June 8, 2026

The geopolitical landscape of global supply chains has entered a phase where mineral resources function as instruments of statecraft rather than mere commodities. Nations controlling processing capabilities for rare earth elements, lithium, cobalt, and graphite wield influence over everything from defense manufacturing to renewable energy deployment. The United States now confronts a strategic vulnerability that extends far beyond traditional trade dependencies, with US reducing reliance on China for rare earths becoming a crucial national security imperative reaching into the core infrastructure of economic competitiveness.

Understanding this challenge requires examining how specific mineral applications create systemic risks across multiple sectors. When a single nation controls the majority of processing capacity for materials essential to both military equipment and civilian technology, the implications cascade through entire economic systems.

Defense Systems Dependent on Specialized Materials

Military applications of rare earth elements center on their unique magnetic and phosphorescent properties that enable advanced electronic systems. Neodymium-iron-boron permanent magnets, containing high concentrations of neodymium and dysprosium, power precision guidance systems in missiles and smart munitions. These same materials drive electric motors in naval propulsion systems and enable the miniaturization of electronic warfare equipment.

The defense sector's vulnerability extends beyond individual components to integrated systems requiring multiple rare earth elements. Radar arrays depend on yttrium for high-frequency operations, while sonar systems utilize terbium-based phosphors for underwater detection capabilities. Furthermore, modern fighter aircraft incorporate dozens of rare earth-dependent subsystems, creating potential points of failure if supply chains face disruption.

According to International Energy Agency assessments, China's dominance extends across 47% to 87% of global refining capacity for copper, lithium, cobalt, graphite, and rare earths. This concentration creates strategic dependencies that military planners must address through defense materials strategy or technological substitution.

Economic Sectors Facing Supply Chain Vulnerabilities

Beyond defense applications, rare earth dependencies permeate civilian infrastructure development. Wind turbine permanent magnets typically require 200-600 kilograms of neodymium and dysprosium per 2-3 megawatt installation. As renewable energy deployment accelerates, these material requirements scale proportionally, creating potential bottlenecks in clean energy transitions.

Electric vehicle manufacturing presents similar challenges. Each electric motor contains approximately 1-2 kilograms of rare earth materials, primarily neodymium and dysprosium for performance optimization. Tesla's Model 3, for instance, utilizes rare earth-free induction motors specifically to avoid supply chain dependencies, demonstrating industry awareness of these vulnerabilities.

The semiconductor manufacturing sector faces indirect exposure through equipment dependencies. While silicon wafers do not contain rare earths, the production machinery requires rare earth-based permanent magnets for precision positioning and high-vacuum systems. Consequently, disruptions in rare earth supply chains could constrain semiconductor manufacturing capacity, amplifying effects across technology sectors.

| Critical Mineral | Primary Defense Application | Civilian Technology Use | Processing Concentration |

|---|---|---|---|

| Neodymium | Missile guidance systems | Wind turbine magnets | 85% China |

| Dysprosium | Electronic warfare systems | Electric vehicle motors | 90% China |

| Terbium | Naval sonar equipment | LED display phosphors | 88% China |

| Yttrium | Radar systems | Fiber optic communications | 82% China |

When big ASX news breaks, our subscribers know first

How China Established Dominance Over Global Rare Earth Processing

China's control over rare earth supply chains resulted from strategic government investment combined with regulatory frameworks that externalized environmental costs. Beginning in the 1990s, Beijing consolidated domestic rare earth production under fewer operators while investing heavily in downstream processing capabilities. This approach created integrated supply chains that competitors struggle to replicate economically.

Strategic Consolidation and Infrastructure Development

The Chinese government's approach differed fundamentally from market-driven development models. Rather than allowing pure competition, authorities guided industry consolidation through Baotou Steel Rare-Earth & Hightech Company and other state-influenced entities. This centralized control enabled coordinated investment in processing infrastructure that individual companies might not pursue due to capital intensity and technical complexity.

