July 27, 2026

The World's Most Vulnerable Energy Corridor Is Back at the Centre of Global Geopolitics

Every major oil supply crisis of the past half century has, in one way or another, circled back to a single 21-mile-wide passage between the Arabian Peninsula and Iran. The Strait of Hormuz reopening talks carry such outsized consequences that understanding them requires looking beyond the immediate military exchanges and into the structural dependencies that make this waterway irreplaceable. When that column trembles, the vibrations are felt from Asian manufacturing hubs to European heating bills to American petrol pumps.

When big ASX news breaks, our subscribers know first

Why Hormuz Remains Impossible to Replace

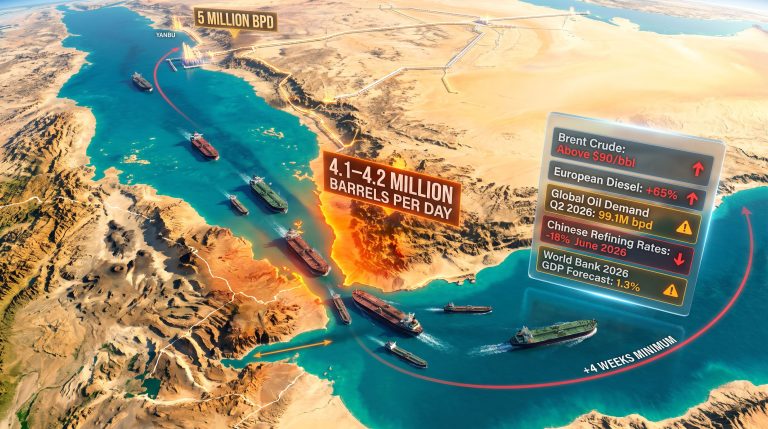

The strait handles approximately one-fifth of the world's combined oil and LNG supply on any given day. That single statistic understates the real concentration of risk, because the nations most exposed — China, Japan, South Korea, and India — are also among the world's largest and most energy-intensive economies. Their industrial output, trade balances, and domestic inflation rates are all directly sensitive to what happens inside those 21 miles of water.

Pipeline alternatives exist in theory. The UAE operates the Abu Dhabi Crude Oil Pipeline, which can bypass Hormuz for certain export volumes. Saudi Arabia's East-West Pipeline provides another partial workaround. However, neither system, nor both combined, can absorb anything close to the full volume that transits the strait on a normal operating day. The mathematical gap between bypass capacity and actual throughput is enormous.

The post-1970s energy security frameworks developed by International Energy Agency member nations were built around one foundational assumption: Hormuz stays open. Strategic petroleum reserves were sized and positioned accordingly. The current disruption is stress-testing those reserves and the diplomatic scaffolding built around them simultaneously.

The LNG supply outlook is further complicated by deepening dependency on the strait over the past two decades. Qatar, now one of the world's top three LNG exporters, and the UAE both route their liquefied natural gas shipments through Hormuz. As Asian economies locked in long-term LNG contracts during the energy transition period, they structurally increased their Hormuz exposure without always recognising it explicitly.

The Negotiating Architecture: More Complex Than a Maritime Dispute

The Strait of Hormuz reopening talks are not, at their core, a shipping negotiation. They are a surface expression of a much deeper set of geopolitical contests that have been running for decades. Any analysis that treats them as a standalone maritime problem will miss the underlying dynamics driving the impasse.

Three distinct but interconnected issues are blocking a durable resolution:

| Issue | U.S. Position | Iran's Position | Current Status |

|---|---|---|---|

| Freedom of Navigation | Non-negotiable precondition | Linked to broader sanctions relief | Unresolved |

| Nuclear Program | Separate but parallel track | Demands sanctions removal first | Unresolved |

| Frozen Iranian Assets | Conditional on compliance | Demands unconditional release | Unresolved |

U.S.-China trade war impacts add further complexity to this already fraught environment. U.S. Secretary of State Marco Rubio has publicly stated that Iran must formally declare an end to threats against commercial shipping and confirm that the strait is open before broader diplomatic progress can be made. This framing positions Hormuz access as a precondition rather than a negotiating chip.

Iranian officials, as of early June 2026, have acknowledged that discussions are ongoing but have signalled that no substantive breakthrough has been achieved. Tehran appears to be treating strait access as leverage within the broader negotiation rather than as an issue to be resolved independently.

China's involvement adds another layer of complexity. Foreign Minister Wang Yi, in direct talks with Iranian counterpart Abbas Araqchi, pushed for the strait to be reopened as quickly as possible and emphasised the need for safe navigation and a stable ceasefire. Beijing's intervention reflects raw economic self-interest — China's industrial demand for Persian Gulf crude is unmatched globally, and any sustained Hormuz disruption threatens its supply chain at a fundamental level.

"The Hormuz reopening talks are embedded within a wider geopolitical architecture involving nuclear diplomacy, frozen asset disputes, and freedom of navigation principles. Resolving any single element without the others risks producing an agreement that collapses under its own internal contradictions."

