August 8, 2026

When Niche Becomes Critical: The Minor Metals Inflection Point

The commodity markets most investors follow closely — copper, aluminium, iron ore — represent only a fraction of the materials underpinning the global technology economy. Beneath the headline metals lies a quieter but increasingly consequential category: minor metals. These materials have historically operated in thin, opaque markets with limited price transparency, small annual production volumes, and highly specialised end uses. For decades, that obscurity was unremarkable. Today, it is a structural risk.

The accelerating buildout of artificial intelligence infrastructure is reshaping the demand landscape for gallium, germanium, indium phosphide, and tantalum in ways that commodity markets have not previously encountered. Unlike base metals, minor metals lack deep futures markets, meaningful strategic stockpiles, and diversified global production bases. Understanding the AI demand for minor metals supply chain prices dynamic requires examining both the technical realities of how these materials function inside AI hardware and the structural reasons why supply cannot simply expand to meet growing needs.

When big ASX news breaks, our subscribers know first

How AI Hardware Consumes Minor Metals: A Technical Breakdown

Gallium Nitride and the Power Electronics Revolution

Inside every hyperscale data centre supporting AI workloads, power management is one of the most consequential engineering challenges. AI accelerator chips operate at extraordinarily high power densities, and converting electrical current efficiently across voltage levels is critical to managing both energy costs and heat generation.

Gallium nitride (GaN) has emerged as the material of choice for next-generation power conversion systems within AI server infrastructure. GaN semiconductors outperform traditional silicon in high-frequency switching applications due to the material's superior electron mobility and wider bandgap properties. In practical terms, GaN-based power electronics achieve meaningfully higher conversion efficiencies, reducing energy waste across the voltage regulation stages that feed GPU clusters and AI accelerator arrays.

This is not a marginal improvement. In hyperscale environments where power consumption is measured in tens of megawatts, even fractional efficiency gains translate into substantial operational savings. The deployment of GaN across AI data centre power infrastructure is accelerating, and with it, demand for gallium deposits as the foundational input.

Germanium and Indium Phosphide: Moving Data at the Speed of Light

Modern AI training clusters require extraordinary data transfer rates between GPU nodes. Moving petabytes of model weights and activation data across interconnects fast enough to prevent processing bottlenecks has driven a fundamental shift in how data centres are architected internally. Copper wiring, which dominated internal data centre connectivity for decades, is being progressively displaced by optical interconnects capable of supporting terabit-scale transmission rates.

Germanium sits at the heart of this optical revolution. Germanium-based photodetectors convert optical signals back into electrical data at the receiving end of fibre optic links, exploiting the material's high refractive index and infrared transparency. Co-packaged optics, which integrate optical transceivers directly adjacent to switching chips, represent the leading edge of this architectural shift and are rapidly increasing germanium consumption per unit of data centre capacity.

Indium phosphide (InP) plays a complementary but equally critical role. As a direct bandgap semiconductor, InP is uniquely suited to the fabrication of laser diodes and coherent optical transceiver modules. InP-based devices enable the coherent optical systems that allow data centres to push transmission rates toward 800 gigabits per second per wavelength and beyond. The transition from electronic to optical interconnects inside data centres is creating an exponential growth trajectory for both germanium and InP demand.

Tantalum: The Silent Enabler Across Multiple AI Hardware Layers

Tantalum's role in AI infrastructure is less visible but equally pervasive. High-capacitance tantalum electrolytic capacitors are essential components in the power delivery networks of AI chipsets, server motherboards, and edge computing devices. These capacitors filter voltage fluctuations and provide localised energy storage within semiconductor packages, becoming more critical as chip designs push toward higher power densities.