Chinese rare earth processing facilities operate with regulatory frameworks that historically imposed less stringent environmental controls compared to Western operations. This regulatory environment allowed cost structures that made competing operations economically challenging. However, while environmental regulations have tightened in recent years, the accumulated cost advantages and technical expertise remain significant barriers for new entrants.

Processing Technology and Expertise Concentration

Rare earth refining involves three technically demanding stages: concentration of raw ore, chemical extraction through leaching processes, and separation of individual elements using solvent extraction. China's advantage extends beyond mining to mastery of complex hydrometallurgical and separation processes that require decades of operational optimization.

The separation stage presents the highest technical barriers. Lanthanide elements share similar chemical properties, making isolation extremely challenging. Furthermore, Chinese facilities have developed proprietary solvent extraction processes and accumulated institutional knowledge that new operations cannot easily replicate. This expertise gap explains why even countries with substantial rare earth deposits struggle to establish competitive processing operations.

According to industry analyses of global rare earth cost structures, Chinese operations benefit from integrated facilities handling all processing stages, reducing transportation costs and enabling operational efficiencies that standalone operations cannot achieve.

The Molycorp bankruptcy in 2015 illustrates these challenges. Despite owning the Mountain Pass Mine, the largest rare earth deposit in the United States, Molycorp failed primarily because it could not achieve profitable separation of individual rare earth elements domestically. The company's collapse demonstrated that mining capacity alone is insufficient without integrated processing capabilities.

Which Nations Are Developing Alternative Supply Networks?

International efforts to diversify rare earth supply chains focus on countries with substantial deposits and governance structures attractive to foreign investment. These initiatives require coordinated development of critical minerals energy security through mining, processing, and manufacturing capabilities to create viable alternatives to Chinese supply chains.

Australia's Integrated Partnership Strategy

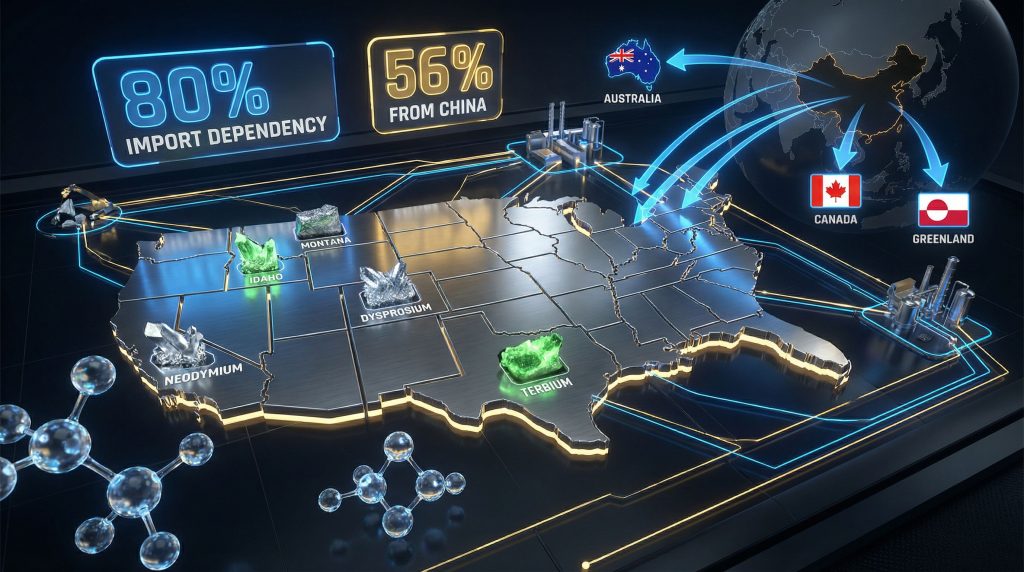

Australia has emerged as the primary alternative supplier through strategic partnerships with consuming nations. In October 2025, the United States signed an agreement with Australia for an $8.5 billion project pipeline aimed at countering China's dominance in critical minerals. This partnership leverages Australia's proposed strategic reserve to supply metals vulnerable to disruption.

