May 22, 2026

The Efficiency Illusion That Priced Geopolitical Risk Out of Global Oil Markets

For most of the past four decades, the global energy system operated on an assumption so deeply embedded it was never formally stress-tested: that roughly 20 million barrels of crude oil and petroleum products could flow daily through a single narrow maritime corridor without meaningful interruption. This was not a calculated risk position. It was a convenience that became a doctrine.

Energy planners, cargo financiers, shipping executives, and derivatives traders all built their models around an invisible subsidy — the unspoken assumption that Gulf transit would remain available, insurable, and affordable indefinitely. Furthermore, geopolitical tensions reshaping trade had long signalled the fragility of this arrangement, yet the warning signs were consistently priced out of market models.

That assumption has now been structurally invalidated. The 2026 Iran-Hormuz crisis did not introduce a new vulnerability to global energy markets. It forced the repricing of one that had existed, unacknowledged, for generations. Understanding why ADNOC warns Gulf oil disruptions could last until 2027 requires moving beyond the immediate geopolitical narrative and examining the compounding infrastructure, logistics, and confidence failures that no diplomatic resolution can quickly reverse.

When big ASX news breaks, our subscribers know first

What the ADNOC Warning Actually Means for Global Energy Supply

ADNOC CEO Sultan Ahmed Al Jaber's public statement that Persian Gulf oil export flows will remain severely disrupted until at least mid-2027 represents one of the most operationally significant disclosures in recent energy market history. This is not an analyst forecast or a geopolitical projection. It is an assessment from the national oil company of the UAE, which has direct operational visibility into the infrastructure damage, restoration timelines, and logistical constraints shaping its own export capacity.

Decoding the Habshan Gas Complex Timeline

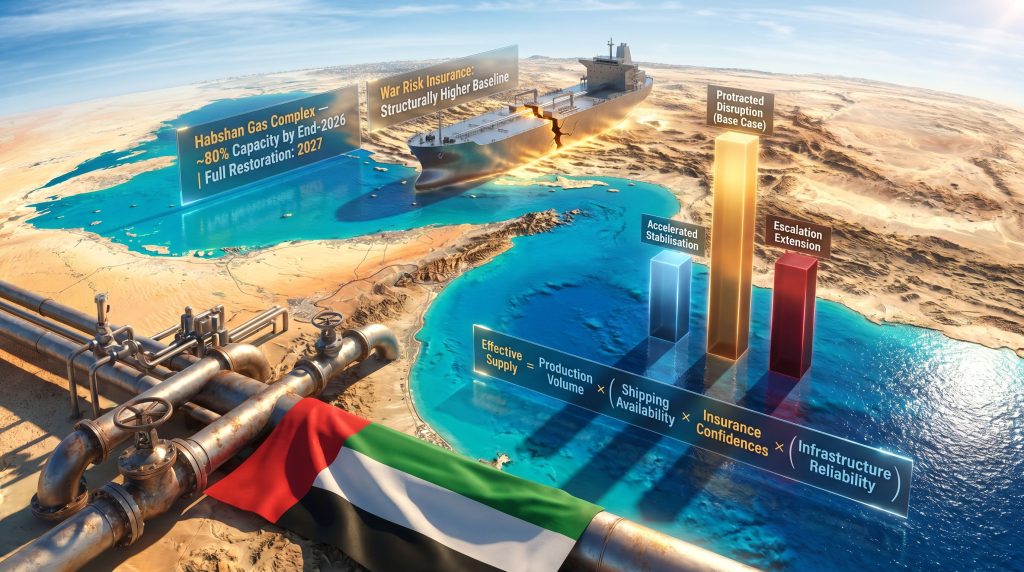

Central to the disruption picture is the Habshan gas processing complex, one of the UAE's most strategically critical upstream assets. The restoration timeline ADNOC has disclosed breaks down as follows:

| Recovery Milestone | Expected Timing | Capacity Restored |

|---|---|---|

| Partial Habshan restoration | End of 2026 | Approximately 80% |

| Full Habshan restoration | 2027 | 100% |

| Hormuz flow normalisation (ADNOC guidance) | Mid-2027 at earliest | Uncertain |

The 20% capacity gap that persists through at least the first half of 2027 is not a rounding error. In large-scale gas processing infrastructure, the final phase of restoration is almost invariably the most technically complex. Engineering teams face increasingly intricate interdependencies between processing trains, compression systems, and pipeline feed arrangements.

