August 6, 2026

The Price-Volume Paradox at the Heart of Modern Commodity Economics

Every few years, global commodity markets produce a data point that challenges conventional assumptions about how resource-dependent economies generate wealth. The standard mental model assumes that more output equals more revenue. Yet in 2026, Chile demonstrated something far more instructive: Chilean copper exports record despite production drop is perhaps the most striking example of price dominating volume in recent commodity history. Understanding this mechanism carries direct implications for investors, policymakers, and mining executives interpreting export data from resource-intensive nations.

This dynamic is best understood through the concept of price elasticity of export revenue, which measures how sensitive a nation's total export earnings are to price movements versus volume changes. When a commodity represents half of all national exports, a sustained price increase of even 30 to 40 percent can mathematically overwhelm a moderate volume decline. Chile's 2026 copper export performance is a near-perfect empirical illustration of this principle, and the full picture is considerably more complex than the headline revenue record suggests. The Chile copper price forecast for this period anticipated elevated prices, though few expected the divergence from production volumes to be this pronounced.

When big ASX news breaks, our subscribers know first

What Chile's $60 Billion Export Milestone in H1 2026 Actually Represents

Breaking Down the Record First-Half Export Performance

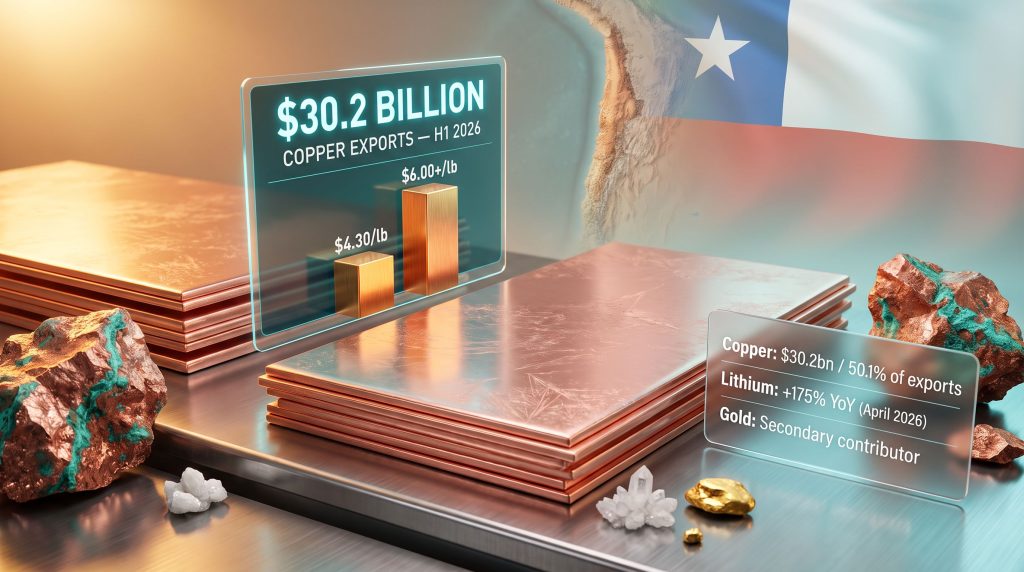

Chile's total export revenues surpassed $60 billion in the first half of 2026, marking the first time on record the country has crossed this threshold within a single six-month window. This represented a 14.2% year-on-year increase, an impressive figure by any macroeconomic standard.

Copper was the engine behind this result. The metal accounted for 50.1% of total national export value, equivalent to $30.2 billion across the first half of the year. June 2026 alone set a new single-month record, with total Chilean exports reaching $10.789 billion, a 25.1% year-on-year increase for that month alone.

To appreciate the structural weight these numbers carry, consider copper's position within Chile's national accounts:

| Metric | Value |

|---|---|

| H1 2026 Total Chilean Exports | >$60 billion |

| H1 2026 Copper Export Value | $30.2 billion |

| Copper Share of Total Exports | ~50.1% |

| June 2026 Monthly Export Record | $10.789 billion |

| Year-on-Year June Growth | +25.1% |

| Copper's Approximate GDP Contribution | ~10% |

Copper is not merely Chile's largest export. It is the single commodity around which the country's fiscal architecture, sovereign wealth accumulation, and national budget planning are constructed. When copper prices surge, Chile's government revenues, corporate tax collections, and royalty streams move in near-lockstep. This creates both opportunity and vulnerability simultaneously. Furthermore, Chile's copper supply role in global markets means these domestic dynamics ripple outward with considerable force.