From Ceasefire to Crisis: The Escalation Timeline

The current disruption to Hormuz transit began in late February 2026, when armed conflict in the region triggered an immediate pullback in commercial shipping volumes. In the weeks that followed, some vessels attempted partial transits, often operating with coordination from U.S. naval forces positioned in the area.

The most recent escalation, in early June 2026, involved Iranian strikes targeting U.S. military infrastructure in Bahrain and Kuwait. American forces responded with strikes against Iranian assets near the strait itself, and U.S. military units intercepted Iranian drone attacks directed at commercial vessels. According to reporting from AP News, diplomatic efforts were already underway even as hostilities continued, reflecting the urgency felt by multiple parties. Oil markets responded with upward price movements, reflecting a reassessment of near-term supply risk.

Despite limited resumptions of transit activity, overall shipping throughput through Hormuz remains significantly below pre-conflict baselines. The operational reality for most commercial shipping operators is that the strait is functionally restricted, not closed outright — a distinction that matters for insurance and routing decisions but changes little about the supply impact on energy markets.

How Energy Markets Are Pricing the Disruption

The market response to each new military exchange has followed a consistent pattern: crude prices move higher as traders embed a larger risk premium into forward pricing. Furthermore, this is not simply a reaction to current supply volumes — it reflects probabilistic pricing of further escalation scenarios that could worsen throughput. The broader oil price rally observed in early 2025 has provided important context for understanding how quickly energy markets can respond to geopolitical shocks.

Persian Gulf producers most affected by the disruption include Saudi Arabia, Iraq, Kuwait, and the UAE, all of which rely on Hormuz as their primary export corridor. Notably, Iran itself exports crude through the strait, meaning Tehran's leverage over the chokepoint cuts both ways economically.

| Risk Category | Impact Level | Industry Response |

|---|---|---|

| War risk insurance premiums | Significantly elevated | Surcharges applied to Persian Gulf voyages |

| Vessel routing decisions | Major rerouting via Cape of Good Hope | Extended transit times and higher freight costs |

| Commercial operator confidence | Low | Many operators awaiting diplomatic clarity |

| LNG tanker availability | Tightening | Longer voyage routes reduce effective fleet capacity |

LNG buyers in East Asia face particularly acute pressure. The absence of comparable alternative supply routes at scale means buyers have been forced to source replacement cargoes from Atlantic Basin producers, including U.S. Gulf Coast export terminals and Australian LNG facilities. This Atlantic-to-Asia rerouting drives up both spot LNG prices and freight costs, compressing margins across the supply chain.

An underappreciated dimension of the disruption involves tanker fleet capacity. When vessels are rerouted around the Cape of Good Hope rather than through Hormuz, voyage durations extend by approximately 10 to 15 days each way. This effectively removes a meaningful percentage of the active tanker fleet from productive circulation at any given time, tightening vessel availability and pushing freight rates higher even for routes that do not pass through the strait.

The Three-Power Dynamic: Washington, Beijing, and Tehran

The United States

Washington is operating a dual-track strategy: maintaining active naval operations in the region while simultaneously using Hormuz access as a precondition lever in diplomatic negotiations. The interception of Iranian drones targeting commercial vessels demonstrates both the military commitment and the ongoing threat environment that makes commercial resumption so difficult. This dual posture creates deterrence value but also generates escalation risk each time a military incident occurs.

China

Beijing's economic vulnerability is the most direct forcing function in the diplomatic process. China imports more Persian Gulf crude than any other nation, and the current disruption is not a distant geopolitical abstraction for Chinese planners — it is an active threat to industrial output and energy security. China's public push for immediate reopening, delivered through the Wang Yi channel, also serves a secondary diplomatic purpose: maintaining Beijing's relevance as a constructive mediating actor in Middle Eastern affairs.

Iran

Tehran holds significant asymmetric leverage through geographic control of the northern strait coastline combined with naval and drone capabilities that have proven capable of threatening commercial shipping. However, prolonged closure carries real costs for Iran as well. Export revenues from Iranian crude are diminished by any restriction on strait access, and extended economic isolation risks further destabilising an already strained domestic economy. Iranian negotiators appear to be calibrating their use of Hormuz access as a bargaining instrument rather than pursuing permanent closure, but miscalculation remains a constant risk.

The next major ASX story will hit our subscribers first

What a Durable Reopening Would Actually Require

Analysts tracking the Strait of Hormuz reopening talks have identified five minimum conditions that would need to be satisfied for any agreement to hold:

- A formal Iranian declaration that commercial shipping will not be targeted, meeting the precondition set by the U.S. Secretary of State.

- A verified ceasefire extension covering both direct military exchanges and proxy drone operations conducted by non-state actors aligned with Tehran.

- An agreed monitoring mechanism involving neutral maritime observers or existing international frameworks capable of independently verifying compliance.

- Parallel progress on at least one core issue — whether the nuclear file, frozen asset release, or navigation rights — to demonstrate that the broader negotiation is moving forward.

