June 7, 2026

The Rare Earth Supply Chain Problem That One Deal Could Help Solve

Building a rare earth supply chain outside of China is not simply a matter of finding ore in the ground. It requires mastering a sequence of industrial processes, each technically demanding, capital intensive, and historically dominated by a single country. The persistent gap in Western rare earth development has never been a shortage of mineral resources. It has been the absence of downstream infrastructure needed to convert those resources into the alloys that power electric motors, wind turbines, and defence systems. Understanding this structural reality is essential context for evaluating why the Energy Fuels ASM acquisition, announced in January 2026, carries significance well beyond its headline valuation.

When big ASX news breaks, our subscribers know first

What the Energy Fuels ASM Acquisition Actually Involves

The transaction is structured as an all-stock scheme of arrangement in which Energy Fuels (NYSE: UUUU | TSX: EFR) would acquire Australian Strategic Materials (ASM) at an implied valuation of approximately US$299 million, or A$1.60 per ASM share. The structure includes several components that investors should understand in detail.

Transaction terms at a glance:

- ASM shareholders receive 0.053 Energy Fuels shares (or CHESS Depository Interests) per ASM share held

- An unfranked special dividend of up to A$0.13 per share is included

- Eligible ASM option holders receive A$0.50 cash per option

- Closing conditions span ASM shareholder approval, Federal Court of Australia sanction, Foreign Investment Review Board (FIRB) clearance, and exchange listing approvals for newly issued Energy Fuels securities

- The anticipated closing timeline is as early as July 2026

What distinguishes this transaction from most critical minerals M&A is its vertical integration rationale. Rather than consolidating resource acreage, it is designed to close a gap in the processing and manufacturing chain that Western producers have consistently failed to bridge organically. Furthermore, the critical minerals demand surge of recent years has made this kind of integration increasingly urgent.

| Deal Attribute | Energy Fuels / ASM | Typical Sector Peer Transaction |

|---|---|---|

| Deal structure | All-stock scheme of arrangement | Mix of cash and stock |

| Implied valuation | ~US$299 million | Varies widely |

| Strategic rationale | Vertical integration (processing to alloys) | Primarily resource consolidation |

| Geographic reach | USA, South Korea, Australia | Typically single jurisdiction |

| Downstream capability added | NdFeB alloy production | Rarely extends to alloys |

The Five-Stage Rare Earth Supply Chain and Where the Gap Has Always Been

To grasp the logic behind the Energy Fuels ASM acquisition, it helps to map out the full supply chain for rare earth permanent magnets. China's dominance derives not from geology alone but from its control of every link in this chain simultaneously. Indeed, the rare earth supply chain challenge has been a persistent structural weakness for Western nations.

- Mining — extraction of monazite, bastnäsite, or other rare earth bearing minerals from the ground

- Beneficiation — physical concentration of feedstock through gravity, magnetic, and flotation techniques

- Hydrometallurgical processing — chemical separation of individual rare earth element (REE) oxides from concentrated feedstock

- Metal and alloy production — conversion of REE oxides into neodymium-iron-boron (NdFeB) alloys suitable for magnet production

- Magnet manufacturing — sintering or bonding of NdFeB alloy into finished permanent magnets for motors, generators, and defence systems

