August 11, 2026

When Underground Wealth Becomes Above-Ground Capital: Zimbabwe's Resource-Financing Gambit

Across Sub-Saharan Africa, a quiet but consequential financing revolution has been unfolding for over a decade. Nations rich in mineral endowments but starved of capital have increasingly turned to a model that trades future resource revenues for present-day infrastructure construction. The logic is seductive: why borrow against uncertain fiscal surpluses when the ground beneath your feet holds billions in extractable value? Zimbabwe minerals-backed deals with China to fund infrastructure are now positioning the country at the centre of this debate, and the stakes extend well beyond its borders.

When big ASX news breaks, our subscribers know first

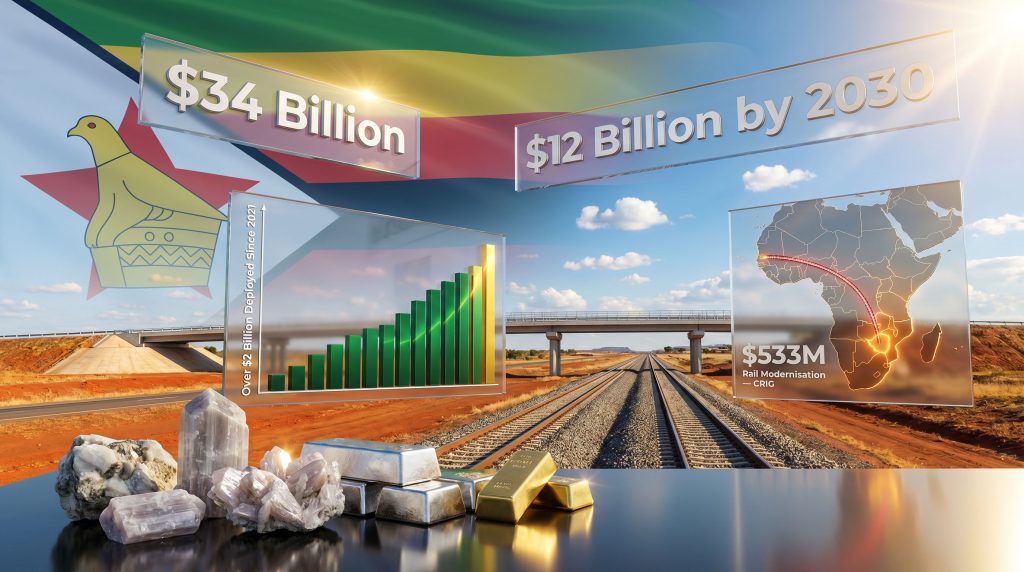

Zimbabwe's $34 Billion Infrastructure Problem and Why Minerals Are the Answer

Zimbabwe's infrastructure deficit is not a minor operational inconvenience. The African Development Bank estimates the country needs approximately $34 billion to modernise its transport and logistics networks, a figure that dwarfs the nation's fiscal capacity under any conventional borrowing scenario. Decades of economic mismanagement, currency crises, and political instability have left roads impassable, rail corridors dormant, and export capacity severely constrained.

The arithmetic is stark. A country sitting atop world-class deposits of lithium, chrome, platinum group metals, and gold cannot efficiently monetise those deposits when the physical infrastructure to move them barely functions. This is the structural bind that makes resource-backed financing so compelling for Harare's policymakers.

Zimbabwe's Finance, Economic Development and Investment Promotion Minister Mthuli Ncube opened formal discussions with China Railway International Group (CRIG) on the sidelines of the World Economic Forum in Dalian, signalling that Harare is actively pursuing what are termed resource-linked debt instruments. Under these arrangements, future revenues generated from natural resource extraction are pledged as collateral against infrastructure loans tied to specific projects.

How Resource-Linked Debt Instruments Actually Function

The mechanics of resource-backed financing differ substantially from conventional sovereign debt. Rather than relying on a government's general creditworthiness and fiscal position, these structures use a defined revenue stream, typically commodity export earnings, as the repayment mechanism.

