July 10, 2026

The Quiet Revolution Reshaping Global Unconventional Oil Markets

For most of the past two decades, the story of shale oil has been told through a distinctly American lens. The Permian Basin, the Bakken, the Eagle Ford — these names became synonymous with the unconventional revolution that fundamentally altered global energy supply dynamics. Yet deep in Argentine Patagonia, a formation has been quietly accumulating the geological credentials and infrastructure prerequisites to challenge that narrative. The scale of capital now being committed to Vaca Muerta suggests the next chapter of the global shale story may be written not in Texas or North Dakota, but in the windswept high desert of Neuquén province.

The YPF Vaca Muerta $25 billion investment plan, submitted under Argentina's Large Investment Incentive Regime (RIGI) for its LLL Oil development, marks a structural inflection point — not merely for Argentina's energy sector, but for how international capital evaluates emerging unconventional basins in jurisdictions historically perceived as high-risk. Understanding what this plan actually proposes, and why it carries genuine geopolitical and macroeconomic weight, requires looking beyond the headline numbers.

Disclaimer: This article contains forward-looking projections based on YPF's publicly announced plans as reported by World Oil on May 18, 2026. Production targets, revenue forecasts, and timeline estimates are subject to material change based on financing conditions, regulatory developments, infrastructure progress, and commodity price movements. Nothing in this article constitutes financial or investment advice.

When big ASX news breaks, our subscribers know first

What the LLL Oil Development Actually Proposes

Before evaluating the broader implications, it is worth establishing precisely what YPF has put forward. The LLL Oil development is not a single drilling program or a discrete asset transaction. It is a fully integrated, multi-decade unconventional development program structured across geographically contiguous acreage in the Vaca Muerta formation, designed to share infrastructure across every stage of the value chain.

The integrated architecture is central to the project's economic logic. By consolidating drilling rigs, hydraulic fracturing spreads, water logistics, sand supply networks, and surface infrastructure across a unified acreage position, YPF aims to achieve the per-well cost reductions that transformed North American shale economics in the 2010s. This pad-drilling, shared-infrastructure model — pioneered by leading Permian Basin operators — allows capital efficiency to compound as development density increases.

