July 31, 2026

Why Crude Oil Prices Cannot Normalise Quickly — Even If US-Iran Peace Talks Succeed

Every major oil price shock in modern history eventually resolves. Crises pass, pipelines reopen, tankers resume their routes, and benchmarks drift back toward equilibrium. However, the mechanism through which resolution translates into price normalisation is rarely instantaneous — and the current disruption to Strait of Hormuz flows presents a uniquely complex set of structural constraints. Understanding why oil prices and US-Iran peace talks remain so deeply intertwined requires moving beyond the headlines and examining the physical, logistical, and financial architecture that underpins global crude markets.

When big ASX news breaks, our subscribers know first

The Strait of Hormuz: A Chokepoint That Concentrates Systemic Risk

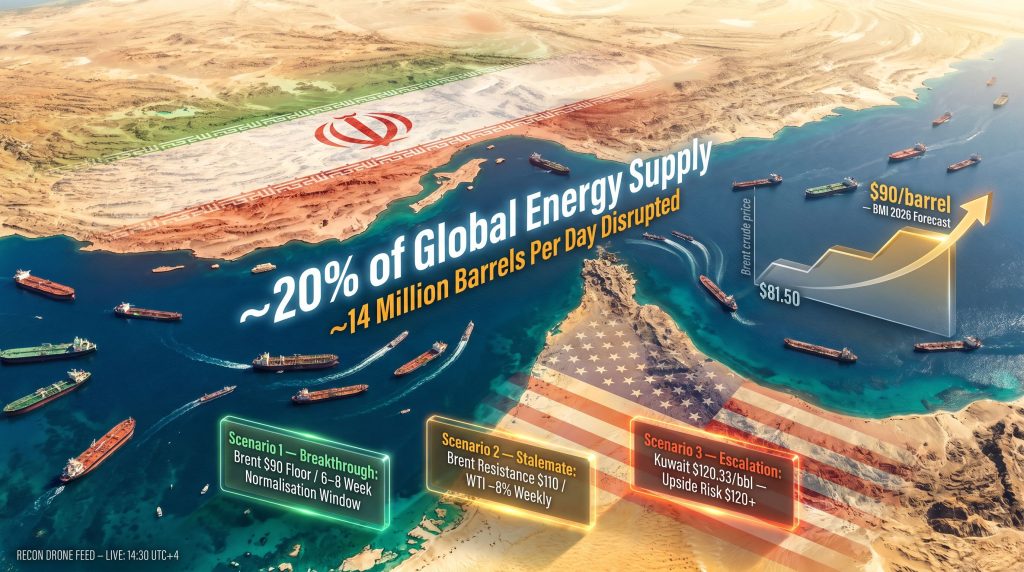

The Strait of Hormuz is a navigational channel roughly 33 kilometres wide at its narrowest navigable point, connecting the Persian Gulf to the Gulf of Oman and, from there, to global shipping lanes. Its strategic significance is not merely geographic — it is structural. Unlike other potential maritime bottlenecks, the Strait has no viable alternative routing for the combined export volumes of Saudi Arabia, Iraq, the UAE, and Kuwait.

Before the current conflict disruption, approximately 20% of total global energy supply transited this passage, encompassing crude oil, refined petroleum products, and liquefied natural gas. The scale of what has been removed from accessible markets is therefore extraordinary: an estimated 14 million barrels per day, representing roughly 14% of total global oil supply, has effectively been locked out of normal distribution channels.

| Supply Variable | Estimated Volume | Share of Global Supply |

|---|---|---|

| Pre-conflict Hormuz transit volume | ~20% of global energy supply | Includes crude, products, LNG |

| Oil removed from market due to disruption | ~14 million barrels per day | ~14% of global supply |

| BMI revised 2026 Brent average forecast | $90 per barrel | Up from prior $81.50 estimate |

| Projected timeline for full flow restoration | Q1–Q2 2027 (earliest) | Assumes no further damage |

What this data reveals is that the Hormuz disruption is not a marginal supply shock. It is a categorical removal of a significant portion of the world's most liquid crude streams from the global balancing system. Furthermore, no amount of diplomatic progress can instantly reverse this physical reality. The geopolitical oil price drivers at play here are deeply structural, not merely headline-driven.

Three Diplomatic Scenarios and Their Price Implications

Framing current oil price behaviour through scenario analysis — rather than reactive headline tracking — offers investors and analysts a far more durable interpretive framework. Understanding where crude benchmarks are likely to trade over the coming quarters depends heavily on which of these three paths emerges.

Scenario 1: A Genuine US-Iran Breakthrough

A successful agreement would require resolution on two core technical issues that remain fundamentally contested: the disposition of Iran's enriched uranium stockpile and the question of navigation controls over the Strait of Hormuz. US Secretary of State Marco Rubio has acknowledged positive signals in the negotiation process, and senior Iranian diplomatic sources have indicated that gaps with Washington have narrowed.

