May 20, 2026

The Hidden Fault Line in the Clean Energy Supply Chain

The global pivot toward electrification has produced one of the most significant, yet least visible, strategic vulnerabilities in modern industrial history. While governments and corporations have poured trillions of dollars into wind turbines, solar panels, and electric vehicle fleets, the mineral foundations underpinning all of these technologies have received a fraction of the corresponding investment or strategic attention.

That imbalance is now correcting rapidly, and the correction is being driven not by climate ambition alone, but by something far older: the calculus of national security. According to the International Energy Agency, approximately 80% of energy experts ranked energy security as their top policy concern in 2025, placing it ahead of both emissions reduction and energy affordability. This striking data point signals that the strategic framing around critical minerals and energy security has undergone a genuine paradigm shift, not merely a rhetorical one.

Nickel sits at the epicenter of this shift. Once evaluated primarily through the lens of stainless steel production and industrial cycles, nickel is now being reassessed as a foundational input to high-energy-density battery chemistries, particularly nickel-manganese-cobalt (NMC) formulations that power the majority of premium electric vehicles on the road today. Demand for battery-grade nickel is growing at a double-digit annual rate, and total clean energy nickel demand is projected to more than double by 2030, according to IEA modelling.

Against this backdrop, the AEMC Nikolai nickel project in interior Alaska is attracting serious strategic attention for reasons that go well beyond its resource tonnage.

When big ASX news breaks, our subscribers know first

Why Global Nickel Supply Is More Fragile Than It Appears

The Indonesia-China Concentration Problem

Most commodity analysts focus on headline supply figures when assessing nickel market health. What those figures obscure is the geographic and processing concentration that makes Western clean energy supply chains deeply exposed to geopolitical disruption.

Understanding nickel's strategic importance helps explain why a large proportion of global nickel mine supply originating from Indonesia creates such concern. China, furthermore, controls a substantial share of global nickel refining capacity and battery precursor chemical production. This dual concentration at both the mining and refining stages means that disruption in either geography can cascade through the entire battery manufacturing ecosystem simultaneously.

This is structurally different from the oil market, which has spent decades building diversified supply infrastructure, strategic reserve systems, and geopolitical management frameworks. The nickel supply chain possesses none of those buffers at comparable scale. Consequently, Indonesian nickel supply challenges leave the market acutely exposed to the kind of shock events that policymakers in Washington, Brussels, and Tokyo are now urgently attempting to address.

The Scarcity Premium on Sulphide Deposits

Compounding the geographic concentration problem is a deposit-type problem that receives far less mainstream attention. The global nickel market has bifurcated into two structurally distinct tiers:

- Laterite nickel deposits account for the majority of global nickel resources. They require high-pressure acid leaching (HPAL) or rotary kiln electric furnace (RKEF) processing, both of which are energy-intensive, capital-heavy, technically complex, and generate significant carbon emissions.

- Sulphide nickel deposits are rarer and can be processed using conventional flotation and smelting methods, producing high-purity Class 1 nickel with meaningfully lower carbon intensity and reduced technical risk compared to laterite processing pathways.

The battery sector specifically requires Class 1 nickel, which meets the purity thresholds necessary for cathode active material production. Laterite-sourced nickel can theoretically be upgraded to Class 1 through HPAL, but the process economics are challenging, the capital requirements are substantial, and the carbon footprint runs contrary to the Scope 3 emissions reduction obligations that major automakers are now contractually committed to.

Most historically significant nickel sulphide deposits globally, including the Sudbury Basin in Canada, the Norilsk complex in Russia, and the Kambalda field in Western Australia, are either mature operations with declining grades or situated in jurisdictions that carry their own political or ESG complications. This narrowing pipeline of new, high-quality sulphide resources is precisely what is driving a structural scarcity premium into the market.

