June 4, 2026

The Mine-to-Market Problem Redefining North American Trade

The global race to secure critical mineral supply chains is exposing a structural weakness that no single nation can solve alone. Decades of underinvestment in domestic mining capacity, combined with the concentration of mineral processing in China, have left Western economies scrambling to retrofit their industrial strategies around resources they cannot reliably access. Within this broader context, the USMCA review and critical minerals in Mexico have emerged as one of the most consequential intersections of trade policy and resource security in the Western Hemisphere.

Understanding why requires stepping back from the headlines and examining the underlying geology, economics, and geopolitics simultaneously. The July 2026 USMCA joint review is not simply a scheduled trade audit. It is arriving at a moment when North America's collective mineral vulnerability has become impossible to ignore, and when Mexico's resource endowment sits at the centre of a three-way contest between allied cooperation, national sovereignty, and Chinese economic influence.

When big ASX news breaks, our subscribers know first

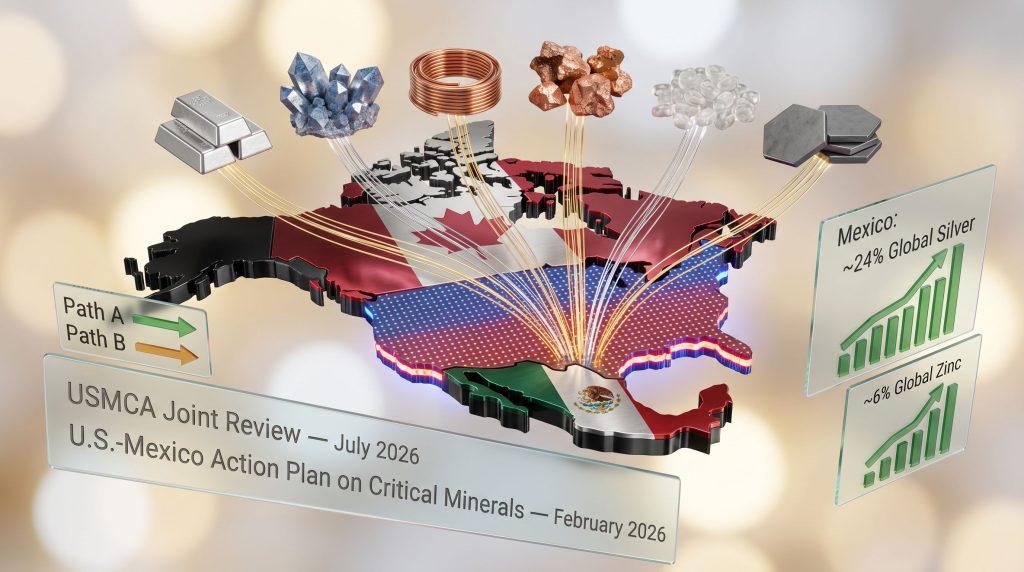

What the July 2026 USMCA Joint Review Actually Requires

The United States-Mexico-Canada Agreement contains a built-in joint review clause requiring all three signatory nations to formally assess the agreement's performance every six years, with the next formal review due by July 1, 2026. Importantly, this review does not automatically trigger renegotiation. It creates an obligation for dialogue, but binding changes to the agreement's architecture require consensus among all three parties.

What makes the 2026 review structurally different from a routine trade assessment is the convergence of three separate pressure tracks. Furthermore, each track carries its own momentum that is difficult to separate from the others:

- Tariff inconsistencies persisting between USMCA member states, particularly U.S. Section 232 steel and aluminium tariffs applied to Mexico despite the agreement's existence — an issue closely tied to broader concerns around tariffs and supply chains

- Supply chain realignment imperatives driven by U.S. efforts to reduce dependence on Chinese-controlled mineral processing

- Mexican domestic policy shifts since 2022 that have complicated foreign investment in its mining sector

The February 2026 announcement of a 60-day U.S.-Mexico Action Plan on Critical Minerals, attributed to U.S. Trade Representative Ambassador Jamieson Greer, added a formal bilateral dimension to what had previously been a more diffuse discussion. That action plan identified copper, silver, lithium, graphite, and zinc as priority minerals, framing their development explicitly in terms of reducing North American exposure to Chinese-controlled supply flows. The findings from that process are now feeding directly into the broader USMCA review deliberations.

