing economies across Asia.

Analysts monitoring the JM Financial commodity desk have characterised the US Iran negotiations impact on bullion as sideways to corrective specifically with reference to Hormuz flow continuity as a key watch variable alongside the negotiation timeline.

The next major ASX story will hit our subscribers first

The Macro Data Dashboard: What Investors Are Watching Beyond Diplomacy

While geopolitical developments dominate near-term sentiment, several scheduled data releases and policy events will interact with diplomatic headlines to determine the net directional outcome for bullion over the coming weeks.

Key macro events and their bullion relevance:

- People's Bank of China monetary policy decision: A looser PBOC stance supports yuan-denominated gold demand and signals broader EM risk appetite

- Flash Manufacturing and Services PMI: Forward indicators for global industrial activity directly influence silver's demand outlook

- US PCE Inflation Data: The Federal Reserve's preferred inflation gauge; a hotter-than-expected reading reinforces the hawkish case and increases gold's opportunity cost

- US Housing Numbers: Secondary indicator for consumer financial health and the trajectory of shelter inflation

- Consumer Sentiment Readings: Proxy for retail investor risk appetite with indirect implications for safe-haven allocation behaviour

- Federal Reserve official commentary: The single most important variable for near-term gold direction given the current rate-sensitive environment

The Russia-Ukraine conflict provides an important contextual backdrop to all of the above. Ongoing hostilities in Eastern Europe maintain a structural floor under safe-haven demand that is independent of West Asia developments, meaning that even a fully successful US-Iran agreement would not eliminate all geopolitical risk premiums from bullion valuations.

Structural Pillars: Why Long-Term Gold Bulls Are Treating Diplomatic Volatility as Noise

Investors with longer time horizons tend to interpret geopolitical-driven gold price swings through an entirely different analytical lens. Three structural demand pillars remain firmly intact regardless of how the US-Iran negotiation unfolds.

-

Central bank accumulation: Sovereign gold purchasing by emerging market central banks, particularly across Asia and the Middle East, has established a durable demand floor beneath spot prices. Understanding gold and silver central banks activity reveals that this trend reflects reserve diversification strategies operating on multi-year rather than quarterly timelines.

-

De-dollarisation trends: The gradual shift by emerging market economies away from US dollar-denominated reserve assets structurally supports gold as an alternative reserve instrument. This dynamic is driven by geopolitical fragmentation of the global financial system rather than by any single negotiation outcome. The ongoing central bank gold buying behaviour further reinforces this structural shift.

-

Fiscal deficit concerns: Elevated government debt levels across the US, Japan, and Europe sustain gold's appeal as a hedge against long-term currency debasement risk, independent of near-term inflation readings.

For long-term investors, the tactical price compression created by positive diplomatic headlines represents an accumulation opportunity within a broader structural bull market, not a trend reversal. The distinction between war premium compression (a tactical, reversible phenomenon) and a fundamental demand deterioration (a structural shift) is critical for interpreting bullion price movements during the 60-day negotiation window. Consequently, reviewing gold-silver ratio analysis can help investors identify relative value opportunities even during periods of heightened diplomatic uncertainty.

Frequently Asked Questions: US-Iran Negotiations and Bullion Markets

Does a US-Iran peace deal automatically push gold prices lower?

Not necessarily. While a credible agreement removes the embedded geopolitical risk premium, the simultaneous effects on the US dollar and oil prices can offset or even reverse any initial selloff. If the deal weakens the dollar and reduces energy inflation, the net impact on gold may be mildly positive despite the removal of the war premium.

Why does the Strait of Hormuz matter specifically for silver prices?

Silver has substantial industrial demand concentrated in electronics manufacturing, solar energy production, and chemical processing. A Hormuz disruption would raise global energy costs, compress industrial margins in key silver-consuming sectors, and reduce offtake from manufacturing economies across Asia, creating a distinct bearish pressure on silver that does not apply equally to gold.

How large is the current war premium in gold?

The war premium is the additional price investors pay above gold's fundamental value to compensate for geopolitical risk. Analyst estimates place this premium in the range of $50 to $150 per troy ounce during active conflict cycles, though the precise figure varies by methodology and is not directly observable. The current environment, with multiple simultaneous geopolitical flashpoints, likely supports a premium toward the upper end of that range.

How does a stronger Indian rupee affect MCX gold prices?

India imports the vast majority of its gold supply, priced in US dollars. When the rupee strengthens against the dollar, the landed cost of imported gold falls in rupee terms, which pushes MCX prices lower even when international Comex prices are stable or rising. This creates periodic divergences between domestic and global gold performance that reflect currency dynamics rather than shifts in fundamental demand. Broader global market sentiment across Asia has similarly reflected caution ahead of key negotiation milestones, compounding the pressure on domestic bullion benchmarks.

Investment Positioning: Navigating the 60-Day Negotiation Window

The US Iran negotiations impact on bullion creates two distinct time horizons that warrant separate strategic responses from investors.

Short-term tactical considerations (0 to 60 days):

- The negotiation deadline creates a bounded volatility window with defined scenario endpoints

- Positive diplomatic progress should be interpreted as war premium compression rather than a structural trend reversal

- Dollar and yield dynamics will determine whether safe-haven buying or rate pressure dominates in breakdown scenarios

- Hormuz flow continuity remains the single most consequential physical risk variable for near-term commodity repricing

Medium-term strategic positioning (60 days to 12 months):

- A fully ratified nuclear agreement would structurally reduce Middle East risk premiums, but structural gold demand from central banks and reserve diversification remains intact

- PCE data and Federal Reserve rate decisions are the primary medium-term price determinants once the negotiation window closes

- Multi-theatre geopolitical risk from the Russia-Ukraine conflict provides a structural demand floor beneath any diplomatic-driven price compression

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Precious metals markets involve significant risk, and past performance is not indicative of future results. Readers should conduct independent research and consult qualified financial professionals before making investment decisions. All price data referenced reflects market conditions as reported in late June 2026.

Want to Stay Ahead of the Next Major Mineral Discovery on the ASX?

While precious metals navigate complex geopolitical crosscurrents, Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries — instantly translating complex data into actionable investment opportunities for both short-term traders and long-term investors. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin your 14-day free trial to position yourself ahead of the broader market.