June 24, 2026

The Copper Supercycle and Why Africa Is at the Centre of It

The global mining industry is experiencing a structural reorientation that happens perhaps once every few decades. Copper, long considered the workaround metal of industrial economies, has quietly graduated into something altogether more consequential. Its conductivity underpins virtually every energy transition technology currently scaling at speed: electric vehicle powertrains, utility-scale battery storage, offshore wind turbines, solar panel interconnects, and the increasingly power-hungry data centre infrastructure being built to support artificial intelligence workloads.

Wood Mackenzie and other commodity research bodies have consistently pointed to a looming copper supply crunch emerging through the late 2020s and into the 2030s, driven by a combination of declining ore grades at established mines, a multi-decade shortage of greenfield project development, and surging downstream demand. Against this backdrop, attention has shifted decisively toward the African Copperbelt, the geological formation stretching across southern Democratic Republic of Congo and northern Zambia that contains some of the world's highest-grade and most geologically enduring copper deposits.

It is within this context that the Vedanta Zambia copper expansion plan carries significance well beyond the boundaries of a single mining company's corporate strategy. The decisions being made at Konkola Copper Mines today will influence how much of the world's copper supply originates from African soil over the next decade.

When big ASX news breaks, our subscribers know first

Zambia's Production Reality and the Distance to Its 3-Million-Tonne Ambition

Zambia produced approximately 890,000 tonnes of copper in 2025, a figure that already positions it as Africa's second-largest copper producer behind the DRC. Yet the Zambian government has set a national production target of 3 million tonnes annually by 2031, a goal that would require the country to more than triple its output within six years.

The arithmetic of that ambition is demanding. Reaching 3 million tonnes from a base of 890,000 tonnes requires adding more than 2.1 million tonnes of annual production capacity, the equivalent of building several large-scale mining operations largely from scratch, while simultaneously maintaining output at existing assets. No single operator can close that gap alone. For a broader view of what's driving this, the Zambia copper outlook reveals the scale of the national ambition and the structural challenges ahead.

The structural barriers involved are substantial:

- Zambia's electricity infrastructure has historically constrained mining operations, with load-shedding events periodically disrupting production schedules

- Rail connectivity between mine sites and port facilities at Dar es Salaam and Durban requires ongoing investment to handle materially higher concentrate and refined metal volumes

- Smelting and refining capacity within Zambia itself remains a bottleneck, with much of the country's copper historically exported as concentrate rather than finished cathode

- Skilled workforce availability at the scale required for a threefold production increase presents its own logistical challenge

Operations controlled by First Quantum Minerals and Barrick Mining accounted for approximately 60% of Zambia's copper output in 2025, making KCM's current contribution of roughly 70,000 to 80,000 tonnes a comparatively modest share. However, policymakers view Konkola as one of the assets with the clearest geological runway to materially expand the national production base.

Vedanta's Return to Konkola: From Dispute to Reinstatement

The history of Vedanta's relationship with Konkola Copper Mines is inseparable from Zambia's broader political cycle. The mine was placed under provisional liquidation by the Zambian government in 2019 under then-President Edgar Lungu, following a period of sustained tension between Vedanta and state authorities over royalty payments, workforce management, and investment commitments. What followed was a protracted legal and operational stalemate that left one of Zambia's most strategically significant mining assets in a state of extended underperformance.

The political turning point arrived with the election of President Hakainde Hichilema in 2021, whose administration adopted a markedly more investment-oriented posture toward the mining sector. Negotiations progressed, and by 2024 Vedanta had formally regained operational control of KCM following the settlement of $246 million in creditor obligations.

What makes this reinstatement analytically interesting is the condition of the asset that Vedanta reclaimed. Years of operational uncertainty had deferred maintenance across underground infrastructure, processing facilities, and the smelter. The expansion thesis being presented to investors through the CopperTech Metals IPO is therefore simultaneously a turnaround story and a greenfield development narrative, two investment risk profiles that carry materially different valuation frameworks.

