July 14, 2026

India's Aluminium Paradox: The Nation Sitting on Bauxite Riches While Importing Finished Metal

Few structural contradictions in global commodities are as striking as India's position in the aluminium supply chain. The country holds approximately 2.9 billion tonnes of bauxite reserves, ranking it among the world's most resource-endowed nations, yet it consistently imports significant volumes of fabricated aluminium products to meet domestic industrial demand. This gap between raw material wealth and finished product capacity represents one of the most compelling investment narratives in Indian metals today, and it sits at the heart of why the Vedanta aluminium buy rating by Nuvama has attracted meaningful institutional attention.

The initiation of coverage by Nuvama Institutional Equities on Vedanta Aluminium Metal Ltd (VAML) is more than a single analyst call. It reflects a broader reassessment of how India's primary aluminium sector is positioned as the country's manufacturing economy continues to scale. Understanding why requires examining the company's operational architecture, its cost reduction roadmap, and the global market forces that either support or threaten the thesis.

When big ASX news breaks, our subscribers know first

From Conglomerate Exposure to Pure-Play Aluminium

Why the Demerger Changes the Investment Calculus

Vedanta Limited's decision to demerge its aluminium operations into a standalone listed entity fundamentally alters how institutional capital can engage with the business. Within a diversified conglomerate structure, aluminium exposure is diluted by zinc, oil, iron ore, and other assets, making clean valuation difficult and limiting the interest of sector-specialist funds that require pure-play mandates.

As VAML, the aluminium business now carries its own balance sheet, its own earnings trajectory, and its own dividend policy. This structural clarity tends to attract a different class of investor, particularly those running commodity-focused or India-focused mandates who previously could not isolate aluminium exposure without taking on unrelated conglomerate risk.

Pure-play industrial producers in capital-intensive sectors historically trade at premium EV/EBITDA multiples relative to diversified parents, because the market can price growth and risk with greater precision. Nuvama's decision to anchor its valuation at 6.5x estimated FY28 EV/EBITDA reflects this dynamic, applying a multiple that accounts for VAML's growth visibility while acknowledging the execution risks embedded in a multi-year vertical integration programme. This kind of aluminium sector restructuring is increasingly common globally as investors demand greater transparency.

VAML's Position Within India's Domestic Aluminium Ecosystem

India's primary aluminium industry is dominated by a small number of integrated producers. VAML, through its Jharsuguda smelter complex in Odisha and its stake in Bharat Aluminium Company (BALCO), operates as the largest primary aluminium producer in India by capacity. The company's competitive positioning is reinforced by a degree of vertical integration that few domestic peers can match, spanning bauxite mining, alumina refining, and smelting through to value-added products.

What makes VAML's trajectory distinctive is not its current scale but its rate of capacity expansion. Nuvama identifies it as the fastest-expanding primary aluminium company in India, a characterisation supported by specific capacity milestones that no domestic competitor appears positioned to replicate on the same timeline. Furthermore, when assessed alongside the top aluminium producers globally, VAML's integration ambitions are notably aggressive.