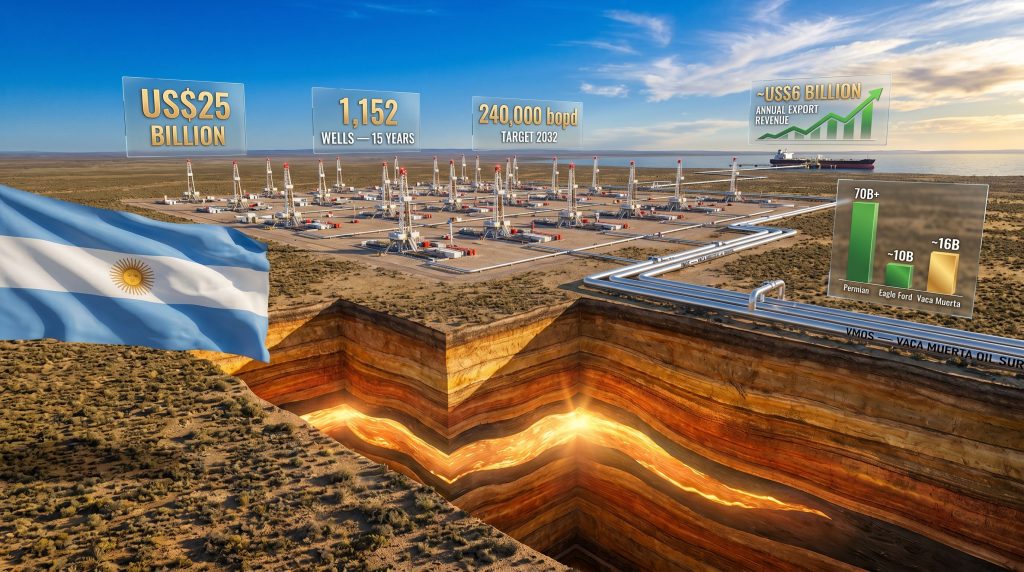

Key Project Metrics at a Glance

| Parameter | Detail |

|---|---|

| Total Capital Commitment | US$25 billion |

| Development Timeline | 15 years |

| Wells to Be Drilled | 1,152 |

| Peak Production Target | ~240,000 bopd (from 2032) |

| Projected Annual Export Revenue | ~US$6 billion (at plateau) |

| Direct Employment Created | ~6,000 jobs |

| Export Destination | International markets via VMOS system |

| Gas Disposition | Argentina's domestic market |

| Regulatory Framework | RIGI Large Investment Incentive Regime |

To contextualise that production target: 240,000 barrels of oil per day from a single integrated project would place it in the same output league as the entire national production of several OPEC member states. It is a volume that demands serious attention from any participant in global energy markets monitoring long-term supply trends. Furthermore, crude oil price trends heading into the mid-2020s have reinforced the strategic logic of locking in long-term unconventional development programs at scale.

A lesser-discussed but technically significant aspect of the project structure is the deliberate separation of crude oil and natural gas revenue streams. All produced crude will flow to export markets, capturing international Brent-linked pricing, while associated gas production feeds domestic supply. This bifurcated disposition strategy is not incidental — it reflects a deliberate optimisation of Argentina's dual objectives: earning hard currency through oil exports while addressing chronic domestic gas supply constraints simultaneously.

What Is Argentina's RIGI Regime and Why Does It Matter for Vaca Muerta?

Understanding the Regulatory Architecture Enabling This Investment

Argentina's Large Investment Incentive Regime was introduced as a mechanism to attract capital into sectors where long payback horizons and sovereign risk premiums have historically deterred institutional investors. For energy projects specifically, the framework delivers a combination of protections that collectively address Argentina's most persistent investment deterrents:

- Tax stabilisation provisions that protect investors from future legislative changes eroding project economics

- Customs duty exemptions reducing the cost of importing specialised drilling and completion equipment

- Foreign exchange flexibility allowing companies to retain and repatriate a defined portion of export revenues

What makes RIGI genuinely consequential for a project of this scale is the legal durability of these provisions. In project finance terms, the ability to structure long-tenor debt around a stable, predictable regulatory baseline fundamentally changes the risk-adjusted return calculation for international lenders and equity partners. Without such a mechanism, securing financing for a 15-year, $25 billion commitment in an economy carrying Argentina's historical volatility would face near-insurmountable hurdles in international capital markets.

Argentina resource investment patterns across other resource sectors demonstrate that when regulatory frameworks credibly protect returns, large-scale capital commitments do follow — even in markets with complex sovereign histories. The YPF LLL Oil application is reported by World Oil to be the largest single submission filed under the RIGI framework to date, which itself signals something important about market confidence in the regime's durability.

What Investors Often Overlook About Regulatory Stability Mechanisms

A subtlety frequently missed in surface-level analysis of investment incentive regimes is that their value is not purely about the tax benefits themselves. The more important function is what economists call credible commitment — the ability of a government to bind future administrations to the same policy conditions. Argentina's 2012 nationalisation of YPF remains a reference point for every international energy investor evaluating Argentine exposure. RIGI's explicit legal stability provisions are therefore as much about rewriting Argentina's sovereign risk narrative as they are about reducing specific project costs.

"The scale of any RIGI application functions as a real-world stress test of Argentina's commitment to its investment framework. When a state-owned company places a $25 billion bet on the enforceability of these provisions, it implicitly communicates confidence that the legal architecture is substantively different from prior regulatory environments."

How Does Vaca Muerta Compare to the World's Major Shale Basins?

