July 10, 2026

The Global Copper Supply Crunch Is Rewriting the Rules of African Mining Finance

For most of the past decade, the critical minerals conversation was dominated by lithium. Battery gigafactories, EV supply chains, and energy storage projects absorbed the investment narrative, leaving copper to play a supporting role. That dynamic is shifting rapidly. Copper's unique combination of electrical conductivity, thermal properties, and near-irreplaceable status across energy, defence, and digital infrastructure is pushing it to the centre of the global resource investment cycle. Nowhere is that repositioning more visible than in Zambia, where a convergence of capital, geology, and geopolitics is reshaping how Africa's copper wealth reaches global markets.

The Vedanta New York IPO Zambia copper expansion story encapsulates this broader transformation. It is not simply a corporate financing event. It is a signal that US equity markets are becoming the preferred destination for large-scale African resource capital raises, and that Zambia's Copperbelt is re-emerging as one of the most strategically valuable mining addresses on the planet. Furthermore, the copper supply crunch underpinning this shift is intensifying with each passing quarter.

When big ASX news breaks, our subscribers know first

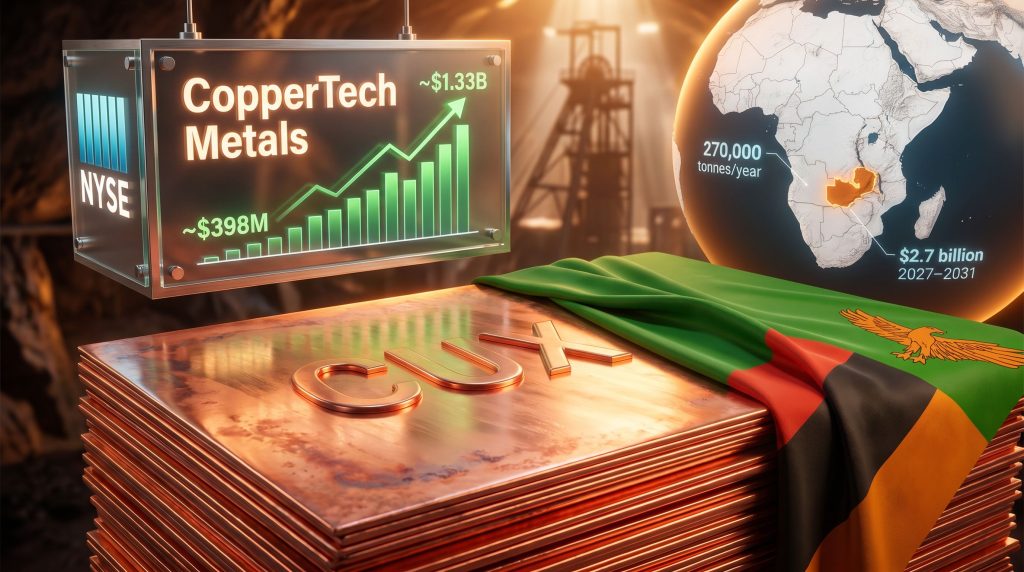

How CopperTech Metals Brings Zambian Copper to the NYSE

The Architecture of the US Listing Structure

Vedanta Resources, the diversified mining group led by billionaire Anil Agarwal, incorporated a dedicated US subsidiary called CopperTech Metals in 2025. This entity serves as a ringfenced capital vehicle specifically designed to hold and expand Vedanta's Zambian copper operations, primarily through its flagship asset, Konkola Copper Mines (KCM).

CopperTech has filed for a listing on the New York Stock Exchange under the proposed ticker symbol CUX. The structural logic behind this approach is deliberate and sophisticated:

- Separating KCM from Vedanta's broader, more complex balance sheet creates a clean, standalone investment case for US-based investors

- A dedicated vehicle allows CopperTech to attract critical minerals-focused institutional capital, sovereign wealth funds, and sector-specific ETFs that may not engage with diversified conglomerates

- The US incorporation establishes regulatory credibility within the American institutional investment community

- A NYSE listing provides access to deeper liquidity pools and potentially higher valuation multiples than alternative exchanges in London or Johannesburg

Where the IPO Capital Is Directed

While the total IPO raise has not been formally disclosed, the use-of-proceeds framework outlined in CopperTech's prospectus filing provides a clear picture of capital allocation priorities:

- Approximately $670 million from the offering is earmarked to fulfil the remaining portion of Vedanta's previously committed $1 billion investment obligation to KCM

- Supplementary capital is allocated toward production expansion infrastructure at the Konkola complex

- Targeted exploration spending is included to extend the known resource base

- The broader CopperTech capital plan encompasses approximately $2.7 billion in total investment scheduled between 2027 and 2031

This structure effectively converts a bilateral corporate commitment into a publicly traded equity obligation, creating a transparency mechanism that aligns investor interests with operational delivery milestones at KCM.

