July 14, 2026

Engineering a Commodity Pivot: Inside the ACG Metals Gediktepe Sulphide Expansion Project

Brownfield mining conversions occupy a unique and frequently underappreciated corner of the capital markets landscape. Unlike greenfield developments that begin from scratch with uncertain geology and unproven infrastructure, brownfield expansions inherit existing site infrastructure, established permitting frameworks, and operational workforce knowledge. Yet the engineering complexity of converting a gold-silver doré producer into a copper-zinc concentrate operation is anything but straightforward. It demands a complete reimagining of the processing circuit, a recalibration of revenue streams, and a financing structure robust enough to sustain the transition period. The ACG Metals Gediktepe Sulphide Expansion Project in Western Türkiye is a live case study in executing this kind of transformation with measurable discipline.

When big ASX news breaks, our subscribers know first

What Is the ACG Metals Gediktepe Sulphide Expansion Project?

From Gold Producer to Copper-Zinc Concentrate Manufacturer

The Gediktepe mine sits in Western Türkiye and has operated through two structurally distinct phases. The first phase processed oxide ore to produce gold and silver doré, a relatively straightforward heap leach or vat leach operation. Oxide mining concluded at the end of 2025, transitioning the site into a stockpile-processing mode for gold equivalent production while the far more complex sulphide expansion takes shape around it.

The sulphide ore body beneath and adjacent to the depleted oxide zone carries an initial mine life of 11 years, representing a fundamental extension of the asset's productive life. Critically, the sulphide resource shifts the commodity profile entirely, replacing precious metal doré with copper concentrate and zinc concentrate as the primary revenue drivers. Gold and silver become byproduct credits rather than primary outputs, expected to contribute approximately 15,000 to 20,000 ounces of gold annually through the copper concentrate stream.

This transition is more than a processing change. It repositions ACG Metals' revenue correlation away from precious metal spot price sensitivity and toward industrial demand dynamics linked to electrification infrastructure, construction activity, and manufacturing cycles. Furthermore, the broader copper supply crunch creates a compelling backdrop for new production entering the market at this scale.

Project Snapshot: Key Parameters at a Glance

| Parameter | Detail |

|---|---|

| Project Type | Brownfield EPC Sulphide Expansion |

| Location | Western Türkiye |

| EPC Contractor | GAP İnşaat (subsidiary of Çalık Holding) |

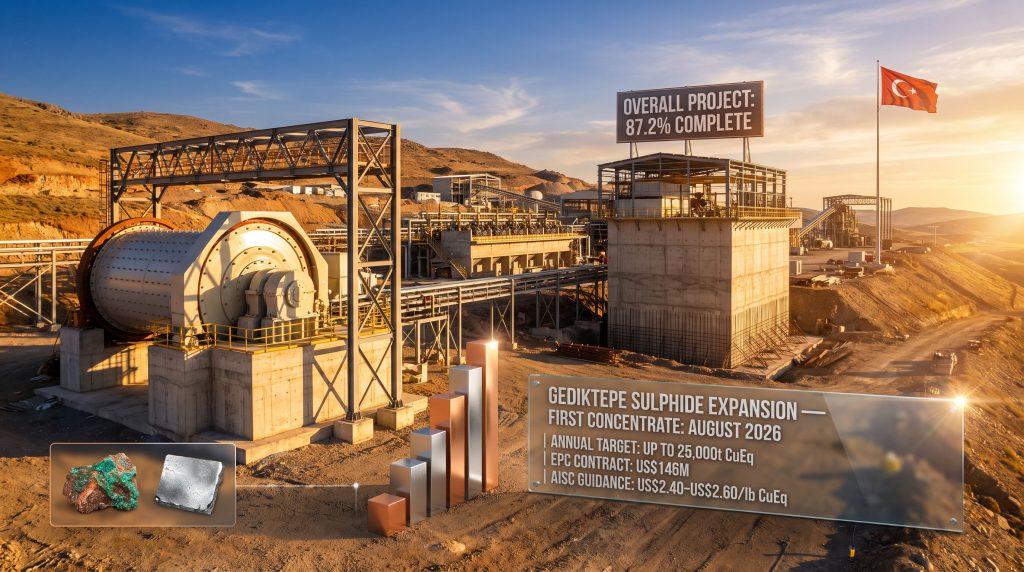

| Fixed-Price Contract Value | US$145–146 million |

| Primary Funding Mechanism | US$200 million senior secured bond (December 2024) + oxide phase cash flows |