This means the 2027 target carries meaningful downside risk, and market participants modelling a clean second-half 2026 recovery are pricing against the operator's own stated guidance. Consequently, the crude oil price trends emerging from this disruption period reflect a market that has not yet fully absorbed the implications of this operational reality.

"The distinction between 80% and 100% operational capacity at a facility of Habshan's scale translates directly into constrained feedstock availability, reduced UAE gas export volumes, and downstream processing limitations that cannot be papered over by headline production announcements."

Three Structural Breaks That Cannot Be Reversed by Open Water Alone

Perhaps the most consequential analytical error circulating in current market discourse is the conflation of an open Strait of Hormuz with a functioning Gulf export system. These are no longer equivalent conditions. Three structural breaks have occurred that persist independently of whether vessels can physically transit the waterway.

1. Tanker Fleet Availability and Hidden Capacity Collapse

Effective tanker capacity serving the Gulf region has contracted far beyond what aggregate production data implies. Fleet rerouting, vessel repositioning decisions by risk-averse operators, and the physical trapping of vessels within the Gulf during active conflict phases have collectively created a supply bottleneck that headline export statistics systematically understate.

Vessels that remain operational in the region now carry layered cost structures that did not exist in the pre-2026 environment:

- Elevated war risk insurance premiums applied per voyage

- Military escort requirements and associated coordination delays

- Crew risk allowances and retention premiums in a labour market increasingly reluctant to deploy to active conflict zones

- Extended voyage times from rerouting and convoy scheduling

- Increased maintenance cycles from accelerated hull wear on alternative routes

Each of these cost layers reduces the commercial viability of individual cargo movements, compressing the effective spare capacity that producers can actually deliver to consuming markets.

2. Insurance Market Repricing as a Structural Floor

War risk insurance rates for Gulf transit have undergone a repricing that cannot be characterised as temporary. Underwriters are now constructing multi-year risk premium structures rather than offering spot coverage at historically normal rates. This means every barrel that transits the region carries an embedded security surcharge that will persist long after immediate hostilities diminish.

The insurance dynamic matters for a reason that goes beyond cost: coverage availability, not just price, determines whether cargo financing can be arranged. Without commercially viable war risk coverage, lenders and cargo financiers cannot secure their positions, which means barrels that are physically producible and logistically movable still cannot enter the market as effective supply. This dynamic compounds the broader oil price shock already reverberating through global energy systems.

3. Infrastructure Vulnerability Beyond the Strait Itself

The Habshan-Fujairah pipeline, designed specifically to bypass Hormuz and move crude directly to a Red Sea-adjacent export terminal, was constructed precisely because Abu Dhabi's leadership recognised Hormuz's long-term strategic exposure decades ago. However, the geopolitical fragmentation that undermined Hormuz has now migrated into the broader Gulf maritime ecosystem, exposing the bypass architecture itself.

Fujairah port, the primary loading terminal for bypass route exports, now faces a distinct set of challenges:

- Shipping congestion from diverted vessel traffic

- Elevated cyber risk exposure targeting port management and navigation systems

- Increased military targeting concern given its role as the primary alternative to Hormuz

- Infrastructure capacity constraints not designed for the throughput volumes now being directed to it

"An open Strait of Hormuz is no longer equivalent to normal Gulf oil operations. The infrastructure, insurance, financing, and security systems that collectively enable barrel movement have been structurally impaired, and restoring them requires far more than navigable water."