Key Insight: The distinction between sulphide and laterite nickel is not merely geological. It is increasingly a commercial, regulatory, and geopolitical filter that determines which projects qualify for premium offtake agreements, ESG-aligned capital, and government strategic support programmes.

AEMC Nikolai Nickel Project: Scale, Structure, and Strategic Position

Resource Scale in the U.S. Context

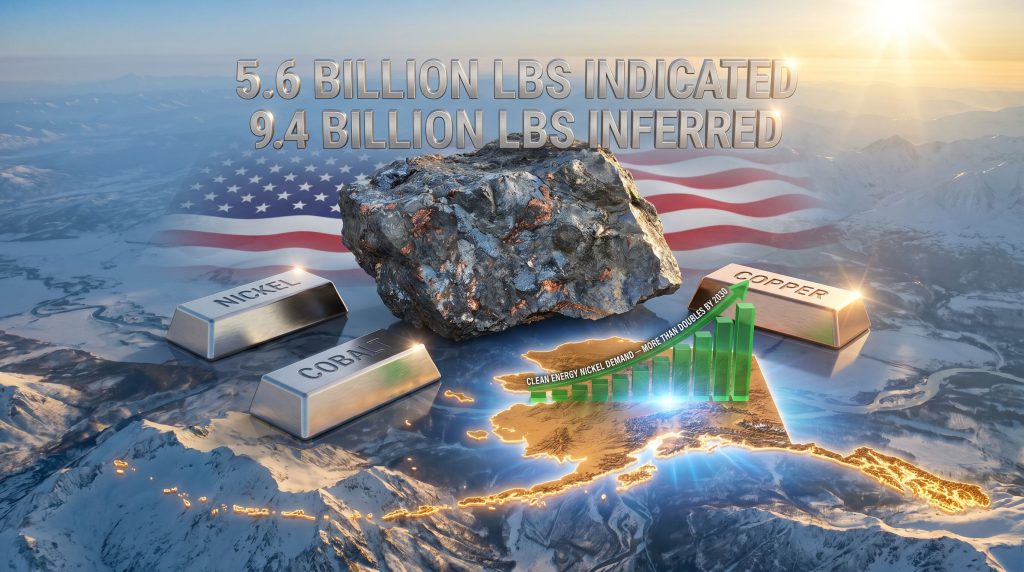

The Nikolai project, operated by Alaska Energy Metals Corporation (AEMC), is a sulphide-hosted nickel and battery metals deposit situated in interior Alaska. Its NI 43-101 compliant resource estimate establishes it as one of the largest known nickel resources within the United States:

| Resource Category | Nickel Pounds |

|---|---|

| Indicated Resource | 5.6 billion lbs |

| Inferred Resource | 9.4 billion lbs |

| Total Combined | ~15 billion lbs |

| Deposit Type | Sulphide (battery-grade capable) |

| Jurisdiction | Alaska, USA |

| Co-Products | Copper, Cobalt, Platinum Group Metals |

NI 43-101 is the internationally recognised standard for mineral resource reporting applied in Canada and the United States, providing a standardised framework for resource classification that institutional investors and technical analysts use as a credibility benchmark.

The combination of resource scale, deposit quality, and jurisdictional location within the continental United States gives the AEMC Nikolai nickel project a profile that very few comparable projects globally can replicate. The domestic address matters enormously in a policy environment where supply chain localisation has moved from an aspirational goal to an active legislative and procurement priority.

Geographic Proximity to U.S. Battery Manufacturing

The United States is undergoing a rapid expansion of domestic battery manufacturing capacity. New gigafactory developments are being established to serve both electric vehicle production and grid-scale energy storage systems. These facilities require reliable, proximate, and traceable mineral inputs to operate competitively.

Nikolai's Alaskan location reduces logistical exposure and transportation risk compared to supply sourced from Southeast Asia or processed through Chinese refineries. This proximity to North American manufacturing corridors is a structural advantage that becomes more valuable as supply chain localisation policies gain legislative traction.

