July 19, 2026

When Geopolitics Rewrites the Rules of Global Commodity Pricing

Few moments in commodity markets are as instructive as when a single geopolitical event collapses decades of supply chain assumptions within a matter of weeks. The sulphur market, long considered a relatively stable industrial by-product category, is delivering precisely that lesson in 2026. ADNOC raises May sulphur price by $160/t, and what traders, fertilizer manufacturers, and agricultural economists are witnessing is not a conventional price cycle driven by demand growth or capacity constraints. It is a forced structural repricing triggered by conflict, infrastructure damage, and a logistics network pushed to its breaking point.

Understanding how this unfolded, what it means for global food production costs, and where it goes next requires looking beyond the headline numbers and into the mechanics of how the Gulf's sulphur pricing architecture actually functions. Furthermore, geopolitical commodity risks are increasingly shaping price outcomes across the entire industrial minerals complex.

When big ASX news breaks, our subscribers know first

How the ADNOC Official Selling Price Actually Works

The Official Selling Price, or OSP, is a monthly benchmark set by a producer to anchor contract negotiations across a defined geographic market. ADNOC's OSP for sulphur exports from its Ruwais terminal in Abu Dhabi serves as the primary reference price for buyers across the Indian subcontinent. When ADNOC adjusts its OSP, it effectively recalibrates the cost foundation for every sulphur-dependent industry in the region.

The distinction between fob (free on board) and cfr (cost and freight) pricing matters significantly here. The fob OSP reflects the price at the point of loading, with risk transferring to the buyer the moment product leaves the terminal. The cfr price, by contrast, includes freight to the destination port and is the figure that Indian manufacturers actually pay in practice.

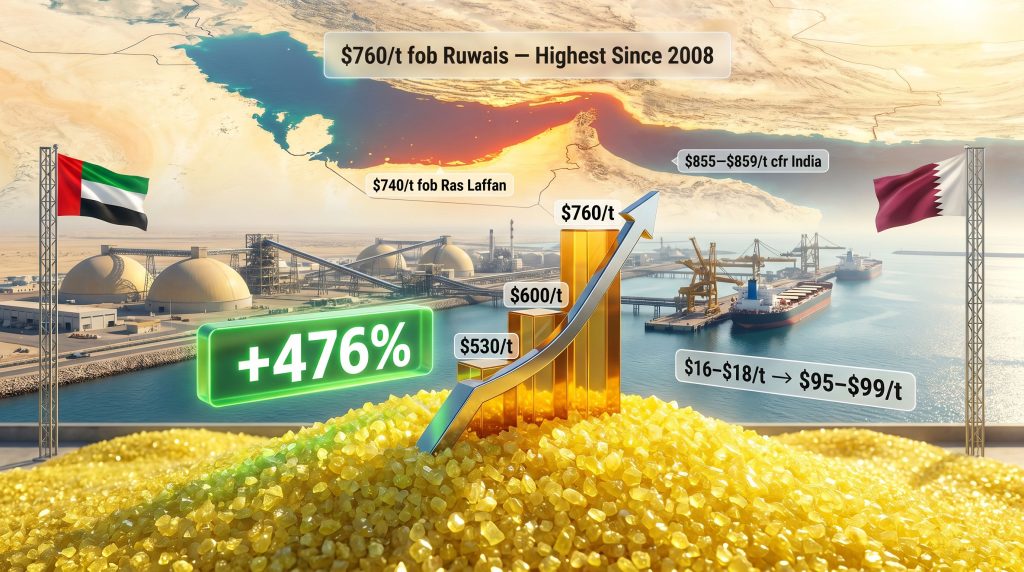

In the current environment, that freight component has become as significant as the headline OSP itself. As of 30 April 2026, freight rates for 40,000 to 45,000 tonne shipments from the Gulf to India's east coast were assessed at $95 to $99 per tonne, implying a delivered cost of approximately $855 to $859/t cfr India based on ADNOC's May 2026 OSP of $760/t fob Ruwais (ADNOC raises May sulphur price, Argus Media, 5 May 2026).

The May 2026 OSP in Historical Perspective

The magnitude of ADNOC's May 2026 adjustment becomes clearer when viewed against the recent price trajectory:

| Period | ADNOC OSP (fob Ruwais) | Month-on-Month Change |

|---|---|---|

| February 2026 | $530/t | +$10/t |

| March 2026 | $530/t | Rolled over |

| April 2026 | $600/t | +$70/t |

| May 2026 | $760/t | +$160/t |

| Peak (Jun–Aug 2008) | $800–$820/t | Historical reference |

The $160/t single-month increase represents a 26.7% jump and is one of the largest monthly OSP adjustments on record in the modern sulphur market. At $760/t fob, this is the highest ADNOC OSP since the extraordinary commodity supercycle of mid-2008, when prices briefly touched $800 to $820/t fob before softening (Argus Media, 5 May 2026).