Beyond capacitors, tantalum nitride is used as a diffusion barrier layer in advanced semiconductor fabrication processes. As chip manufacturers push toward smaller nodes, tantalum's role in preventing copper diffusion between interconnect layers becomes more pronounced. The compounding demand from capacitor manufacturers, semiconductor fabs, and the broader energy transition minerals sector is creating a multi-vector pressure on tantalum supply that is qualitatively different from previous demand cycles.

| Metal | Primary AI Application | Key Property | Supply Concentration |

|---|---|---|---|

| Gallium | GaN power electronics | High electron mobility, wide bandgap | China controls >80% of primary production |

| Germanium | Fibre optic photodetectors, co-packaged optics | Infrared transparency, high refractive index | China accounts for >60% of global output |

| Indium Phosphide | Coherent optical transceivers, laser diodes | Direct bandgap semiconductor | China, Japan, South Korea dominate |

| Tantalum | Capacitors, chip diffusion barriers | High capacitance density, corrosion resistance | DRC, Rwanda, Brazil are primary sources |

Quantifying the Demand Surge: What the Projections Actually Reveal

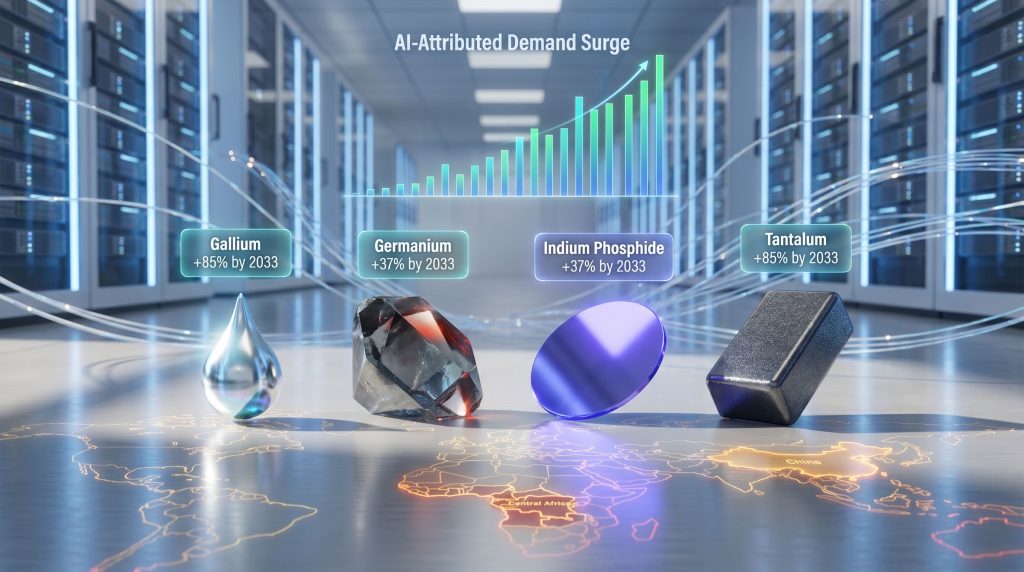

Germanium: A 37% AI-Attributed Demand Increase by 2033

Germanium currently serves several end markets: fibre optic systems, infrared optical components, solar cells used in concentrated photovoltaics, and emerging AI hardware applications. Furthermore, demand projections point toward a 37% increase in germanium consumption attributable specifically to AI infrastructure expansion by 2033, a figure that carries significant weight when placed against the material's constrained supply base.

One of the most underappreciated dimensions of the germanium supply challenge is the inadequacy of existing recycling infrastructure. Current secondary recovery processes cover only approximately 30% of projected future demand, leaving a structural supply gap that cannot be closed through circular economy measures alone. Compounding this is China's own domestic trajectory: as Chinese AI infrastructure investment accelerates, the country's internal germanium consumption is projected to grow substantially, with some analyses suggesting China could face domestic germanium shortfalls by 2040 as internal demand doubles.

Critical Insight: Germanium is not produced as a primary mined commodity in most jurisdictions. It is recovered as a by-product of zinc smelting and, in some cases, from coal combustion fly ash. This means germanium supply volumes are fundamentally governed by zinc production economics, not germanium price signals. Price increases for germanium do not automatically incentivise greater production.