Following the U.S. agreement, Australia received interest from Europe, Japan, South Korea, and Singapore, indicating broader international demand for supply chain diversification. Lynas Rare Earths, operating the Mount Weld mine in Western Australia with processing facilities in Malaysia, represents the most advanced non-Chinese integrated operation currently operational.

Australian projects benefit from transparent regulatory frameworks and proximity to Asian manufacturing centers. However, scaling requires substantial capital investment in processing infrastructure. Current Australian capacity focuses primarily on light rare earth elements, with heavy rare earth separation requiring additional technological development and investment.

Canada's North American Integration Model

Canadian rare earth development emphasizes integration with United States supply chains under frameworks established by the United States-Mexico-Canada Agreement (USMCA). Quebec deposits, including the Montviel and Kipawa projects, offer potential sources for North American rare earth production with shorter supply lines than overseas alternatives.

Canadian projects must navigate consultation requirements under the Canadian National Action Plan on Responsible Business Conduct, particularly regarding First Nations partnerships. These consultation processes, while extending development timelines, create more sustainable frameworks for long-term operations compared to regions with less robust environmental and social governance standards.

The integrated North American approach recognises that individual countries cannot efficiently replicate China's entire supply chain. Instead, Canada focuses on mining and preliminary processing, with refined separation potentially occurring in United States facilities. This division of labour optimises each country's comparative advantages while maintaining supply chain security within allied territories.

European Union's Strategic Autonomy Framework

The European Commission's Critical Raw Materials Act, adopted in 2023, establishes targets for supply chain diversification by 2030. EU objectives include sourcing no more than 65% of any critical mineral from a single third country, requiring substantial diversification from current Chinese dependencies.

European initiatives focus on strategic partnerships with resource-rich nations rather than domestic production alone. The EU's approach emphasises technology transfer and investment facilitation to develop alternative suppliers while maintaining access to European markets for processed materials.

Greenland's Kvanefjeld project, containing rare earth deposits along with uranium, represents a potential European supply source. However, environmental concerns and regulatory challenges have delayed development. The project's current status remains uncertain due to political changes in Greenland and ongoing environmental assessments.

| Country | Production Capacity Target | Development Timeline | Key Advantages |

|---|---|---|---|

| Australia | 15% global processing share | 2030-2032 | Existing operations, stable governance |

| Canada | Integrated North American supply | 2030-2035 | USMCA integration, shorter supply lines |

| European Sources | 35% non-Chinese sourcing | 2030 | Technology transfer, market access |

How Are U.S. Domestic Projects Addressing Supply Dependencies?

American efforts to establish domestic rare earth capabilities centre on reviving the Mountain Pass Mine while developing integrated processing infrastructure. These projects must overcome both technical challenges and cost competitiveness issues that previously led to industry consolidation in China, as part of the broader US reducing reliance on China for rare earths strategy.

Mountain Pass Mine's Strategic Revival

MP Materials Corporation acquired the Mountain Pass Mine from Molycorp's bankruptcy and has implemented a phased approach to establishing domestic processing capabilities. Unlike Molycorp's attempt to build complete separation facilities immediately, MP Materials is developing capabilities incrementally to reduce technical and financial risks.

Current operations focus on mining and producing rare earth concentrates, with initial processing sending concentrates to China for separation. This approach provides revenue streams while MP Materials develops domestic separation capabilities. Phase 1 targets light rare earth element separation, achievable with 2-3 year development timelines and established technology.

Phase 2 development will address heavy rare earth element separation, which requires more complex chemistry and represents higher technical risks. Heavy rare earth elements, including dysprosium and terbium, command higher prices but require specialised separation processes that few facilities outside China have mastered.

Emerging Processing Infrastructure Development

Beyond Mountain Pass, additional projects aim to establish rare earth processing capabilities in strategic locations. Texas has attracted interest for processing facilities due to existing chemical industry infrastructure and access to international shipping. However, specific project announcements require verification against official state economic development records.

Idaho National Laboratory participates in critical minerals research through programmes focused on extraction methodology optimisation and recycling technologies. These research partnerships aim to develop processes that improve extraction efficiency while reducing environmental impacts compared to traditional methods through AI optimization in mining.