Positioning Argentina's Unconventional Resource Within the Global Shale Hierarchy

Vaca Muerta's geological credentials have been extensively discussed in petroleum engineering literature, but several characteristics that distinguish it from North American analogues are less frequently emphasised in mainstream energy coverage.

Comparative Basin Analysis

| Shale Basin | Country | Estimated Recoverable Resource | Development Status |

|---|---|---|---|

| Permian Basin | USA | 70+ billion barrels | Mature, high-output |

| Bakken Formation | USA | ~8–10 billion barrels | Mature |

| Eagle Ford | USA | ~10 billion barrels | Mature |

| Vaca Muerta | Argentina | ~16 billion barrels oil equivalent | Early-to-mid development |

| Duvernay | Canada | ~3–5 billion barrels | Early development |

Note: Resource estimates are approximate and drawn from publicly available geological assessments. Methodologies vary between agencies and studies.

What Makes Vaca Muerta Technically Distinctive

Three geological factors set Vaca Muerta apart from many of its North American counterparts in ways that directly affect development economics:

1. Exceptional formation thickness

Vaca Muerta's productive intervals span a notably greater vertical thickness than most North American shale plays. Where the Barnett Shale typically offers a net pay thickness of roughly 100 metres, Vaca Muerta's productive zone extends across several hundred metres of formation depth in core areas. This multi-zone stacking potential means that a single well pad can target multiple productive horizons, amplifying recoverable resource per surface location — a critical factor in reducing cost-per-barrel metrics at scale.

2. Rock quality consistency across large acreage blocks

The formation demonstrates relatively uniform geomechanical properties — particularly brittleness and total organic carbon content — across broad acreage positions. This consistency is operationally valuable because it allows operators to standardise completion designs across well programs without the extensive variability management that characterises some North American plays. Standardised completions reduce completion costs and improve hydraulic fracturing efficiency at scale.

3. Total organic carbon content and thermal maturity

Vaca Muerta's source rock quality, measured by total organic carbon (TOC) content, is among the highest documented in any major unconventional formation globally. TOC levels averaging between 4% and 6% in core areas, with peak values exceeding 8% in some intervals, indicate exceptional hydrocarbon generation potential. When combined with the formation's thermal maturity window — which spans the optimal range for liquid hydrocarbon generation — the geological fundamentals underpin the high initial production rates observed in early development wells.

4. Export infrastructure proximity

Unlike the landlocked Permian sub-basins that required massive pipeline buildout to reach Gulf Coast terminals, Vaca Muerta benefits from relative proximity to Atlantic export corridors via the VMOS pipeline system. This structural midstream advantage reduces the incremental infrastructure investment required per barrel of export capacity compared to many continental shale analogues.

What Is the VMOS Export System and How Does It Unlock Vaca Muerta's Export Potential?

The Infrastructure Backbone Behind the $6 Billion Annual Export Target

The Vaca Muerta Oil Sur (VMOS) pipeline and marine export system represents the critical midstream infrastructure connecting Vaca Muerta's wellheads to international tanker routes. This distinction matters more than it might initially appear: in unconventional oil development, the gap between announced production targets and actual export delivery is almost always determined by midstream infrastructure capacity, not by reservoir quality.

The specific infrastructure dependencies for the LLL Oil project to achieve its 240,000 bopd plateau include:

- Pipeline capacity sufficient to handle incremental volumes from 1,152 wells across a 15-year ramp

- Marine terminal throughput capable of loading supertanker-class vessels for long-haul Atlantic export routes

- Water supply and disposal infrastructure supporting one of the largest hydraulic fracturing programs ever proposed in South America

- Sand logistics networks — potentially including domestic proppant supply development — for continuous fracturing operations across the drilling program

- Power generation infrastructure for large-scale fracturing spread operations in Neuquén's arid environment

"The 2032 production plateau target is achievable only if VMOS expansion proceeds in strict operational parallel with upstream drilling activity. Historical unconventional development programs globally suggest that midstream lag, rather than drilling execution, represents the most common cause of plateau timeline slippage."