| Annual Production Target | Up to 25,000 tonnes copper equivalent per year |

| Initial Mine Life | 11 years |

| Output Commodities | Copper concentrate, zinc concentrate; gold and silver as byproducts |

| First Concentrate Production | August 2026 |

| Full-Year 2026 Guidance | 20,000–22,000 kt CuEq |

How Is the Gediktepe Sulphide Expansion Being Financed?

Fixed-Price EPC Contracts: A Critical Risk Transfer Mechanism

One of the least discussed but most consequential decisions in large-scale mining project development is the choice of contract structure between project owner and construction contractor. Fixed-price turnkey Engineering, Procurement, and Construction contracts transfer the risk of cost overruns directly to the contractor. If material costs rise, labour becomes scarce, or construction timelines slip due to factors within the contractor's control, the financial exposure falls on GAP İnşaat rather than ACG Metals.

This is a materially different risk profile compared to cost-reimbursable contracts, where every additional dollar of construction expense flows directly back to the project owner. In an era of persistent global construction inflation, the fixed-price structure at Gediktepe represents a meaningful form of capital discipline. GAP İnşaat, as a subsidiary of the diversified Çalık Holding conglomerate, carries the financial depth to absorb this contractual risk credibly. The EPC contract details confirm the fixed-price terms that underpin this risk transfer arrangement.

Capital Deployment Timeline and Bond Structure

As of 30 June 2026, approximately US$101 million of the total US$146 million project capital expenditure had been deployed, representing roughly 69% of committed capital, with an estimated US$45 million in remaining expenditure to complete the build.

The US$200 million senior secured bond issued in December 2024 was sized deliberately above the EPC contract value to cover not just construction costs but also working capital requirements during the transition period between oxide wind-down and sulphide commissioning. This pre-funding approach avoids the scenario where a cash shortfall during construction forces unfavourable emergency financing.

Oxide phase cash flows have served as a supplementary funding bridge throughout H1 2026. The combination of bond proceeds and ongoing oxide revenue from stockpile processing has reduced the need for additional debt drawdowns during the most capital-intensive construction phase.

Liquidity Position as of Mid-2026

The balance sheet as of 30 June 2026 reflects a project in the final stages of capital deployment:

- Net debt: approximately US$140 million

- Cash balance: approximately US$60 million

- Restricted cash component: US$28 million (earmarked for specific obligations, reducing freely available liquidity)

The restricted cash designation is a detail worth understanding. In project finance structures, restricted cash is typically held in reserve accounts tied to bond covenants, debt service requirements, or environmental rehabilitation obligations. It cannot be freely deployed for operational purposes, which means the effectively available cash position is closer to US$32 million. This is a standard feature of high-yield project bond structures rather than a sign of financial stress, but it is relevant context for assessing near-term operational liquidity as commissioning costs accumulate.

Engineering Milestones: What Has Actually Been Built?

Civil and Structural Construction Progress

Concrete works across the site had reached 86% completion of the total civil scope as of mid-2026. For a sulphide flotation plant of this scale, concrete represents the foundational infrastructure upon which all mechanical equipment is mounted. Rebar placement at fine ore bin foundations in mid-2025 was an early structural indicator, signalling the transition from earthworks and groundwork into above-ground construction momentum.

The progression from civil works to structural steel placement is a critical sequencing milestone in EPC construction. Once structural steel is erected and grouted into concrete foundations, the pace of mechanical installation can accelerate significantly, as equipment can be lifted and positioned using structural frames rather than relying entirely on temporary rigging systems.