A coordinated Qatari negotiating team has engaged directly in Tehran as part of a US-aligned diplomatic effort, while Pakistan's military leadership has conducted parallel engagement with Iranian counterparts through a separate track. Yet even under the most optimistic resolution scenario, BMI (a unit of Fitch Solutions) models a six-to-eight week post-conflict normalisation window before supply flows begin recovering in any meaningful way.

"A peace deal announcement would almost certainly trigger a sharp speculative sell-off in crude futures as traders unwind risk-premium positions. But the physical reality of damaged Gulf energy infrastructure, depleted global inventories, and logistical restoration timelines would prevent benchmarks from returning to pre-conflict levels for multiple quarters — meaning any initial price drop following a breakthrough could represent a buying opportunity for medium-term energy exposure."

Scenario 2: Prolonged Stalemate and the Persistent Risk Premium

A frozen conflict scenario — where active hostilities cease but no formal agreement is reached — creates a durable supply-risk premium embedded in crude benchmarks without any clear resolution catalyst. PVM Oil Associates has highlighted the market tension between optimism around an imminent truce and the consistent bearish sentiment that re-emerges whenever Brent crude approaches $110 per barrel.

Weekly price volatility during the current period has been severe: Brent declined more than 5% on a weekly basis while WTI fell approximately 8% as diplomatic expectations oscillated between cautious optimism and renewed scepticism. This pattern reflects not irrational market behaviour but rather a rational response to asymmetric and frequently contradictory diplomatic signals. In addition, OPEC's market influence continues to shape how these competing pressures resolve across the forward curve.

Scenario 3: Escalation and the Path to $120+ Crude

If talks break down entirely — driven by irreconcilable differences over Iran's enriched uranium stockpile or contested sovereignty claims — the upside price risk becomes substantial. Kuwait's crude benchmark, already trading at $120.33 per barrel before a modest decline, provides a real-world illustration of where the upper range of current market pricing sits.

Critically, OPEC+ production increases cannot compensate for Hormuz-disrupted volumes. Several of the seven leading OPEC+ producers expected to agree on a modest output hike for July at their June 7 meeting are themselves directly affected by the conflict, meaning their deliverable supply remains constrained regardless of what headline production decisions are announced.

The Infrastructure Recovery Problem: Why 2027 Is the Realistic Timeline

One of the most underappreciated dimensions of the current oil price environment is the distinction between conflict resolution and supply normalisation. These are two entirely separate events with very different timelines.

The head of UAE state oil firm ADNOC has assessed that complete restoration of Strait of Hormuz throughput cannot realistically occur before the first or second quarter of 2027, even under a scenario where the conflict ends immediately. This assessment is grounded in the physical realities of Gulf energy infrastructure recovery:

- Upstream production resumption requires safety inspections of wellheads, platforms, and gathering systems that may have sustained damage or been placed in shutdown configurations.

- Midstream pipeline and terminal restoration involves integrity assessments across hundreds of kilometres of critical infrastructure that cannot be rushed without creating new safety and environmental risks.

- Downstream terminal operability must be confirmed before export volumes can reliably reach tanker loading facilities.

- Tanker scheduling and cargo programming requires weeks of lead time to rebuild regular shipping rotations once loading terminals are confirmed operational.

Each stage of this cascade creates compounding delays. The six-to-eight week normalisation window modelled by BMI represents a best-case scenario, not a central expectation. This is precisely why BMI's revised average 2026 Brent crude forecast of $90 per barrel — up from a prior estimate of $81.50 — incorporates the infrastructure repair lag as a core input rather than treating diplomatic resolution as synonymous with price resolution.

China, OPEC+, and the Inventory Depletion Acceleration

The supply-side picture is further complicated by the behaviour of two critical market actors: China and the OPEC+ coalition. China's refined fuel exports for June are projected to reach approximately 550,000 metric tons, only marginally above the roughly 500,000 metric tons estimated for May, according to trade sources cited by Reuters.

This restrained export posture reflects Beijing's prioritisation of domestic energy security over export revenue — a rational response to global supply tightness but one that removes a potential buffer from markets already under significant strain. The Asian LNG market pressures compounding this dynamic have further tightened the regional energy balance.

Meanwhile, global oil inventories are depleting at an accelerating pace as Hormuz flows remain constrained. As those buffers thin, the market's ability to tolerate additional disruptions without sharp price responses diminishes significantly.

The Macro Spillover: Oil Prices, Inflation, and the Rate-Hike Feedback Loop

The consequences of sustained crude prices in the $90 to $120 per barrel range extend well beyond the energy sector. For oil-importing economies, elevated energy costs transmit directly into headline consumer price inflation through transport, manufacturing, and utilities channels. This inflationary pressure raises the probability that central banks maintain or increase interest rates, tightening financial conditions across asset classes.