The structure requires determining several interdependent variables:

- Which infrastructure project is being financed and its total cost

- What toll fees or usage revenues the completed infrastructure will generate

- How large the gap is between those toll revenues and the total loan obligation

- Which mineral resource stream will fill that repayment gap

- What commodity price assumptions underpin the revenue projections

| Feature | Traditional Sovereign Debt | Resource-Backed Financing |

|---|---|---|

| Collateral | Government creditworthiness | Future mineral revenues |

| Repayment trigger | Fixed schedule | Revenue-linked milestones |

| Risk exposure | Currency and fiscal risk | Commodity price volatility |

| Lender security | Sovereign guarantee | Physical resource stream |

| Precedent example | IMF/World Bank loans | DRC-China Sicomines deal |

The critical insight here is that the lender, typically a Chinese state-linked entity, effectively gains a secured claim against a sovereign nation's mineral wealth. The borrower gains infrastructure it could not otherwise finance. Both sides carry asymmetric risks that are rarely made fully transparent at the time of signing.

The DRC Blueprint: Sicomines and the Model Zimbabwe Is Studying

The most extensively documented precedent for this type of arrangement in Africa is the Democratic Republic of Congo's minerals-for-infrastructure deal structured around the Sicomines joint venture, valued at approximately $7 billion. Under this framework, Chinese state-linked companies gained access to the DRC's copper and cobalt resources through a joint venture, with infrastructure commitments covering roads, hospitals, and schools forming the development component of the deal.

Zimbabwe's finance leadership has explicitly referenced this structure as a guide for its own negotiations with CRIG. The parallels are instructive. Both countries hold globally significant deposits of battery-critical minerals. Both face infrastructure deficits that conventional multilateral financing has failed to address at the required scale. Furthermore, in both cases, Chinese companies had already established a dominant operational presence before the infrastructure financing conversations began.

However, the Sicomines model is not without controversy. Key concerns that have emerged over time include:

- Renegotiation difficulties when commodity prices underperform initial projections

- Limited transparency in the original contract terms

- Questions about whether the infrastructure delivered matched the value of resources extracted

- Constraints on future policy flexibility for subsequent governments

For Zimbabwe, studying where the DRC arrangement succeeded and where it created long-term frictions is not merely academic. It is the foundational due diligence for any comparable deal. Indeed, the ongoing Zimbabwe mining debt dispute underscores just how consequential these negotiations can be for the country's long-term financial standing.

China's Dominant Position in Zimbabwe's Extractive Economy

Understanding why Zimbabwe is negotiating primarily with Chinese counterparts requires appreciating the depth of investment Beijing has already deployed in the country's mining sector. Chinese firms have invested over $2 billion in Zimbabwe's lithium sector alone since 2021, establishing a level of operational control that makes Chinese participation in any infrastructure financing arrangement the path of least resistance, commercially if not politically.

| Company | Sector | Investment Activity |

|---|---|---|

| Sinomine Resource Group | Lithium | Bikita mine operations; lithium refinery under development |

| Zhejiang Huayou Cobalt | Lithium processing | Commissioned lithium sulphate processing plant |

| China Railway International Group (CRIG) | Rail infrastructure | $533 million rail modernisation agreement |

| JinAn Group | Chrome and energy | Solar plant investment to power chrome operations |

This concentration creates both leverage and dependency. Chinese mining firms have a direct commercial interest in functional Zimbabwean rail because their own mineral output depends on it. This alignment of interests is one reason why the $533 million rail modernisation deal with CRIG carries credibility as a commercial proposition, not merely a diplomatic gesture.

Why Rail Revival Is as Much Beijing's Problem as Harare's

Zimbabwe's rail network is the arterial system through which Chinese-controlled mineral production reaches port. A dormant or degraded rail corridor is not simply an inconvenience for Zimbabwean state planners. It is a direct constraint on the return profile of billions in Chinese private and state-linked mining investment.

Projections associated with the rail modernisation scope suggest a potential 30% reduction in mineral transport times and an export efficiency improvement of 25 to 30%. For high-volume commodities like lithium concentrate and chrome ore, those efficiency gains translate directly into margin improvement and competitive positioning in global supply chains.

Zimbabwe's $12 Billion Mining Revenue Target by 2030

Against the backdrop of this infrastructure push, Zimbabwe has articulated an ambitious revenue target: $12 billion in annual mining revenues by 2030. Assessing the feasibility of this target requires examining the baseline, the commodity mix, and the infrastructure prerequisites.