Equipment Delivery and Installation

By 30 June 2026, all major process equipment had been delivered to the Gediktepe site. This logistical milestone materially de-risks the commissioning timeline, eliminating supply chain delay as a variable in the August 2026 first production target.

The significance of this cannot be overstated. Global supply chains for large-scale mining process equipment remain constrained in 2026, with SAG mills, ball mills, and flotation cells frequently carrying lead times of 18 to 24 months from order placement to delivery. The fact that all long-lead items arrived on site as planned reflects either exceptional procurement planning or favourable supplier relationships, or both.

The SAG (Semi-Autogenous Grinding) mill and ball mill are the most capital-intensive individual line items in a sulphide flotation circuit. These grinding mills reduce ore particle size to a fineness suitable for flotation chemistry to separate copper and zinc minerals from waste rock. Their foundation seating represents a critical path predecessor to mechanical completion and dry commissioning.

Engineering, Procurement, and Construction Completion Rates

| Workstream | Completion Rate (Dec 2025) | Completion Rate (Jun 2026) |

|---|---|---|

| Engineering | 68% | Near complete |

| Procurement | 66% | Complete (all equipment delivered) |

| Construction | 37% | Approaching completion |

| Overall Project | ~55% (implied) | 87.2% |

The acceleration in construction completion rates between December 2025 and June 2026 is particularly notable. Moving from 37% construction completion to an overall project status of 87.2% across just six months indicates a significant ramp-up in on-site labour activity and installation rates. This kind of construction acceleration is characteristic of the late-stage EPC build, when civil and structural prerequisites unlock simultaneous mechanical installation across multiple workstreams. According to recent project updates, the project has consistently tracked toward its H1 2026 production milestones.

How Does the Sulphide Expansion Change ACG Metals' Production and Revenue Profile?

Oxide Wind-Down and Stockpile Processing

Oxide mining concluded at Gediktepe at the end of 2025. All gold equivalent production in H1 2026 came entirely from processing stockpiled oxide ore. This distinction matters for understanding the H1 2026 production figure of 18,487 oz AuEq, which not only exceeded the full-year oxide target of 17,500 oz AuEq in just six months but did so without any fresh mining activity.

Approximately 2,500 oz AuEq of additional production is expected through the remainder of 2026 from continued oxide stockpile and residual material processing. Beyond that, the oxide contribution to ACG Metals' production profile effectively disappears, replaced entirely by sulphide concentrate output. In this context, understanding the copper price growth drivers that will underpin future revenue becomes essential for evaluating the project's long-term value proposition.

Selling Concentrates vs. Selling Doré: A Fundamentally Different Commercial Model

A lesser-known but commercially significant dimension of this transition involves the mechanics of how each product is sold. Gold and silver doré is a partially refined precious metal product that is sold directly to refineries with relatively simple pricing based on spot prices minus refining fees. Copper and zinc concentrates, however, operate under an entirely different commercial framework:

- Treatment Charges (TC): Smelters charge a per-tonne fee to process concentrate into refined metal

- Refining Charges (RC): An additional per-unit fee for electrolytic refining

- Payability Terms: Smelters typically pay for only a percentage of the contained metal (commonly 96–97% for copper)

- Penalty Elements: Concentrate containing impurities such as arsenic, bismuth, or fluorine attracts price deductions

- Price Participation: Some smelter contracts include price sharing provisions where the producer receives a portion of the upside when metal prices exceed specified thresholds

This commercial complexity means that realised copper prices in concentrate are always below the LME copper spot price by a margin that varies with TC/RC rates, which themselves fluctuate with global smelter capacity utilisation. Understanding payability terms is essential for accurately modelling Gediktepe's future revenue.