Why Chilean Copper Production Is Falling Despite Record Export Revenues

The Structural Decline in Output: A Nine-Year Low

The financial record is real, but the physical reality beneath it tells a different story. Chilean copper production in Q1 2026 fell by approximately 5.8 to 6%, landing in the range of 1.21 to 1.23 million tonnes, the weakest quarterly output figure recorded in nine years. February 2026 was particularly notable, with monthly output of 378,554 metric tonnes, the lowest single-month figure since March 2017, representing a 4.8% year-on-year decline.

The divergence between surging revenues and contracting physical output is not coincidental. It reflects a fundamental tension at the heart of Chile's mining sector. According to data on Chilean copper output, this structural weakening has been building for several years.

Operational Pressures at Chile's Major Mining Operations

What makes the 2026 production decline structurally significant, rather than simply cyclical, is that multiple major operations experienced simultaneous contractions:

- Escondida, the world's largest copper mine by output, recorded a production decline of approximately 16%, primarily driven by deteriorating ore grades across the deposit.

- Codelco, Chile's state-owned copper giant, saw output fall by roughly 10%, compounded by ageing infrastructure challenges and scheduled maintenance cycles. Notably, Codelco production trends have been under intense scrutiny as the state miner navigates these headwinds.

- Collahuasi, one of the highest-altitude large-scale copper operations in the world, experienced a volume contraction of approximately 11%, reflecting similar grade pressure as Escondida.

The convergence of these declines across three of Chile's most productive operations in the same period signals something beyond routine disruption.

The simultaneous production contraction across Chile's largest copper operations strongly suggests a systemic rather than episodic challenge, rooted in the natural lifecycle of maturing ore bodies and the compounding effects of deferred capital investment in grade management infrastructure.

Ore Grade Degradation: The Silent Constraint on Chilean Copper Supply

Ore grade, expressed as the percentage of copper contained within a given tonne of mined rock, is arguably the most consequential and least publicly discussed variable in copper mining economics. As a deposit matures, miners must process progressively larger volumes of rock to extract the same quantity of refined copper. This dynamic, known within the industry as grade dilution, directly increases the cost per pound of copper produced.

Chile's major porphyry copper deposits, which include the geological formations hosting Escondida and Collahuasi, are classic examples of large-tonnage, low-grade systems. These deposits were extraordinarily productive during earlier extraction phases when near-surface, higher-grade ore was accessible. As mining has progressed deeper into lower-grade zones, the economics have tightened considerably.

A less commonly understood aspect of this challenge is the relationship between grade and acid consumption in heap leach processing. As oxide ore zones are depleted and operations transition toward sulphide ores at greater depths, operators must shift toward more energy-intensive flotation and smelting circuits. This requires substantial capital investment and extends timelines before new ore zones contribute meaningfully to overall production.

How Rising Copper Prices Compensate for Falling Production Volumes

The Revenue Arithmetic of a Price Surge

The mathematics of price-driven revenue growth in a commodity-dependent economy can be broken down systematically:

- Establish the prior price baseline: Copper was trading at approximately $4.30 per pound in the comparable prior period.

- Identify the new price level: In 2026, copper prices exceeded $6.00 per pound, representing an increase of roughly 40%.

- Apply the volume adjustment: Production declined by approximately 6% over the same period.

- Calculate the net revenue effect: A 40% price increase applied against a 6% volume reduction produces a substantial net revenue expansion, as the price multiplier dramatically outweighs the volume subtraction.

- Recognise the temporal limitation: This arithmetic only holds for as long as prices remain elevated. It does not reflect any improvement in Chile's underlying productive capacity.

The following table illustrates how export revenue sensitivity changes across different copper price scenarios, assuming Chile's current constrained production volumes persist:

| Copper Price (USD/lb) | Estimated Revenue Impact | Production Volume Assumption |

|---|---|---|

| $4.00 (downside scenario) | Significant revenue compression | Volume decline persists |

| $4.30 (prior baseline) | Baseline revenue level | Stable historical volumes |

| $5.00 | Moderate growth above baseline | Slight volume decline |

| $6.00+ (2026 actual) | Record export revenue achieved | ~6% volume decline |

| $7.00 (hypothetical upside) | Further material upside possible | Continued volume pressure |

The critical insight from this table is the asymmetric risk profile. Revenue upside from further price appreciation is real but increasingly marginal, while the downside from a price correction is amplified by the absence of volume growth to cushion the impact. In addition, the copper price drivers underpinning this rally are tied closely to energy transition demand, which introduces its own set of long-term uncertainties.