A point worth noting that rarely receives prominent coverage: the water management dimension of this project is arguably as operationally complex as the drilling program itself. Hydraulic fracturing at the scale of 1,152 wells over 15 years in an arid high-desert environment requires either large-scale water sourcing agreements from the Neuquén River system or significant investment in produced water recycling infrastructure. The Neuquén River basin's regulatory framework governing water rights and produced water disposal will be a critical operational variable throughout the project's life.

What Are the Macroeconomic Implications for Argentina?

From Structural Dollar Shortage to Export Powerhouse: The Balance of Payments Equation

Argentina's chronic foreign exchange constraints have historically operated as a binding ceiling on economic activity — restricting import capacity, distorting domestic pricing mechanisms, and complicating external debt servicing. A project capable of generating approximately US$6 billion in annual export revenues at plateau would represent a structurally significant addition to Argentina's foreign exchange earnings, with compounding effects across the broader economy.

Projected Macroeconomic Impact Scenarios

| Scenario | Production Achievement | Annual Export Revenue | Balance of Payments Impact |

|---|---|---|---|

| Base Case | 240,000 bopd by 2032 | ~US$6 billion | Significant positive |

| Conservative Case | 180,000 bopd by 2034 | ~US$4.5 billion | Moderate positive |

| Delayed Case | Infrastructure lag to 2036 | ~US$3–4 billion | Limited near-term impact |

The employment dimension carries its own macroeconomic multiplier logic. The project's 6,000 direct employment positions during the development phase generate substantial indirect and induced economic activity in Neuquén province. Historical unconventional development programs in comparable basins have documented indirect-to-direct employment ratios of between 3:1 and 5:1, suggesting the project's total employment footprint could ultimately represent 18,000 to 30,000 jobs across direct, indirect, and induced categories in the regional economy.

The Peso Stability Dimension

A dimension less frequently analysed in project-level coverage is the potential contribution of a sustained, large-scale oil export stream to Argentina's peso stability trajectory. Chronic dollar shortages have historically fed into currency pressures that periodically destabilised business planning horizons.

A reliable, growing pipeline of hard-currency export revenues from Vaca Muerta could provide the Argentine central bank with a more stable reserve accumulation pathway than has been achievable through most of the past two decades — though this outcome is contingent on both project execution and the durability of the macroeconomic reform agenda. In addition, the oil price rally dynamics of recent years have further strengthened the case for accelerating export-oriented unconventional development in resource-rich emerging markets.

The next major ASX story will hit our subscribers first

What Are the Key Operational Risks Investors and Analysts Should Monitor?

A Multi-Dimensional Risk Framework for Evaluating the LLL Oil Development

1. Financing and Capital Markets Risk

Securing $25 billion across a 15-year horizon requires sustained access to international debt markets, export credit agency facilities, and potentially multilateral lending institutions. Argentina's sovereign credit profile adds a meaningful risk premium to all financing structures. The pace at which YPF can syndicate project debt — and the interest rate conditions governing those facilities — will materially affect development economics and timeline adherence.

2. Regulatory Continuity Risk

RIGI's fiscal stability provisions carry legal weight, but Argentina's regulatory history introduces a residual sovereign discount that international investors will incorporate into required returns. The 2012 YPF nationalisation remains an active reference point in investor due diligence processes, and any signals of policy reversal under future administrations would materially affect the project's financing conditions.

