June 2, 2026

The Structural Forces Reshaping African Gold M&A Before a Single Bid Is Placed

Large-scale cross-border mining acquisitions have never been purely commercial transactions. Behind every headline valuation lies a complex architecture of sovereign approval mechanisms, geopolitical risk assessments, and commodity price timing that collectively determine whether a deal closes, collapses, or transforms into something unrecognisable from its original form. In the gold sector specifically, where asset values are directly tethered to a notoriously volatile commodity, the window between signing and closing can be the difference between a transformative deal and a regulatory cautionary tale.

The Zijin Gold International Allied Gold acquisition in Mali, a transaction initially framed as a landmark bet on African gold production, has since become a study in how quickly the economics of fixed-price commodity M&A can deteriorate. With China's National Development and Reform Commission (NDRC) raising formal concerns and the original deal deadline already lapsed, this transaction now sits at the intersection of commodity cycles, sovereign risk assessment, and China's evolving framework for governing outbound capital deployment. The broader gold M&A activity sweeping global markets makes the regulatory friction here all the more striking.

When big ASX news breaks, our subscribers know first

China's Regulatory Architecture and the Gatekeeping Function of the NDRC

How Beijing Evaluates Outbound Mining Investments

China's approach to large-scale outbound acquisitions is not simply bureaucratic process. The NDRC functions as a strategic filter, applying criteria that extend well beyond whether an acquisition price seems commercially reasonable at the time of signing. For mining deals of significant scale, regulators examine three interlocking dimensions: whether the valuation premium remains defensible relative to prevailing commodity prices at the time of approval, whether the host jurisdiction's political environment introduces systemic risk to Chinese capital, and whether the acquisition serves China's broader resource security objectives efficiently.

For Hong Kong-listed Chinese entities such as Zijin Gold International, this regulatory burden is compounded by a dual compliance framework. These companies must satisfy domestic Chinese regulatory requirements while simultaneously navigating international deal mechanics, shareholder obligations, and the disclosure norms of Hong Kong's equity markets. This dual exposure creates a structural vulnerability in deal timelines that purely Western or purely domestic Chinese acquisitions do not face to the same degree.

When Gold Prices Move Against a Fixed-Price Structure

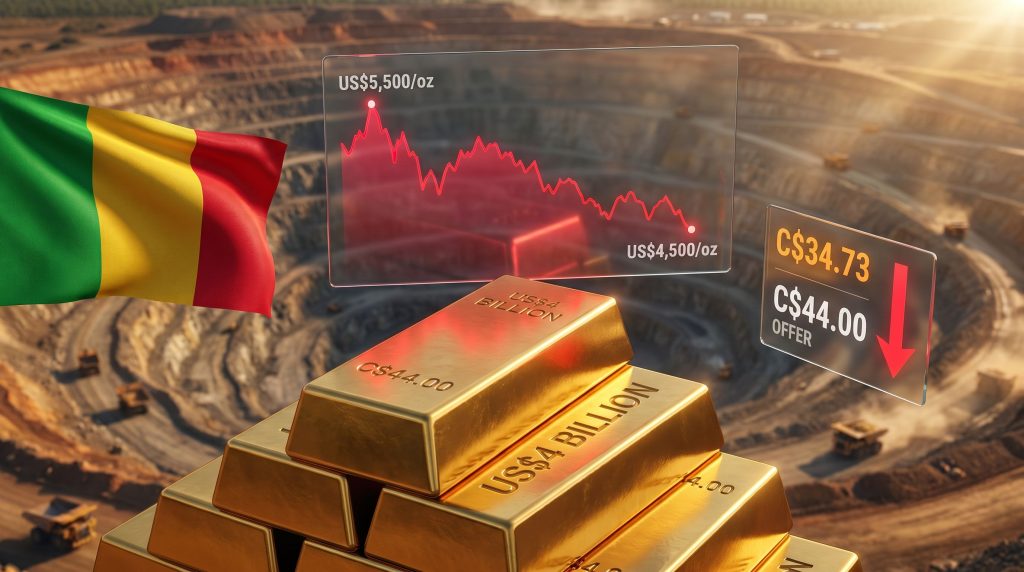

The NDRC's current concerns are crystallised by one particularly uncomfortable arithmetic reality. When the arrangement agreement was struck in January 2026, gold was trading above US$5,500 per ounce, near record highs that had been fuelling a wave of global mining M&A activity. By the time regulators began their substantive review, spot gold had corrected to approximately US$4,500 per ounce, representing a decline of roughly 18% from peak levels. Furthermore, the gold price impact on mining equities during this period added another layer of complexity to the valuation debate.

