May 22, 2026

Two Continents, One Corridor: The Case for a Formal Africa South America Energy Partnership

The global energy map is being redrawn, and the redrawn lines do not run exclusively between the traditional power centres of the Northern Hemisphere. Across both sides of the Atlantic, two of the world's most resource-abundant regions are beginning to recognise something that decades of geopolitical framing had obscured: their energy challenges, technical capabilities, and investment timelines are far more complementary than they are competitive. The emerging Africa South America energy partnership is not simply a diplomatic talking point. It reflects a structural convergence driven by capital cycles, technical expertise gaps, and a shared appetite for development pathways that do not depend on Northern-hemisphere conditionality.

When big ASX news breaks, our subscribers know first

Africa's Upstream Investment Cycle: Scale, Geography, and Opportunity

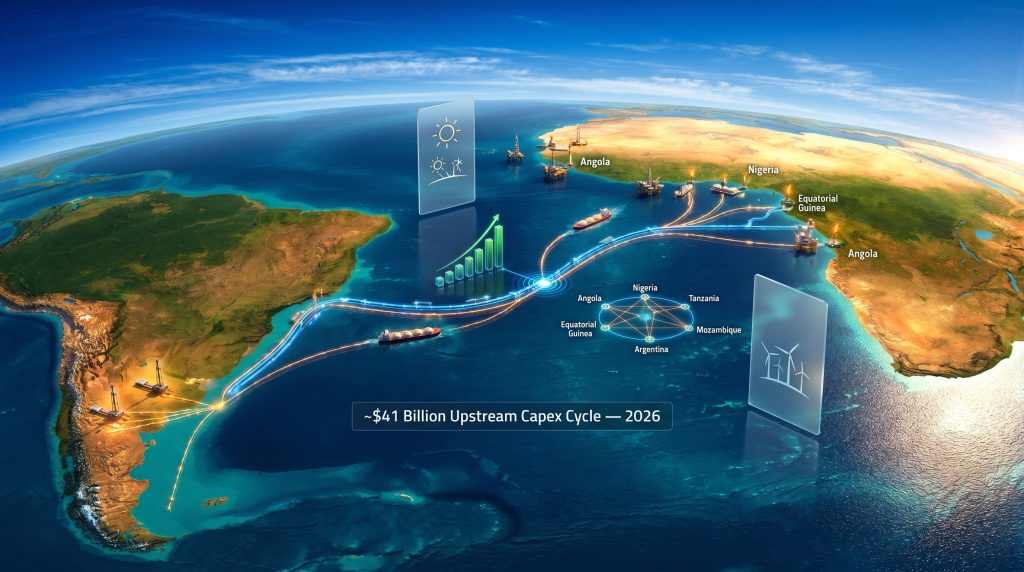

Africa is entering one of its most concentrated upstream capital expenditure periods in recent memory. Projected upstream spending across the continent for 2026 sits at approximately $41 billion, supported by active licensing rounds and accelerating exploration activity across multiple jurisdictions. This is not a single-country phenomenon. The investment is distributed across a geographically and geologically diverse set of markets, each with distinct resource profiles and development timelines.

| Country | Primary Resource Focus | Key Development Driver |

|---|---|---|

| Angola | Deepwater oil, gas monetisation | IOC re-engagement, new licensing rounds |

| Nigeria | LNG expansion, offshore blocks | Export capacity growth, infrastructure upgrades |

| Tanzania | Undeveloped gas reserves | LNG project pipeline development |

| Algeria | Conventional and unconventional gas | Domestic demand management, export diversification |

| Sierra Leone | Frontier exploration acreage | Early-stage licensing and seismic activity |

| Equatorial Guinea | Regional gas hub strategy | LNG aggregation and processing ambitions |

| Mozambique | Large undeveloped gas fields | Long-term LNG export development |

Key Insight: The breadth of this capex cycle means the opportunity extends well beyond the continent's established oil producers. Frontier markets and undeveloped gas basins represent a significant portion of the investable universe, and that is precisely where South American technical expertise becomes most relevant.

What distinguishes this investment cycle from previous African upstream booms is the growing centrality of gas monetisation as a strategic objective. While oil has historically dominated the conversation, the pipeline of LNG-focused projects in Mozambique, Nigeria, and Tanzania signals that African governments and their national oil company partners are now thinking seriously about how to convert stranded gas reserves into long-term export revenue.

This shift in upstream strategy is one of the primary catalysts drawing South American operators and technical service providers into the African conversation. Furthermore, the LNG supply outlook for 2025 and beyond reinforces why African gas monetisation has become such a strategic priority for cross-regional investment.

Vaca Muerta as a Technical Blueprint: What Argentina Has Built and Why It Matters

Argentina's Vaca Muerta formation has undergone a transformation that few unconventional plays outside North America have managed to replicate. From an underexplored frontier prospect to a globally recognised shale benchmark, Vaca Muerta now represents one of the most technically refined unconventional development environments outside the United States. The operational capabilities accumulated through years of horizontal drilling campaigns, multi-stage hydraulic fracturing programs, water management systems, and well completion optimisation have positioned Argentina as a credible technical peer to any shale-producing nation.