Key context: The 2008 sulphur spike was demand-driven, fuelled by a global commodity supercycle and fertilizer boom. The 2026 escalation is fundamentally different in origin, reflecting an acute supply destruction event rather than demand expansion. This distinction matters enormously for how quickly prices might correct.

What Is Behind the Unprecedented Surge in Sulphur Prices

The price surge traces directly to the onset of the US-Iran conflict in late February 2026, which fundamentally disrupted the commodity logistics architecture of the Middle East. The effective closure of the Strait of Hormuz stranded sulphur shipments that would ordinarily flow freely toward Indian and Asian destinations. Infrastructure damage, including to Qatar's Ras Laffan gas processing complex, reduced regional production well below normal operating levels (Argus Media, 30 April 2026).

Sulphur is predominantly a by-product of natural gas processing and petroleum refining. When upstream infrastructure sustains damage, there is no alternative production pathway to activate. The output loss is immediate and the recovery timeline is tied directly to physical reconstruction rather than to market price signals or capital allocation decisions. In addition, global supply chain disruption of this magnitude creates ripple effects that extend far beyond the directly affected region.

Compounding the production shortfall, dwindling storage capacity across the region has limited producers' ability to accumulate exportable inventory. Sulphur loadings from the Middle East have continued at dramatically reduced rates, creating a structural gap between regional supply availability and ongoing import demand from South and Southeast Asia (Argus Media, 30 April 2026).

The Freight Cost Multiplier: A Hidden Price Driver

The freight escalation layered on top of the OSP increase is perhaps the most underappreciated dimension of the current crisis. Consider the trajectory:

| Date | Route | Shipment Size | Freight Rate | Change from Feb 26 Baseline |

|---|---|---|---|---|

| 26 February 2026 | Gulf to India East Coast | 40,000–45,000t | $16–$18/t | Baseline |

| 30 April 2026 | Gulf to India East Coast | 40,000–45,000t | $95–$99/t | +476% |

| 23 April 2026 | Gulf to Chinese Ports | 30,000–35,000t | $116–$122/t | N/A |

A 476% freight rate increase since 26 February 2026 reflects the compounding effect of war risk insurance premiums, elevated bunker fuel surcharges, and dramatically reduced vessel availability in the conflict zone (Argus Media, 5 May 2026). These costs are not captured in the headline OSP figure but are absorbed entirely by the importer.

This creates an important analytical distinction: even if the fob OSP were to stabilise at current levels, delivered costs for Indian and Asian buyers would remain structurally elevated for as long as conflict conditions persist. The freight component alone has added roughly $77 to $81 per tonne above pre-conflict levels to every cargo arriving at an Indian east coast port. Consequently, commodity market volatility of this kind demands robust hedging strategies from downstream buyers.

How ADNOC's Pricing Compares to Other Gulf Producers

ADNOC is not the only major Gulf sulphur producer responding to the supply disruption with significant price increases. QatarEnergy Marketing raised its May 2026 Qatar Sulphur Price (QSP) to $740/t fob Ras Laffan/Mesaieed, a level that marks an all-time record high in Argus price records dating back to 2013 (Argus Media, 30 April 2026).

The scale of the QSP escalation is striking in its own right. The previous record high of $490/t fob, set in August 2022, has now been surpassed by $250/t, representing a 51% premium over the prior all-time high (Argus Media, 30 April 2026). For Chinese buyers, QatarEnergy's pricing implies a delivered cost of approximately $856 to $862/t cfr China based on freight assessments of $116 to $122/t for 30,000 to 35,000 tonne shipments, before additional insurance premiums are factored in.

| Producer | May 2026 OSP | Loading Port | Primary Market | Implied cfr (Key Route) |

|---|---|---|---|---|

| ADNOC | $760/t fob | Ruwais, UAE | Indian Subcontinent | ~$855–$859/t cfr India |

| QatarEnergy | $740/t fob | Ras Laffan/Mesaieed, Qatar | China and broader Asia | ~$856–$862/t cfr China |

The narrow pricing band between the two producers is analytically significant. This is not a situation where one producer is opportunistically outpacing the other. Both are responding to the same underlying supply constraint, and their convergence validates that the pricing pressure is systemic rather than commercially strategic. According to World Fertilizer's analysis of Middle Eastern sulphur prices, this regional price alignment is consistent with broader structural tightness across Gulf export markets.