The Scale of the Vedanta Zambia Copper Expansion Plan at KCM

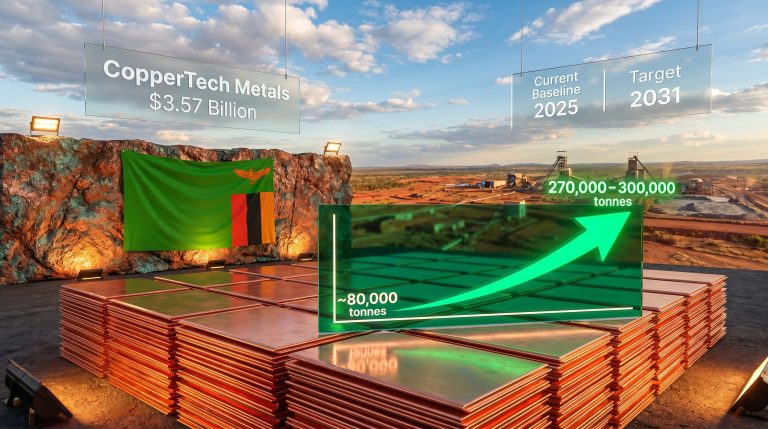

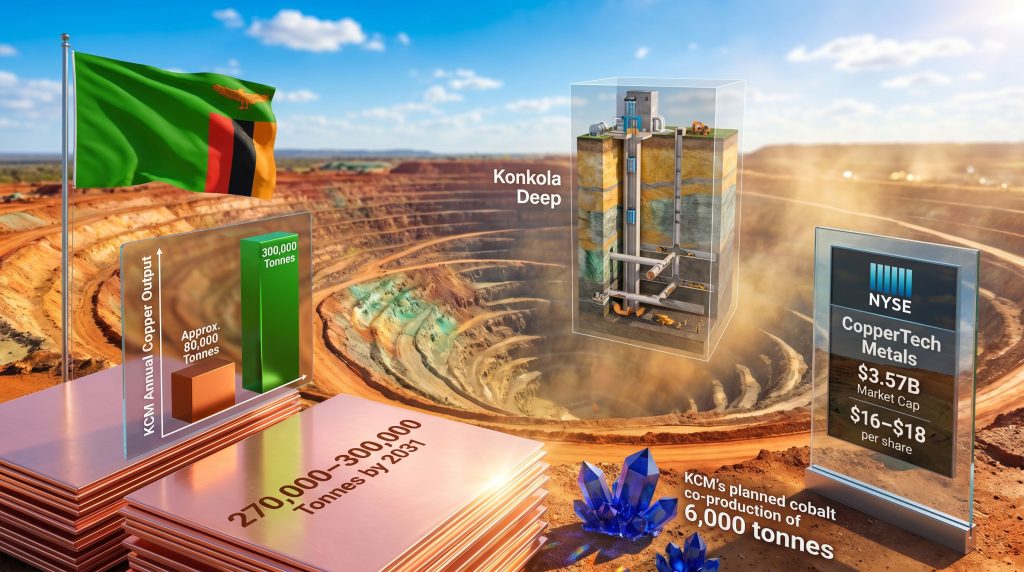

Vedanta has committed between $1.3 billion and $1.5 billion to the modernisation and expansion of Konkola Copper Mines, with approximately $1 billion to be raised through debt instruments. Rand Merchant Bank has been engaged as financial adviser on the debt financing structure. The equity component of the capital raising is anchored by the planned New York Stock Exchange listing of CopperTech Metals Inc., a US-domiciled holding company created specifically to hold Vedanta's KCM stake and access Western institutional capital markets.

The production targets embedded in the expansion plan are ambitious by any measure:

| Metric | 2025 Baseline | Expansion Target | Timeline |

|---|---|---|---|

| Annual Copper Production | ~70,000-80,000 tonnes | 270,000-300,000 tonnes | By 2031 |

| Annual Cobalt Production | Not disclosed | 6,000 tonnes | Early next decade |

| Total Capital Expenditure | Baseline | $1.3B-$1.5B | Multi-year |

| IPO Gross Proceeds (NYSE) | N/A | Up to $423.5M | 2026 listing |

| Implied Production Growth | Baseline | ~3.75x to 4.3x | 5-6 years |

Achieving a near-fourfold increase in copper output within five to six years requires simultaneous progress across multiple workstreams: new shaft development to access deeper ore horizons, refurbishment of the existing smelter, construction of a tailings leaching plant to recover copper from previously processed material, and the scaling of underground mining operations at Konkola Deep.

The Konkola Deep Underground Project: The Engine of Expansion

Konkola Deep sits at the core of the entire investment thesis. The Konkola orebody is widely regarded within the mining geology community as one of the highest-grade undeveloped copper deposits remaining in the global Copperbelt, with ore grades that compare favourably against many currently operating underground mines in both Zambia and the DRC. Higher ore grades translate directly into lower processing costs per tonne of metal produced, a critical economic advantage when capital requirements are this substantial.

Underground mining at depth presents specific engineering challenges. As shafts extend deeper, rock temperatures increase, ground conditions become more demanding, and ventilation requirements grow significantly. KCM's geological profile at Konkola Deep requires careful shaft engineering and progressive ground support investment, elements that account for a material portion of the total capital budget.