The Hidden Supply Equation Markets Are Ignoring

One of the most penetrating analytical frameworks for understanding the current disruption centres on a fundamental redefinition of what constitutes available supply. In conventional energy economics, supply is measured in production volumes. However, effective supply is a function of multiple interdependent variables, each of which can independently constrain market availability:

Effective Supply = Production Volume x (Shipping Availability x Insurance Accessibility x Financing Confidence x Infrastructure Reliability)

When any single multiplier in this equation approaches zero, headline production figures become strategically misleading. A barrel that cannot be insured cannot be financed. A barrel that cannot be financed cannot be contracted. A barrel that cannot reach the specific refinery grade it was purchased for does not function as market supply, regardless of what production statistics report.

This dynamic has given rise to what analysts are increasingly calling a two-tier oil system, where barrels with secure, non-Hormuz routing command structural premiums over Gulf-origin crude. Furthermore, the traditional stabilising function of OPEC's market influence is materially degraded by delivery-side constraints rather than production-side limitations.

Scenario Modelling: Three Trajectories Through 2027

| Scenario | Probability | Hormuz Normalisation | Price Impact | Security Premium Duration |

|---|---|---|---|---|

| Accelerated Stabilisation | Low | Q4 2026 | Moderate decline | 12 to 18 months |

| Protracted Disruption (Base Case) | High | Mid-2027 | Sustained elevation | 2 to 4 years |

| Escalation Extension | Moderate tail risk | Post-2027 | Significant upside | Structural / permanent |

Scenario 1: Accelerated Stabilisation assumes diplomatic resolution before late 2026, Habshan restoration tracking ahead of schedule, and partial insurance market normalisation. Even under this optimistic scenario, the structural fragility of the Gulf export system persists. A security premium, once embedded in underwriting models and freight rate structures, does not simply evaporate.

Scenario 2: Protracted Disruption represents the base case, consistent with ADNOC's own operational guidance. Habshan reaches approximately 80% capacity by end-2026, full restoration follows in 2027, and Hormuz remains operationally constrained through mid-2027. Two-tier oil pricing becomes entrenched, and the traditional relationship between OPEC production announcements and price outcomes breaks down.

Scenario 3: Escalation Extension involves restoration timelines slipping beyond 2027, the Fujairah bypass capacity becoming operationally compromised, and major tanker operators formally withdrawing from Gulf route commitments. Under this scenario, energy security replaces cost optimisation as the primary planning criterion for virtually every oil-importing economy on the planet.

Why Market Complacency Persists Despite Clear Operational Signals

The cognitive architecture of energy trading has historically been built around mean-reversion: the assumption that geopolitical disruptions are episodic, that spare capacity will eventually stabilise prices, and that the Gulf will always switch back on. This mental model performed adequately when disruptions were genuinely temporary. It becomes actively dangerous when the disruption is structural.

Current pricing still reflects a scenario that contradicts ADNOC's own disclosed operational realities. Investment banks are modelling gradual normalisation. Traders continue building positions around Hormuz reopening as a catalyst for supply recovery. In addition, the trade war impact on oil has further complicated these pricing dynamics, layering demand-side uncertainty onto an already impaired supply picture.

The psychological dynamic driving this complacency is well-documented in behavioural finance. Market participants anchor to prior equilibria and assign insufficient probability weight to structural breaks. When the disruption is visible but the full mechanism of impairment is technically complex, the cognitive shortcut is to simplify: lanes are open, therefore supply is flowing. This shortcut is now producing systematic mispricing.