Downstream Consequences for Global Fertilizer Markets

Sulphur's role in the agricultural supply chain is not widely understood outside the industry, but it is critical. The majority of commercially produced sulphur is processed into sulphuric acid, which is the primary reagent used in the manufacture of phosphate fertilizers including DAP, MAP, TSP, and SSP. When sulphur input costs escalate sharply, phosphate fertilizer manufacturing costs follow with a meaningful lag.

The current disruption is arriving into an already stressed fertilizer complex. Key market developments as of late April and early May 2026 include:

- Urea prices at New Orleans have risen by $159/short tonne, or 24%, since the conflict began, reaching $629/st as of late April 2026. This level sits $144/st above year-ago comparisons (Argus Media, 30 April 2026).

- India's IPL is coordinating an industry-wide collective tender for 1.6 million tonnes of DAP and TSP, closing 7 May 2026, reflecting the scale of import requirements and the need to consolidate buyer negotiating power in a supply-constrained environment (Argus Media, 29 April 2026).

- Egyptian producer NCIC's late-April tender saw DAP clear at up to $880/t fob and urea at up to $852/t fob Ain Sokhna, underscoring the extent of broad fertilizer market tightness (Argus Media, 30 April 2026).

- Indian fertilizer producer and importer RCF has separately issued a tender for phosphate rock, DAP/MAP, and MOP with a closing date of 9 May, specifying phosphate rock from Togo at a minimum grade of 35% P2O5 (Argus Media, 29 April 2026).

The simultaneous escalation of sulphur, phosphate, and nitrogen prices represents a compound input cost shock for agricultural producers across South and Southeast Asia, markets that depend heavily on imported fertilizer rather than domestic production capacity.

El Nino Adds a Demand-Side Complication

An additional layer of complexity is emerging on the demand side. The Philippines' Department of Agriculture has activated a preparedness plan for moderate to strong El Nino conditions expected in the latter part of 2026. El Nino brings drier and warmer weather to the region, which can suppress fertilizer application rates given that nutrient uptake and application timing are closely tied to rainfall patterns (Argus Media, 30 April 2026).

The Philippines' last significant El Nino event in 2024 saw rice output fall sharply, driving rice imports to 4.8 million tonnes, the highest level recorded in at least a decade and a 32% increase on 2023 volumes (Argus Media, 30 April 2026). A repeat scenario in late 2026 could reduce fertilizer offtake from a key Southeast Asian market at precisely the moment when global supply chains are under maximum stress.

Three Scenarios for Where Sulphur Prices Go From Here

The following scenarios represent analytical frameworks for understanding possible market trajectories and do not constitute financial or investment advice. Commodity market outcomes are inherently uncertain and depend on geopolitical, logistical, and macroeconomic variables that cannot be precisely forecast.

Scenario 1: Conflict Resolution and Rapid Market Normalisation

If the US-Iran conflict resolves and the Strait of Hormuz reopens within the third quarter of 2026, freight rates could normalise within 60 to 90 days as vessel availability recovers and war risk premiums fall away. OSPs would likely retrace sharply toward the $400 to $500 per tonne range seen in late 2025. The 2008 precedent is instructive: that spike collapsed rapidly once demand destruction and normalised supply flows reasserted themselves.

Scenario 2: Prolonged Conflict with Partial Logistics Workarounds

Producers and shippers develop alternative routing strategies, gradually reducing but not eliminating freight cost escalation. OSPs stabilise in an elevated $600 to $700/t range as partially functional supply chains are reestablished. Downstream fertilizer markets adapt through sourcing diversification and, where possible, demand reduction. However, oil price movements in this scenario would remain under significant upward pressure as well.

Scenario 3: Extended Infrastructure Damage and Structural Supply Loss

Damage to facilities such as Ras Laffan extends the production deficit beyond 12 months, forcing permanent reorientation of global sulphur supply chains toward non-Gulf sources. These include Canadian oil sands by-product sulphur, Kazakhstan's Tengiz field output, and Russian exports. Prices remain historically elevated and fundamentally reprice sulphur-dependent fertilizer inputs across multiple growing seasons. The implications for trade and geopolitics in oil and associated by-products under this scenario would be far-reaching.