The tailings leaching plant represents a less commonly discussed but economically meaningful component of the plan. Decades of historical processing at Konkola have left behind substantial tailings volumes containing recoverable copper at grades that modern hydrometallurgical technology can profitably extract. This creates an additional copper recovery stream that does not require new ore development, furthermore lowering the marginal cost of production and improving overall capital efficiency.

According to Phesto Musonda, chairman of ZCCM Investment Holdings, the state-owned shareholder in KCM, proceeds from the IPO could shorten the Konkola Deep development timeline by approximately three years, a materially significant acceleration for a project of this scale and complexity. The smelter refurbishment programme underway at KCM is a further indication of how comprehensively the asset is being rebuilt from the ground up.

CopperTech Metals' NYSE Listing: Structure, Scale, and Strategic Logic

CopperTech Metals is targeting a valuation of up to $3.57 billion through its planned NYSE listing. The offering involves approximately 23.5 million shares priced in a range of $16 to $18 per share, generating gross proceeds of up to $423.5 million. Separately, Vedanta intends to sell an 11.9% stake in CopperTech, generating approximately $372 million, with the potential for proceeds to reach $429 million if underwriters exercise their overallotment option fully.

The decision to list an African copper asset on the New York Stock Exchange rather than in London, Johannesburg, or Toronto reflects a deliberate strategy to tap US institutional capital pools that are increasingly mandated to build exposure to critical minerals. It also elevates the asset's governance and disclosure requirements to NYSE standards, which can reduce perceived political and operational risk for international investors.

The investor documentation positions KCM not merely as an African mining turnaround but as a potential contributor to American copper supply security. This framing resonates with the broader copper price drivers shaping Western policy, particularly efforts to diversify supply chains away from single-source dependencies. Whether this positioning will resonate sufficiently with institutional investors to support the upper end of the valuation range remains to be seen.

What the IPO Structure Reveals About Vedanta's Long-Term Intentions

The creation of a standalone, US-listed vehicle to hold the KCM stake is a structurally significant signal. It indicates that Vedanta is not simply seeking project-level financing but is building a capital markets platform that could, in principle, accommodate future acquisitions or expansions within the African copper sector. A NYSE-listed entity with established investor relations infrastructure and US disclosure standards is meaningfully better positioned to raise incremental equity capital than a privately held subsidiary of an Indian conglomerate.

At the same time, Vedanta retaining the majority of CopperTech after the IPO preserves its economic exposure to the upside of the expansion while monetising a portion of its position at a valuation that reflects the growth narrative rather than the current operational baseline.

Cobalt as a Strategic Co-Product: A Revenue Stream Often Overlooked

KCM's planned cobalt production target of 6,000 tonnes annually deserves more attention than it typically receives in coverage of the Vedanta Zambia copper expansion plan. The Konkola orebody carries cobalt as a natural co-product of copper mineralisation, a geological characteristic common across the Central African Copperbelt but less prominent in major copper districts elsewhere in the world.

Cobalt demand from battery manufacturers, particularly for nickel-manganese-cobalt cathode chemistries used in electric vehicle batteries and stationary energy storage, has created a structurally supported price environment for responsibly sourced cobalt from stable jurisdictions. In addition, the broader Congolese cobalt rivalry between Western and Chinese supply chain actors has heightened interest in Zambian cobalt as a credible alternative sourcing option.

A Zambian supply source, subject to NYSE-level governance standards through the CopperTech structure, could attract premium pricing interest from battery supply chain participants seeking to demonstrate sourcing credibility. Six thousand tonnes of annual cobalt production, while not transformative at the global scale, represents a meaningful revenue diversification stream that reduces KCM's commodity concentration risk and strengthens the overall investment case.

The next major ASX story will hit our subscribers first

Zambia's Competitive Copper Landscape

Understanding where KCM fits within Zambia's existing copper production structure provides important context for evaluating the expansion's potential impact:

| Operation | Approximate Share of 2025 Output | Primary Operator |

|---|---|---|

| First Quantum Minerals assets | ~35-40% | First Quantum Minerals |

| Barrick Mining assets | ~20-25% | Barrick Mining |

| Konkola Copper Mines | ~9% | Vedanta / CopperTech Metals |

| Other producers | Remainder | Various |

A fully expanded KCM producing 270,000 to 300,000 tonnes annually would shift the competitive dynamics of Zambia's copper industry substantially, lifting KCM's share of national output and reducing the sector's dependence on any single operator. For the Zambian government, production diversification across multiple large-scale operators represents a meaningful reduction in sovereign revenue concentration risk. Consequently, the global copper supply gap that analysts have long warned about makes this kind of African expansion all the more strategically important.