Full-Year 2026 Production Guidance

| Metric | Guidance Range |

|---|---|

| Total Production | 20,000–22,000 kt CuEq |

| AISC | US$2.40–US$2.60 per pound CuEq |

| First Concentrate Production | August 2026 |

| Production Basis | Combined oxide stockpile output + sulphide concentrate (H2 2026) |

H1 2026 Financial Performance: Unpacking the Numbers

Commodity Price Tailwinds and Revenue Amplification

| Commodity | H1 2025 Realised Price | H1 2026 Realised Price | Change |

|---|---|---|---|

| Gold | ~US$2,950/oz (implied) | US$4,838/oz | +64% |

| Silver | ~US$32.3/oz (implied) | US$78.2/oz | +142% |

Precious metal prices at these levels represent a historically elevated pricing environment. Gold above US$4,800 per ounce and silver above US$78 per ounce significantly amplify revenue from even modest production volumes. The H1 2026 oxide production of 18,487 oz AuEq, while operationally modest, generated substantial revenue precisely because of this pricing backdrop.

However, the fiscal architecture at Gediktepe includes royalty obligations that scale with realised prices. Higher gold and silver prices triggered elevated royalty payments, partially offsetting the revenue benefit of the price environment. This is a structural feature of royalty-linked fiscal regimes common in Türkiye and many other mining jurisdictions, where the state captures additional economic rent when commodity prices are elevated.

Why the 52% AISC Increase Is Structurally Misleading

AISC rising to US$1,609 per ounce in H1 2026 requires careful contextualisation. Three compounding factors drove this increase:

- Royalty escalation directly linked to higher gold and silver realised prices

- Lower production volumes relative to H1 2025, as oxide mining had ceased and only stockpile processing was underway, spreading fixed costs across fewer ounces

- Elevated site workforce levels during the peak labour intensity of sulphide construction activity

AISC metrics calculated during an operational transition period are structurally unrepresentative of steady-state operating costs. Once sulphide production commences at scale, the cost basis shifts to a per-pound CuEq framework with a guided range of US$2.40 to US$2.60 per pound, a figure that will reflect the genuine economics of the sulphide operation rather than the distorted cost structure of the transition period.

Investors and analysts should apply particular caution to year-on-year cost comparisons during transition periods, as the denominators (ounces produced, pounds produced) and the cost bases change simultaneously, making direct comparisons misleading without adjustment.

Safety Performance in Context

The project-to-date Lost Time Injury Frequency rate of 2.9 per million man-hours was achieved during the most labour-intensive phase of the construction programme. Peak EPC construction periods, when multiple subcontractor crews work simultaneously across civil, structural, mechanical, and electrical disciplines, represent statistically elevated injury risk environments. Maintaining an LTIF below 3.0 per million man-hours across a project of this scale and complexity reflects meaningful safety management capability.

The next major ASX story will hit our subscribers first

The SART Plant: A Parallel Value-Creation Stream

What SART Technology Does and Why It Matters

SART stands for Sulphidisation, Acidification, Recycling, and Thickening. It is a metallurgical process applied to cyanide-bearing solutions containing dissolved copper, enabling copper recovery from solutions that would otherwise be treated as waste or require costly cyanide destruction. At Gediktepe, the SART plant targets copper recovery from stockpiled oxide ore that carries cyanide-soluble copper content.

This technology generates an important but underappreciated operational benefit beyond just copper recovery: by precipitating copper from the leach solution, SART frees up cyanide for recycling back into the leach circuit, reducing reagent consumption costs. In environments with high cyanide-soluble copper grades, this reagent saving can be economically significant.

SART Plant vs. Sulphide Expansion: A Comparison

| Feature | Sulphide Expansion Project | SART Plant |

|---|---|---|

| Ore Source | Fresh sulphide ore | Stockpiled oxide ore |

| Primary Output | Copper and zinc concentrates | Copper equivalent production |

| Production Timeline | First production August 2026 | 2026–2030 |

| Annual Scale | Up to 25,000 kt CuEq/year | ~57 kt CuEq total over 4 years |

| Capital Nature | Major EPC brownfield expansion | Supplementary processing addition |

The SART plant's targeted output of 57 kt CuEq across the 2026 to 2030 period is modest relative to the sulphide circuit's nameplate capacity, but it represents incremental value extraction from material that would otherwise generate no revenue. It is a capital-efficient value capture mechanism rather than a growth driver.