The next major ASX story will hit our subscribers first

How Buyers Are Adapting to the Supply Crunch

With Gulf sulphur availability constrained and prices at near-record levels, importing countries and end-users are responding through several distinct procurement strategies:

- Collective purchasing consolidation: Indian buyers are pooling demand through industry tenders, as demonstrated by IPL's coordinated 1.6 million tonne DAP and TSP tender, improving negotiating leverage when individual buyer power is diminished in a supply-constrained market.

- Geographic sourcing diversification: Buyers are exploring alternative origin points for both sulphur and phosphate inputs. RCF's tender specifying Togolese phosphate rock reflects a deliberate effort to reduce exposure to Middle East supply chains.

- Longer-term offtake structures: Spot market volatility at current levels is creating strong incentives for buyers to explore longer-duration supply agreements that provide cost certainty across multiple seasons.

- Alternative non-Gulf sulphur sourcing: Canada, Kazakhstan, and Russia represent the most commercially viable non-Gulf sulphur supply alternatives. However, logistical cost differentials, quality specification requirements, and the time needed to redirect established trade flows create practical limits on how quickly substitution can occur at scale.

Frequently Asked Questions: Middle East Sulphur Prices in 2026

What is ADNOC's sulphur OSP and why does it matter?

ADNOC's Official Selling Price is a monthly benchmark set by Abu Dhabi's state energy company for sulphur exports from the Ruwais terminal. It serves as the primary pricing reference for buyers across the Indian subcontinent and cascades through contract negotiations for sulphur-dependent industries throughout the region.

Why did ADNOC raises May sulphur price by $160/t?

The increase reflects an acute regional supply shortage driven by the US-Iran conflict, which has disrupted Middle East sulphur production and export logistics. Reduced export availability, infrastructure damage including to Qatar's Ras Laffan gas plant, and dramatically higher freight costs all contributed to the escalation (Argus Media, 5 May 2026).

How does the May 2026 sulphur price compare to historical levels?

At $760/t fob Ruwais, ADNOC's May 2026 OSP is the highest since June to August 2008, when prices peaked at $800 to $820/t fob during the global commodity supercycle (Argus Media, 5 May 2026).

What is the delivered cost of sulphur to India in May 2026?

Based on freight assessments of $95 to $99/t for standard shipment sizes to India's east coast, the implied delivered cost sits at approximately $855 to $859/t cfr before additional war risk insurance and surcharge costs are applied (Argus Media, 5 May 2026).

How much have sulphur freight rates increased since the conflict began?

Freight rates for Gulf-to-India sulphur shipments rose approximately 476% between 26 February 2026 and 30 April 2026, moving from $16 to $18/t to $95 to $99/t (Argus Media, 5 May 2026).

What impact does elevated sulphur pricing have on fertilizer costs?

Sulphur is a core feedstock for sulphuric acid production, which is in turn essential for manufacturing phosphate fertilizers including DAP, MAP, and TSP. Higher sulphur input costs increase phosphate fertilizer production expenses, contributing to the broader fertilizer price inflation currently affecting agricultural supply chains across South and Southeast Asia.

Key Takeaways: What the Sulphur Price Surge Signals for Commodity Markets

The convergence of data points across the sulphur and fertilizer complex in May 2026 communicates several important signals for market participants:

- The $160/t single-month ADNOC OSP increase is among the largest monthly adjustments in the modern sulphur market, underscoring the severity of the underlying supply disruption.

- Prices are approaching but have not yet exceeded the all-time highs of mid-2008, leaving room for further escalation if conflict conditions persist or intensify.

- The near-identical pricing between ADNOC and QatarEnergy confirms the disruption is systemic and regional, not producer-specific or commercially manufactured.

- The 476% freight rate escalation since late February means that delivered costs for Asian importers are being amplified well beyond what the headline OSP movements alone suggest.

- Downstream fertilizer markets across South and Southeast Asia face compounding input cost pressures at a critical point in the 2026 agricultural calendar, with potential El Nino conditions adding a demand-side uncertainty layer.

- Unlike the 2008 supercycle, where demand destruction ultimately corrected prices, the 2026 spike's resolution depends primarily on geopolitical and military developments rather than conventional supply-demand rebalancing mechanisms.

Readers seeking ongoing price assessments and market analysis across the sulphur and fertilizer complex can access Argus Media's dedicated coverage at argusmedia.com, which provides continuous pricing intelligence and market commentary for industry participants tracking the sulphur market and its downstream implications.

Want to Stay Ahead of Geopolitical Commodity Disruptions Like This One?

When conflict rewrites the rules of commodity pricing overnight, timing is everything — Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, translating complex market shifts into actionable investment opportunities the moment they emerge. Explore how historic discoveries have generated substantial returns by visiting Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the next major market move.