The Financial Scale Behind the IPO Narrative

Revenue Growth Heading Into the Offering

One of the most compelling elements of CopperTech's investor story is the velocity of its recent revenue growth. The financial trajectory heading into the IPO demonstrates that KCM has been successfully rehabilitated from a contested, underperforming asset into a commercially active and rapidly scaling operation.

| Metric | FY Ended March 2025 | FY Ended March 2026 |

|---|---|---|

| Net Sales | ~$398 million | ~$1.33 billion |

| Year-on-Year Revenue Growth | Baseline | ~234% |

| Primary Revenue Driver | Konkola Copper Mines, Zambia | Konkola Copper Mines, Zambia |

This more than threefold increase in net sales within a single fiscal year is a materially important data point for the IPO process. It signals to prospective investors that:

- The operational turnaround at KCM is already well advanced before the listing occurs

- The asset is not speculative or pre-revenue; it is generating substantial and growing commercial output

- The growth trajectory supports the credibility of the 270,000-tonne annual production target as a reachable medium-term goal rather than an aspirational projection

Understanding KCM's Production Profile and Resource Base

KCM operates within the Central African Copperbelt, a geological formation that spans northern Zambia and the Democratic Republic of Congo and is widely regarded as the world's most copper-rich stratigraphy. The Copperbelt's deposits are characterised by sediment-hosted, stratiform copper mineralisation, which typically delivers consistent ore grades across large, continuous resource bodies.

This geology is fundamentally different from the porphyry copper deposits that dominate South American production and tends to support more predictable underground mining operations once developed. CopperTech's prospectus targets 270,000 tonnes of annual copper production as the long-term output benchmark. A central component of reaching that figure is the development of the Konkola Deep Mining Project, an underground resource considered among the most significant untapped copper deposits remaining in the Copperbelt.

The deep orebody extends to considerable depth below existing workings, requiring shaft deepening, expanded ventilation infrastructure, and high-volume dewatering systems. These capital requirements explain the scale of the $2.7 billion investment programme and the necessity of equity capital rather than incremental debt financing.

Zambia's Production Ambitions and the Capital Gap

The Scale of What Needs to Be Built

Zambia produced approximately 890,346 tonnes of copper in 2025, representing an 8% increase from the prior year, according to industry data. Despite this recovery momentum, the country fell short of the symbolically important one-million-tonne threshold. In addition, Zambia copper growth ambitions extend far beyond simple incremental progress.

The Zambian government's stated ambition is far more aggressive than incremental improvement. The national target calls for 3 million tonnes of annual copper production by 2031, effectively requiring the country to add more than 2.1 million tonnes of new annual capacity within six years from a base that has not yet reached one million tonnes. The arithmetic of that gap makes the scale of capital currently entering Zambia not just welcome, but mathematically essential.

The Competitive Investment Landscape Inside Zambia

| Operator | Project | Committed Investment | Target Annual Output |

|---|---|---|---|

| CopperTech Metals (Vedanta) | Konkola Copper Mines | ~$2.7 billion (2027-2031) | 270,000 tonnes |

| KoBold Metals | Mingomba Copper Project | ~$2.5 billion | ~300,000 tonnes |

| First Quantum Minerals | Kansanshi and Sentinel | Ongoing expansion | Major existing producer |

| Mopani Copper Mines | Mopani rehabilitation | Ongoing | Recovery phase |

| Multiple Chinese operators | Various Copperbelt sites | Undisclosed | Expanding |

The simultaneous commitment of multiple billion-dollar programmes across a single national jurisdiction is historically unusual and reflects how decisively Zambia's investment profile has changed. KoBold Metals, backed by Bill Gates and Jeff Bezos, is targeting its Mingomba project for production in the early 2030s with potential output of around 300,000 tonnes annually, directly comparable to CopperTech's ambitions.

What makes this moment distinctive is not just the volume of capital, but the diversity of its origins. US technology billionaires, Indian conglomerates, established Canadian miners, and Chinese state-linked operators are all converging on the same Copperbelt geology simultaneously — an intensity of focus not seen since the original colonial-era mining development of the region.

The Four Structural Forces Driving Copper Demand

Why This Demand Cycle Feels Different from Previous Commodity Booms

CopperTech's prospectus identifies four distinct structural copper demand drivers, each of which is independently capable of sustaining elevated copper consumption. Their convergence creates compounding pressure on a supply base that cannot respond quickly.

-

Artificial intelligence and data centre infrastructure: Every large-scale AI data centre requires substantial copper for power distribution busbars, cooling systems, rack-level electrical interconnections, and facility-wide grounding networks. As hyperscalers accelerate data centre construction globally, copper intensity per megawatt of deployed computing capacity is rising.