Breaking Down the Nuvama Buy Rating: Valuation and EBITDA Growth

The Target Price Architecture

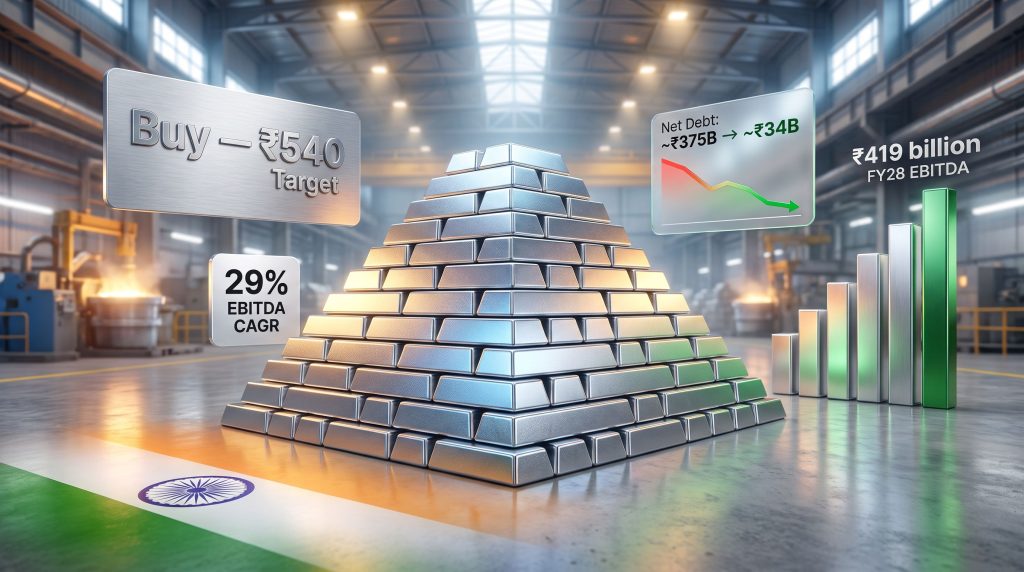

Nuvama Institutional Equities has assigned VAML a Buy rating with a target price of ₹540 per share, representing approximately 21 to 22% upside from the prevailing market price of around ₹444. The valuation methodology uses a 6.5x EV/EBITDA multiple applied to FY28 earnings estimates, a framework commonly employed for capital-intensive industrials where medium-term earnings visibility is supported by contracted or captive input structures.

EV/EBITDA is the preferred valuation lens in this context because it strips out the distortions of high depreciation charges typical in smelting operations and adjusts for debt levels, making cross-company comparisons more meaningful. For a company undergoing simultaneous capacity expansion and aggressive deleveraging, applying the multiple to a forward year that captures the post-integration cost base is analytically sound. Nuvama's full research note provides a detailed breakdown of the assumptions underpinning this framework.

The 29% EBITDA CAGR: What the Numbers Actually Mean

The headline figure in Nuvama's coverage initiation is a projected 29% compound annual growth rate in EBITDA over FY26 to FY28, culminating in an estimated EBITDA of approximately ₹419 billion (USD 4.37 billion) by FY28. To appreciate why this is an unusually strong projection, consider that most Indian metals companies are projecting single-digit EBITDA growth over the same period.

| Metric | FY26 Baseline | FY28 Estimate | Change |

|---|---|---|---|

| EBITDA | Base year | +29% CAGR | |

| Production Volume Growth | Base year | +8% CAGR (FY26-FY28) | Fastest among Indian peers |

| Hot Metal Cost (USD/tonne) | ~USD 1,914 (FY22-FY26 avg.) | Below USD 1,600 (from FY28) | ~16% reduction |

| Net Debt | ~91% reduction | ||

| Dividend Per Share (DPS) | Not established | ₹15 (FY27 and FY28) | New dividend policy |

The 29% CAGR is not driven by a single factor but by the simultaneous convergence of volume growth, cost compression, and supportive pricing. Each component reinforces the others, meaning the combined effect on EBITDA per tonne can be considerably more powerful than any individual lever in isolation.

A projected decline in net debt of approximately 91% over just two fiscal years would represent one of the most aggressive balance sheet transformations in the Indian metals sector. The credibility of this forecast depends almost entirely on the pace at which captive input integration delivers real cash flow improvement rather than accounting adjustments.

The Three-Pillar Cost Reduction Strategy

How Vertical Integration Compresses the Cost Curve

Aluminium production is unique among base metals in that input costs are layered across multiple distinct raw material categories: bauxite, alumina, and energy. Each layer carries its own price volatility profile, and exposure to spot markets at multiple stages amplifies margin sensitivity. VAML's cost reduction thesis rests on progressively reducing that exposure through captive sourcing across all three layers simultaneously.

