June 24, 2026

The Deep Underground Bet Reshaping African Copper Supply

Few metals carry the weight of the global energy transition the way copper does. Every electric vehicle rolling off a production line, every offshore wind turbine spinning above the North Sea, every AI data centre humming with server racks — each demands copper in quantities that existing mines are increasingly struggling to supply. The structural gap between where copper production currently sits and where demand is heading by the end of this decade has made the metal a focal point for industrial strategists, mining investors, and sovereign policymakers alike. It is against this backdrop that the Vedanta Zambia copper expansion plan has moved from a regional mining story to one of genuine global significance.

The numbers behind this supply anxiety are striking. Global copper demand is forecast to increase substantially through the early 2030s, driven by a convergence of electrification megatrends that have no viable substitution pathway at industrial scale. Understanding the copper supply crunch helps contextualise why high-grade assets are attracting such intense investor attention right now. Aluminium can replace copper in limited applications, but its inferior conductivity and higher weight make it unsuitable for most precision electrical uses. This irreplaceability is precisely what makes high-grade copper assets in politically stabilising jurisdictions so commercially attractive.

When big ASX news breaks, our subscribers know first

Konkola Copper Mines: A World-Class Asset With a Complicated History

Situated within the Central African Copperbelt, one of the most mineralogically endowed regions on Earth, Konkola Copper Mines occupies a genuinely rare position in global copper geology. Its ore grades exceed 2.4% copper, a figure that warrants serious attention from investors who understand what ore grade means for mine economics.

To appreciate why this matters, consider the broader context. The global average copper ore grade has been declining for decades as the world's easiest deposits are depleted. Most large-scale open-pit operations today process ore grading between 0.4% and 0.8% copper, meaning that for every tonne of rock hauled to surface, only four to eight kilograms of copper is recovered. KCM's ore grade is roughly three to five times higher than these industry benchmarks, which fundamentally changes the cost profile and margin resilience of the operation, particularly when copper prices soften.

Beyond copper, KCM holds meaningful cobalt co-production potential. Cobalt, as a critical input in lithium-ion battery cathodes, carries its own strategic importance in the battery supply chain. An operation capable of producing approximately 6,000 tonnes of cobalt annually at full capacity would rank among the leaders in global cobalt production — a dimension of KCM's asset quality that receives less attention than it deserves.

The mine's recent history is inseparable from Zambian politics. In 2019, the Zambian government under President Edgar Lungu placed KCM into provisional liquidation, citing alleged breaches of mining obligations. The move triggered years of legal disputes and operational deterioration. The political landscape shifted materially when President Hakainde Hichilema took office in 2021 and pursued a more investor-friendly approach to the mining sector. By 2024, Vedanta had regained operational control of KCM, having first settled approximately $246 million in creditor obligations — a payment that served as both a financial commitment and a credibility signal to prospective investors.

What the Vedanta Zambia Copper Expansion Plan Actually Involves

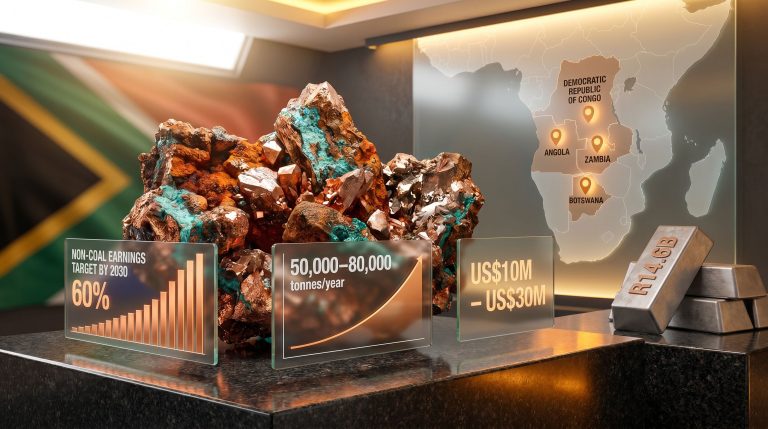

The scale of ambition embedded in the Vedanta Zambia copper expansion plan is best understood through the production trajectory it targets.

| Metric | Current Baseline (2025) | Target (2031) |

|---|---|---|

| Annual Copper Output | ~80,000 tonnes | 270,000–300,000 tonnes |

| Annual Cobalt Output | Sub-commercial | ~6,000 tonnes |

| Ore Grade | >2.4% copper | Maintained through deep mining |

| Share of Zambia's National Target | ~9% | ~10% of 3 million tonne goal |

This near-fourfold increase in copper output over six years is not a modest operational improvement — it is a wholesale transformation of the asset. Achieving it requires simultaneous execution across three distinct technical and commercial domains:

-

Underground mine development at Konkola Deep, including shaft sinking, ventilation systems, underground haulage infrastructure, and expanded ore access headings.

-

Surface processing upgrades, including smelter refurbishment to restore structural integrity and increase throughput capacity to handle the substantially larger ore volumes that Konkola Deep will eventually deliver.