What Role Other Minerals Played in Chile's 2026 Export Surge

Beyond Copper: Lithium, Gold, and the Diversification Question

While copper dominated the headline figure, other commodities contributed meaningfully to Chile's record H1 2026 export performance. Lithium export values recorded a year-on-year increase of approximately 175% in April 2026, driven by sustained global demand growth from electric vehicle battery manufacturing and grid-scale energy storage deployment.

Gold also performed as a secondary revenue contributor, benefiting from elevated safe-haven demand in a period of broader geopolitical and macroeconomic uncertainty. The combination of strong lithium, gold, and copper prices created a compounding effect on total mining export revenues. However, a structurally important question emerges: is Chile's export revenue base genuinely diversifying, or are multiple commodity prices simply rising together due to shared macro drivers?

| Commodity | Key Performance Indicator | Demand Driver |

|---|---|---|

| Copper | $30.2bn; 50.1% of total exports | Electrification, construction, manufacturing |

| Lithium | ~175% value growth (April 2026 YoY) | EV batteries, grid storage |

| Gold | Secondary contributor to mining revenues | Safe-haven demand, central bank buying |

If the underlying catalyst is a single macroeconomic force, such as a weakening US dollar or synchronised global manufacturing expansion, then the apparent diversification offers limited protection against a broad-based commodity price correction.

Is Chile's Export Revenue Record a Sign of Strength or Structural Vulnerability?

Scenario Modelling: What Happens When Prices Normalise?

The most strategically uncomfortable insight from Chile's 2026 data is that record revenues can simultaneously mask and accelerate structural production decay. High prices reduce the financial urgency for operators to undertake expensive grade management programmes, greenfield development, or deep infrastructure reinvestment. Consequently, three distinct future scenarios are worth examining:

Scenario A: Soft Landing (Copper stabilises at $5.00 to $5.50/lb)

- Export revenues contract from record levels but remain above long-run historical averages

- Production decline continues without a price buffer adequate to fully offset volume losses

- Fiscal revenue pressure begins to emerge within 12 to 18 months of price stabilisation

- Moderate but manageable adjustment for both Codelco and private operators

Scenario B: Sharp Price Correction (Copper falls to $4.00 to $4.30/lb)

- Export revenues revert toward pre-2026 levels with no corresponding recovery in production volumes

- Margin compression at major operations potentially triggers capital expenditure deferrals

- Chile's fiscal position deteriorates, increasing pressure on the sovereign wealth fund

- Risk of a cycle where underinvestment compounds the existing structural production decline

Scenario C: Sustained High Prices ($6.00/lb and above)

- Record export revenues persist, temporarily masking the production decline

- Ore grade degradation continues to progress unchecked, deepening the long-term supply deficit

- Global copper supply tightness intensifies, reinforcing the very price support that masks the problem

- The productive base continues to erode while financial performance remains superficially strong

From a long-term supply security perspective, Scenario C may represent the most strategically dangerous outcome for Chile. Sustained high prices reduce the urgency to address declining ore grades and ageing infrastructure, potentially creating a far deeper supply deficit over a five to ten year horizon.

The next major ASX story will hit our subscribers first

The Long-Term Implications for Global Copper Supply

Chile's Production Trajectory as a Global Variable

Chile's position as the source of approximately 25 to 27% of global copper mine production means its domestic operational challenges carry international consequences. Furthermore, the broader copper supply crunch facing global markets makes Chile's production trajectory a critical variable for energy transition planning worldwide.

When Escondida, Codelco, and Collahuasi simultaneously reduce output, the effect on global copper availability is not marginal. It shifts the global supply-demand balance in ways that influence prices, downstream manufacturing costs, and the economics of energy transition infrastructure everywhere from Germany to South Korea. Copper is the primary conductor in electric vehicle drivetrains, grid-scale battery storage systems, solar panel wiring, and offshore wind turbine generators. According to research into the impacts of Chilean copper mining, the sector's long-term sustainability is deeply intertwined with responsible resource management.

Investment, Water, and the Expansion Pipeline

Reversing Chile's production decline requires addressing three interconnected constraints:

- Capital investment depth: Greenfield copper development from discovery to first production typically requires 15 to 20 years and billions of dollars in pre-production expenditure. Brownfield expansions are faster but require sustained high capital allocation when ore grades are already declining.