This matters enormously for African unconventional development, where resource potential is substantial but technical readiness lags significantly behind. The structural gaps in African shale and tight gas development today include:

- Limited domestic expertise in horizontal well design and hydraulic fracturing execution

- Underdeveloped oilfield services ecosystems capable of supporting unconventional completions at scale

- Infrastructure deficits spanning pipeline networks, water sourcing logistics, and gas processing facilities

- Regulatory frameworks that have not yet been adapted to the specific risk profiles and operational requirements of unconventional resource development

The African Energy Chamber has specifically highlighted Vaca Muerta as an example of operational experience that could directly support African shale and tight gas projects through technology transfer and drilling expertise. The logic is straightforward: Argentina has already absorbed the learning curve costs that African producers would otherwise face independently.

A structured technical collaboration between Argentine operators and African national oil companies could realistically compress unconventional development timelines by several years. Such arrangements might cover well design methodology, completion technology protocols, and hands-on operational training programs. Financing structures for cross-regional technical agreements of this kind have precedents in Asia-Africa and Middle East-Africa energy cooperation models, where development bank financing from institutions such as the African Development Bank and CAF has helped bridge the initial capital commitment gap.

The ARPEL Conference: Industry Diplomacy in Action

The ARPEL Conference, scheduled for June 1 to 4, 2026 in Buenos Aires, represents a pivotal venue for cross-regional upstream dialogue. ARPEL, which has served as the cooperative framework for Latin American and Caribbean petroleum industries since 1965, provides an institutional platform that formal government-to-government negotiations rarely match in terms of speed or operational flexibility.

The African Energy Chamber's planned engagement at the Buenos Aires event reflects a deliberate strategy of using industry-led diplomacy to pre-position investment relationships before formal bilateral frameworks are in place. This approach has several practical advantages over treaty-based processes:

- Speed: Chamber-led and private-sector negotiations can reach heads of agreement in months, while government treaty processes can take years.

- Flexibility: Non-binding cooperation frameworks allow both parties to structure phased commitments, reducing early-stage financial exposure.

- Risk distribution: Joint technical studies and pilot programs spread the cost of early-stage uncertainty across multiple participants.

- Adaptability: Industry forums can pivot quickly as market conditions, commodity prices, and regulatory environments evolve.

The African Energy Chamber's executive leadership is expected to engage directly with regional operators and industry decision-makers during the Buenos Aires event, advancing upstream collaboration opportunities that span both conventional and unconventional resource plays.

LNG: The Central Pillar of Cross-Regional Energy Collaboration

If unconventional development is the long-term technical partnership opportunity, LNG is the near-term commercial priority. The undeveloped gas reserves held by Mozambique and Nigeria alone represent a supply potential that, if successfully monetised, would have meaningful implications for global LNG trade balances. South American operators with experience in export infrastructure development and gas processing represent natural technical and commercial partners for African LNG project proponents.

Nigeria's ambitions to expand LNG export capacity have been a recurring theme in African energy planning for years, but infrastructure constraints and project financing complexity have repeatedly slowed execution. Mozambique's resource base is substantial, but the project development path has faced well-documented security and financing challenges. Both countries, and others in sub-Saharan and North Africa, are actively seeking partners who can contribute more than capital alone.

This is where the Africa South America energy partnership framing gains its most immediate commercial traction. Argentine and Brazilian operators bring LNG-adjacent expertise, unconventional gas development capabilities, and a track record of navigating complex frontier project environments that is directly applicable to African market conditions. In addition, the shifting geopolitical mining landscape is further reinforcing the strategic logic behind South-South resource collaboration.

Renewable Energy: The Dimension That Broadens the Partnership Beyond Hydrocarbons

The hydrocarbon narrative, while dominant, represents only part of the cross-regional opportunity. Both Africa and South America possess renewable resource endowments of extraordinary scale, and the symmetry between the two regions extends well beyond oil and gas.

| Renewable Resource | African Scale | South American Parallel |

|---|---|---|

| Solar (utility-scale) | Saharan and sub-Saharan irradiance corridors | Atacama Desert, Brazilian cerrado |

| Wind (onshore and offshore) | East African Rift, South African coastline | Patagonian wind corridor |

| Hydropower | Congo Basin, Zambezi River system | Amazon tributaries, Andean river systems |

| Green Hydrogen | North African coastal export zones | Chilean and Argentine production hubs |

South America, particularly Chile and Argentina, has developed sophisticated renewable energy auction frameworks and accumulated operational experience managing variable renewable generation at grid scale. These are precisely the regulatory and operational challenges that African nations are currently working through as they scale up renewable capacity. The advancement of renewable energy solutions across both continents is consequently becoming a natural bridge for cross-regional knowledge exchange.