In commodity-linked M&A, a fixed-price acquisition structure that appears opportunistic at announcement can appear materially overpriced at the regulatory review stage if the underlying commodity has corrected sharply. This is not merely a financial observation; it is precisely the kind of risk calculus that informs how the NDRC assesses capital allocation prudence in outbound deals.

The implications for the C$44 per share all-cash offer, implying a total equity value of approximately C$5.5 billion (around US$4 billion), are significant. A premium that reflected the prevailing gold price environment at announcement now requires justification against a substantially lower commodity price backdrop. This is not a cosmetic concern for regulators whose mandate explicitly includes evaluating whether Chinese capital is being deployed at defensible valuations.

Understanding the Deal: Zijin Gold International, Allied Gold, and the Mali Question

Strategic Rationale and Asset Portfolio

The Zijin Gold International Allied Gold acquisition in Mali represents the Hong Kong-listed company's first major transaction since completing its IPO in late 2025. That context matters considerably. First deals post-listing carry disproportionate significance for investor confidence, management credibility, and the company's ability to access capital markets for future growth. A failed or heavily renegotiated inaugural acquisition would carry reputational consequences beyond the immediate financial impact.

Allied Gold's appeal as an acquisition target stems from a geographically diversified portfolio of producing and development assets across three African jurisdictions:

| Asset | Location | Operational Status | Strategic Role |

|---|---|---|---|

| Sadiola Mine | Mali | Producing (Phase 1 expansion complete) | Primary anchor asset and deal value driver |

| West African Operations | Côte d'Ivoire | Producing | Regional diversification |

| Kurmuk Project | Ethiopia | Development-stage | Long-term growth optionality |

Chinese mining groups have consistently demonstrated a preference for acquiring producing assets over greenfield developments in Africa. This preference is rational: producing mines eliminate exploration risk, compress the timeline between capital deployment and revenue generation, and provide immediate exposure to commodity price movements. For a company seeking to build gold production credibility quickly following its IPO, Allied's producing portfolio offered exactly this profile.

The Sadiola Mine: Understanding Why This Asset Anchors the Entire Transaction

Sadiola is not simply one asset among several in Allied Gold's portfolio; it is the operational and strategic centrepiece that underpins the entire commercial rationale for the acquisition. Situated in western Mali near the Senegalese border, Sadiola has a long production history and Allied Gold completed the first phase of its expansion programme prior to the deal announcement, meaning the mine enters the post-acquisition period with enhanced near-term production capacity rather than requiring further capital-intensive development work.

This distinction matters enormously in the context of acquisition due diligence and regulatory assessment. A producing asset with a recently completed expansion is a fundamentally different investment proposition from one requiring significant future capital deployment. The former offers more predictable cash flow modelling; the latter introduces execution risk that complicates valuation. Sadiola's position as a de-risked, producing, recently expanded asset made it a compelling anchor for any acquirer seeking immediate West African gold exposure.

Mali's status as Africa's third-largest gold producer provides the macro backdrop that makes Sadiola's geographic positioning significant. The country's established gold endowment, existing mining infrastructure, and proximity to other producing operations in the Birimian Greenstone Belt create network effects that enhance the value of assets within the jurisdiction, provided that jurisdiction remains operationally accessible.

Mali's Mining Jurisdiction: A Layered Risk Assessment

Security, Sovereignty, and the Interventionist State

Mali's risk profile for foreign mining investment cannot be adequately captured by a single risk category. It requires a layered analysis that distinguishes between security risk, governance risk, and what might be termed sovereign intervention risk, each of which operates on different timescales and affects investor calculations differently.

Security risk relates to the physical operating environment. Mali has experienced sustained violence from separatist and jihadist groups, particularly in its northern and central regions. While the Sadiola mine operates in western Mali, insurgency dynamics in the Sahel have demonstrated a capacity to shift and expand geographically in ways that were not anticipated even several years prior.

Governance risk relates to the stability and predictability of the regulatory and legal frameworks governing mining operations. Mali's military government, which came to power through a coup, has taken an increasingly interventionist approach to the country's extractive sector, treating resource sovereignty as a political instrument rather than simply an economic policy framework.

