June 8, 2026

The convergence of clean energy expansion, defense modernization, and supply chain vulnerabilities has created unprecedented demand for diversified sourcing strategies across critical mineral sectors. As geopolitical tensions and technological transitions fundamentally reshape how nations secure access to essential industrial materials, U.S. ties to African rare earths have emerged as a cornerstone of America's strategic response to concentration risks in global supply chains.

Furthermore, the emergence of alternative supply networks reflects broader shifts in global economic architecture, where resource security increasingly determines technological competitiveness and national security capabilities. These dynamics have accelerated institutional responses that prioritize long-term strategic relationships over short-term cost optimization, creating opportunities for countries with untapped mineral resources to participate in next-generation supply chains through sophisticated partnership structures.

Understanding America's Strategic Pivot to African Critical Minerals

Washington's systematic reorientation toward African mineral partnerships represents a comprehensive response to concentration risks that have accumulated over decades of single-source dependencies. China's 85% control of global rare earth processing capabilities creates systemic vulnerabilities that extend beyond simple market dominance, encompassing technological bottlenecks and geopolitical leverage points that threaten supply continuity during periods of international tension.

This strategic pivot encompasses multiple institutional mechanisms designed to create sustainable alternatives to existing supply structures. The U.S. Trade and Development Agency (USTDA) has emerged as a key facilitator, providing grants and technical assistance that enable African mining companies to integrate with American capital markets and technology ecosystems.

Recent developments demonstrate the effectiveness of this approach, with British rare earths company Altona Rare Earths successfully listing on the OTCQB Venture Market in March 2026 to support its Monte Muambe project in Mozambique. This milestone reflects how the critical minerals transition is accelerating institutional support for alternative supply networks.

Key Strategic Drivers Behind U.S.-Africa Mineral Partnerships

- Supply chain resilience: Reducing dependence on single-source suppliers for defence-critical materials

- Technology sector requirements: Supporting semiconductor, renewable energy, and electric vehicle manufacturing

- Strategic stockpiling capabilities: Building reserve capacity for emergency supply scenarios

- Alliance strengthening: Creating economic partnerships that support broader geopolitical objectives

The Monte Muambe project exemplifies this strategic integration, targeting 15,000 tonnes of mixed rare earth carbonate annually over an 18-year operational timeline. The project's rapid progression from USTDA grant recipient to OTCQB-listed entity demonstrates how U.S. institutional support creates pathways for African mining ventures to access American capital markets and strategic partnerships.

Institutional Framework for Partnership Development

| Agency | Primary Function | African Focus |

|---|---|---|

| USTDA | Feasibility studies, technical assistance | Project development support |

| DFC | Equity investments, loan guarantees | Risk mitigation for private investors |

| EXIM Bank | Export financing, working capital | Equipment and technology financing |

| OTCQB Markets | Capital market access | Investor engagement platform |

This coordinated institutional approach creates multiple touchpoints between African mining companies and U.S. financial systems, establishing dependencies that extend beyond simple commercial relationships. The rapid approval of Altona's OTCQB listing signals institutional commitment to facilitating African rare earth company integration within American capital market infrastructure.

When big ASX news breaks, our subscribers know first

What Makes African Rare Earth Deposits Strategically Valuable?

African rare earth deposits offer unique geological and strategic advantages that extend far beyond simple mineral abundance. The continent's deposits present optimal combinations of mineral composition, geographic distribution, and political alignment that create sustainable competitive advantages for Western supply chain integration.

Consequently, this strategic realignment has prompted analysts to examine how the critical minerals pivot might influence global market structures and competitive dynamics across the next decade.

Geological Advantages and Mineral Quality Characteristics

African rare earth mineralisation patterns typically involve complex polymetallic deposits that contain multiple valuable elements within single ore bodies. This geological characteristic reduces extraction costs while providing operational flexibility to adjust production profiles based on market demand fluctuations.

The Monte Muambe project demonstrates this advantage through its mixed rare earth carbonate production profile, enabling responsive manufacturing based on downstream market requirements. Southern African deposits concentrate neodymium and praseodymium, essential elements for permanent magnet applications in electric vehicle motors and wind turbine generators.

