July 30, 2026

Understanding Africa's Strategic Petroleum Foundation

Continental petroleum dynamics extend far beyond simple reserve tallies, encompassing complex geological systems, infrastructure networks, and economic interdependencies that shape regional energy security. The largest proven oil reserves in Africa represent approximately 7.5% of global proven reserves, yet the continent's influence on international energy markets derives not merely from resource quantity but from strategic positioning, production flexibility, and export capacity across diverse geological provinces.

The classification of petroleum reserves follows internationally standardised frameworks established by the Society of Petroleum Engineers, distinguishing between proven reserves with 90% extraction certainty, probable reserves with 50-90% confidence levels, and possible reserves carrying 10-50% geological risk. This technical hierarchy becomes critically important for investment decisions, as institutional capital allocation depends on reserve certainty rather than speculative resource potential.

Geological Survey Standards and Independent Verification

Reserve verification requires comprehensive seismic interpretation, well-log analysis, and production performance monitoring to establish economic extractability under current technological and market conditions. Independent third-party auditing examines pressure-volume-temperature analysis of reservoir fluids, decline curve projections, and enhanced recovery potential to validate reported figures against international standards.

The verification process becomes particularly complex in regions experiencing political instability, where comprehensive geological surveys face operational constraints. Libya's measurement infrastructure has deteriorated following the 2011 conflict, limiting the National Oil Corporation's capacity for frontier basin evaluation despite substantial unexplored potential across the Murzuq and Ghadames basins.

Economic Integration Across Continental Petroleum Sectors

Petroleum revenue dependency creates distinct fiscal patterns across African economies, with Libya deriving over 90% of government revenue from hydrocarbon sectors, while Nigeria historically generated similar proportions before diversification initiatives. This concentration exposes national budgets to global price volatility, creating boom-bust cycles that influence infrastructure development and social spending. Furthermore, this dependency has significant implications for energy exports challenges facing the continent.

The continental petroleum sector supports approximately 12 million direct and indirect jobs, spanning exploration, production, refining, transportation, and service industries. Revenue flows fund critical infrastructure including roads, ports, electrical grids, and telecommunications networks that enable broader economic development beyond the energy sector itself.

When big ASX news breaks, our subscribers know first

North African Hydrocarbon Supremacy and Continental Leadership

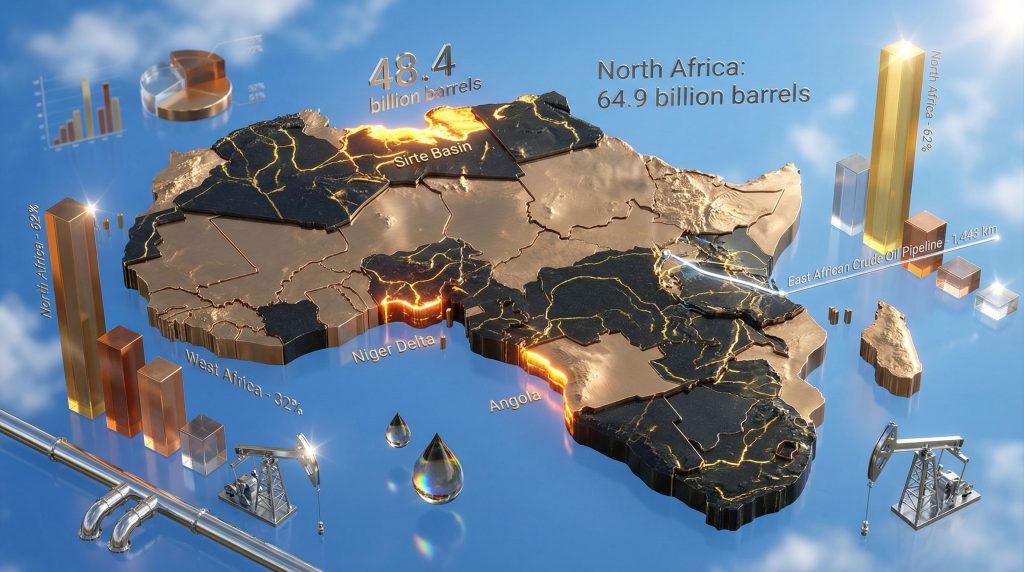

Libya maintains Africa's most substantial proven petroleum reserves at 48.4 billion barrels, representing the ninth-largest global endowment and establishing North African dominance over continental energy resources. The Sirte Basin contains approximately 35.2 billion barrels across multiple producing formations, while the Murzuq Basin holds 8.1 billion barrels and the Ghadames Basin contributes 5.1 billion barrels to national reserves.