-

Refining infrastructure, ensuring that the increased copper concentrate produced can be processed through to refined cathode copper efficiently, preserving the value-add that distinguishes a fully integrated copper operation from a simple concentrate exporter.

The Konkola Deep Project: Technical Realities of Deep Underground Mining

Deep underground copper mining is among the most capital-intensive forms of resource extraction. The Konkola Deep project requires reaching ore bodies at depths that demand engineered shaft systems capable of operating reliably for decades. Ventilation in deep mines is not simply a comfort consideration — at the temperatures and depths involved in operations like Konkola Deep, it is a fundamental production constraint. Without adequate airflow and cooling, worker safety cannot be maintained and productivity collapses.

Underground haulage systems must be designed to move large ore volumes continuously from working faces to surface, typically via a combination of conveyors, underground trucks, and shaft hoisting. The capital required to build this infrastructure is substantial and largely irreversible once committed — which is precisely why the financing structure Vedanta has assembled around this project is so significant.

Technical Note: Deep underground copper mines typically operate at sustained capital intensity levels far above open-pit equivalents. The ore grade advantage at KCM is critical here — higher grades mean more copper recovered per tonne of rock moved, improving the operating economics that must justify the upfront infrastructure investment.

How Vedanta Is Financing a World-Class Mining Build-Out

Vedanta has not approached the KCM expansion with a single funding mechanism. Instead, the capital structure combines three distinct pillars, each serving a different financial and strategic function.

Pillar 1: Project-Level Debt

Rand Merchant Bank has been mandated to raise up to $1 billion in project-level debt to fund operational upgrades and mine development. Project finance structures in sub-Saharan African mining typically require lenders to assess ore grade certainty, offtake arrangements, and sovereign risk mitigation. KCM's ore grade quality strengthens the bankability case considerably.

Pillar 2: The CopperTech Metals NYSE IPO

Vedanta has created a US-domiciled entity, CopperTech Metals Inc., to hold its KCM interest. Furthermore, the company is pursuing a listing on the New York Stock Exchange, offering approximately 23.5 million shares at $16–$18 per share, targeting a raise of up to $423.5 million, with potential upside to $429 million if underwriter over-allotment options are exercised. The implied valuation of CopperTech Metals reaches $3.57 billion at the top of the price range. Vedanta intends to divest an 11.9% stake, generating approximately $372 million from the transaction. Notably, Vedanta spun off Konkola Copper Mines into CopperTech Metals Inc. as part of this broader capital markets strategy.

Pillar 3: Committed Equity Program

The total committed investment program allocates approximately $1.1 billion to Konkola Deep over five years, within a broader $2.7 billion capital program. ZCCM Investment Holdings Chairman Phesto Musonda has indicated that the IPO proceeds could accelerate the Konkola Deep development timeline by up to three years compared to the pace achievable through internal funding alone.

| Investment Component | Estimated Allocation |

|---|---|

| Konkola Deep underground development | Core of $1.1B five-year commitment |

| Smelter refurbishment and processing upgrades | Within broader capital program |

| Debt facility (Rand Merchant Bank) | Up to $1B |

| CopperTech Metals IPO proceeds | Up to $423.5M–$429M |

| Total program (broad estimate) | ~$2.7B |

Why New York Over London or Johannesburg?

The choice of a NYSE listing over the London Stock Exchange or Johannesburg Stock Exchange reflects deliberate strategic calculation. US institutional investors have demonstrated stronger appetite for critical minerals assets, and valuation multiples awarded to copper producers in New York have historically exceeded those available in London's mining-heavy market.

There is also a narrative dimension. CopperTech's investor materials position KCM not merely as an African mining turnaround but as a potential contributor to Western copper supply security. Major economies' industrial strategies have created a receptive environment for this framing among US institutional allocators who understand the strategic minerals landscape. A NYSE listing also enhances CopperTech's profile with procurement frameworks and investment screens that prioritise assets in jurisdictions with improving governance trajectories.

Zambia's 3 Million Tonne Ambition: The National Stakes

Context: Zambia produced approximately 890,000 tonnes of copper in 2025, making it Africa's second-largest copper producer behind the Democratic Republic of Congo. The government's target of 3 million tonnes annually by 2031 represents a more than threefold increase in six years — one of the most ambitious national mining production targets anywhere in the world.

The Zambia copper growth forecast underpins much of the commercial rationale behind KCM's expansion. Operations run by First Quantum Minerals and Barrick Mining accounted for roughly 60% of Zambia's 2025 copper output. KCM, at full expansion, is projected to contribute approximately 10% of the national 3 million tonne target, making it a significant but not singular component of the overall ambition. Closing the remaining gap will require additional capital deployment across multiple other Zambian operations.

A successful CopperTech NYSE listing carries signalling value beyond Vedanta's own balance sheet. If an African copper asset with KCM's operational history can access US capital markets at a valuation above $3.5 billion, it demonstrates a viable pathway for other Zambian and African mining projects seeking international equity capital. That demonstration effect could influence investment decisions well beyond the KCM perimeter.