These light rare earth elements command premium pricing due to their critical role in clean energy technologies, making African deposits particularly valuable as global decarbonisation efforts accelerate. East African mineralisation contains higher concentrations of dysprosium and terbium, heavy rare earth elements crucial for high-temperature magnetic applications and advanced electronics manufacturing.

Strategic Value Beyond Geological Characteristics

Critical Market Insight: African rare earth projects offer strategic value through their potential to create alternative processing capabilities outside Chinese control, addressing the most significant vulnerability in current global supply chains.

The strategic value of African deposits extends to their compatibility with Environmental, Social, and Governance (ESG) standards increasingly required by Western institutions and corporations. Unlike some existing global production facilities, new African projects can integrate modern environmental technologies and community engagement frameworks from initial development phases.

This creates sustainable competitive advantages in ESG-conscious markets, particularly as mining innovation trends increasingly emphasise responsible production practices and community engagement protocols.

Partnership Framework Benefits and Technology Integration

Technology Transfer Components:

- Beneficiation and concentration technologies for initial ore processing

- Hydrometallurgical separation systems for individual element isolation

- Environmental remediation capabilities for sustainable production practices

- Digital monitoring systems for operational optimisation and compliance reporting

Capacity Building Initiatives:

- Local technical expertise development programmes

- Equipment maintenance and optimisation training

- Financial management and project development capabilities

- Regulatory compliance and international standards implementation

These technology transfer components create long-term competitive advantages that extend beyond initial project development, establishing African operations as sustainable participants in global rare earth markets rather than simple raw material exporters.

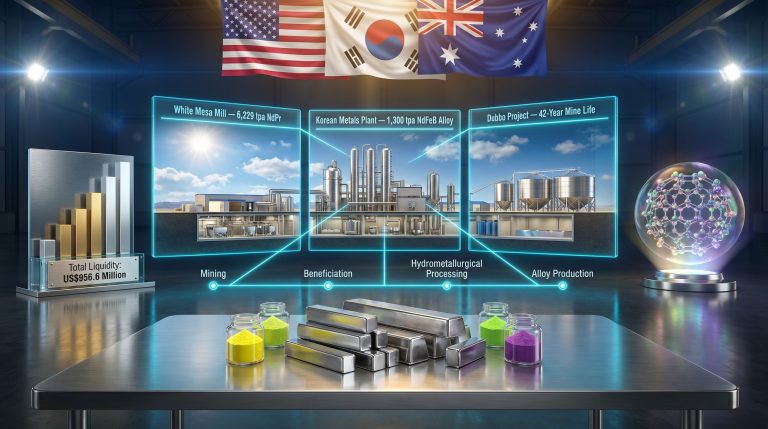

Which African Projects Are Receiving U.S. Government Support?

The United States has strategically allocated resources across multiple African rare earth initiatives, creating a diversified portfolio approach that reduces individual project risks whilst maximising collective supply chain impact. This comprehensive support structure demonstrates institutional commitment to African mineral development as a cornerstone of American critical materials strategy.

Monte Muambe Project: Mozambique's Strategic Development

Project Specifications:

- Annual Production Target: 15,000 tonnes mixed rare earth carbonate

- Operational Timeline: 18-year mine life with expansion potential

- Investment Structure: USTDA grant plus OTCQB market access

- Development Stage: Pre-feasibility study completion in progress

The Monte Muambe project represents the most advanced example of U.S.-African rare earth partnership integration. British company Altona Rare Earths achieved OTCQB listing approval in March 2026, trading under ticker ANRCF and providing American investors direct exposure to Mozambican rare earth development.

The project's strategic importance extends beyond production capacity, serving as a model for technology transfer and capital market integration that other African projects are replicating. However, the success of these initiatives remains vulnerable to broader geopolitical tensions, particularly as the US‑China trade war continues to influence global supply chain strategies.

Market Integration Strategy:

Altona's dual listing approach maintains London Stock Exchange presence whilst accessing U.S. capital markets, creating multiple funding sources and reducing dependency on single financial ecosystems. This structure enables flexible capital allocation during different development phases whilst maintaining alignment with both British and American institutional requirements.