Sovereign intervention risk is where Mali's recent track record becomes most concerning for potential investors and, critically, for regulatory bodies evaluating whether Chinese capital should be exposed to this jurisdiction. The government's documented detention of foreign mining executives and its pursuit of forced contract renegotiations with major international operators, including Barrick Gold and Resolute Mining, signal a willingness to apply pressure directly to foreign corporate personnel and established contractual arrangements. These are not abstract policy risks; they are documented precedents with named counterparties. Indeed, the geopolitical mining risks present in the Sahel region have become a central theme in global mining investment discussions.

The distinction regulators draw between short-term operational disruption and long-term jurisdictional risk is critical. Operational disruptions can be managed through contingency planning. Jurisdictional risk, particularly the risk that a host government will detain personnel or unilaterally alter contractual terms, is structural and cannot be insured away through operational mitigation measures alone.

The Western Exit and the Chinese Entry: Understanding the Capital Flow Dynamic

The retreat of Western mining majors from elevated-risk African jurisdictions is not simply risk aversion. It reflects a complex interaction between shareholder ESG expectations, the increased cost of political risk insurance in frontier jurisdictions, and the governance requirements imposed by stock exchanges in London, Toronto, and New York that create liability exposure for boards operating in jurisdictions with documented human rights concerns.

This systematic Western retreat has created structural acquisition opportunities for Chinese mining groups, which operate under a different set of institutional constraints and which often calculate geopolitical risk premiums differently from their Western counterparts. Chinese state-linked capital has historically demonstrated a higher tolerance for jurisdictional complexity in exchange for securing strategic resource access.

Zijin Mining Group, the parent entity of Zijin Gold International, has already established a growing operational footprint across Mali, Côte d'Ivoire, and Ethiopia. The Zijin Mining expansion strategy signals that the parent company's leadership views African gold jurisdictions as central to its long-term growth thesis, even where those jurisdictions carry elevated risk profiles.

What the Market Is Saying About Deal Completion Probability

Decoding the Merger Arbitrage Spread

For investors unfamiliar with merger arbitrage dynamics, the gap between a target company's current trading price and the announced acquisition offer price functions as a real-time probability instrument. When a deal is announced at a premium and the market fully believes it will close on the stated terms, the target's share price will trade very close to the offer price, with only a small discount reflecting the time value of money and minor execution risk.

When that gap widens materially and persists over time, the market is communicating something specific: institutional investors with sophisticated deal assessment capabilities have concluded that the probability of deal completion on the original terms is meaningfully less than certain.

In the case of the Zijin Gold International Allied Gold acquisition in Mali, Allied's shares were trading at approximately C$34.73 against the C$44 per share offer price as of early June 2026. The arithmetic is direct: this represents a discount of roughly 21% to the acquisition price. For a deal that was initially presented as commercially compelling and strategically rational for both parties, a gap of this magnitude encodes significant market scepticism.

The fact that this discount persisted beyond the original May 29, 2026 arrangement agreement deadline without deal closure amplifies the signal. Deadlines in acquisition agreements are not merely administrative markers; they represent legally significant milestones. When a deadline passes without closure, it typically indicates that one or more approval conditions remain unresolved, and in this case, the acquisition delay appears to stem directly from unresolved NDRC regulatory clearance.

Three Scenarios and Their Market Implications

The current state of the transaction creates three distinct forward pathways, each carrying different implications for Allied Gold shareholders, Zijin Gold International's post-IPO credibility, and the broader market for Chinese mining M&A in Africa:

Scenario 1: Conditional Approval with Renegotiated Terms

The NDRC clears the transaction subject to a revised offer price that more closely reflects the post-correction gold price environment. Allied Gold shareholders receive less than the original C$44 headline figure, and the deal closes at a materially lower valuation. This outcome resets the M&A benchmark for African gold assets and may generate shareholder dissatisfaction at Allied's end, depending on how significant the price reduction is.

Scenario 2: Regulatory Rejection and Deal Collapse

The NDRC withholds approval entirely, citing the combination of an unjustifiable valuation premium relative to current gold prices and unacceptable geopolitical exposure in Mali. Allied Gold returns to the market as an independent operator, but given the Western retreat from high-risk African jurisdictions, the company may face a narrower field of credible alternative acquirers and potentially at lower valuations. Zijin Gold International's post-IPO growth strategy is consequently set back materially.