Mexico's Mineral Endowment: Deeper Than Most Investors Realise

Mexico is frequently discussed in commodity markets as a silver and zinc producer, which undersells the true scope of its resource base. A more complete picture reveals a country whose geological diversity spans multiple critical mineral categories simultaneously.

| Mineral | Mexico's Approximate Global Production Share | Strategic Relevance |

|---|---|---|

| Silver | ~24% | Solar panels, electronics, industrial applications |

| Zinc | ~6% | Industrial use, emerging battery chemistry |

| Molybdenum | ~6% | Steel hardening, aerospace, energy infrastructure |

| Copper | Significant and growing | EV motors, grid infrastructure, renewables |

| Lithium | Emerging, nationalised | Battery inputs, constrained by policy |

| Graphite | Identified in Action Plan | Li-ion battery anodes, Chinese-dominated globally |

What is less commonly understood is how Mexico's profile complements rather than competes with the mineral strengths of its USMCA partners. The United States produces roughly 56% of global beryllium output and contributes meaningfully to molybdenum supply at around 14% of world production. Canada holds significant niobium and lithium assets. Mexico's strengths in silver, zinc, copper, and molybdenum fill precise gaps in a potential integrated North American supply chain model, particularly given rising critical minerals demand for clean energy and defence applications.

The value of regional complementarity in critical minerals is not simply additive. When extraction, processing, and manufacturing capacity are distributed across allied nations within a single trade framework, the resulting supply chain becomes structurally more resistant to disruption than any single-nation approach could achieve.

The Nearshoring Multiplier Effect

Mexico's strategic mineral relevance is further amplified by the nearshoring trend. As multinational manufacturers relocate production capacity closer to U.S. end markets, Mexico has become a primary beneficiary. This creates a reinforcing dynamic: nearshored manufacturing facilities increase domestic demand for critical mineral inputs, which in turn raises the strategic value of developing Mexico's own mineral reserves rather than importing processed materials from Asia.

The economic logic is compelling. Mining a copper deposit in Sonora, processing it into cathode within Mexico, and supplying it to an EV assembly facility in Monterrey represents a fully integrated North American value chain. However, building that chain requires policy certainty at each stage.

The Policy Tools Under Discussion Inside the USMCA Framework

Trade analysts tracking the USMCA review and critical minerals in Mexico have identified several specific mechanisms being considered for potential inclusion in any updated framework:

- Border-adjusted price floors for critical minerals produced within the USMCA zone, designed to protect North American producers from below-cost imports that have historically destabilised investment cycles

- Regulatory harmonisation timelines that would align permitting standards across all three jurisdictions, reducing the compliance burden for companies operating in multiple countries

- Trilateral geological mapping coordination to systematically identify underdeveloped mineral deposits across the region using shared data and survey methodologies

- Strategic stockpiling provisions that would establish minimum reserve requirements for designated critical minerals, providing a buffer against supply shocks

- Plurilateral expansion clauses that could eventually allow allied nations outside North America to participate in the framework under defined conditions

Each of these mechanisms addresses a different failure mode in the current system. Price floors target market volatility. Regulatory harmonisation reduces transaction costs. Geological coordination unlocks undiscovered value. Stockpiling builds systemic resilience. None of them, however, can function effectively if Mexico's domestic regulatory environment remains structurally hostile to private investment. In addition, concerns around critical raw materials supply are being mirrored across other Western frameworks, reinforcing the urgency of North American action.

Mexico's Regulatory Reversal and Its Investment Consequences

The year 2022 marked a decisive turning point in Mexico's mining policy posture. Legislative changes introduced shorter concession periods, tightened environmental restrictions, imposed new open-pit mining limitations, and most significantly, nationalised lithium reserves under state control through the creation of LitioMx, a state-owned entity tasked with managing lithium development.

The investment implications are serious and compound over time. Mine development globally averages approximately 18 years from initial discovery to commercial production. This timeline reflects the sequential demands of exploration, resource estimation, feasibility studies, environmental assessment, permitting, construction, and commissioning. Mexico's post-2022 regulatory changes do not simply add cost to this process. They introduce compounding uncertainty at multiple points along a timeline where capital commitments must be made years before returns materialise.

Investment Risk Consideration: Compressed concession windows create a mismatch between the time horizon required to develop a mine and the duration of the legal rights protecting that investment. When a concession expires before a project reaches production, the capital deployed in earlier stages is at risk of stranding. This is not a theoretical concern. It is a fundamental underwriting problem that affects how mining companies model project economics and how lenders price risk.

The Camino Rojo Labour Panel: A Supply Chain Wake-Up Call

In March 2026, a USMCA labour dispute panel issued a ruling related to violations documented at a gold and zinc mining operation in Mexico. The case drew attention not only because of the specific infractions identified, but because it surfaced the role of narcotrafficker-related intimidation as a workforce stability risk within Mexico's mining sector.