1. Captive Alumina Production Expansion

Alumina, produced by refining bauxite through the Bayer process, typically constitutes the largest single input cost in primary aluminium production, often representing 30 to 35% of the cost of hot metal. When alumina is purchased on spot markets, producers are exposed to price cycles that can move independently of the aluminium price, creating margin compression even when smelting economics are otherwise favourable.

VAML's Lanjigarh alumina refinery in Odisha has significant expansion potential, and increasing captive alumina output directly reduces the proportion of alumina procured externally. Each percentage point shift from purchased to captive alumina represents a structurally lower and more stable cost baseline, not merely a cyclical improvement.

2. Sijimali Bauxite Mine Operationalisation

The Sijimali bauxite deposit in Odisha is central to the long-term raw material security of the Lanjigarh refinery. Bauxite quality matters enormously in aluminium production: the alumina-to-silica ratio and the reactive silica content of ore directly determine refinery yields and the quantity of caustic soda consumed per tonne of alumina produced. Higher-quality bauxite translates to lower reagent costs and better refinery throughput efficiency.

Operationalising Sijimali would significantly reduce VAML's dependence on third-party bauxite suppliers, whose pricing power increases during periods of tight supply. In the context of global bauxite production dynamics, securing captive ore supply is increasingly a prerequisite for competitive cost structures in primary aluminium. The timeline for mine commencement carries regulatory dimensions, however, as forest clearances and environmental approvals in India's mining sector have historically extended beyond initial projections.

3. Captive Coal Access and Energy Cost Management

Aluminium smelting is among the most electricity-intensive industrial processes on earth, requiring roughly 14 to 16 megawatt-hours of electricity per tonne of aluminium produced. In India, where grid power for industrial consumers can be expensive and unreliable, captive coal-based power generation is a critical competitive differentiator.

VAML operates captive thermal power plants at Jharsuguda, and increasing the proportion of captive coal that feeds these plants reduces dependence on merchant power purchases and open-market coal procurement, both of which carry significant cost variability. The energy cost trajectory for Indian smelters versus global peers in regions with access to cheap hydropower remains a structural gap, but captive coal integration narrows the disadvantage materially.

When captive sourcing improves across bauxite, alumina, and coal simultaneously, the cost compression effect is non-linear. As integration deepens, each additional tonne of captive input eliminates not just the raw material premium but also the logistics, procurement, and working capital costs associated with external supply chains.

Global Aluminium Market Dynamics: The Pricing Backdrop

Supply Deficit, Price Support, and the FY29 Transition

Nuvama's positive outlook is partly anchored in a view that the global aluminium market will remain in supply deficit through at least the first half of FY28. This assessment is consistent with broader industry analysis pointing to constrained smelting capacity additions in energy-challenged regions such as Europe, where high electricity costs have forced curtailments, and geopolitical disruptions affecting Russian aluminium supply flows.

The deficit dynamic matters because it creates a price floor that supports VAML's EBITDA margin even before the full benefit of cost reduction is realised. Consequently, if aluminium prices remain above USD 2,400 to 2,500 per tonne on the LME during the critical FY26 to FY28 integration window, the margin expansion from cost compression is additive to an already supportive price environment.

The anticipated shift toward market surplus in FY29, as new smelting capacity comes online in Indonesia and the Gulf region, introduces a time-sensitive element to the investment thesis. Investors assessing the Vedanta aluminium buy rating by Nuvama should be aware that the strongest part of the earnings trajectory is projected to coincide with the deficit period, meaning execution delays could push key milestones into a less favourable pricing environment.

What Recent Price Softening Reveals About Market Sensitivity

A temporary easing in aluminium prices following expectations of improved shipping conditions through the Strait of Hormuz illustrates how quickly sentiment can shift in this market. Aluminium pricing is influenced not only by smelter supply and end-use demand but also by freight economics, energy market developments, and currency dynamics in major producing countries.