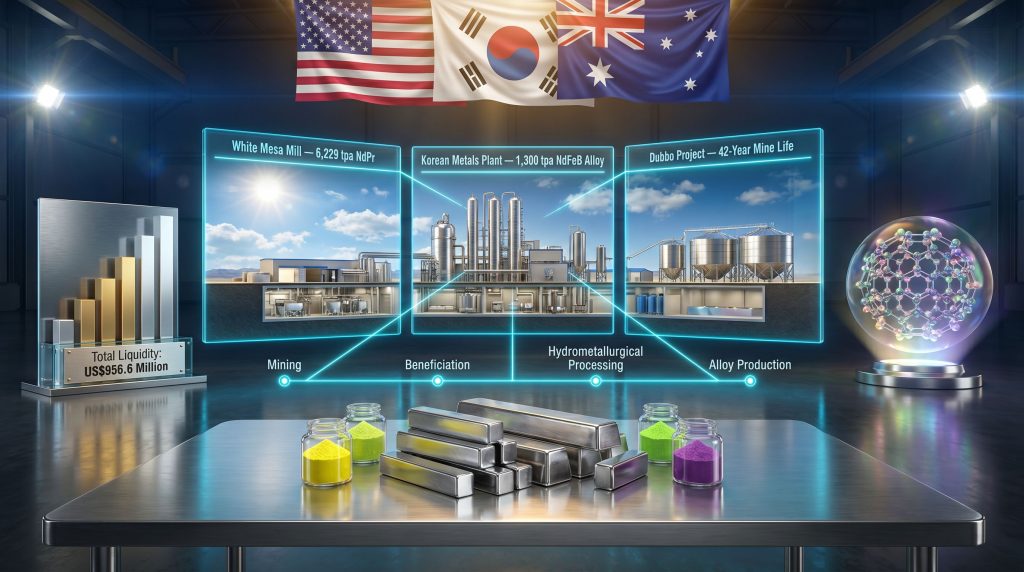

Prior to the announced acquisition, Energy Fuels had established credible capabilities across stages one through three, anchored by the White Mesa Mill in Blanding, Utah. What stage four requires, specifically the ability to melt, strip-cast, and hydrogen-decrepitate REE oxides into alloy flake, is a metallurgical skill set that cannot simply be imported from a textbook. It requires operating equipment, trained personnel, and commercial relationships with magnet manufacturers. ASM's Korean Metals Plant in Ochang, South Korea, provides all three.

Why this matters: Western governments have repeatedly identified NdFeB alloy production as a critical vulnerability in their defence and clean energy supply chains. Yet as of mid-2026, no other Western-aligned rare earth company operates a commercial-scale alloy facility outside of China. The Korean Metals Plant represents a category of infrastructure that has taken years to build and that competitors cannot replicate quickly.

What ASM Brings to the Combined Entity

The Korean Metals Plant: Operating Infrastructure That Took Years to Build

The Korean Metals Plant in Ochang, South Korea, is currently producing approximately 1,300 tonnes per annum of NdFeB alloy. An expansion pathway targeting approximately 3,600 tonnes per annum is already planned. For context, NdFeB alloy is the precursor material from which sintered permanent magnets are manufactured, and those magnets are the components inside electric vehicle traction motors and direct-drive wind turbine generators.

What is rarely appreciated by generalist investors is that alloy production for magnet-grade NdFeB is not simply smelting. The process involves precision strip casting under inert atmosphere conditions, followed by controlled hydrogen decrepitation to produce the alloy flake geometry required by downstream magnet manufacturers. These are process-specific skills tied to specific equipment configurations. The Korean plant's existing customer relationships with magnet manufacturers in Asia represent additional commercial value beyond the physical assets.

The Planned American Metals Plant: Onshoring a Critical Manufacturing Step

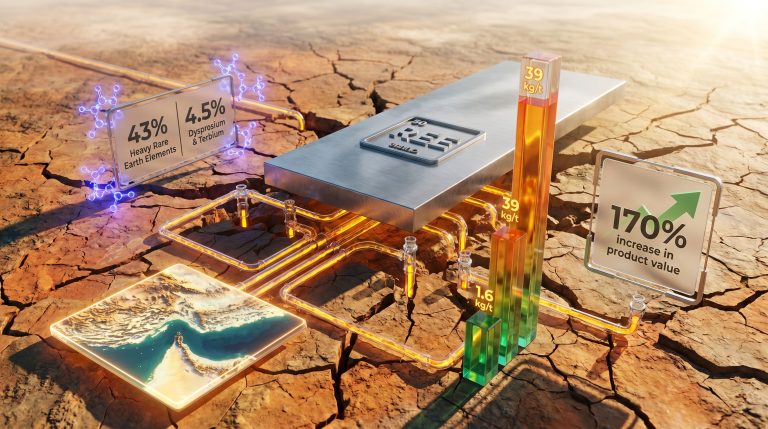

A planned American Metals Plant carries an initial target capacity of approximately 2,000 tonnes per annum of NdFeB alloy. This facility would represent the first commercial-scale NdFeB alloy production in the United States. The significance is not just industrial but structural: it would allow Energy Fuels to supply US defence and clean energy sectors with domestically produced alloy, consequently reducing reliance on imported material from China or Japan. The broader US rare earth supply chain strategy makes this development particularly timely.

The Dubbo Project: Long-Duration Feedstock Security

The Dubbo Project in New South Wales, Australia, is a construction-ready rare earth and critical minerals development asset with a modelled mine life of 42 years. Beyond rare earth elements, the project contains zirconium, hafnium, and niobium, which broadens the combined company's critical minerals portfolio. For Energy Fuels, Dubbo functions as a long-horizon feedstock option that sits outside the monazite-centric supply chain currently under development, providing geological diversification that few Western rare earth companies can match.