Longonjo Development: Angola's Advanced Project Portfolio

Financial Structure:

- Capital Requirements: $276.3 million estimated total investment

- Equity Placement: $100 million completion confirmed

- EXIM Bank Negotiations: $160 million potential debt facility

- Market Strategy: Nasdaq listing consideration for 2026

British firm Pensana Plc's Longonjo project demonstrates more advanced development positioning compared to early-stage African initiatives. The project's progression toward potential Nasdaq listing indicates institutional confidence in project viability and alignment with U.S. strategic objectives.

Angola's established mining regulatory framework and infrastructure capabilities support accelerated development timelines compared to greenfield jurisdictions. This positioning has benefited from policy shifts, including the Trump mineral policy that prioritised critical mineral security through strategic partnerships.

Songwe Hill & Kangankunde: Malawi's Expandable Production Platform

Production Specifications:

- Initial Capacity: 15,300 tons concentrate annually

- Expansion Potential: 50,000 tons concentrate capability

- DFC Commitment: $4.6 million approved, $100 million potential

- Operational Timeline: 45-year mine life projection

Development Advantages:

- Modular expansion capabilities enabling responsive capacity increases

- Established regulatory framework supporting international mining investment

- Strategic location facilitating regional supply chain integration

- Long-term operational timeline providing sustainable supply security

Mkango Resources' Malawi operations represent scalable production platforms that can adjust output based on market demand evolution. The project's 45-year mine life exceeds typical rare earth operations, providing exceptional long-term supply security for strategic applications.

Phalaborwa Complex: South Africa's Infrastructure Advantage

Investment Structure:

- DFC Equity Investment: $50 million via TechMet partnership

- Focus Elements: Neodymium, praseodymium, dysprosium, terbium

- Infrastructure Benefits: Established mining and processing facilities

- Strategic Importance: Immediate production capability potential

The Phalaborwa Complex leverages existing mining infrastructure to reduce development timelines and capital requirements compared to greenfield projects. South Africa's established mining expertise and regulatory framework provide operational advantages that support rapid scaling of rare earth production capacity.

How Do U.S. Financing Mechanisms Support African Rare Earth Development?

American financial institutions have deployed sophisticated funding structures that combine development finance, trade facilitation, and strategic partnerships to accelerate African rare earth project advancement. These mechanisms create coordinated support systems that address different aspects of project development whilst maintaining alignment with U.S. strategic objectives.

Multi-Agency Coordination Framework

U.S. International Development Finance Corporation (DFC) Capabilities:

- Equity investment authority up to $1 billion per project

- Loan guarantee programmes reducing investor risk exposure

- Political risk insurance covering expropriation and currency scenarios

- Technical assistance funding for capacity building initiatives

U.S. Trade and Development Agency (USTDA) Functions:

- Feasibility study financing for project viability assessment

- Technical assistance grants supporting regulatory compliance

- U.S. technology export facilitation creating equipment supply relationships

- Regulatory framework development assistance for host countries

Export-Import Bank of the United States (EXIM) Services:

- Project finance solutions for large-scale infrastructure development

- Working capital facilities supporting operational requirements

- Equipment financing programmes facilitating U.S. technology exports

- Long-term supply agreement backing for offtake commitments

Capital Market Integration Strategy

The OTCQB listing mechanism represents a sophisticated approach to integrating African mining companies within American financial ecosystems. This platform enables retail and institutional investors to participate in African rare earth development whilst maintaining companies' primary listings on established exchanges, creating dual-market liquidity and broader investor participation.

OTCQB Strategic Benefits:

- Regulatory compliance streamlining compared to full exchange listing

- Investor base diversification across multiple geographic markets

- Currency hedging opportunities through dollar-denominated trading

- Strategic partnership facilitation with U.S. institutional investors

Risk Mitigation and Investment Protection

Financing Innovation: The combination of USTDA grants, DFC equity participation, and OTCQB market access creates multiple layers of U.S. institutional involvement that reduce overall project risk whilst maintaining strategic alignment with American supply chain objectives.