- Insurance and liability clarity sufficient to restore commercial operator confidence, allowing shipping companies to resume normal transit scheduling without extraordinary risk surcharges.

The fifth condition is frequently underestimated in diplomatic analyses but is critically important in practice. Even if a ceasefire is declared and both governments commit to its terms, commercial shipping operators will not return to normal transit patterns until war risk insurance premiums fall to commercially viable levels. That requires not just a political announcement but a sustained period of incident-free transit that convinces underwriters the threat environment has genuinely improved.

Historical precedent in the region is not encouraging on this point. Previous ceasefire arrangements have been undermined by proxy forces operating outside direct government control, by domestic political pressures that incentivise hardline positioning, and by the technical complexity of verifying compliance across a contested maritime environment.

Three Scenarios for Hormuz: Outcomes and Probabilities

Scenario 1: Negotiated Phased Reopening

A structured, monitored easing of restrictions allows commercial traffic to resume incrementally under third-party observation. Oil prices begin to retrace conflict-era premiums, LNG spot markets in Asia ease, and shipping insurers gradually reduce war risk surcharges. The key driver for this outcome is sustained diplomatic pressure from China combined with economic incentives on both the U.S. and Iranian sides to avoid prolonged disruption.

Scenario 2: Prolonged Diplomatic Stalemate

Talks continue without a breakthrough. Limited, U.S.-coordinated transits remain the operational norm for commercial shipping. Energy markets sustain an elevated risk premium for an extended period, and global supply chains adapt through rerouting and alternative sourcing at structurally higher costs. This scenario is most likely if the three core unresolved issues — nuclear program, asset release, and navigation rights — remain deadlocked.

Scenario 3: Renewed Escalation and Extended Closure

A significant military incident triggers a breakdown in ceasefire arrangements, forcing a full suspension of commercial transit. IEA member nations would likely initiate coordinated strategic petroleum reserve releases to buffer markets, but the scale of a complete Hormuz closure would test those reserves significantly. Oil prices could spike sharply, and the cascading economic effects on energy-importing nations would substantially elevate global recession risk. This tail-risk scenario is driven by miscalculation, proxy actor escalation, or domestic political disruption in either Washington or Tehran.

What Investors and Energy Participants Should Watch

The geopolitical landscape in mining and energy markets is shifting rapidly, making the following indicators particularly valuable for tracking negotiation trajectory in real time:

- Diplomatic channel activity between U.S. and Iranian negotiators, specifically any formal announcement related to freedom of navigation commitments

- Chinese diplomatic engagement with Tehran, which functions as a leading indicator of whether a phased reopening framework is gaining traction

- Crude oil price movements, particularly the spread between near-term and forward contracts, which reflects market confidence in supply continuity

- War risk insurance premium trends, since a reduction in surcharges would signal that commercial underwriters believe transit safety is improving materially

- Ceasefire compliance reporting, with any new drone interception or military exchange event indicating that the fragile truce remains under active stress

Frequently Asked Questions: Strait of Hormuz Reopening Talks

What percentage of global oil flows through the Strait of Hormuz?

Approximately 20% of global oil supply and a substantial share of worldwide LNG exports transit the Strait of Hormuz, making it the single most consequential maritime energy chokepoint in the world.

Why is China pushing for the Strait of Hormuz to reopen?

China is the world's largest importer of Persian Gulf crude oil. Any sustained disruption to Hormuz transit directly threatens Chinese energy security and economic stability, giving Beijing strong incentive to advocate for rapid reopening through diplomatic channels.

What is the U.S. precondition for advancing Hormuz reopening negotiations?

Secretary of State Marco Rubio stated that Iran must publicly declare it will cease threatening commercial shipping and confirm the strait is open before the U.S. will advance broader diplomatic negotiations on related issues.

Has shipping through the Strait of Hormuz completely stopped?

No. Some vessels have resumed limited transits, in some cases with U.S. military coordination. However, overall shipping volumes through the strait remain significantly below pre-conflict levels that existed prior to the outbreak of hostilities in late February 2026.

What are the main obstacles to a Hormuz reopening deal?

Three core issues remain unresolved: Iran's nuclear program, the release of frozen Iranian financial assets, and the establishment of freedom of navigation guarantees. Meaningful progress on all three is considered necessary for a durable and enforceable agreement.

How are oil prices reacting to the Hormuz situation?

Energy markets have responded with upward price movements following each new military exchange, as traders price in supply disruption risk and uncertainty surrounding future Persian Gulf export volumes. The uncertainty premium embedded in current pricing reflects not only present disruption but the probabilistic risk of further escalation.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking statements, scenario projections, and market assessments involve inherent uncertainty and should not be relied upon as predictions of future events. Readers are encouraged to conduct independent research and consult qualified professionals before making any investment or commercial decisions related to the topics discussed.

Want to Stay Ahead of Commodity Market Shifts Driven by Geopolitical Events Like Hormuz?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex market data into actionable insights for both short-term traders and long-term investors — start your 14-day free trial at Discovery Alert today, or explore how historic mineral discoveries have generated substantial returns even amid volatile global commodity markets.