The White Mesa Mill: America's Only Commercial REE Separation Facility

The White Mesa Mill is the operational backbone of the combined entity's rare earth platform. It is currently the sole US facility with commercial capacity to process monazite concentrate into separated REE oxides, a fact that carries significant competitive weight.

Phase 1 operating parameters:

- Monazite processing capacity: up to 10,000 metric tonnes per annum

- NdPr oxide production capacity: up to 1,000 metric tonnes per annum

Phase 2 Bankable Feasibility Study results:

| Metric | Value |

|---|---|

| Capital expenditure | US$410 million |

| NdPr production capacity | 6,229 tonnes per annum |

| NPV at 8% discount rate | US$1.9 billion |

| Internal rate of return | 33% |

| Average annual EBITDA (first 15 years) | US$311 million |

| Targeted commissioning | 2028 to 2029 |

A technical milestone achieved during Q1 2026 added further weight to the Mill's rare earth credentials. The team produced pilot-scale terbium oxide at 99.9% purity, meeting the specification requirements of permanent magnet manufacturers. Terbium is a heavy rare earth element added to NdFeB alloys to improve coercivity at elevated temperatures, a property critical for automotive traction motor applications. There is currently no commercial Western terbium oxide production outside of China, which makes this milestone more significant than its modest scale would suggest.

A Monazite Feedstock Pipeline Across Four Continents

The rare earth processing circuit at White Mesa requires a reliable, scaled feedstock supply to justify Phase 2 capital deployment. Energy Fuels has contracted approximately 40,900 tonnes per annum of monazite across four projects.

| Project | Location | Key Detail | Status |

|---|---|---|---|

| Donald Project | Victoria, Australia | JV with Astron Corp; Energy Fuels earning 49% interest, entitled to 100% of monazite | Deliveries targeted late 2027 |

| Vara Mada Project | Madagascar | FS NPV of US$1.8B at 10% discount rate; 38-year mine life | Pending FID and fiscal agreement |

| Bahia Project | Brazil | Potential 3,000 to 5,000 tpa monazite; resource estimate targeting late 2026 | Active drilling underway |

| Chemours Offtake | USA | Existing agreement | ~800 tpa contribution |

Combined estimated annual contained REE supply across the four projects:

| Element | Estimated Annual Supply |

|---|---|

| Neodymium-Praseodymium (NdPr) | 5,381 tonnes |

| Dysprosium | 260 tonnes |

| Terbium | 64 tonnes |

One nuance worth understanding is the nature of monazite as a feedstock. Monazite is a phosphate mineral that occurs as a byproduct of heavy mineral sand mining, meaning it is often produced without dedicated mining economics. This co-product structure can provide cost advantages over primary REE mining operations, though it also introduces supply dependencies tied to the economics of the primary heavy mineral sand commodities. Energy Fuels' strategy of sourcing from multiple geographies partially mitigates this dependency risk.

The next major ASX story will hit our subscribers first

Uranium: The Cash Engine Financing the Critical Minerals Build-Out

One of the least-appreciated structural advantages Energy Fuels holds over pure-play rare earth developers is its operating uranium business. While REE developers typically rely entirely on equity issuance or debt to fund processing infrastructure, the uranium operations at White Mesa generate real cash flows that can subsidise the rare earth build-out.

Q1 2026 financial performance:

| Metric | Q1 2026 | Q1 2025 | Change |

|---|---|---|---|

| Net loss | US$10.8M (US$0.04/share) | US$26.3M (US$0.13/share) | Improved ~59% |

| Uranium revenue | US$35.7 million | Not disclosed | New period |

| Uranium sold | 510,000 lbs at US$70.04/lb | Not applicable | New period |

| Operating cash flow | US$8.3 million | (US$18.8 million) | Positive swing |

| Cash and equivalents | US$108.4 million | Not disclosed | New period |

| Marketable securities | US$802.2 million | Not disclosed | New period |

| Total liquidity | US$956.6 million | Not disclosed | New period |

At a realised sale price of US$70.04 per pound against Pinyon Plain processing costs of US$23.00 to US$30.00 per pound, the uranium business is generating cash margins that pure-play REE developers structurally cannot access. The weighted average cost of finished uranium oxide inventory declined approximately 16% from end-2025 to roughly US$36.00 per pound, reflecting improving operational efficiency.