Comprehensive Risk Coverage:

- Political risk insurance through DFC programmes

- Currency fluctuation protection via dollar-denominated financing

- Technology transfer warranties ensuring equipment performance

- Regulatory compliance support reducing permitting uncertainties

What Role Does the Mineral Security Partnership Play?

The Mineral Security Partnership represents a multilateral framework for coordinating critical mineral supply chain development across Western allies and mineral-rich partner countries. This initiative establishes cooperation mechanisms that extend beyond bilateral relationships, creating integrated approaches to supply chain diversification that leverage collective resources and expertise.

Partnership Structure and Geographic Scope

Member Countries: 14 nations plus the European Union

African Focus Countries: Angola, Botswana, Democratic Republic of Congo, South Africa, Tanzania, Uganda, Zambia

Core Operational Objectives:

- Supply chain diversification away from single-source dependencies

- Responsible mining standards implementation across partner projects

- Technology transfer facilitation between member countries and African partners

- Alternative financing mechanisms development for project advancement

Strategic Differentiation from Alternative Engagement Models

| Partnership Aspect | Western MSP Approach | Alternative Models |

|---|---|---|

| Development Focus | Value-addition and processing capabilities | Extraction and raw material export |

| Standards Implementation | ESG compliance mandatory from project inception | Variable environmental and social standards |

| Technology Integration | Knowledge transfer and local capacity building | Equipment supply and technical services |

| Timeline Orientation | Long-term strategic cooperation frameworks | Project-specific engagement periods |

| Financial Structure | Multi-source financing with risk sharing | Single-source development financing |

Coordination Mechanisms and Implementation

The MSP framework operates through working groups that address specific aspects of mineral supply chain development. These groups coordinate member country resources, expertise, and financing capabilities to support African projects that align with collective strategic objectives.

Technical Working Groups:

- Geological assessment and exploration coordination

- Processing technology development and transfer programmes

- Environmental standards implementation and monitoring systems

- Infrastructure development planning for regional integration

Financial Coordination Mechanisms:

- Co-financing arrangements among member development agencies

- Risk-sharing protocols for large-scale project investment

- Market access facilitation through member country trade relationships

- Strategic stockpiling coordination for emergency supply scenarios

How Are Market Dynamics Shifting Due to U.S.-Africa Partnerships?

The emergence of U.S.-backed African rare earth projects is creating fundamental changes in global market structures, potentially reducing price volatility and supply concentration risks that have characterised rare earth markets for decades. These shifts represent structural transformations rather than temporary adjustments, establishing new competitive dynamics that will influence global rare earth markets through 2030 and beyond.

Supply Chain Diversification Impact

Current Global Market Structure:

- China: 70% global production dominance, 85% processing control

- Rest of World: 30% fragmented production across multiple countries

- Processing Bottlenecks: Limited alternative processing capabilities outside China

Projected 2030 Market Structure with African Projects:

- China: 55-60% market share with continued processing advantages

- Africa (U.S.-partnered): 15-20% market share with expanding processing capabilities

- Other Regions: 20-25% market share including Australia, Canada, and Brazil

Price Stability and Strategic Reserve Benefits

The development of alternative supply sources creates several structural market improvements that benefit both producers and consumers of rare earth materials. Reduced price volatility emerges from diversified production capacity that prevents single-country supply disruptions from creating global shortages.

Market Stability Mechanisms:

- Alternative supply activation during geopolitical tensions or trade disputes

- Competitive pricing pressure reducing monopolistic pricing capabilities

- Strategic reserve capabilities enabling government stockpiling for critical applications

- Supply security enhancement for defence and technology sector requirements

Investment Flow Redirection and Capital Market Effects

Market Transformation: The integration of African rare earth companies within U.S. capital markets creates new investment channels that redirect global capital flows toward alternative supply chain development, fundamentally altering traditional investment patterns in the sector.

Capital Allocation Shifts:

- Institutional investor engagement with African mining companies through OTCQB access

- Development finance integration reducing private investor risk exposure

- Technology sector participation in upstream supply chain development

- Strategic partnership formation between mining companies and end-user industries

The next major ASX story will hit our subscribers first

What Challenges Face U.S.-Africa Rare Earth Partnerships?