Regulatory and Political Risk: What History Teaches

The 2019 nationalisation of KCM under the Lungu administration remains the central cautionary data point for investors evaluating Zambia's sovereign risk profile. The circumstances that led to state intervention — including disputes over alleged environmental breaches, unpaid obligations, and disagreements over mine development commitments — illustrate how quickly the relationship between a mining operator and a host government can deteriorate.

The Hichilema administration has pursued a materially different approach, prioritising private investment attraction and regulatory stability. However, structural vulnerabilities persist. Power supply constraints remain a significant operational risk for deep underground mining, which demands continuous and reliable electricity for pumping, ventilation, hoisting, and processing. Zambia's power grid faces intermittency challenges tied to hydroelectric generation and drought exposure. Royalty structures and fiscal terms are also subjects of ongoing industry dialogue.

KCM Versus Peer African Copper Operations: A Competitive Lens

| Operation | Country | Operator | Annual Output (Current) | Expansion Target | Key Differentiator |

|---|---|---|---|---|---|

| Konkola Copper Mines | Zambia | Vedanta/CopperTech | ~80,000t | 270,000–300,000t by 2031 | >2.4% ore grade; cobalt by-product |

| Kansanshi Mine | Zambia | First Quantum Minerals | ~150,000t+ | Expansion underway | Largest single copper mine in Africa |

| Lumwana Mine | Zambia | Barrick Mining | ~100,000t+ | Ongoing | Large-scale open pit |

| Tenke Fungurume | DRC | CMOC | ~200,000t+ | Ongoing | World-class cobalt co-production |

| Kamoa-Kakula | DRC | Ivanhoe Mines/Zijin | ~450,000t+ | Targeting 600,000t+ | Highest-grade large-scale copper mine globally |

KCM's ore grade advantage positions it favourably against lower-grade bulk tonnage operations, where margin compression during copper price downturns can be severe. The copper price drivers that support elevated valuations for high-grade assets further reinforce KCM's competitive positioning. The cobalt co-production dimension additionally differentiates the asset from pure-play copper peers, providing a secondary revenue stream with its own strategic demand drivers.

The DRC comparison is instructive. Kamoa-Kakula represents the current global benchmark for high-grade large-scale copper mining, but it operates within a jurisdiction carrying its own sovereign risk profile. KCM's Zambia location, with an improving but not yet fully tested governance framework, occupies a different risk-reward position on the spectrum available to global copper investors.

The next major ASX story will hit our subscribers first

Key Milestones and Risk Factors for Investors to Monitor

Near-Term Catalysts (2025–2026)

- Completion of the CopperTech Metals NYSE IPO and final capital raise quantum

- Formal commencement of the Rand Merchant Bank debt facility drawdown

- Smelter refurbishment progress and restoration of full processing capacity

- Official confirmation of the accelerated Konkola Deep development schedule

Medium-Term Execution Benchmarks (2027–2029)

- Underground development progress at Konkola Deep: shaft sinking completions, lateral development metreage, and first ore access from expanded headings

- Copper production ramp trajectory as an early indicator of whether 300,000 tonnes annually is achievable within the stated timeframe

- Cobalt production commencement and initial offtake contract terms

- Zambia's national copper output trajectory relative to the 3 million tonne 2031 goal

Key Investor Risk Factors

The market will scrutinise several dimensions carefully. Broader mining consolidation trends also suggest that assets of KCM's calibre may attract strategic interest from major miners seeking to secure long-life, high-grade copper inventory.

- Operational credibility: KCM spent years under financial strain and political uncertainty. Rebuilding institutional trust with investors requires consistent execution across multiple reporting periods.

- Sovereign risk: Zambia's track record of state intervention, however improved under the current administration, cannot be fully discounted in a multi-decade mining investment.

- Execution complexity: Ramping a deep underground mine from 80,000 to 300,000 tonnes annually is technically demanding. Underground mining projects globally carry a history of schedule overruns and cost escalations.

- Commodity price sensitivity: Copper's dual identity as an industrial metal and a macro-economic indicator means its price can move sharply on demand signals from China, US interest rate cycles, and global manufacturing data — factors entirely outside Vedanta's control.

- Power supply reliability: Zambia's electricity infrastructure constraints pose a specific operational risk for energy-intensive deep underground operations.

This article is intended for informational purposes only and does not constitute financial or investment advice. Mining projects involve material risks including commodity price volatility, operational complexity, and sovereign risk. Readers should conduct independent due diligence before making investment decisions.

Want to Stay Ahead of the Next Major Copper Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including copper and cobalt opportunities — turning complex data across 30+ commodities into a single, actionable gold-equivalent metric, so investors can act before the broader market catches on. Explore why historic mineral discoveries have generated extraordinary returns and begin a 14-day free trial to position yourself at the forefront of the next major find.