Despite geological advantages, Libya's production capacity remains constrained by security challenges and infrastructure deterioration, with actual output fluctuating between 1.0-1.2 million barrels per day compared to pre-2011 capacity exceeding 1.6 million barrels per day. This 25-37% capacity deficit reflects operational disruptions rather than geological limitations, indicating substantial production recovery potential under improved stability conditions.

Algeria's Integrated Energy Infrastructure Strategy

Algeria's proven reserves of 12.2 billion barrels position the nation as Africa's third-largest petroleum holder, while state-owned Sonatrach operates an integrated value chain encompassing upstream exploration, midstream transportation, and downstream refining operations. This vertical integration enables revenue capture across multiple stages and provides strategic flexibility in export pricing and product mix optimisation.

| Algeria's Energy Infrastructure | Capacity/Output |

|---|---|

| Combined Refining Capacity | ~500,000 barrels/day |

| LNG Production Capacity | ~30 million tonnes/year |

| Primary Export Markets | Europe (via pipeline) |

| Integrated Operations | Upstream through downstream |

Sonatrach's pipeline networks connect Mediterranean export terminals with European markets, positioning Algeria as a critical energy security partner for continental European nations seeking supply diversification. The company's exploration programmes target enhanced oil recovery techniques in mature fields including Hassi Messaoud, Berkine, and Illizi basins to sustain long-term production trajectories.

Continental Energy Diplomacy Through Resource Management

Both Libya and Algeria participate in OPEC production impact coordination mechanisms, though compliance challenges arise from domestic fiscal pressures and infrastructure constraints. Libya's quota adherence depends on production stability, while Algeria balances OPEC discipline against European supply commitments and domestic revenue requirements.

The concentration of 64.9 billion barrels (62% of continental reserves) across North African producers creates regional influence over continental energy policy, infrastructure development priorities, and international partnership strategies. This geographic concentration shapes Africa's engagement with global energy markets and international oil companies seeking stable, high-volume production platforms.

West African Production Dynamics and Economic Integration

Nigeria maintains Africa's second-largest proven petroleum reserves at 36.9 billion barrels, ranking 11th globally and representing approximately 35.2% of continental reserves. The country's historical production capacity exceeded 2.5 million barrels per day before operational challenges reduced output to current levels of approximately 1.5-1.8 million barrels per day.

Production constraints stem from pipeline vandalism, petroleum theft estimated at 150,000-400,000 barrels per day during peak periods, and systematic underinvestment in infrastructure maintenance and security. These operational challenges reflect security instability and community grievances rather than geological limitations, as the underlying Niger Delta petroleum systems remain prolific across multiple fault-bounded structures.

Nigeria's Legislative Reform and Investment Framework

The Petroleum Industry Act represents Nigeria's most comprehensive energy sector reform, establishing clearer fiscal terms, enhanced transparency requirements, and targeted capital attraction initiatives. The legislation aims to generate $10 billion in new petroleum investment by 2027 through improved regulatory clarity, streamlined bidding processes, and competitive fiscal frameworks.

Nigeria's reform trajectory focuses on production stabilisation through enhanced security measures, infrastructure protection, and community engagement programmes designed to address underlying grievances affecting operational continuity.

Key reform elements include gradual subsidy withdrawal, increased local content requirements, and third-party reserve auditing standards that align with international best practices. These changes target sustained capital attraction and production recovery following decades of regulatory uncertainty and operational instability. Moreover, these developments occur amid growing concerns about oil price stagnation factors affecting global markets.