The Department of Defense's Defense Production Act Title III investments provide funding for strategic projects deemed essential to national security. These programmes offer risk mitigation for private investors by providing government backing for projects that might not achieve commercial viability under pure market conditions.

What Role Does Technology Innovation Play in Domestic Operations?

American projects emphasise technological innovation to overcome cost disadvantages compared to established Chinese operations. Advanced extraction techniques, including in-situ leaching and biotechnology applications, aim to reduce processing costs while minimising environmental impacts.

Artificial intelligence optimisation of extraction processes represents another technological advantage. Machine learning algorithms can optimise chemical processes and reduce waste streams, potentially achieving cost competitiveness with traditional methods. These technologies require substantial development investment but offer pathways to sustainable domestic production.

Recycling technologies for end-of-life products containing rare earth elements present additional supply sources. Urban mining of electronic waste could provide significant rare earth recovery, though current separation costs remain higher than primary mining. Research focuses on cost-effective separation technologies that could make recycling economically viable.

The United States currently imports approximately 80% of its rare earth requirements, with significant portions originating from China either directly or through intermediate processing countries. Domestic projects aim to reduce this dependency to 40% by 2030, though achieving this target requires successful development of processing capabilities rather than mining alone.

What Role Do International Alliances Play in Supply Security?

Coordinated international action amplifies individual nations' leverage in developing alternative supply chains. When countries representing 60% of global critical mineral demand coordinate purchasing and development strategies, they create sufficient market power to influence supplier behaviour and justify large-scale infrastructure investments.

Diplomatic Urgency and Implementation Challenges

Recent diplomatic meetings reveal frustration among allied nations about implementation speed despite broad agreement on strategic objectives. U.S. Treasury Secretary Scott Bessent's January 2026 meetings with G7 finance ministers, European Union representatives, and officials from Australia, India, South Korea, and Mexico emphasised that coordination exists but execution requires acceleration.

The diplomatic urgency stems from recognition that supply chain vulnerabilities continue expanding while alternative infrastructure develops slowly. As U.S. officials noted, there are many different angles and countries involved, and the need to move faster has become paramount for achieving meaningful supply chain resilience.

Japan's experience provides both precedent and cautionary lessons for current initiatives. Following China's abrupt restriction of critical mineral supplies to Japan in 2010, Tokyo successfully diversified sources toward Vietnam, Myanmar, and Australia. However, this diversification required over a decade and substantial government support for alternative suppliers.

Minerals Security Partnership Coordination Mechanisms

The Minerals Security Partnership represents a multilateral framework for coordinating critical minerals development among allied nations. Partner countries share investment risks for third-country projects while harmonising technical standards for minerals processing and trading.

Coordination extends beyond financial support to technology sharing for processing innovations and intelligence sharing regarding supply security threats. This approach recognises that individual countries cannot efficiently replicate China's integrated supply chains but can collectively develop competitive alternatives through specialisation and coordination.

Joint investment mechanisms reduce individual country risks while enabling larger-scale projects that achieve greater cost competitiveness. Furthermore, when multiple nations coordinate offtake agreements, project developers gain demand certainty that justifies substantial capital investments in processing infrastructure.

Regional Integration Through Trade Agreements

The Indo-Pacific Economic Framework (IPEF) incorporates supply chain resilience as a core objective, with critical minerals representing a priority area for regional coordination. IPEF members aim to develop integrated supply chains that reduce dependencies on non-partner countries while maintaining cost competitiveness.

Regional integration recognises geographic advantages in critical minerals development. Southeast Asian nations possess substantial rare earth deposits and lower labour costs, while more developed economies provide technology and capital for processing infrastructure. Coordinated development optimises these comparative advantages while maintaining supply chain security within allied frameworks.

NATO's elevation of supply chain security to collective defence considerations reflects recognition that economic dependencies can create strategic vulnerabilities equivalent to traditional military threats. While NATO's Article 5 framework historically focused on territorial defence, economic security discussions acknowledge that supply chain weaponisation represents a form of hybrid warfare requiring collective responses.