3. Execution and Supply Chain Risk

Drilling 1,152 wells over 15 years requires continuous availability of:

- Drilling rigs designed for Vaca Muerta's specific well geometries and depths

- Hydraulic fracturing spreads at sufficient scale to sustain the drilling program's pace

- Proppant supply chains, either domestic or imported, adequate for the completion program

- Specialised engineering and completion crews with specific unconventional expertise in Vaca Muerta's geological conditions

4. Commodity Price Risk

At $25 billion in capital expenditure, the project's internal rate of return is highly sensitive to long-term oil price assumptions. The specific breakeven Brent price for the project has not been publicly disclosed, but a sustained period of sub-$60/barrel pricing would materially compress project economics and could trigger capital allocation reviews. Consequently, monitoring the US oil production decline trajectory remains relevant context for understanding the global supply backdrop against which Vaca Muerta's export ramp will occur.

5. Environmental and Water Management Risk

Large-scale hydraulic fracturing in arid environments generates water sourcing and produced water management challenges that can generate both regulatory friction and community opposition. The Neuquén province's water governance framework and the specific conditions attached to environmental impact approvals will shape operational flexibility throughout the development lifecycle.

How Does This Investment Plan Fit Within YPF's Broader Corporate Strategy?

From Domestic Supplier to World-Class Unconventional Operator

The LLL Oil development submission signals a deliberate strategic repositioning. YPF is not merely seeking to increase production — it is structurally aligning its operational model with the integrated development playbook that defined the most cost-efficient Permian Basin operators during the North American shale revolution. According to Bloomberg's reporting on the RIGI application, the scale and structure of this submission represents a marked departure from prior incremental development approaches.

Strategic Parallels with Leading Unconventional Operators

- Shared infrastructure model: Reduces per-well capital costs through economies of scale across pad drilling programs, compressing development costs as the well count grows

- Logistics integration: Centralised water and sand supply systems lower variable operating costs per barrel below what isolated well-by-well development could achieve

- Plateau production targeting: Front-loading capital investment to achieve and sustain a defined production plateau optimises long-term free cash flow generation relative to a gradual ramp approach

The bifurcated export strategy — directing all crude to international markets while supplying associated gas domestically — reflects a sophisticated revenue optimisation structure. By capturing Brent-linked international pricing for oil while fulfilling domestic energy security obligations through gas, YPF maximises hard currency earnings without sacrificing the political viability of a project that requires sustained government support across multiple election cycles.

A subtle but important corporate strategy observation: the RIGI application positions YPF as a proof-of-concept operator for Argentina's investment framework itself. If the LLL Oil development executes on its stated timeline and economics, it establishes a template that international oil majors with existing or prospective Vaca Muerta positions — including TotalEnergies, Shell, and Chevron — could follow with their own integrated development submissions.

What Does This Mean for South America's Regional Energy Landscape?

Argentina's Emerging Role as a Continental Oil Export Hub

Comparative Regional Context

| Country | Primary Export Resource | Export Maturity | Key Constraint |

|---|---|---|---|

| Brazil | Deepwater pre-salt oil | Mature and growing | High offshore development costs |

| Colombia | Conventional onshore oil | Declining production | Reserve replacement challenges |

| Argentina (Vaca Muerta) | Unconventional shale oil | Early export phase | Infrastructure and financing |

| Venezuela | Heavy crude oil | Severely constrained | Sanctions and infrastructure decay |

A successful LLL Oil execution would materially shift Argentina's position within this regional hierarchy. The combination of Vaca Muerta's resource scale, improving fiscal stability, and export infrastructure development creates conditions under which Argentina could realistically challenge Brazil's regional dominance in oil exports within the following decade — though this outcome remains contingent on consistent execution across financing, infrastructure, and drilling milestones.

The less-discussed regional implication is the potential effect on Atlantic crude market pricing dynamics. Argentina's Medanito and Escalante crude grades, which are medium-gravity, relatively low-sulphur blends, compete in Atlantic Basin markets where European refinery configurations have a natural preference for these specifications. A sustained increase in Argentine export volumes of this grade could exert meaningful pricing pressure on competing Atlantic Basin crudes. Furthermore, shifts in global LNG supply patterns are already reordering how Atlantic Basin buyers approach long-term energy procurement, which may amplify Argentina's strategic relevance in the years ahead. This is particularly relevant as European refiners manage declining North Sea and West African supply reliability.