This sensitivity reinforces the importance of VAML's cost reduction programme. A company producing at USD 1,914 per tonne has a meaningfully different risk profile during a price correction than one producing at sub-USD 1,600 per tonne. The lower the cost base, the wider the margin buffer against adverse price movements. Indeed, India metals demand trends suggest that downstream consumption will continue rising regardless of short-term price volatility, providing further support for capacity investment.

Capacity Expansion and Production Volume Trajectory

BALCO's 435,000-Tonne Expansion as the Near-Term Catalyst

The commissioning of BALCO's 435,000 MTPA aluminium expansion is the most proximate volume growth driver within Nuvama's forecast period. This addition brings VAML's group production capacity to an estimated 2.8 MTPA by the end of FY27, with a further increase to approximately 3.0 MTPA by FY28.

| Producer Category | Volume Growth (FY26-FY28) | Primary Growth Driver |

|---|---|---|

| Vedanta Aluminium Metal (VAML) | ~8% CAGR | BALCO expansion + Sijimali mine |

| Indian domestic peers (average) | Limited, single-digit | Input supply constraints |

| Global majors (reference) | Region-dependent | Varies by energy and regulatory context |

An 8% volume CAGR positions VAML among the fastest-growing primary aluminium producers in Asia over this period. Volume growth matters independently of pricing because it absorbs fixed costs across a larger production base, improving cost per tonne even before operational efficiency gains are counted separately.

The next major ASX story will hit our subscribers first

Balance Sheet Transformation and Shareholder Returns

Deleveraging as a Value Unlock

The projected reduction in net debt from approximately ₹375 billion (USD 3.91 billion) in FY26 to approximately ₹34 billion (USD 354.72 million) by FY28 is the most striking single element of Nuvama's financial model. A 91% reduction in net debt over two fiscal years implies an extraordinary level of free cash flow generation, which in turn depends on the simultaneous delivery of volume growth, cost reduction, and supportive aluminium prices.

Reduced debt servicing costs create a compounding benefit: as interest expenses fall, more operating cash flow converts to free cash flow, which accelerates further debt reduction or funds additional capital returns. For a newly independent entity seeking to establish credibility with institutional investors, a credible deleveraging trajectory is often more important than near-term earnings per share.

What the ₹15 Dividend Per Share Signals

An estimated ₹15 dividend per share in both FY27 and FY28 is significant not just for its yield implications but for what it communicates about management confidence. Newly demerged companies frequently defer dividend initiation until the balance sheet is stabilised and earnings are proven. Committing to a dividend policy early in VAML's independent existence signals that management believes operating cash flows will be sufficient to simultaneously fund capital expenditure, service debt, and return capital to shareholders.

At the prevailing price of around ₹444, a ₹15 DPS translates to a dividend yield of approximately 3.4%, which is competitive within the Indian metals sector and provides an income component alongside the capital appreciation thesis. Furthermore, the low-carbon metals transition reshaping global industry could provide additional long-term tailwinds for producers investing in integrated, lower-emission production models.

Risk Factors Investors Should Monitor

No investment thesis of this ambition is without material risks. The key variables that could cause Nuvama's projections to diverge from actual outcomes include:

- Aluminium price correction: If LME prices decline materially before VAML's cost base reaches sub-USD 1,600 per tonne, the EBITDA CAGR forecast faces downward pressure.

- Sijimali mine delays: Forest clearance and environmental approvals in Indian mining have a well-documented history of timeline slippage. Delays here directly impair the bauxite cost reduction pillar.

- Captive coal policy changes: Regulatory adjustments affecting coal block allocations or captive power plant operations could disrupt the energy cost trajectory.

- Execution risk on BALCO expansion: Large-scale smelter commissioning is technically complex; any delay in reaching nameplate capacity affects the volume growth CAGR.