Active mining operations as of Q1 2026:

- Pinyon Plain Mine, Arizona: high-grade conventional uranium, averaging 1.12% uranium oxide in Q1 2026, with higher-grade zones anticipated as mining advances

- La Sal Mine, Utah: conventional uranium production

- Pandora Mine, Utah: conventional uranium production

- Combined Q1 2026 mine output: 425,000 pounds of contained uranium oxide

Full-year 2026 uranium production guidance stands at 1.5 million to 2.5 million pounds, with sales targeting 1.5 million to 2 million pounds. Six long-term contracts with US nuclear utilities cover deliveries through 2032, providing revenue visibility uncommon in the critical minerals sector.

Radium Isotopes: A High-Value Revenue Stream Few Investors Have Modelled

Arguably the least-discussed component of the White Mesa Mill's commercial potential is its radium isotope programme. The hydrometallurgical infrastructure used to process monazite into REE oxides also allows separation of radium-226 and radium-228, both of which are being developed for use in targeted alpha therapy (TAT) cancer treatments.

TAT is an emerging class of radiopharmaceutical treatment that delivers ionising radiation directly to tumour cells via alpha-emitting isotopes. Radium-226 is the parent isotope of actinium-225, itself one of the most sought-after therapeutic isotopes in oncology. Commercial-scale radium production at White Mesa is targeted as early as 2028, subject to successful pilot-scale production and regulatory clearance. This programme adds a high-value, low-volume revenue dimension that leverages infrastructure already being built for uranium and rare earth processing, representing a form of capital efficiency that is genuinely unusual in the mining sector.

Risks and Conditions That Remain Before Closing

The Energy Fuels ASM acquisition is not yet complete. Several material conditions remain outstanding as of mid-2026. However, the rare earth geopolitics driving this deal suggest strong motivations on both sides to navigate the regulatory requirements efficiently.

Pending approvals:

- ASM shareholder vote approval

- Federal Court of Australia scheme sanction

- Foreign Investment Review Board (FIRB) clearance

- Exchange listing approvals for Energy Fuels securities issued to ASM shareholders

Execution and integration risks to monitor:

- The transaction spans Australian, South Korean, and US regulatory environments, each with distinct timelines and requirements

- Phase 2 White Mesa expansion carries a US$410 million capex requirement that must be sequenced alongside integration costs

- The Donald Project and Vara Mada Project both carry execution risk before contracted monazite volumes reach the Mill

- NdFeB alloy pricing is partially sensitive to Chinese export policy, which has shown increasing volatility since 2023

- The Bahia Project resource estimate, expected in late 2026, remains a variable that could alter feedstock projections

In addition, the rare earth processing challenges involved in scaling up operations across multiple jurisdictions represent a further layer of complexity that investors should factor into their assessments.

Investor note: All forecasts, valuations, NPV calculations, and timeline projections referenced in this article reflect company-reported feasibility studies and announcements. They involve forward-looking assumptions that may not materialise. Independent financial advice should be sought before making any investment decision.

What to Watch Through the Second Half of 2026

For investors and industry observers tracking the strategic trajectory of the combined entity, several specific datapoints will serve as meaningful progress indicators.

- Final court approval timing and FIRB clearance for the ASM scheme

- Integration planning milestones for the Korean Metals Plant, particularly any announcements regarding alloy supply agreements with US or allied defence customers

- Progress on the Donald Project monazite delivery schedule, targeted for late 2027

- Publication of the Bahia Project resource estimate and its implications for feedstock adequacy

- NdPr and heavy REE oxide pricing trends as Chinese export restrictions on critical minerals continue to evolve

- Radium isotope programme milestones at White Mesa as a potential upside catalyst not widely embedded in analyst models

The rare earth supply chain challenge is one of the defining industrial policy problems of the current decade. What makes the Energy Fuels ASM acquisition analytically interesting is that it represents a genuine attempt to solve that problem through commercial means rather than through aspiration. Whether the execution matches the ambition across three continents and multiple regulatory jurisdictions is the question that will define the combined company's value trajectory through 2027 and beyond.

Further analysis of Energy Fuels and the broader Western critical minerals sector is available through the Crux Investor platform at cruxinvestor.com.

Want to Stay Ahead of the Next Major Critical Minerals Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly cutting through complex data to surface actionable opportunities in rare earths, uranium, and beyond before the broader market catches on. Explore how historic discoveries have generated exceptional returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself at the forefront of the next major find.