Gallium: An 85% Projected Surge by 2033

The demand trajectory for gallium is even more dramatic. Projections indicate an 85% increase in gallium demand attributable to AI data centre energy efficiency requirements by 2033, driven primarily by the scaling deployment of GaN power electronics across hyperscale infrastructure. This figure dwarfs the projected growth rates for most base metals and reflects the concentrated nature of gallium's AI exposure.

Like germanium, gallium is produced almost entirely as a by-product of aluminium refining, extracted during the processing of bauxite ore. This geological reality means that the global gallium supply is structurally coupled to aluminium production, not to gallium demand or pricing. Building meaningful non-Chinese gallium processing capacity would require years of investment in refining infrastructure, and the developmental timelines involved suggest that new supply from Western projects will not materially alter the market balance before 2028 at the earliest.

The Broader Critical Mineral Super Cycle

Minor metals do not exist in isolation. The AI infrastructure buildout is generating critical minerals demand pressure across the entire spectrum. Modelling suggests that data centre construction could lift global copper demand by approximately 2% and rare earth element consumption by roughly 3% by 2030. To contextualise the scale: a single large-scale hyperscale data centre requires more than 1,000 tonnes of copper in its construction and electrical systems. Copper prices have been tracking toward the $12,000 per tonne threshold as AI demand compounds existing supply disruptions from mine depletion and permitting delays.

Silver and gold also carry indirect AI exposure. Silver's conductivity properties make it relevant to sensor arrays and conductive pathways in high-precision electronics, while gold's reliability under extreme temperature and humidity conditions keeps it embedded in mission-critical AI microelectronics.

| Metal | Projected Demand Increase (AI-attributed) | Current Recycling Coverage | Primary Demand Driver |

|---|---|---|---|

| Germanium | +37% by 2033 | ~30% of projected future demand | Fibre optic photodetectors, coherent optics |

| Gallium | +85% by 2033 | Limited secondary recovery infrastructure | GaN power electronics in data centres |

| Copper | +2% globally by 2030 | Established industrial recycling base | Data centre construction and wiring |

| Rare Earth Elements | +3% globally by 2030 | Nascent recovery capacity | Magnets, cooling systems, motors |

Why Supply Cannot Simply Respond: Geopolitical and Structural Bottlenecks

China's Export Control Architecture

Beginning in mid-2023, China introduced licensing requirements for gallium and germanium exports, formalising what had previously been an implicit advantage into an explicit policy mechanism. The licensing regime does not constitute an outright ban, but it creates meaningful uncertainty for Western manufacturers who previously relied on predictable supply flows from Chinese processors.

The strategic rationale is transparent: China's dominant position in minor metals refining provides leverage in broader technology competition, and the export control impacts serve as both a domestic industrial policy instrument and a diplomatic signalling mechanism. The practical impact on spot pricing has been observable, with price escalation episodes correlating directly with periods of heightened export control enforcement and licensing uncertainty.

The DRC Instability Factor: Tantalum Under Structural Pressure

The geographic concentration of tantalum mining in the Democratic Republic of Congo and Rwanda creates a persistent supply fragility that is qualitatively distinct from the Chinese export control risk. The Rubaya mine collapse in February 2026 illustrated how single-event disruptions can cascade through tantalum markets with limited buffering capacity. Rubaya had been one of the DRC's most significant artisanal and small-scale tantalum producing areas, and its collapse removed a meaningful volume of concentrate from the market at a time when demand was already tightening.

Responsible sourcing frameworks, including provisions analogous to those in the Dodd-Frank Act's Section 1502 and the EU Conflict Minerals Regulation, add logistical complexity to tantalum procurement from Central African sources. These regulatory requirements are legitimate from a human rights perspective, but they effectively reduce the pool of readily usable supply and create certification-related price premiums for responsibly sourced material.