The Defense Production Act Connection: What a MET Rating Actually Means

One of the most significant, and least widely understood, dimensions of the Nikolai project's current development trajectory is its engagement with U.S. federal defence procurement frameworks.

Through the Department of Defense's Defense Industrial Base Consortium (DIBC), AEMC submitted a proposal for the Nikolai project under the Defense Production Act Title III funding programme. The submission received a "MET" rating, indicating the project satisfied the programme's eligibility criteria. Defense Production Act support through requests for more detailed proposals under this funding pathway could commence as early as May 2026.

Defense Production Act Title III authority allows the U.S. government to fund domestic industrial capacity development for materials deemed critical to national defence. A MET rating does not guarantee funding, but it confirms that the project has cleared a meaningful eligibility threshold within a programme specifically designed to de-risk domestic critical mineral supply chains.

Separately, the Department of Energy launched a $500 million funding initiative targeting domestic battery supply chains and critical minerals processing capacity, creating additional potential pathways for projects with Nikolai's profile to access non-dilutive capital.

Important Note: A MET rating under the DIBC process represents an eligibility determination, not a funding commitment or project endorsement. Investors should not interpret federal programme submissions as confirmation of financial support unless explicitly awarded and confirmed by both the company and the relevant government agency.

The Multi-Metal Dimension: Why Co-Products Matter Strategically

A detail that often gets underweighted in assessments of the Nikolai project is its multi-metal composition. Beyond nickel, the deposit hosts economically meaningful quantities of copper, cobalt, and platinum group metals (PGMs), each of which occupies a distinct and critical node within the clean energy supply chain.

| Co-Product | Primary Clean Energy Application | Additional Strategic Relevance |

|---|---|---|

| Copper | EV wiring, grid infrastructure, renewables | Faces its own structural supply deficit through 2030 |

| Cobalt | NMC cathode chemistry alongside nickel | Supply heavily concentrated in the DRC |

| Platinum Group Metals | Hydrogen fuel cells, catalytic converters | Emerging green hydrogen demand driver |

This multi-metal profile serves two important functions. First, it provides revenue diversification that improves project economics and resilience against single-commodity price cycles. Second, it reduces the number of separate supply chain dependencies that downstream manufacturers must manage, making Nikolai a more compelling potential offtake partner for battery and automotive companies seeking consolidated supply solutions.

Domestic Refining: The Hydrometallurgical Dimension

A less-discussed but strategically significant element of AEMC's development approach involves exploring a domestic refining concept for the Nikolai project. The company has worked with RecycLiCo to test hydrometallurgical refining methods applicable to nickel, cobalt, and platinum group metals.

If validated, this processing approach would allow the project to produce refined battery-grade material within the United States rather than exporting concentrate for overseas processing. This distinction matters enormously from a policy perspective. The current U.S. critical minerals strategy explicitly targets the development of full, end-to-end domestic supply chains, meaning projects that can demonstrate refining capability within U.S. borders carry significantly enhanced strategic value compared to concentrate-only operations.

The key technical milestones that must be achieved before this concept can be formally incorporated into project economics include:

- Confirmation of sulphide metallurgical recoveries through ongoing testing programmes

- Demonstration of achievable concentrate purity specifications meeting battery-grade thresholds

- Comparative economic assessment of domestic refining versus conventional concentrate export

- Capital requirement modelling for refinery infrastructure within the Alaskan operating context

The next major ASX story will hit our subscribers first

Development Pathway and Key Risk Factors

Where the Project Stands Today

The Nikolai project is currently in the advanced exploration and pre-economic study phase. The development sequence from current status to potential production involves several clearly defined stages:

- Completed: NI 43-101 compliant resource estimate (5.6 billion lbs indicated + 9.4 billion lbs inferred nickel)

- In Progress: Metallurgical studies confirming processing routes, recovery rates, and concentrate specifications