The minerals most likely to drive growth toward this target include:

- Lithium — Zimbabwe holds some of the world's highest-grade hard-rock lithium deposits, and the global lithium market creates structural demand driven by EV battery supply chains

- Platinum group metals — The Great Dyke geological formation hosts world-class PGM resources with significant unexploited depth

- Gold — Historically Zimbabwe's largest mining export earner, with artisanal and large-scale production both contributing

- Chrome — A major existing export commodity with Chinese smelting partnerships already operational

The critical variable, however, is infrastructure. Without functional rail to export terminals and roads capable of sustaining heavy haulage, the volume growth required to reach $12 billion annually simply cannot materialise. This creates a circular dependency: the revenue target requires infrastructure, and the infrastructure financing relies on projected revenues from the very target it is meant to enable.

Analysts have noted this circularity creates a sequencing risk. If commodity prices decline materially before infrastructure is operational, repayment models built on resource revenue projections can unravel rapidly, as several African resource-backed deals from the 2010s demonstrated.

The Lithium Export Ban: Beneficiation Policy Meets Commercial Reality

Separately from the infrastructure financing discussions, Zimbabwe has confirmed that a ban on the export of unprocessed lithium concentrate will proceed as scheduled, taking effect in January 2027, despite sustained pressure from industry operators requesting a delay.

This policy decision reflects a broader economic philosophy: raw material export without domestic value addition transfers the bulk of economic value to importing nations. By forcing processing onshore, Zimbabwe is attempting to capture a larger share of the lithium value chain before material leaves its borders.

The processing infrastructure currently in place or under development includes:

- Zhejiang Huayou Cobalt lithium sulphate processing plant: now operational

- Sinomine at Bikita mine secondary processing facility: currently under active development

- Sinomine planned lithium refinery: approximately $500 million committed investment in planned construction phase

How the Export Ban Reshapes Chinese Operator Economics

For Chinese firms that have invested heavily in Zimbabwean lithium extraction, the export ban is a forced pivot in business model. Companies that were exporting spodumene concentrate for processing in China must now either build or utilise local processing capacity. This is commercially disruptive in the short term but aligns with Harare's beneficiation agenda.

Lithium sulphate, the intermediate product produced by Huayou Cobalt's plant, represents a step up the value chain from raw spodumene, but remains well short of battery-grade lithium hydroxide or lithium carbonate. The strategic question is whether Zimbabwe can attract the downstream refining investment needed to progress further along the value chain, or whether it remains locked at the intermediate processing stage while the highest-value refining continues to occur in China.

Compared to other African resource nations pursuing beneficiation mandates, Zimbabwe's approach is relatively firm. Guinea's bauxite-to-alumina push and the DRC's cobalt processing ambitions have both encountered execution gaps between policy aspiration and industrial reality. Zimbabwe's advantage is that the Chinese operators with whom it is negotiating already have the processing technology and capital to build the required facilities. Consequently, advances in lithium extraction technology may further shape how this processing landscape evolves in coming years.

The next major ASX story will hit our subscribers first

Structural Risks Investors and Policymakers Must Weigh

Zimbabwe minerals-backed deals with China to fund infrastructure are not financial instruments without meaningful downside scenarios. The risks are structural, not merely operational.

Commodity price volatility sits at the top of the risk register. The lithium market downturn has already demonstrated extraordinary cyclicality, with prices collapsing by over 80% from peak levels in 2022 to 2024 as battery supply chains overbuilt inventory. A repayment model calibrated to 2022 lithium prices would have collapsed under 2024 market conditions.

Sovereignty constraints represent a second-order risk that manifests over longer time horizons. When a nation pledges future mineral revenues as collateral, subsequent governments inherit obligations that may constrain their policy options. Renegotiating resource-backed deals is politically and legally complex, particularly when the counterparty is a state-linked Chinese enterprise operating under different legal norms.

Labour and environmental governance in Chinese-operated African mines has been the subject of documented concerns across multiple jurisdictions. Zimbabwe is not immune to these dynamics, and the long-term social licence for these operations depends on how seriously governance standards are enforced domestically.