This dimension of operational risk is frequently absent from supply chain analyses that focus primarily on geological and regulatory factors. Consequently, worker safety and community security conditions at mine sites directly affect production continuity, recruitment capacity, and social licence to operate. A critical minerals framework that does not incorporate enforceable labour and security standards would be building on unstable foundations.

China's Shadow Over the Negotiating Table

No analysis of the USMCA review and critical minerals in Mexico is complete without examining the geopolitical context that gives urgency to the entire discussion. China's position in the global critical minerals supply chain is not simply one of production dominance. It extends through processing and refining in ways that give Beijing leverage over finished material availability even for minerals physically extracted elsewhere.

The ongoing US-China trade war has further sharpened this dynamic, pushing Washington to accelerate alternative sourcing strategies across North America. China's growing footprint in Mexico's electric vehicle and battery manufacturing sector adds a specific layer of strategic concern for U.S. policymakers. Chinese-affiliated manufacturers establishing production facilities in Mexico introduce questions about whether USMCA's rules-of-origin provisions are capturing the true origin of value-added content, and whether materials processed through Chinese-controlled entities qualify for preferential treatment under the agreement.

Mexico's diplomatic position in this dynamic is genuinely complex. It seeks to attract North American capital to develop its mineral resources while managing existing economic relationships with Chinese investors and manufacturers. The USMCA review framework gives Mexico a structured multilateral forum in which to manage these competing pressures, providing diplomatic cover for policy adjustments that would otherwise be more politically exposed.

Finance-level bilateral dialogue between U.S. and Mexican officials, including discussions attributed to Treasury Secretary Scott Bessent and Mexican Finance Minister Edgar Amador, signals that the mineral supply chain conversation has moved beyond trade policy circles into macroeconomic and sovereign finance territory, reflecting the systemic importance both governments now attach to the outcome.

The next major ASX story will hit our subscribers first

Two Scenarios for the July 2026 Review Outcome

The USMCA review and critical minerals in Mexico could resolve along two fundamentally different paths, each with distinct consequences for investment, supply chain development, and geopolitical positioning.

Path A: Binding Critical Minerals Provisions Are Adopted

All three parties agree to embed enforceable critical minerals cooperation clauses within the USMCA framework. Regulatory harmonisation timelines are established. Price floor mechanisms are activated for designated minerals. Private capital begins re-entering Mexico's mining sector as policy uncertainty recedes. Within a 5-to-10 year horizon, North American supply chains begin demonstrably reducing their dependence on Chinese processing capacity.

Path B: Review Concludes Without Structural Minerals Integration

Trade continuity is preserved in a narrower sense. Tariff disputes are managed. However, critical minerals remain outside any binding USMCA discipline. Mexico's domestic regulatory environment continues to deter foreign investment in mining. China retains its processing advantage. North American supply chain vulnerability persists and deepens as clean energy demand for battery and grid materials accelerates.

The difference between these outcomes is not primarily geological. Mexico has the mineral resources either way. The difference is institutional. Whether the three USMCA nations can construct a durable policy architecture around those resources — one that also supports broader critical minerals energy security objectives — is the central question before July 2026.

What Investors and Industry Stakeholders Should Monitor Before July 2026

For those tracking this space, several leading indicators will signal which path the review is taking:

- Progress on resolving Section 232 steel and aluminium tariff inconsistencies within the USMCA framework

- Whether Canada and Mexico formalise a joint position on critical minerals ahead of the review deadline

- LitioMx operational developments and any signals of partial private investment accommodation within the lithium nationalisation framework

- Additional USMCA labour panel activity in the mining sector, which would either reinforce or undermine confidence in the enforcement mechanism

- Bilateral geological survey cooperation announcements, which would indicate technical-level integration is proceeding independent of the formal review outcome

Inaction carries its own strategic cost. Every year that North American critical mineral supply chains remain underdeveloped is a year in which Chinese processing capacity deepens its structural advantage. The USMCA review represents a bounded window for institutional action. Whether that window is used effectively will shape the competitive position of the North American industrial economy for the decade ahead.

This article is intended for informational purposes only and does not constitute financial or investment advice. Statements regarding policy outcomes, investment timelines, and supply chain projections involve inherent uncertainty and should not be relied upon as predictions of future events. Readers should conduct independent research and consult qualified advisors before making investment decisions.

Want to Stay Ahead of Critical Mineral Discoveries Reshaping North American Supply Chains?

As governments race to secure strategic mineral resources, Discovery Alert's proprietary Discovery IQ model instantly notifies subscribers of significant ASX mineral discoveries — transforming complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore how historic mineral discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the next major find.