A peer-learning exchange between the two regions could accelerate African renewable energy deployment without the conditionality often attached to Northern-hemisphere development financing. Furthermore, the Africa-EU Energy Partnership provides a useful institutional reference point for how formal cross-regional energy frameworks can be structured to support long-term investment.

Green hydrogen presents a particularly interesting convergence point. Both North Africa and the Southern Cone of South America are being positioned as potential green hydrogen export hubs for European markets. Shared experience in electrolyser deployment, coastal export infrastructure design, and offtake agreement structuring could make bilateral cooperation on this emerging value chain commercially productive well before either region reaches full export scale.

How Does Critical Minerals Fit Into the Broader Picture?

Beyond energy, the critical minerals demand driven by the global energy transition is adding another dimension to cross-regional collaboration. Both Africa and South America hold significant deposits of battery metals and transition minerals, creating further incentive for shared investment frameworks. Similarly, advances in direct lithium extraction technology are making South American lithium resources increasingly relevant to African battery supply chain ambitions.

The next major ASX story will hit our subscribers first

Structural Barriers and Why They Are Not Insurmountable

An honest assessment of the Africa South America energy partnership must acknowledge the obstacles alongside the opportunities. The barriers are real:

- There is currently no overarching multilateral framework binding African and South American energy sectors in the way that the Africa-EU Energy Partnership or Power Africa structures link the continent to Northern-hemisphere institutions.

- Cross-regional project finance requires navigating multiple currency regimes, divergent sovereign risk profiles, and the mandates of different development banking institutions simultaneously.

- Physical distance between the two continents increases mobilisation costs for equipment, personnel, and technical support.

- Regulatory heterogeneity across both continents creates complexity for operators seeking to establish standardised operating models.

However, none of these barriers is fundamentally different from the obstacles that have been overcome in other South-South energy cooperation frameworks. Asia-Africa energy investment has scaled significantly over the past two decades despite similar structural challenges. The multilateral development bank ecosystem, including the African Development Bank, CAF, and the Inter-American Development Bank, provides financing architecture that can bridge gaps that private capital alone cannot close.

Digital collaboration tools are also reducing the friction associated with cross-hemispheric technical knowledge transfer in ways that were not available during earlier rounds of South-South cooperation. Remote drilling supervision, digital twin technology, and cloud-based reservoir modelling allow technical expertise to be applied across geographic distances that would previously have required permanent on-site teams. According to research on energy security across South America and Africa, structural complementarity between the two regions represents a meaningful and underutilised foundation for durable cooperation.

Analytical Note: The absence of a formal bilateral framework should be understood as a starting point for institutional development, not a structural ceiling on cooperation. The most durable South-South energy partnerships of the past two decades began as industry-forum relationships before graduating into formal investment agreements.

Frequently Asked Questions: Africa South America Energy Partnership

What is driving the push for an Africa South America energy partnership in 2026?

Africa's approximately $41 billion upstream capex cycle for 2026, combined with South America's proven unconventional development expertise and a broader geopolitical shift toward South-South cooperation, is creating the conditions for expanded cross-regional energy collaboration. The African Energy Chamber is actively promoting these connections ahead of the ARPEL Conference in Buenos Aires.

Which African countries are most relevant to South American energy investors?

Angola, Nigeria, Tanzania, Mozambique, Algeria, Sierra Leone, and Equatorial Guinea represent the most active markets, spanning deepwater oil, LNG development pipelines, and emerging unconventional gas plays. Each country offers a distinct risk-return profile and development timeline.

How does Argentina's Vaca Muerta experience apply to African unconventional development?

Vaca Muerta has established Argentina as a global benchmark for shale and tight gas development. The technical capabilities developed there, covering horizontal drilling, hydraulic fracturing, and completion optimisation, are directly transferable to African tight gas and shale prospects that currently lack domestic technical capacity.

Is there a formal Africa South America energy partnership agreement currently in place?

As of mid-2026, no single overarching bilateral framework exists. Cooperation is advancing through industry forums, chamber-led diplomacy, and project-specific technical agreements rather than formal government-to-government treaties.

What role does LNG play in the Africa South America energy relationship?

LNG is the most immediate commercial opportunity, with African nations including Mozambique and Nigeria holding significant undeveloped gas reserves. South American operators and technical service providers represent credible partners for developing export infrastructure and advancing gas monetisation strategies.

How do renewable energy opportunities factor into cross-regional cooperation?

Both regions possess complementary renewable resource bases across solar, wind, hydropower, and green hydrogen potential. Opportunities exist for shared regulatory learning, joint investment frameworks, and collaborative clean energy development that extends the partnership narrative well beyond hydrocarbons.

Disclaimer: This article contains forward-looking analysis and projections related to energy investment trends and cross-regional cooperation frameworks. Such projections involve inherent uncertainty and should not be construed as financial or investment advice. Capital expenditure figures and project timelines are subject to change based on commodity price movements, regulatory developments, and project financing conditions.

Want To Be First When Major Resource Discoveries Hit the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across the commodities driving the global energy transition — from critical minerals to gas and beyond. Explore historic discoveries and their exceptional returns, then start your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.