Investor Risk Considerations: What Must Be Weighed Against the Growth Story

The investment thesis for CopperTech rests on a turnaround narrative layered over a commodity supercycle argument. Each element carries its own risk profile, and prospective investors will need to assess both independently.

Key risk factors include:

- Sovereign and political risk: Zambia's history of government intervention in the mining sector, most recently at KCM itself in 2019, cannot be dismissed as a resolved matter. Regulatory frameworks and fiscal terms can change with administrations.

- Execution risk: The gap between current production of 70,000 to 80,000 tonnes and the 300,000-tonne target is a substantial operational challenge requiring sustained capital deployment, skilled project management, and reliable infrastructure support.

- Asset condition: Years of operational deterioration during the liquidation period mean that the capital required to restore and then expand KCM is higher than would be the case for a well-maintained asset.

- Commodity price sensitivity: Copper price volatility directly affects project economics. While the structural demand outlook is broadly constructive, near-term price swings can materially alter the financial case for capital-intensive underground development.

- Financing execution: Raising approximately $1 billion in debt for an African mining asset with a complicated recent history requires supportive credit market conditions and lender confidence in the operational team's delivery capability.

This article is for informational purposes only and does not constitute financial or investment advice. Readers should conduct their own due diligence before making any investment decisions.

What a Successful KCM Expansion Would Mean for African Mining Investment

The broader implications of the Vedanta Zambia copper expansion plan extend beyond KCM's production targets. If CopperTech successfully completes its NYSE listing at or near its target valuation, and if the Konkola Deep development proceeds materially on schedule, it would demonstrate something that African mining investment has long needed: that large-scale turnaround projects in the region are financeable through mainstream Western capital markets at institutional scale.

That precedent matters enormously for the pipeline of copper development projects across the Copperbelt. Several substantial deposits in both Zambia and the DRC remain undeveloped partly because operators have struggled to access the scale of capital required at acceptable cost. A NYSE-listed African copper vehicle with demonstrated execution credibility would, furthermore, expand the financing toolkit available to the sector as a whole.

The Vedanta Zambia copper expansion plan is, in this sense, as much a test of capital market architecture as it is a mining development story. Its outcome will be watched carefully by every major resource company with African copper ambitions.

Frequently Asked Questions: Vedanta Zambia Copper Expansion Plan

What is Vedanta's total investment commitment at Konkola Copper Mines?

Vedanta has committed between $1.3 billion and $1.5 billion to modernise and expand KCM, with approximately $1 billion expected to be raised through debt financing and the balance through equity capital markets, primarily via the planned CopperTech Metals NYSE listing.

What is CopperTech Metals and why was it created?

CopperTech Metals Inc. is a US-domiciled holding company established by Vedanta to hold its stake in KCM. The structure was designed to facilitate access to US capital markets and enable a New York Stock Exchange listing, with a target valuation of up to $3.57 billion.

How much copper does KCM currently produce and what is the target?

KCM produced approximately 70,000 to 80,000 tonnes of copper annually as of 2025. Vedanta's expansion plan targets 270,000 to 300,000 tonnes per year by 2031, representing a near-fourfold increase in output.

What is the Konkola Deep project?

Konkola Deep is the underground mining development at the heart of KCM's expansion. It involves sinking new shafts to access deeper, high-grade ore reserves, supported by smelter refurbishment and a tailings leaching plant. ZCCM Investment Holdings has indicated that IPO proceeds could accelerate this project's completion by approximately three years.

How does KCM's expansion support Zambia's national copper production goals?

Zambia has set a target of producing 3 million tonnes of copper annually by 2031, compared with approximately 890,000 tonnes in 2025. A fully expanded KCM producing up to 300,000 tonnes per year would represent a meaningful contribution toward that national target, though achieving the full 3-million-tonne goal will require parallel expansion across multiple operators.

Who is Anil Agarwal and what is his role in the Vedanta expansion?

Anil Agarwal is the founder and controlling shareholder of Vedanta Resources, the Indian-headquartered natural resources conglomerate. Forbes estimates his net worth at approximately $4.6 billion. He has been the central figure in Vedanta's re-engagement with KCM following the political and legal disputes that led to the mine's government seizure in 2019.

For additional context on Zambia's copper sector and the broader African mining investment environment, Ecofin Agency at ecofinagency.com provides ongoing coverage of regulatory developments and sector-level trends relevant to this expansion story.

Want to Know Which ASX Copper Discoveries Could Deliver the Next Major Return?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries — including copper — and turning complex data into actionable investment insights before the broader market reacts. Explore historic examples of major mineral discoveries and their extraordinary returns, then start your 14-day free trial at Discovery Alert to position yourself ahead of the next big find.