Recent reports indicate China has begun restricting exports to Japanese companies of rare earths and powerful magnets, while banning exports of dual-use items to Japanese military applications. These actions demonstrate how supply chain control can be weaponised for geopolitical objectives, validating concerns driving allied coordination efforts.

Which Technologies Could Accelerate Supply Chain Independence?

Technological innovations offer pathways to reduce rare earth dependencies through alternative materials, improved recycling, and more efficient extraction processes. These technologies require substantial development investment but could fundamentally alter supply chain dynamics if successfully commercialised, supporting the broader mining industry evolution toward greater independence.

Alternative Material Development

Research into rare earth-free permanent magnets represents the most transformative potential technology for reducing dependencies. Alternative magnet technologies, including manganese-based compounds and iron nitride materials, aim to match the performance of neodymium-iron-boron magnets without rare earth content.

Tesla's adoption of rare earth-free induction motors in some vehicle models demonstrates that alternatives exist for specific applications, though with performance trade-offs. Induction motors achieve comparable efficiency but require larger sizes and weights compared to permanent magnet systems, illustrating the challenges in developing complete substitutes.

Advanced research focuses on nanostructured materials and composite systems that could achieve similar magnetic properties using more abundant elements. While promising in laboratory settings, scaling these technologies to industrial production requires overcoming significant manufacturing challenges and cost competitiveness hurdles.

Urban Mining and Recycling Technologies

Electronic waste processing for rare earth recovery presents substantial opportunities given the accumulated stock of devices containing these materials. Current recycling rates for rare earths remain below 5% globally, primarily due to economic challenges in separation processes rather than technical impossibility.

Biotechnology applications in mineral processing offer potential breakthroughs in recycling economics. Bacterial leaching processes and bioengineered organisms designed to concentrate specific elements could reduce processing costs while minimising environmental impacts compared to traditional chemical separation methods.

Automated disassembly systems combined with advanced separation technologies could make urban mining economically viable. Machine learning algorithms can optimise device disassembly for maximum material recovery while reducing labour costs that currently make recycling uneconomical for many applications.

Advanced Extraction and Processing Innovations

In-situ leaching techniques reduce environmental disruption while potentially lowering extraction costs compared to traditional mining. These methods inject solutions to dissolve target minerals underground, then pump enriched solutions to surface processing facilities. While established for uranium extraction, adapting these techniques to rare earth deposits requires additional technological development.

Artificial intelligence optimisation of extraction processes enables real-time adjustment of chemical parameters to maximise recovery rates while minimising waste generation. Machine learning systems can identify optimal extraction conditions faster than traditional trial-and-error approaches, potentially reducing development timelines for new processing facilities.

| Technology Category | Commercialisation Timeline | Potential Impact | Required Investment |

|---|---|---|---|

| Rare earth-free magnets | 2028-2030 | Revolutionary | $5-8 billion |

| Advanced recycling | 2026-2027 | Significant | $2-3 billion |

| Bio-extraction processes | 2030-2032 | Transformative | $3-5 billion |

| AI-optimised processing | 2025-2027 | Incremental | $1-2 billion |

The next major ASX story will hit our subscribers first

What Economic Incentives Are Driving Private Investment?

Government support mechanisms aim to overcome market failures that prevent competitive rare earth industries from developing in Western economies. These incentives address the reality that competing with subsidised Chinese operations requires risk mitigation and cost support that pure market mechanisms cannot provide.

Federal Funding and Risk Mitigation Programmes

Defense Production Act Title III investments provide government backing for projects deemed essential to national security but commercially risky under normal market conditions. These programmes offer both direct funding and guaranteed purchase agreements that reduce investor risks in developing processing capabilities.

Department of Energy loan guarantee programmes enable private companies to access capital for large-scale projects at reduced interest rates. Given the capital intensity of rare earth processing facilities, which can require $500 million to $1 billion+ investments, access to low-cost capital significantly improves project economics.