Scenario 3: Extended Review Under Amended Conditions

Both parties extend the arrangement agreement and continue pursuing regulatory approvals under modified terms. This scenario is partially supported by the statement from Allied's spokesperson confirming that both parties remain committed to closing, citing what is described as strong commercial logic underpinning the transaction. This is the scenario of prolonged uncertainty, where Allied's share price continues to trade at a discount and operational financing decisions become complicated by the unresolved strategic situation.

China's Broader African Resource Strategy and This Deal's Place Within It

The Architecture of Chinese Mining Expansion in Africa

Understanding this transaction requires situating it within a broader strategic framework. Chinese mining groups have systematically pursued producing African gold assets as a mechanism for building gold reserve exposure through M&A rather than relying exclusively on organic domestic production growth, which faces increasing geological and environmental constraints within China itself.

The preference for producing assets over greenfield developments reflects a calculated approach to risk management. Greenfield projects in high-risk jurisdictions require sustained capital deployment across multi-year timelines during which political conditions can change materially. Producing mines, by contrast, generate cash flow from day one and provide a platform from which to manage political relationships from a position of operational leverage rather than developmental dependency.

The structural distinction between Zijin Mining Group (the established parent entity with an existing African operational footprint) and Zijin Gold International (the Hong Kong-listed vehicle through which this acquisition is being pursued) deserves particular attention. Listing in Hong Kong creates both strategic flexibility and additional regulatory accountability. The flexibility comes from access to international capital markets and a deal-making currency that is more readily deployed in cross-border transactions. The accountability comes from Hong Kong's disclosure requirements and the NDRC oversight layer that applies specifically to outbound deals of this scale.

| Metric | Allied Gold Deal | Sector Context |

|---|---|---|

| Transaction Value | Among the largest Chinese mining acquisitions in Africa | |

| Offer Price Per Share | C$44.00 | Agreed January 26, 2026 |

| Current Market Price | ~C$34.73 | ~21% below offer price |

| Gold Price at Announcement | Above US$5,500/oz | Near record highs |

| Gold Price at Review | ~US$4,500/oz | ~18% correction from peak |

| Primary Jurisdiction Risk | Mali (military government, active conflict) | Elevated relative to peer African gold jurisdictions |

| Acquirer Structure | Hong Kong-listed vehicle | Creates dual regulatory compliance burden |

The next major ASX story will hit our subscribers first

Broader Implications for African Mining Investment Policy

The Signalling Effect Beyond This Transaction

The regulatory uncertainty surrounding this deal carries implications that extend well beyond the immediate parties. For Chinese mining groups evaluating other West African asset opportunities, the NDRC's scrutiny functions as a signal about the risk thresholds the regulator is prepared to accept. If NDRC hesitation creates a perception that deals in politically complex African jurisdictions face a higher bar for approval, it may reduce the pipeline of Chinese bids for African assets, at least in the near term.

For Mali specifically, the consequences of structural reluctance from Chinese capital would be significant. If the country's interventionist approach to its mining sector — including the detention of executives and forced contract renegotiations — creates a deterrent effect on both Western and Chinese investment simultaneously, the country faces a narrowing pool of credible foreign investors. The fiscal implications for a government heavily dependent on mining revenues would be material. The broader gold market outlook suggests that capital will flow to jurisdictions with more stable governance frameworks if this pattern continues.

Governance Gaps in Cross-Border Mining M&A

One of the most consequential and underexamined dimensions of deals like this is the absence of a standardised international framework for evaluating geopolitical risk in cross-border mining acquisitions. Unlike financial services M&A, where regulatory equivalence frameworks and bilateral agreements provide a reasonably structured environment for cross-border transactions, mining M&A in frontier jurisdictions operates in a space where legal protections can be thin, enforcement mechanisms unreliable, and bilateral investment treaty coverage incomplete.

The legal protections available to Chinese investors in Mali are shaped by whatever bilateral frameworks exist between China and Mali, as well as by the terms of Mali's own mining code, which the military government has demonstrated a willingness to revisit. This structural vulnerability is precisely what sophisticated regulatory bodies like the NDRC are paid to assess. The concern is not hypothetical; it is grounded in recent documented precedents involving other Chinese mining entities in similarly structured jurisdictions.

Frequently Asked Questions

What is the Zijin Gold International Allied Gold acquisition in Mali?

Zijin Gold International, a Hong Kong-listed Chinese gold mining company that completed its IPO in late 2025, agreed in January 2026 to acquire Allied Gold through an all-cash offer priced at C$44 per share. The total implied equity value of the transaction is approximately C$5.5 billion, equivalent to around US$4 billion. Allied Gold's principal assets include the producing Sadiola mine in Mali, producing operations in Côte d'Ivoire, and the development-stage Kurmuk project in Ethiopia.