- Water availability in the Atacama: Chile's major copper operations are located in one of the driest environments on Earth. As ore grades decline and processing volumes must increase, water demand per unit of copper produced rises. Desalination infrastructure is being developed to partially address this, but it introduces additional energy cost and capital complexity.

- Regulatory and permitting environment: Investment timelines in Chilean mining have extended over recent years, partly reflecting more rigorous environmental impact assessment processes. While these serve legitimate purposes, their net effect on the speed of new capacity development is a material variable for long-term supply planning.

Frequently Asked Questions: Chilean Copper Exports and the 2026 Record

Why did Chilean copper export value reach a record despite lower production?

The record $30.2 billion copper export value in H1 2026 was driven by copper prices exceeding $6.00 per pound, a roughly 40% increase from the prior period baseline. This price surge was large enough to more than compensate for the approximately 6% decline in physical production volumes, generating higher total revenues from a smaller quantity of copper shipped.

How significant was the production decline in quantitative terms?

Q1 2026 copper production fell to between 1.21 and 1.23 million tonnes, representing a decline of approximately 5.8 to 6% and the lowest quarterly output in nine years. February 2026 was the weakest single month since March 2017.

Which operations recorded the largest output contractions?

Escondida recorded approximately a 16% decline, Codelco approximately 10%, and Collahuasi approximately 11%, with all three primarily affected by declining ore grades compounded by maintenance and infrastructure challenges.

What is ore grade and why does it matter for production volumes?

Ore grade refers to the concentration of copper metal within each tonne of mined rock. As deposits mature, average grades typically decline, meaning operators must mine and process more rock to produce the same quantity of copper. This drives up costs, energy consumption, and water usage per unit of output, creating a structural headwind that cannot be resolved simply by scaling up operations.

What other commodities contributed to Chile's H1 2026 export record?

Lithium recorded approximately a 175% year-on-year value increase in April 2026, while gold also contributed as a secondary revenue driver. However, copper's dominance at 50.1% of total exports meant the metal's price surge was the primary determinant of the overall record.

Is the production decline in Chilean copper likely to reverse quickly?

The concurrent decline across multiple major operations, all of which face the shared structural challenge of grade degradation, suggests that a rapid reversal is unlikely without substantial new capital investment, new project development, or significant improvements in processing technology.

Key Takeaways: Understanding Chile's 2026 Copper Export Paradox

The 2026 data from Chile's copper sector presents a compelling case study in how financial performance metrics can diverge from operational fundamentals in commodity-dependent economies. Several conclusions stand out:

- Chile's total H1 2026 exports exceeded $60 billion for the first time on record, with copper contributing $30.2 billion at 50.1% of total export value, entirely driven by price rather than volume growth.

- Copper production reached a nine-year low in Q1 2026, with Escondida, Codelco, and Collahuasi all recording material output contractions simultaneously.

- The price mechanism, copper trading above $6.00 per pound against a prior baseline of approximately $4.30 per pound, mathematically compensated for volume losses but provides no structural protection if prices normalise.

- Ore grade degradation across Chile's major porphyry copper deposits represents a slow-moving but accelerating constraint on long-term productive capacity, with implications that extend well beyond Chile's borders given its 25 to 27% share of global mine supply.

- The energy transition's escalating copper demand trajectory creates a strategic imperative for investment in Chilean copper capacity that current financial incentives, paradoxically elevated by high prices, may actually be delaying.

The Chilean copper exports record despite production drop remains one of the most instructive paradoxes in recent commodity market history, demonstrating precisely how price and volume can pull in opposite directions with profound consequences for both national economies and global supply chains.

This article contains forward-looking analysis, scenario modelling, and commodity price projections for informational purposes only. None of the content should be construed as financial or investment advice. Commodity markets are inherently volatile and actual outcomes may differ materially from any scenarios described. Readers should conduct independent research and consult qualified financial advisers before making investment decisions.

Want to Capitalise on the Next Major Copper Discovery Before the Broader Market Reacts?

As Chile's copper production decline deepens and global supply tightness intensifies, the window to position ahead of significant ASX mineral discoveries is narrowing — Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on high-potential copper and critical mineral announcements, turning complex ASX data into actionable insights instantly. Explore historic discoveries and their returns to understand the scale of opportunity, then begin your 14-day free trial at Discovery Alert to secure your market-leading edge.