The Commissioning Sequence: How First Production Actually Happens

Step-by-Step: From Mechanical Completion to Commercial Output

The pathway from the current 87.2% project completion to first copper and zinc concentrate shipment in August 2026 follows a structured commissioning sequence that is often poorly understood outside the engineering community:

-

Dry Commissioning: All mechanical, electrical, and instrumentation systems are tested without ore or water. Equipment is rotated, interlocks are verified, and control systems are calibrated. This phase identifies installation errors before any process media is introduced.

-

Water Commissioning: Process circuits are flooded and hydraulic performance is validated. Pumps, pipelines, thickeners, and flotation cells are tested under realistic hydraulic loads. Pipeline leak testing and pump curve verification occur at this stage.

-

Ore Commissioning: First ore is introduced to the grinding and flotation circuit. Flotation reagent additions (collectors, frothers, depressants) are optimised iteratively to achieve target copper and zinc recoveries. Concentrate quality is benchmarked against offtake contract specifications.

-

Ramp-Up to Commercial Production: Throughput rates are progressively increased toward nameplate capacity. Recoveries are stabilised across varying ore types. First commercial concentrate parcels are prepared, sampled, assayed, and dispatched to smelters.

Long-Term Competitive Positioning: What Gediktepe Means at Scale

Copper Supply Scarcity and the Value of Mid-Tier Producers

The global copper market faces a structural supply deficit that has been documented extensively by major commodity research institutions. New large-scale copper mine development has lagged exploration investment, environmental permitting timelines have extended in key jurisdictions, and average ore grades at existing operations continue to decline. Against this backdrop, a project capable of delivering up to 25,000 tonnes of copper equivalent annually over an 11-year mine life occupies a meaningful position in the mid-tier producer landscape.

Zinc provides secondary revenue diversification. While zinc's demand profile is less directly tied to electrification narratives than copper, its role in galvanised steel production links it to construction and infrastructure cycles. In a portfolio sense, the combination of copper and zinc concentrates from a single operation provides natural commodity diversification without requiring separate asset ownership. Furthermore, investors evaluating copper investment opportunities of this nature should consider how mid-tier producers with fixed-cost EPC structures compare to exploration-stage assets on a risk-adjusted basis.

Execution Track Record as a Capital Markets Signal

Large-scale mining EPC projects completing on schedule and within their fixed-price budget remain statistically rare. The combination of a fixed-price contract structure, pre-funded bond financing, and demonstrated construction progress tracking toward an August 2026 first production date sends a meaningful signal to bond investors and potential future capital partners. Completing a definitive feasibility study with rigorous cost controls is one thing; executing against it at this scale is another matter entirely.

Credible EPC execution at this scale materially lowers the perceived risk premium for any future capital raising activity, whether for mine life extension, resource expansion drilling, or potential refinancing of the existing bond structure at more favourable rates. In addition, broader mining consolidation trends suggest that assets demonstrating on-schedule, within-budget delivery increasingly attract strategic interest from larger operators seeking proven production platforms.

The ACG Metals Gediktepe Sulphide Expansion Project demonstrates a replicable template for brownfield conversions: fix the construction cost risk through a turnkey EPC contract, pre-fund the transition period through bond markets before it begins, and extract supplementary value from legacy ore stockpiles through parallel processing technology. This three-part structure materially reduces the execution risks that have historically caused cost and schedule blowouts in equivalent greenfield developments.

Disclaimer: This article contains forward-looking statements including production guidance, cost forecasts, and project completion timelines. These reflect the company's current expectations and are subject to material risks including commodity price movements, construction delays, geological variability, and regulatory changes. Past operational performance does not guarantee future results. This article does not constitute financial advice.

Want to Capitalise on the Next Major Copper or Zinc Discovery Before the Broader Market Reacts?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across copper, zinc, and over 30 other commodities, instantly translating complex geological data into actionable investment insights — explore Discovery Alert's discoveries page to understand how historic mineral discoveries have generated substantial market returns, and begin your 14-day free trial at discoveryalert.com.au to position yourself ahead of the market.