Africa's Minerals-for-Infrastructure Landscape: A Regional Comparison

| Country | Resource Pledged | Infrastructure Target | Chinese Partner | Deal Value |

|---|---|---|---|---|

| DRC | Copper and cobalt | Roads, hospitals, schools | Sicomines JV | ~$7 billion |

| Zimbabwe (proposed) | Lithium and other minerals | Roads and rail | CRIG | Under negotiation |

| Angola | Oil | General infrastructure | Multiple SOEs | Multi-billion |

| Guinea | Bauxite | Rail and port | SMB-Winning Consortium | ~$14 billion |

Zimbabwe's negotiating position differs from several of these precedents in one meaningful respect. The Chinese firms most motivated to see infrastructure built are already operating inside the country and have invested capital that is currently constrained by the absence of that infrastructure. This creates a genuine alignment of commercial interests that arguably gives Harare more negotiating leverage than Angola or Guinea held at equivalent stages of their own processes.

Frequently Asked Questions: Zimbabwe's Minerals-for-Infrastructure Strategy

What minerals is Zimbabwe pledging in these deals with China?

Discussions centre primarily on lithium given its dominant role in Chinese investment activity, though the broader mineral endowment including chrome, gold, and platinum group metals forms part of Zimbabwe's negotiating portfolio.

Is Zimbabwe at risk of losing sovereign control over its mineral assets?

Resource-backed financing does not transfer ownership of mineral assets. It pledges future revenue streams. However, if commodity prices fall dramatically and revenues fail to service debt, renegotiation or enforcement actions could create de facto constraints on how those assets are managed.

How does the lithium export ban affect Chinese companies operating in Zimbabwe?

Companies currently exporting raw concentrate must redirect that material to local processing facilities. This accelerates the need for domestic refining capacity and has been a key driver of Sinomine's planned $500 million refinery investment. In addition, rising critical minerals demand globally means the pressure to establish local processing will only intensify.

What is the timeline for Zimbabwe's infrastructure development under these arrangements?

Formal negotiations are at an early stage. The discussions between Ncube and CRIG at Dalian represent exploratory conversations rather than concluded agreements. Infrastructure delivery timelines will depend on the speed at which deal terms are finalised and financing instruments are structured.

Key Data Summary

| Metric | Figure |

|---|---|

| Estimated infrastructure upgrade cost | ~$34 billion |

| Chinese investment in lithium sector since 2021 | Over $2 billion |

| Rail modernisation deal with CRIG | $533 million |

| Projected mineral transport time reduction | Up to 30% |

| Export efficiency improvement target | 25 to 30% |

| Zimbabwe's 2030 mining revenue target | $12 billion |

| Lithium concentrate export ban effective date | January 2027 |

| DRC Sicomines precedent deal value | ~$7 billion |

| Sinomine planned lithium refinery investment | ~$500 million |

The Geopolitical Dimension: What Western Capitals Are Watching

Zimbabwe minerals-backed deals with China to fund infrastructure do not occur in a geopolitical vacuum. Western governments and multilateral institutions are acutely aware that Chinese consolidation of African critical mineral supply chains carries strategic implications for electric vehicle battery supply security, defence technology inputs, and clean energy transition timelines.

The minerals that underpin Zimbabwe's resource-backed financing discussions, lithium foremost among them, sit at the heart of the global energy transition. A supply chain in which Chinese-controlled entities mine, process, and export the bulk of Zimbabwe's lithium output represents a concentration of strategic commodity control that has prompted policy responses from Washington, Brussels, and Canberra.

Whether Zimbabwe can attract credible alternative financing partners from Western-aligned nations remains an open question. The competitive disadvantage for non-Chinese partners is significant: they lack the existing operational presence, the integrated processing capability, and the state-backed risk tolerance that allows Chinese entities to underwrite complex resource-backed arrangements in frontier markets.

For Zimbabwe's policymakers, the immediate priority is securing the infrastructure capital its economy urgently requires. The longer-term challenge is ensuring that the terms under which that capital is obtained do not foreclose the country's options in a mineral landscape whose strategic importance is only likely to grow.

Disclaimer: This article contains forward-looking projections, including Zimbabwe's 2030 mining revenue target and infrastructure financing timelines. These projections are subject to commodity price movements, geopolitical developments, and execution risks. Nothing in this article constitutes financial or investment advice. Readers should conduct independent research before making any investment decisions.

Want To Track The Next Major Mineral Discovery Before The Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across lithium, gold, platinum group metals, and over 30 other commodities — instantly turning complex geological announcements into actionable investment insights. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.