Angola's Offshore Development Model and Technology Adoption

Angola's 7.8 billion barrels of proven reserves rank 18th globally, with offshore deepwater fields accounting for over 80% of national production. The deliberate focus on marine petroleum systems reduces infrastructure vulnerability compared to onshore operations, though capital intensity increases significantly for deepwater development projects.

| Angola's Deepwater Projects | Specifications |

|---|---|

| Typical Water Depth | 800-2,500 metres |

| Primary Technology | FPSO vessels |

| Key Fields | Kizomba, Kuito, Saxi-Batuque |

| Security Advantage | Reduced terrestrial vulnerability |

Deepwater operations require sophisticated floating production, storage, and offloading systems, umbilical infrastructure, and specialised subsea completion technology capable of operating in harsh Atlantic conditions. This technological specialisation positions Angola as a stable West African producer despite broader regional volatility affecting onshore operations.

Emerging Producers and Infrastructure Development Strategies

Uganda represents continental petroleum development potential with 2.5 billion barrels of proven reserves concentrated in the Tilenga and Kingfisher fields. Unlike established producers, Uganda's petroleum sector remains under development, requiring substantial infrastructure investment before achieving meaningful export capacity.

The East African Crude Oil Pipeline Strategic Framework

The East African Crude Oil Pipeline (EACOP) represents Uganda's primary export route, extending 1,443 kilometres through Tanzania to Indian Ocean terminals with designed capacity of 216,000 barrels per day. The $5 billion total project investment demonstrates the infrastructure requirements for landlocked petroleum development and regional cooperation frameworks.

| EACOP Project Specifications | Details |

|---|---|

| Total Length | 1,443 kilometres |

| Design Capacity | 216,000 barrels/day |

| Project Investment | $5 billion |

| Route | Uganda to Tanzania coast |

EACOP development requires coordination between Uganda's petroleum policies, Tanzania's transit agreements, and international financing mechanisms. The project timeline extends through 2026-2028 for full operational capacity, representing a model for landlocked petroleum development across the continent.

Cross-Border Dependencies and Political Risk Factors

South Sudan's 3.75 billion barrels of proven reserves face unique monetisation challenges due to landlocked geography and pipeline dependencies through Sudan. Export infrastructure vulnerabilities create political and logistical risks that affect production planning and investment decisions.

Revenue-sharing agreements between South Sudan and Sudan include transit fees, processing charges, and political coordination mechanisms that influence petroleum economics beyond simple market pricing. These arrangements demonstrate how geographic constraints shape petroleum development strategies and regional cooperation requirements.

Regional Reserve Distribution and Strategic Implications

Continental petroleum reserves concentrate across three distinct geographical zones, creating strategic implications for infrastructure development, export logistics, and regional economic integration. North African reserves dominate with 64.9 billion barrels (62% of continental total), while West African holdings contribute 49.6 billion barrels (32%) and East/Central African regions contain 9.75 billion barrels (6%).

| Regional Reserve Analysis | Proven Reserves | Continental Share |

|---|---|---|

| North Africa | 64.9 billion barrels | 62% |

| West Africa | 49.6 billion barrels | 32% |

| East/Central Africa | 9.75 billion barrels | 6% |

This geographic distribution influences continental energy security strategies, as North and West African producers possess sufficient reserves for sustained export capacity, while East/Central African nations require infrastructure development and regional cooperation for effective resource monetisation. According to global oil reserves data, these regional concentrations place African nations among significant global petroleum holders.

Production Capacity versus Reserve Ratios Analysis

Reserve-to-production ratios indicate long-term sustainability of current extraction rates, with Libya maintaining over 50+ years at present production levels, Nigeria approximately 63 years, and Angola 16-17 years. These metrics demonstrate varying urgency for reserve replacement through exploration and enhanced recovery implementation.

Angola's lower reserve life index creates greater pressure for new discoveries and field development, while Nigeria and Libya possess longer reserve security that enables strategic production management and infrastructure optimisation. Investment requirements for maintaining output levels vary accordingly across different geological and operational contexts.

Long-term Energy Transition and Investment Climate Considerations

Continental energy transition planning requires integration of renewable energy infrastructure with existing petroleum systems, carbon pricing impact assessment on long-term reserve valuations, and regional energy trading mechanism development. The timeline for global petroleum demand transition affects investment strategies and infrastructure development priorities across African producers.