Despite strategic advantages and institutional support, several operational and structural challenges must be addressed to ensure successful project development and long-term partnership sustainability. These challenges span technical, regulatory, and infrastructure domains that require coordinated responses from multiple stakeholders.

Infrastructure and Logistics Constraints

Transportation Network Limitations:

- Rail connectivity gaps between mining areas and export ports

- Road infrastructure capacity insufficient for heavy mineral transport volumes

- Port handling capabilities requiring upgrades for bulk mineral exports

- Regional integration deficits limiting cross-border transport efficiency

Power and Utilities Infrastructure:

- Reliable electricity supply essential for processing operations and equipment functionality

- Water access requirements for mineral processing, dust suppression, and environmental compliance

- Telecommunications infrastructure necessary for remote operations monitoring and control

- Maintenance service availability for specialised mining and processing equipment

Regulatory and Political Risk Considerations

Mining Code Evolution and Stability:

- Regulatory framework predictability affecting long-term investment decisions

- Tax regime consistency ensuring project economic viability throughout operational lifecycles

- Environmental permitting processes requiring streamlined but comprehensive assessment procedures

- Local content requirements balancing community benefits with operational efficiency

Political Risk Factors:

- Government stability and policy continuity affecting contract sanctity

- Community engagement effectiveness ensuring social licence for operations

- Regional security considerations in areas affected by conflict or instability

- Currency stability and foreign exchange availability for international transactions

Technical and Operational Challenges

Skilled Workforce Development:

- Technical expertise availability for specialised rare earth processing operations

- Training programme development creating local capabilities for equipment operation and maintenance

- Management capacity building ensuring effective project administration and compliance

- Technology transfer effectiveness establishing sustainable local competencies

How Will Technology Transfer Accelerate African Rare Earth Development?

Technology partnerships between U.S. companies and African operations represent critical components of sustainable development strategies that create capabilities extending far beyond simple extraction activities. These partnerships establish local expertise that reduces operational dependencies whilst building long-term competitive advantages for African operations in global markets.

Processing Technology Development and Implementation

Advanced Beneficiation Capabilities:

- Magnetic separation systems for initial ore concentration and waste material removal

- Flotation technologies optimising recovery rates for specific rare earth elements

- Gravity separation processes enhancing mineral concentration efficiency

- Optical sorting systems improving ore grade consistency and reducing processing costs

Hydrometallurgical Processing Systems:

- Leaching technologies for rare earth element extraction from concentrated ores

- Solvent extraction processes enabling individual element separation and purification

- Precipitation and crystallisation systems producing high-purity rare earth compounds

- Recycling capabilities for processing water and chemical reagent recovery

Environmental Technology Integration

Sustainable Production Technologies:

- Tailings management systems minimising environmental impact and enabling rehabilitation

- Water treatment and recycling technologies reducing freshwater consumption and discharge

- Air quality control systems managing dust emissions and atmospheric pollutants

- Carbon footprint reduction methodologies supporting climate compliance objectives

Monitoring and Compliance Systems:

- Real-time environmental monitoring enabling immediate response to operational variations

- Digital data management supporting regulatory compliance and ESG reporting requirements

- Remote sensing technologies for environmental impact assessment and mitigation

- Community engagement platforms facilitating transparent communication and feedback

Capacity Building and Knowledge Transfer Programmes

Technology Transfer Strategy: Comprehensive technology transfer programmes create local expertise that reduces operational dependencies whilst building long-term competitive advantages for African operations in global markets.

Technical Education Initiatives:

- University partnership programmes developing specialised rare earth engineering curricula

- Vocational training centres creating skilled technician capabilities for operations and maintenance

- Management development programmes establishing local project administration competencies

- Research and development facilities enabling continuous operational improvement and innovation

Institutional Development Support:

- Regulatory framework strengthening ensuring effective environmental and safety oversight

- Financial management systems supporting transparent accounting and investor relations

- Quality assurance programmes meeting international standards for rare earth products

- Market development capabilities enabling direct customer relationships and strategic partnerships

What Are the Long-Term Implications for Global Rare Earth Markets?