Tax incentives for domestic processing facilities include accelerated depreciation schedules and production tax credits that improve long-term project returns. These incentives recognise that domestic operations may require ongoing support to compete with established international suppliers operating under different regulatory and cost structures.

Market Development and Demand Certainty

Government offtake agreements provide demand certainty that enables private investment in processing capabilities. When the Department of Defense commits to purchasing specified quantities of domestically processed rare earths at predetermined prices, investors gain revenue certainty that justifies substantial capital commitments.

Strategic stockpile purchases support market development while building national reserves for supply security. These purchases provide immediate revenue streams for domestic producers while creating buffer stocks that reduce vulnerability to supply disruptions.

Price floor mechanisms protect investors against predatory pricing strategies that could undermine domestic industry development. Given China's ability to manipulate rare earth prices through export controls or subsidised dumping, price protection enables sustained domestic industry development.

Public-Private Partnership Models

Cost-sharing arrangements for high-risk projects enable government participation in development while maintaining private sector efficiency incentives. These partnerships typically involve government funding for technology development phases while private partners manage commercial operations and scaling.

Technology transfer from national laboratories provides access to research developments that individual companies could not afford to develop independently. Idaho National Laboratory's critical minerals research, for instance, offers processing innovations that private companies can licence and commercialise with reduced development risks.

Regulatory streamlining for strategic projects accelerates permitting processes that traditionally create lengthy delays for mining and processing operations. Environmental reviews and permitting can require 5-10 years for major projects, and expedited processes significantly improve project economics by reducing development timelines and associated carrying costs.

How Might China Respond to Western Diversification Efforts?

China's potential responses to supply chain diversification range from market competition strategies to export controls and diplomatic pressure on alternative suppliers. Understanding these potential responses helps Western nations prepare counter-strategies and develop resilient frameworks for supply chain independence.

Export Control and Trade Policy Escalation

Recent restrictions on rare earth and magnet exports to Japanese companies demonstrate China's willingness to use supply chain control as a geopolitical tool. These selective restrictions target specific applications while maintaining broader trade relationships, creating pressure without triggering comprehensive trade wars as part of broader US–China trade impacts.

Quota systems limiting total export volumes represent another policy tool that China has employed historically. By constraining overall supply availability, China can maintain price control and market influence while developing domestic downstream industries that consume raw materials domestically rather than exporting them.

Quality specifications and technical standards can create non-tariff barriers that favour Chinese suppliers. Given China's dominance in processing technology, specifications that require particular processing methods or purity levels could disadvantage alternative suppliers lacking comparable technical capabilities.

Market Competition and Pricing Strategies

Price manipulation represents China's most powerful competitive tool given its cost advantages and market control. Temporary price reductions can undermine alternative suppliers' economic viability, particularly during the vulnerable early years of project development when operators face high fixed costs and limited cash flows.

Vertical integration strategies extend Chinese control into downstream applications, making it more difficult for alternative suppliers to access end markets. When Chinese companies control magnet manufacturing, motor assembly, and final product integration, upstream suppliers face limited market access regardless of competitive positioning.

Strategic acquisitions in third-country projects could prevent alternative suppliers from developing competitive capabilities. Chinese investments in Australian, Canadian, or African rare earth projects might provide access to raw materials while preventing independent development of non-Chinese supply chains.

Diplomatic and Economic Pressure Campaigns

Economic incentives for continued Chinese partnerships might include preferential trade agreements, infrastructure investments, or technology transfer offers that compete with Western alternatives. China's Belt and Road Initiative demonstrates the country's ability to provide comprehensive economic packages that influence partner countries' strategic decisions.

Technology transfer offers to maintain market relationships could provide short-term benefits to alternative suppliers while creating long-term dependencies. Chinese companies might offer processing technology or joint venture arrangements that appear beneficial but ultimately constrain independent capability development.

Infrastructure investment competing with Western alternatives represents another diplomatic tool. When China offers to build processing facilities, transportation infrastructure, or power generation capacity in resource-rich countries, these investments can influence those nations' alignment with Chinese rather than Western supply chains.