Capital Allocation Trends and Domestic Capacity Building

Foreign direct investment patterns in African petroleum sectors reflect global energy transition considerations, geopolitical stability assessments, and technological capability requirements. International oil companies balance short-term production optimisation against long-term portfolio transition strategies that influence capital allocation priorities. In addition, current market conditions including oil price rally analysis trends affect investment decision timelines.

Domestic capacity building initiatives include local content requirements, workforce development programmes, and technology transfer arrangements that develop indigenous petroleum industry capabilities. Nigeria's Petroleum Industry Act mandates increasing local participation, while Angola implements similar frameworks for domestic supplier development and skills transfer programmes.

Sovereign wealth fund development from petroleum revenues provides mechanisms for economic diversification and long-term fiscal stability. Norway's model influences African petroleum producers seeking to transform hydrocarbon wealth into sustainable economic foundations beyond resource extraction phases.

The next major ASX story will hit our subscribers first

Infrastructure Constraints and Reserve Monetisation Challenges

Transportation and logistics infrastructure requirements vary significantly across continental petroleum producers, with landlocked nations requiring pipeline networks, coastal nations developing port facilities, and offshore producers implementing marine export systems. Regional refining capacity decisions involve trade-offs between crude export revenues and domestic value addition through processed petroleum products.

Technology Requirements and Expertise Development

Enhanced oil recovery techniques become increasingly important for mature field management, requiring water injection systems, pressure maintenance programmes, and advanced reservoir monitoring technologies. Deep-water drilling capabilities in Atlantic offshore regions demand sophisticated equipment, specialised expertise, and substantial capital investment for successful field development.

Local workforce development programmes address skills gaps in geological analysis, petroleum engineering, and project management capabilities required for sustainable industry development. Technology transfer arrangements with international oil companies provide knowledge sharing mechanisms while building domestic technical capacity for long-term resource management.

Global Market Positioning and Export Strategy Optimisation

African petroleum exports target diverse global markets with varying crude oil quality specifications, refining compatibility requirements, and pricing mechanisms. Asian market penetration strategies focus on diesel-rich crude grades suitable for regional refining configurations, while European markets emphasise supply security and transportation reliability.

Competitive Analysis Against International Producers

Cost structure analysis reveals varying production economics across African petroleum operations, from low-cost Libyan desert fields to higher-cost deepwater developments offshore Angola. Quality specifications affect refining compatibility and premium pricing opportunities in international markets, while strategic partnerships with international oil companies provide technical expertise and market access.

Price volatility management through production coordination mechanisms, strategic petroleum reserves, and export diversification strategies enable African producers to optimise revenues while maintaining market share in competitive global petroleum markets. However, ongoing oil price trade war dynamics continue to influence these strategic considerations.

Frequently Asked Questions About African Oil Reserves

Which African Country Maintains the Largest Proven Oil Reserves?

Libya holds the largest proven oil reserves in Africa at 48.4 billion barrels, representing approximately 46% of continental reserves and ranking ninth globally according to comprehensive African oil reserves statistics. The Sirte Basin contains the majority of these reserves across multiple geological formations developed since the 1960s.

How Accurate Are Current African Reserve Estimates?

Reserve estimates undergo regular third-party auditing using Society of Petroleum Engineers standards, though political instability in conflict-affected regions can limit comprehensive geological surveys and verification processes. Independent certification provides reasonable confidence in reported figures, while unexplored frontier basins may contain additional undiscovered resources.

What Proportion of Global Reserves Does Africa Control?

Africa contains approximately 7.5% of global proven petroleum reserves based on current estimates, with significant exploration potential remaining in frontier sedimentary basins across the continent. This proportion has remained relatively stable despite new discoveries and field development across multiple countries and geological provinces.

Disclaimer: Petroleum reserve estimates involve geological uncertainty and may change based on technological developments, economic conditions, and additional exploration results. Investment decisions should consider multiple risk factors beyond reserve quantities alone.

Want to Capitalise on Africa's Resource Revolution?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, empowering subscribers to identify actionable opportunities ahead of the broader market in Africa's resource-rich landscape. Explore how historic mineral discoveries have generated substantial returns and begin your 14-day free trial today to position yourself strategically in this dynamic sector.