Why is China's NDRC reviewing the deal?

China's National Development and Reform Commission, which oversees large outbound investment approvals, has raised concerns focused on two primary areas. The first is whether the acquisition price remains defensible given that gold has declined approximately 18% from above US$5,500 per ounce at deal signing to around US$4,500 per ounce during the review period. The second is whether Mali's security environment and the military government's track record of interventions in the mining sector introduce an unacceptable level of geopolitical risk for Chinese capital.

Why is the Sadiola mine so important to this deal?

The Sadiola mine is the primary producing asset in Allied Gold's portfolio and the strategic anchor of the acquisition's commercial rationale. Allied Gold completed the first phase of the mine's expansion programme prior to the deal announcement, meaning the asset offers near-term production upside without requiring further capital-intensive development. This de-risked producing profile made it particularly attractive to a Chinese acquirer seeking immediate West African gold exposure.

What does the share price gap tell investors?

Allied Gold's shares were trading at approximately C$34.73 as of early June 2026, representing a discount of roughly 21% to the C$44 offer price. In merger arbitrage terms, this gap reflects the market's probabilistic assessment of deal completion risk. A persistent discount of this magnitude, particularly following the lapse of the original May 29, 2026 deadline, signals that institutional investors with deal assessment expertise are pricing in a meaningful probability that the transaction will not close on original terms.

What happens if the deal collapses?

If NDRC approval is withheld and the acquisition falls through, Allied Gold would return to the market as an independent operator. Given the systematic retreat of Western mining companies from high-risk African jurisdictions, the company may face a narrower field of credible alternative acquirers and potentially at valuations below the Zijin offer price. The operational and financing uncertainty associated with a prolonged unresolved acquisition process could also weigh on the company's near-term strategic planning.

Is Mali a viable jurisdiction for long-term mining investment?

Mali presents a complex risk profile that combines genuine geological endowment, as evidenced by its status as Africa's third-largest gold producer, with an elevated and deteriorating governance environment. The military government's documented interventions in the sector, including detaining foreign executives and pursuing forced renegotiations with established international operators, represent structural rather than temporary risks. Whether this makes Mali unviable or simply higher-risk is a judgement that different investors and regulators are currently reaching different conclusions about.

What This Transaction Reveals About the Future of African Gold M&A

The Zijin Gold International Allied Gold acquisition in Mali has evolved from a straightforward narrative about Chinese expansion into African gold into a multidimensional case study in the limits of fixed-price M&A structures in volatile commodity markets, the evolving sophistication of Chinese regulatory risk assessment, and the structural consequences of governance deterioration in resource-rich African states.

Several conclusions emerge from a careful analysis of this situation:

- The NDRC's scrutiny signals that Chinese regulators are applying increasingly granular risk filters to outbound mining deals, moving beyond capital quantum to evaluate valuation integrity against current commodity prices and jurisdictional geopolitical profiles simultaneously.

- A commodity price correction of approximately 18% between deal signing and regulatory review is sufficient to materially alter the financial logic of a fixed-price acquisition, demonstrating a structural vulnerability in commodity M&A timing that acquirers and their advisers must plan for explicitly.

- Mali's combination of active conflict zones, military governance, and a documented pattern of contract renegotiation and executive detention represents one of the most complex jurisdiction risk profiles in Sub-Saharan Africa for foreign mining capital.

- The 21% gap between Allied Gold's market price and the Zijin offer price, persisting beyond the original deal deadline, encodes the market's real-time assessment of completion probability in a form that is more reliable than any single analyst's opinion.

- Regardless of whether this deal ultimately closes, it is reshaping how Chinese mining capital evaluates African jurisdictions and how African governments must consider the consequences of resource nationalism on their ability to attract the foreign investment their mining sectors require.

Disclaimer: This article is intended for informational and educational purposes only and does not constitute financial or investment advice. The scenarios, projections, and analyses presented are based on publicly available information and should not be relied upon as the basis for any investment decision. Readers should conduct their own due diligence and consult qualified financial advisers before making investment decisions. Past performance and historical precedents are not guarantees of future outcomes.

Want to Stay Ahead of the Next Major African Gold Discovery Before the Market Catches On?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries the moment they hit the exchange, transforming complex geological and commodity data into actionable insights — explore historic discoveries and their exceptional returns to understand the potential, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.