Frequently Asked Questions: YPF Vaca Muerta $25 Billion Investment Plan

What is the YPF LLL Oil development project?

The LLL Oil development is a US$25 billion unconventional oil project proposed by Argentina's state energy company YPF within the Vaca Muerta shale formation. The project involves drilling 1,152 wells over 15 years, targeting a production plateau of approximately 240,000 barrels of oil per day beginning in 2032, with all crude directed to international export markets.

What is the RIGI investment regime?

RIGI (Régimen de Incentivo para Grandes Inversiones) is Argentina's Large Investment Incentive Regime, a regulatory framework providing tax, customs, and foreign exchange benefits to qualifying large-scale investment projects. The YPF LLL Oil submission is the largest application filed under this programme to date, according to World Oil's reporting of the announcement.

When will the project reach full production?

YPF has targeted a production plateau of approximately 240,000 bopd beginning in 2032, subject to infrastructure development, financing completion, and regulatory approvals proceeding on schedule.

How much export revenue could the project generate?

At plateau production, YPF estimates the project could generate approximately US$6 billion in annual export revenues, representing a potentially transformative contribution to Argentina's foreign exchange earnings.

What infrastructure is required to export Vaca Muerta oil?

The project relies on the VMOS (Vaca Muerta Oil Sur) export pipeline and marine terminal system to transport crude from the formation to international shipping routes. Expansion of this infrastructure is a critical dependency for achieving stated production and export targets. Reuters' coverage of the RIGI submission provides additional detail on the regulatory milestones ahead.

Is Vaca Muerta comparable to US shale basins?

Vaca Muerta is widely regarded among petroleum geologists as one of the world's premier unconventional hydrocarbon formations, with geological characteristics — including exceptional formation thickness, high total organic carbon content, and rock quality consistency — that draw frequent technical comparisons to leading North American shale plays. In certain geological metrics, particularly formation thickness and TOC levels, it exceeds many of its North American counterparts.

The Path Forward: Execution Milestones That Will Define the Project's Success

A Timeline Framework for Monitoring LLL Oil Development Progress

Phase 1: Regulatory and Financing (2025–2027)

- RIGI application approval and fiscal stability certification

- Project financing syndication across international lenders and export credit agencies

- Environmental impact assessment completion and regulatory permitting

Phase 2: Infrastructure and Ramp-Up (2027–2030)

- VMOS pipeline and terminal capacity expansion to handle incremental export volumes

- Drilling rig and hydraulic fracturing spread mobilisation at scale

- Initial well pad construction and early production commencement

Phase 3: Plateau Acceleration (2030–2032)

- Drilling program intensification toward the 240,000 bopd target

- Full export logistics operationalisation through VMOS

- Domestic gas supply integration from associated production volumes

Phase 4: Sustained Production (2032 onwards)

- Plateau maintenance through infill drilling programs and well performance optimisation

- Ongoing infrastructure investment to sustain export volumes at target levels

- Potential expansion phases contingent on reservoir performance and prevailing market conditions

The YPF Vaca Muerta $25 billion investment plan represents one of the most consequential upstream commitments made anywhere in the world in the current decade. Whether it reshapes global shale oil markets as its proponents suggest depends ultimately on the convergence of geological quality, infrastructure execution, financing availability, and regulatory stability — four variables that have rarely aligned simultaneously in Argentine energy history. The degree to which they align this time will determine not just YPF's corporate trajectory, but Argentina's broader position in the global energy order for the coming generation.

Want to Track the Next Major Resource Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex resource data into clear, actionable investment insights — whether you're monitoring unconventional energy plays or major commodity finds. Explore how historic discoveries have generated substantial returns and begin your 14-day free trial to position yourself ahead of the broader market.