The next major ASX story will hit our subscribers first

Cascading Downstream Consequences Across Global Energy Systems

The implications of a prolonged Gulf disruption extend well beyond crude oil benchmarks. The cascade runs through virtually every energy-linked market:

- Refining margins: Refineries configured for Gulf crude grades face feedstock substitution costs as alternative origins carry different sulphur content, density profiles, and logistics expenses

- LNG freight markets: The same conflict that disrupted crude flows has simultaneously tightened Asian LNG supply, compounding gas market stress and driving freight rate increases

- Petrochemical feedstocks: Gulf-sourced naphtha and condensate disruptions are transmitting production cost increases through Asian manufacturing supply chains

- Bunker fuel pricing: Fleet rerouting and repositioning add secondary cost layers to global shipping economics, affecting trade costs across all commodity categories

- Consumer price indices: Energy cost transmission through freight, manufacturing inputs, and retail fuel prices is increasingly linking Gulf instability to headline inflation in importing economies

Japan's crude imports from the Middle East have slumped to their lowest recorded levels, prompting deepening bilateral energy cooperation with South Korea. India is actively exploring direct loading alternatives to reduce Hormuz transit exposure, though port infrastructure constraints limit near-term optionality. Australia has turned to non-traditional sources for emergency jet fuel procurement, illustrating how the disruption's reach extends into downstream product markets far from the Persian Gulf.

What Genuine Recovery Actually Requires

Restoring confidence in Gulf energy exports is not a binary event triggered by a ceasefire announcement or a diplomatic communique. It requires simultaneous, sustained progress across five interdependent domains:

- Physical infrastructure restoration: Habshan complex, regional pipeline networks, port facilities, and terminal capacity must reach full operational status and demonstrate sustained reliability

- Cybersecurity hardening: Digital systems protecting energy assets, shipping navigation, and port operations require multi-year investment programmes that cannot be accelerated by political will alone

- Insurance market re-engagement: War risk underwriters must be willing to offer commercially viable, multi-voyage coverage for Gulf transit at volumes sufficient to support normal trade flows

- Geopolitical stabilisation: Regional security conditions must improve durably enough for tanker operators, cargo financiers, and shipping companies to commit capital back into Gulf route exposure

- Confidence reconstruction: Market trust, once destroyed, requires an extended period of operational normalcy before it rebuilds, and this timeline cannot be compressed by announcements alone

Even under optimistic assumptions, achieving meaningful simultaneous progress across all five domains before mid-2027 is unlikely. According to Fox Business, Saudi Aramco's CEO has similarly cautioned that oil markets may not recover until 2027 due to Hormuz disruptions, reinforcing precisely why ADNOC's stated guidance deserves to be treated as a baseline rather than a worst case.

The Permanent Security Premium and the New Energy Baseline

The most consequential long-term implication of the 2026 Gulf disruption is not the price spike. It is the permanent embedding of a security premium into Gulf energy economics. Freight volatility, insurance cost floors, and infrastructure redundancy requirements will transition from exceptional circumstances into baseline operating assumptions.

The old model, in which energy security and market efficiency were treated as separate considerations managed by separate institutions, has collapsed. What replaces it is a framework in which the survivability of supply chains takes precedence over their cost optimisation. Buyers will accelerate crude import diversification. Cargo financiers will build defensive optionality into contract structures. Insurance capital will require higher return thresholds before fully re-engaging with Gulf exposure.

"Markets waiting for a return to pre-2026 Gulf energy conditions are, in effect, waiting for a world that no longer exists. The strategic question is not when normalcy returns. It is how rapidly market participants, infrastructure operators, and energy policymakers can adapt their frameworks to a structurally altered energy security landscape."

The situation in which ADNOC warns Gulf oil disruptions could last until 2027 is not a pessimistic outlier. It is an operational disclosure from an institution with unparalleled visibility into the system's actual condition. The mid-2027 timeline it references should be understood not as the outer bound of disruption but as the earliest plausible moment for partial functional recovery, contingent on conditions that remain uncertain at every level from physical infrastructure through to geopolitical stability.

This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking statements and scenario projections involve inherent uncertainty and should not be relied upon as predictions of future outcomes. Readers are encouraged to conduct independent research and consult qualified advisors before making investment decisions.

Want to Stay Ahead of Commodity Market Shifts Driven by Global Supply Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex market data into actionable investment insights — ensuring subscribers are positioned ahead of the broader market as energy and commodity dynamics continue to evolve. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin your 14-day free trial today to gain an immediate market-leading edge.