-

Energy transition and grid electrification: The shift to renewable energy generation and the electrification of transport are copper-intensive across the entire value chain. Wind turbines use between 3 and 5 tonnes of copper per megawatt of capacity, offshore installations use significantly more, and EV drivetrain and charging networks require copper at multiple points in the system architecture.

-

Defence spending escalation: Rising military budgets across NATO member states and Indo-Pacific nations are increasing demand for copper in advanced weapons platforms, electronic warfare systems, naval vessels, and communications infrastructure. This demand stream is largely price-inelastic, creating a stable floor under consumption even during economic downturns.

-

Emerging market urbanisation: Infrastructure development across South and Southeast Asia, Sub-Saharan Africa, and Latin America continues to drive long-cycle demand for copper in construction, industrial plant, and grid buildout as hundreds of millions of people are connected to modern electrical systems for the first time.

The Supply Response Problem

What differentiates this copper demand cycle from prior commodity supercycles is the structural impediment on the supply side. Key constraints include:

- New mine development from discovery to nameplate production typically requires 10 to 20 years, meaning no supply response initiated today can meaningfully address demand growth before the mid-2030s

- Average ore grades at operating copper mines globally have been declining for decades as higher-grade surface deposits are progressively exhausted, requiring more ore processing per tonne of refined output

- Permitting timelines in established mining jurisdictions, particularly in North and South America, have lengthened significantly due to environmental review requirements and community consultation processes

- Water scarcity is increasingly constraining operations at major copper-producing regions in Chile and Peru, which together account for approximately 40% of global mine supply

This supply-demand asymmetry creates a structural premium for large-scale, developable copper assets in jurisdictions where permitting environments are supportive and resources are confirmed. That description fits the Central African Copperbelt more precisely today than at any point in the past two decades.

Copper's Geopolitical Elevation and the NYSE Listing Logic

Washington's Strategic Minerals Agenda

The Trump administration formally designated copper as a strategically important mineral, adding it to the growing roster of materials considered critical to US economic competitiveness and national security. This classification reflects a broader industrial policy shift, and the evolving metals geopolitics of this era are reshaping how resource capital flows globally.

The designation is aimed at reducing American dependence on Chinese-controlled supply chains across the full spectrum of materials essential to defence manufacturing, clean energy deployment, and advanced technology production.

It is important to note that this designation represents a national policy framework, not project-specific support. CopperTech's IPO and KCM's expansion programme are commercial undertakings, and no confirmed government backing, funding, or formal project designation for CopperTech from US authorities has been publicly disclosed.

Why New York Makes Strategic Sense for This Specific Listing

Vedanta's decision to list CopperTech in New York rather than on the London Stock Exchange, the Toronto Stock Exchange, or a regional African exchange reflects a calculated capital markets strategy:

- US institutional investors are being redirected toward critical mineral supply chain assets outside of China's sphere of influence, creating an audience specifically motivated to consider a Zambian copper vehicle

- The depth and liquidity of US equity markets can support larger transaction sizes and more complex investor syndications than most alternative exchanges

- A NYSE listing positions CopperTech within the same conversation as US-oriented critical minerals companies, potentially qualifying the stock for inclusion in sector-specific indices and ETFs focused on energy transition materials

- The US corporate structure of CopperTech may facilitate engagement with offtake counterparties, infrastructure co-investors, and trade finance providers who have a preference for dealing with US-domiciled entities

The next major ASX story will hit our subscribers first

Key Risks That Investors Need to Understand

Operational Complexity at Depth

The Konkola Deep Mining Project is not a straightforward development. Underground copper mining at depth introduces a specific set of technical and financial challenges that are materially different from open-pit operations or shallow underground mines:

- Dewatering requirements: The Konkola orebody is located in a naturally water-bearing geological formation. Managing inflows at depth requires continuous high-volume pumping operations, which represent both a significant operating cost and a potential production disruption risk if systems fail

- Shaft infrastructure capital intensity: Accessing deep orebodies requires either deepening existing vertical shafts or sinking new ones, each of which is a multi-year, capital-intensive programme with limited flexibility to accelerate timelines

- Ventilation and cooling systems: At depths below 1,000 metres, rock temperatures rise substantially, requiring engineered ventilation and cooling infrastructure to maintain safe working environments and operational productivity

- Production ramp-up timelines: Even well-capitalised deep underground projects typically require several years between the start of development capital expenditure and achieving nameplate production rates

Sovereign and Regulatory Risk

KCM's history is inseparable from the broader narrative of Zambia's mining policy volatility. The asset was previously subject to a prolonged ownership dispute between Vedanta and the Zambian government, a period during which production deteriorated significantly and the asset's commercial value was materially impaired. While Vedanta regained operational control and has since demonstrated strong revenue recovery, this history remains a reference point for investors assessing sovereign risk within the Zambian jurisdiction.