What Timeline Should Investors Expect for Supply Chain Transformation?

Realistic timelines for rare earth supply chain transformation span decades rather than years, reflecting the complexity of establishing competitive processing capabilities and integrated manufacturing systems. Investors should prepare for extended development periods with significant milestone achievements rather than rapid complete transitions in US reducing reliance on China for rare earths.

Short-term Milestones (2025-2027)

Initial domestic processing capacity is expected to come online through expanded operations at Mountain Pass and potentially new facilities in strategic locations. These early-stage facilities will likely focus on light rare earth element separation, which presents lower technical barriers than heavy rare earth processing.

Strategic stockpile establishment completion will provide buffer capacity for supply disruptions while supporting domestic industry development through guaranteed purchases. These stockpiles serve dual purposes of national security and market development, creating demand certainty for emerging suppliers.

First alternative supplier agreements becoming operational include expanded Australian production capacity and initial Canadian project development. However, these early-stage operations will supplement rather than replace Chinese supply, representing incremental rather than transformational change.

Medium-term Targets (2028-2032)

A 40% reduction in Chinese import dependency represents an ambitious but achievable target given coordinated development of domestic and allied supplier capabilities. This reduction requires successful operation of multiple processing facilities and established supply chain integration with downstream manufacturers.

Integrated North American supply chain functionality would enable rare earth mining in Canada with processing in the United States, or vice versa, creating regional supply security within allied territories. This integration requires regulatory harmonisation and transportation infrastructure development between partner countries.

Technology alternatives reaching commercial viability could include rare earth-free magnet systems for specific applications and advanced recycling processes that provide meaningful secondary supply sources. These technologies require continued research investment and scaling to achieve cost competitiveness with traditional materials.

Long-term Vision (2033-2040)

Complete supply chain independence for critical applications remains aspirational but represents the strategic objective driving current investments. Achieving this independence requires not only raw material production and processing but also downstream manufacturing capabilities for magnets, motors, and finished systems.

Global leadership in sustainable extraction technologies could position Western countries as preferred suppliers for nations concerned about environmental and social governance standards. This leadership combines technical innovation with regulatory frameworks that address environmental externalities that traditional operations often ignore.

Export capacity to allied nations represents the ultimate measure of supply chain transformation success. When Western countries can supply rare earth materials to global markets rather than merely meeting domestic needs, true supply chain independence will have been achieved.

The transformation from Chinese dependency to supply chain resilience represents a generational undertaking requiring sustained political commitment across multiple election cycles and unprecedented coordination among allied nations with different economic priorities and regulatory frameworks.

Navigating Investment Opportunities in Supply Chain Transformation

The movement toward rare earth supply chain independence creates significant opportunities for informed investors while requiring realistic expectations about development timelines and risk factors. Success demands understanding both the technical challenges of establishing competitive processing capabilities and the geopolitical dynamics driving government support for strategic industries.

Private investment opportunities span mining operations, processing technology development, and downstream applications requiring rare earth materials. Government support mechanisms, including loan guarantees, tax incentives, and purchase agreements, improve project economics while reducing typical commodity investment risks through strategic importance recognition.

However, investors must prepare for extended development periods with substantial capital requirements and uncertain competitive dynamics. Chinese responses to Western diversification efforts could include market manipulation, acquisition attempts, or diplomatic pressure that affects project viability. Successful investment strategies require comprehensive risk assessment and portfolio diversification across multiple projects and technologies.

The strategic imperative driving US reducing reliance on China for rare earths ensures continued political support regardless of electoral changes, though implementation approaches may vary based on policy priorities and international developments. This consistency provides foundation for long-term investment planning while requiring flexibility to adapt to evolving market conditions and technological developments.

Ready to Invest in Critical Minerals Before Major Discoveries?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, helping investors identify opportunities in the critical minerals sector as supply chain diversification creates new market dynamics. Visit Discovery Alert's dedicated discoveries page to understand how major mineral discoveries can generate substantial returns, then begin your 30-day free trial to position yourself ahead of the market in this rapidly evolving sector.