The feedback loop is particularly damaging for non-yielding assets. Gold, for instance, faces simultaneous headwinds from oil-driven inflation fears boosting rate-hike expectations — a dynamic that illustrates how a single geographic chokepoint can generate cascading effects across seemingly unrelated financial markets. Furthermore, the trade war oil impact is amplifying these macro pressures, creating a more complex and interconnected set of risks for policymakers globally.

| Economy Type | Primary Oil Price Impact | Key Structural Vulnerability |

|---|---|---|

| GCC oil exporters (Saudi Arabia, UAE, Kuwait) | Revenue windfall at elevated prices | Physical export disruption via Hormuz |

| Asian importers (China, Japan, South Korea) | Rising import costs, inflationary pressure | Refinery feedstock shortages |

| European importers | Energy security concerns, LNG substitution | Limited alternative routing capacity |

| Global shipping and logistics | Freight cost escalation | Hormuz rerouting delays and insurance premiums |

A ceasefire that has been nominally in effect for approximately six weeks has failed to generate meaningful economic relief. The distinction between a cyclical price spike and a structurally elevated price environment is critical here: sustained high prices risk permanently altering consumption patterns and accelerating demand destruction in ways that could reshape long-term energy market fundamentals.

The next major ASX story will hit our subscribers first

Key Price Levels Every Energy Market Participant Should Monitor

Given the complexity of forces currently acting on crude benchmarks, a framework of reference price levels helps distinguish between noise and signal. The recent oil price rally has already demonstrated how quickly these levels can be tested and breached.

- $96.87/barrel (WTI): The US benchmark level reflecting approximately 8% weekly losses — indicative of significant intraday volatility and directional uncertainty rather than sustained bearish conviction.

- $103.75/barrel (Brent): The current trading level representing a 1.1% intraday gain, sitting at a technically balanced position between bullish supply-deficit fundamentals and bearish peace-deal speculation.

- $110/barrel (Brent resistance): The psychological ceiling at which bearish profit-taking consistently dominates, per PVM Oil Associates analysis, capping the upside of sustained rallies in the current environment.

- $120.33/barrel (Kuwait crude benchmark): A real-world data point illustrating the upper range of current Gulf market pricing and the plausible ceiling in an escalation scenario.

- $90/barrel (BMI 2026 floor forecast): The revised baseline that accounts for supply deficit, infrastructure repair lag, and the post-conflict normalisation window — functioning as a structural price floor rather than a cyclical mean.

Frequently Asked Questions: Oil Prices and US-Iran Peace Talks

Why do oil prices remain elevated even when US-Iran peace talks show progress?

Diplomatic progress reduces the probability of further supply disruption but does not address the existing physical deficit already embedded in the market. With approximately 14 million barrels per day removed from accessible supply and global inventories already depleting rapidly, even a confirmed peace agreement cannot immediately restore the volumes that have been lost. The market is pricing a structural supply gap, not merely a geopolitical risk premium that disappears upon handshake.

What are the two core obstacles preventing a rapid US-Iran agreement?

The fundamental unresolved issues are Iran's enriched uranium stockpile — particularly the volume and disposition of highly enriched material accumulated during the conflict period — and the question of sovereign navigation controls over the Strait of Hormuz. Both issues involve existential national security considerations for their respective parties, making rapid technical compromise structurally improbable despite reported progress on secondary negotiating dimensions.

How should investors interpret the sharp weekly losses in WTI and Brent alongside intraday gains?

Large weekly losses combined with periodic intraday recoveries reflect a market caught between two competing pricing signals: speculative positioning that prices in a peace deal scenario (bearish) and fundamental supply-deficit pricing that supports elevated benchmarks (bullish). When diplomatic optimism rises, speculative sellers dominate. When talks stall or sticking points resurface, fundamental buyers reassert. Neither force currently has sufficient conviction to establish a durable directional trend, which itself is informative — it suggests the market is genuinely uncertain rather than confidently positioned in either direction. Consequently, oil prices and US-Iran peace talks will continue to move in close tandem until a definitive resolution emerges.

"This article contains forward-looking analysis, scenario modelling, and price forecasts sourced from third-party analysts including BMI (Fitch Solutions) and PVM Oil Associates. These projections are subject to material revision as geopolitical conditions evolve. Nothing in this article constitutes financial advice. Readers should conduct independent research and consult qualified financial professionals before making investment decisions related to energy markets or commodity-linked assets."

Want To Stay Ahead of the Next Major Commodity Discovery?

While oil markets navigate geopolitical uncertainty, significant mineral discoveries on the ASX continue to create extraordinary investment opportunities — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment they're announced, turning complex data across 30+ commodities into clear, actionable insights. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin your 14-day free trial to ensure you're positioned ahead of the broader market.