Additional regulatory risk factors include the potential for changes to Zambia's mining royalty structure, export levy framework, or foreign exchange repatriation rules, any of which could alter the economics of KCM's expansion programme without necessarily changing the underlying ore resource.

Market and Valuation Risks

- Copper prices remain cyclically sensitive to Chinese industrial output, global GDP growth, and US dollar movements, meaning CopperTech's financial performance will be partially correlated with macro factors outside management control

- US equity markets have historically applied more demanding listing standards and liquidity requirements to mining and resources companies than to technology or healthcare businesses, requiring CopperTech to build a compelling differentiated investment thesis

- The concentration of CopperTech's value in a single asset, in a single country, creates idiosyncratic risk that cannot be diversified within the vehicle itself

Consequently, investors considering this offering should review appropriate copper investment strategies before making any allocation decisions.

This article contains forward-looking statements and financial projections sourced from publicly available information. These projections are inherently uncertain and should not be construed as investment advice. Readers should conduct independent due diligence before making any investment decisions.

What CopperTech's NYSE Listing Signals for African Mining Finance

A Structural Shift in How African Resources Access Global Capital

Beyond the specifics of KCM and Vedanta, the Vedanta New York IPO Zambia copper expansion may represent the beginning of a more fundamental change in the architecture of African resource finance. For most of the post-colonial era, large African mining assets accessed global capital through London, Toronto, or Johannesburg listings. Each of these markets carries a different investor base, valuation framework, and liquidity profile.

The pivot toward New York reflects the recognition that US capital markets now offer a superior combination of depth, critical minerals-awareness, and institutional appetite for assets that align with Washington's strategic materials agenda. If CopperTech's listing succeeds in attracting substantial US institutional participation and achieves a competitive valuation multiple, it will establish a template that other African resource operators are likely to follow.

The Broader Zambia Investment Story

The concentration of capital in Zambia from CopperTech, KoBold Metals, First Quantum Minerals, Barrick, Mopani, and multiple Chinese operators simultaneously creates a unique dynamic. The infrastructure investments required to service these projects — from power transmission upgrades to improved road and rail logistics — create positive externalities that benefit all operators and progressively de-risk the jurisdiction for future entrants.

Zambia's ability to sustain and attract this capital over the next decade will ultimately depend on the consistency and predictability of its regulatory environment. The country's trajectory toward the 3-million-tonne production target is technically achievable given the confirmed resource base, but it is contingent on maintaining an investment climate that protects existing capital commitments while attracting new ones.

For global investors, Zambia's Copperbelt represents one of the few places on earth where confirmed large-scale copper resources, advancing development programmes, and growing institutional capital infrastructure are converging at precisely the moment when the world's demand for copper is entering its most structurally compelling period in generations.

Frequently Asked Questions

What is CopperTech Metals and how does it relate to Vedanta Resources?

CopperTech Metals is a US-incorporated subsidiary established by Vedanta Resources in 2025. It functions as the dedicated capital-raising and holding entity for Vedanta's Zambian copper operations, with Konkola Copper Mines as its primary asset. The company has filed for a New York Stock Exchange listing under the proposed ticker CUX.

How much capital is being raised through the CopperTech IPO?

The total IPO size has not been formally disclosed. The prospectus indicates that approximately $670 million of the proceeds will be directed toward completing Vedanta's $1 billion investment commitment to KCM, with additional funds allocated to production expansion and exploration.

What is the Konkola Deep Mining Project?

The Konkola Deep Mining Project is a substantial underground copper resource within the KCM complex in Zambia's Copperbelt. It is considered one of the most significant undeveloped copper deposits remaining in Central Africa and is central to CopperTech's ambition of reaching 270,000 tonnes of annual copper output. Its development requires deep shaft infrastructure, high-volume dewatering systems, and sustained capital investment over multiple years.

Why is Zambia attracting so much copper investment in 2026?

Zambia's government has set a national production target of 3 million tonnes of copper annually by 2031, roughly triple current output. Combined with rising global demand from AI infrastructure, electrification, and defence spending, alongside the US government's designation of copper as a strategically important mineral, Zambia has become one of the most actively targeted copper investment destinations in the world.

Does the US critical minerals policy provide direct support to CopperTech's project?

No. The US government's critical minerals designation for copper represents a national policy framework, not project-specific support for CopperTech or KCM. The designation creates a favourable investment climate and redirects institutional capital toward non-Chinese copper supply chain assets, however no confirmed government funding, strategic project designation, or accelerated permitting for CopperTech has been publicly disclosed.

Want to Track the Next Major Copper Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries — including copper — and delivering actionable insights directly to subscribers before the broader market has time to react. Start your 14-day free trial at Discovery Alert today, or explore the discoveries page to understand how historic mineral finds have generated substantial returns for early movers.