The successful development of U.S.-backed African rare earth projects will fundamentally reshape global supply chains, creating new competitive dynamics and strategic relationships that extend well beyond the mining sector. These transformations represent structural changes that will influence international trade, technology development, and geopolitical relationships through the next decade and beyond.

Geopolitical Realignment Effects and Strategic Implications

Supply Chain Resilience Enhancement:

- Diversified sourcing capabilities reducing vulnerability to single-country supply disruptions

- Alternative supply route development enabling continued production during trade disputes or sanctions

- Strategic stockpiling capacity providing government reserves for defence and critical technology applications

- Alliance strengthening mechanisms creating deeper economic relationships between producing and consuming nations

Technology Sector Independence:

- Domestic processing capabilities reducing dependence on foreign value-added services

- Innovation ecosystem development linking mining, processing, and manufacturing activities

- Research and development coordination accelerating advancement in rare earth applications and efficiency

Market Structure Evolution and Competitive Dynamics

Industry Consolidation and Integration:

- Vertical integration opportunities enabling mining companies to develop downstream processing capabilities

- Strategic partnership formation between rare earth producers and technology manufacturers

- Regional supply chain development creating integrated production networks across multiple countries

- Investment diversification reducing concentration risks for institutional and strategic investors

Innovation and Technology Advancement:

- Processing efficiency improvements reducing costs and environmental impacts

- Alternative material development creating substitutes for critical rare earth applications

- Recycling technology advancement enabling circular economy approaches to rare earth utilisation

- Application optimisation improving performance whilst reducing material requirements

Economic Development and Regional Integration

African Economic Transformation:

- Value-addition capacity building enabling local processing and manufacturing capabilities

- Infrastructure development acceleration supporting broader economic growth and integration

- Technology transfer spillovers creating capabilities applicable to other industrial sectors

- Regional cooperation enhancement facilitating coordinated approaches to mineral development

Global Investment Pattern Changes:

- Development finance mobilisation directing capital toward African mining and processing projects

- Private sector participation increasing through risk mitigation and strategic partnership opportunities

- Technology sector engagement creating upstream supply chain investment and integration

- Strategic partnership formation establishing long-term cooperation frameworks beyond traditional commercial relationships

Future Market Scenarios and Strategic Considerations

Long-term Outlook: The emergence of African rare earth production capacity supported by U.S. partnerships creates opportunities for downstream processing development, regional supply chain integration, and innovation ecosystems linking mining, technology, and manufacturing across multiple continents.

Scenario Planning Considerations:

- Continued U.S. institutional support through 2030 and beyond, maintaining strategic priority status

- Private sector co-investment acceleration in processing, technology development, and downstream applications

- Regional development bank participation in infrastructure and capacity building projects

- International coordination expansion including U.S.-Japan rare earth cooperation on select minerals, demonstrating multilateral partnership potential

The transformation of global rare earth markets through U.S.-Africa partnerships represents a fundamental shift from concentrated, single-source supply chains toward diversified, strategically aligned networks that balance economic efficiency with supply security and geopolitical stability. This evolution creates opportunities for sustained economic development, technological advancement, and international cooperation that extend far beyond traditional mineral commodity relationships.

Disclaimer: This analysis contains forward-looking statements and projections based on current market conditions and policy frameworks. Actual outcomes may vary significantly due to changes in geopolitical conditions, technological developments, regulatory environments, and market dynamics. Investment decisions should consider comprehensive due diligence and professional financial advice. Project development timelines and financial projections are subject to various risks including regulatory approval processes, commodity price fluctuations, and operational challenges that may affect actual performance.

Ready to Capitalise on Critical Mineral Market Shifts?

As the U.S.-Africa rare earth partnership reshapes global supply chains and creates new investment opportunities, Discovery Alert's proprietary Discovery IQ model provides instant notifications on significant ASX mineral discoveries, empowering subscribers to identify actionable opportunities ahead of the broader market. Explore why historic critical mineral discoveries can generate substantial returns by visiting Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.