- Emerging market capital flows: Broader risk-off episodes in global markets disproportionately affect Indian equities, creating mark-to-market volatility independent of fundamental performance.

Investor Framework: The most useful leading indicators to track are quarterly hot metal cost disclosures relative to the sub-USD 1,600 target, net debt progression against the ₹34 billion FY28 objective, and the pace of captive alumina output as a proportion of total refinery input requirements.

Frequently Asked Questions

What is Nuvama's Target Price for Vedanta Aluminium Metal?

Nuvama Institutional Equities has set a target price of ₹540 per share, implying approximately 21 to 22% upside from the prevailing market price of around ₹444. According to coverage published by Financial Express, this makes VAML one of the more compelling large-cap initiations in the Indian metals space this year.

What Valuation Methodology Underpins the Nuvama Rating?

The target price applies a 6.5x EV/EBITDA multiple to estimated FY28 earnings, a methodology suited to capital-intensive industrials with visible medium-term growth catalysts.

What is the Projected EBITDA Growth Rate for VAML?

Nuvama forecasts EBITDA to compound at approximately 29% per annum over FY26 to FY28, reaching around ₹419 billion (USD 4.37 billion) by FY28.

Why Does the Sijimali Bauxite Mine Matter So Much to the Cost Thesis?

Captive bauxite eliminates dependence on third-party suppliers whose pricing power increases during tight supply periods. It also allows the Lanjigarh refinery to optimise ore blending for maximum alumina yield, reducing per-tonne refining costs.

What Are the Primary Risks to This Investment Thesis?

The main risks include aluminium price corrections before cost integration is complete, delays in Sijimali mine operationalisation, regulatory changes affecting captive coal access, and BALCO expansion execution risk.

What is VAML's Production Capacity Target by FY28?

The group is targeting approximately 3.0 MTPA by FY28, driven principally by the commissioning of BALCO's 435,000-tonne expansion.

Assessing the Strength of the Nuvama Thesis

What the Bull Case Requires

For Nuvama's projections to materialise, the following conditions must hold concurrently:

- BALCO's 435,000-tonne expansion commissions on schedule and ramps to nameplate capacity within the projected window.

- The Sijimali bauxite mine receives necessary regulatory approvals and begins contributing meaningful ore volumes within the FY27 to FY28 timeframe.

- Global aluminium market supply-demand balance remains in deficit through at least H1 FY28, supporting LME prices above levels that stress VAML's margin.

- Captive alumina output continues growing as a proportion of total input, reducing the exposure to spot alumina price swings.

- Captive coal availability improves without adverse regulatory intervention.

The Broader Significance for India's Aluminium Sector

The Vedanta aluminium buy rating by Nuvama carries implications beyond a single stock call. It reflects a thesis that India's domestic aluminium value chain is at an inflection point, where the combination of large-scale captive integration, rising downstream demand from infrastructure, electric vehicles, and packaging, and a supportive global pricing cycle could allow Indian producers to close the structural gap between the country's bauxite endowment and its finished aluminium output.

Whether VAML delivers on the 29% EBITDA CAGR will ultimately be determined in the refinery, the mine, and the smelter, not in the analyst model. However, analyst consensus estimates tracked by major financial data providers suggest that Nuvama's thesis is gaining traction among institutional researchers. The framework Nuvama has constructed provides investors with a clear set of operational milestones against which progress can be measured quarter by quarter.

This article is intended for informational and educational purposes only and does not constitute financial advice or an investment recommendation. All financial projections referenced are analyst estimates and are inherently subject to uncertainty. Readers should conduct independent due diligence and consult a qualified financial adviser before making any investment decisions. Past performance and analyst forecasts are not reliable indicators of future results.

Want to Track the Next Major ASX Mineral Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex geological and market data into clear, actionable insights for both short-term traders and long-term investors. Explore Discovery Alert's dedicated discoveries page to understand how historic mineral discoveries have generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the market.