- Planned: Options study evaluating alternative development configurations and processing scenarios

- Next Major Milestone: Preliminary Economic Assessment (PEA), the first formal evaluation of the project's economic viability

Risk Factors Investors and Observers Should Monitor

Early-stage mineral development projects carry a distinct and substantial risk profile that differs fundamentally from producing assets. The key risk dimensions for the AEMC Nikolai nickel project include:

- Metallurgical outcome risk: Processing test results will materially determine whether the project's sulphide mineralisation responds to flotation efficiently enough to justify development

- Commodity price sensitivity: Nickel has experienced significant price volatility in recent years; the project's economics will be sensitive to long-term nickel price assumptions used in any future feasibility studies

- Capital requirements: Moving from resource estimate through PEA, pre-feasibility study, and eventual construction will require substantial capital across multiple rounds, the terms of which remain undetermined

- Permitting timeline uncertainty: Federal environmental review processes introduce timeline variability even within jurisdictions generally supportive of resource development

- No production decision made: No mine construction or production timeline has been confirmed; the project remains a development-stage asset

⚠ Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice or a solicitation to buy or sell securities. Early-stage mineral exploration and development companies carry significant investment risk, including the potential loss of invested capital. Readers should conduct independent research and consult a qualified financial adviser before making any investment decisions. Forward-looking statements, timelines, and projections referenced in this article are subject to material risks and uncertainties.

Nickel's Structural Transformation: From Cyclical Commodity to Strategic Asset

The longer-term investment and policy case for projects like the AEMC Nikolai nickel project rests on a structural market transformation that extends well beyond the near-term price cycle.

Historically, nickel pricing was anchored to stainless steel demand, which follows industrial production and construction cycles with reasonable predictability. Battery demand has, however, introduced a fundamentally different pricing dynamic: one where strategic security premiums, ESG compliance requirements, and geopolitical risk factors co-price the metal alongside traditional supply-demand fundamentals.

Several behavioural shifts in how industrial buyers approach nickel procurement reflect this transformation:

- Major automakers and cell manufacturers are signing long-term supply agreements years ahead of production requirements, accepting higher prices in exchange for supply certainty

- Vertical integration across the supply chain, where battery manufacturers or automakers take equity stakes in upstream mining projects, is accelerating as a risk management strategy

- ESG-aligned procurement frameworks at large corporations are actively disqualifying supply sourced from high-emission or geopolitically opaque jurisdictions, creating a bifurcated demand pool with differentiated pricing

These shifts mean that nickel assets are increasingly evaluated on dimensions beyond cost and scale alone. Location, carbon footprint, processing pathway, and alignment with national industrial strategy are becoming co-equal factors in how projects are valued by potential partners, offtakers, and investors. For a broader overview of how this dynamic is reshaping supply chains, the analysis from CarbonCredits.com provides useful additional context.

In this evolving framework, a domestic U.S. sulphide deposit of Nikolai's scale, with its multi-metal exposure, low-carbon processing pathway, and active engagement with federal defence and energy programmes, is positioned at an intersection of forces that did not exist in nickel markets a decade ago. Whether that positioning translates into realised economic value will ultimately depend on the outcome of metallurgical studies, economic assessments, and the broader trajectory of U.S. critical minerals policy through the latter half of the 2020s.

This content is disseminated on behalf of Alaska Energy Metals Corporation. New Era Publishing Inc. and/or CarbonCredits.com received a one-time payment of $75,000 to provide marketing services for a term of three months. This article does not constitute an offer to sell or a solicitation to buy any securities. All resource estimates referenced are NI 43-101 compliant as reported by the company. Readers are encouraged to review the company's filings on SEDAR+ at www.sedarplus.ca before making any investment decisions.

Ready to Identify the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex resource data into actionable investment insights for both short-term traders and long-term investors. Explore historic discoveries and the substantial returns they generated, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.