The By-Product Production Constraint: A Market Mechanism That Doesn't Apply

Warning: The by-product nature of gallium and germanium production fundamentally breaks the standard commodity supply response model. In most commodity markets, rising prices incentivise increased production. For gallium and germanium, supply volumes are governed by the output decisions of aluminium and zinc producers, respectively. A doubling of gallium prices does not cause aluminium smelters to produce more bauxite.

This structural reality has profound implications for procurement teams and policymakers alike. It means:

- New primary supply can only come from dedicated refining capacity additions, which require 5-10 year development horizons

- Refining expertise outside China for both gallium and germanium is severely limited

- Recycling infrastructure is in early stages and cannot bridge near-term supply gaps

- Price signals are an unreliable indicator of future supply availability for these materials

Pricing Dynamics: How Minor Metals Markets Actually Work

Opacity as a Structural Market Feature

One aspect of minor metals markets that is rarely discussed outside specialist procurement circles is the fundamental opacity of price discovery. Unlike copper or aluminium, which trade on major exchanges with transparent, real-time pricing, gallium and germanium prices are typically determined through bilateral negotiations between producers and consumers. Published price assessments by specialist services represent estimates derived from disclosed transaction data, rather than exchange-clearing prices.

According to analysis of AI and minor metals supply chains, the AI demand for minor metals supply chain prices dynamic is increasingly being recognised as a systemic risk requiring coordinated industry and policy responses.

Featured Insight: For procurement teams navigating AI-driven demand surges in minor metals, independent price assessment services are not merely useful references. In markets where bilateral negotiation dominates, they provide the only systematic basis for benchmarking contract terms and identifying when spot pricing has moved beyond normal ranges.

Gallium and Germanium: Pricing Since 2023

The implementation of China's export licensing requirements from mid-2023 onward created visible price escalation in both gallium and germanium. Pre-2023 gallium prices had been relatively stable and low for extended periods, reflecting the material's historically modest demand profile. The export control regime introduced a risk premium that has persisted, as buyers cannot be certain that licensing approvals will be granted on commercially useful timescales.

Germanium pricing has followed a similar pattern, with the added complexity that demand growth from AI optical applications is compounding the supply-side uncertainty. The combination of geopolitical supply restriction and structurally growing demand is shifting both materials from cyclical commodity pricing patterns toward a structural premium pricing regime.

Tantalum: Longer Contracting Cycles and Conflict-Free Premiums

Tantalum pricing operates differently from gallium and germanium. Longer-term supply contracts are more common in the tantalum industry, with pricing typically structured around concentrate grade specifications and refined metal purity levels rather than spot-market dynamics. The conflict-free certification premium is a real and persistent feature of tantalum markets, with responsibly sourced material commanding meaningfully higher prices than uncertified concentrate.

Simultaneous demand growth from capacitor manufacturers, semiconductor fabrication facilities, and the energy sector is creating a multi-directional pressure on tantalum pricing that contract structures designed for previous demand environments were not built to accommodate.

Strategic Responses: Diversification, Substitution, and Policy Intervention

Western Policy Frameworks and Their Limitations

The US Department of Defense has directed investment toward domestic gallium and germanium processing capacity as part of broader critical minerals security initiatives. The EU Critical Raw Materials Act has formally designated minor metals including gallium and germanium as strategic raw materials, with associated targets for domestic processing capacity and diversified sourcing. Japan and South Korea have pursued bilateral mineral partnership frameworks with resource-holding nations to reduce single-source dependency.

These policy responses are substantive and reflect a genuine recognition of supply chain vulnerability. However, they share a common limitation: the development timelines involved mean that new Western supply capacity will not materially impact market balances before 2028-2030 at the earliest. Policy ambition and geological reality are operating on different timeframes.

Industry Responses: Where Substitution Is and Is Not Possible

The technology industry is actively exploring partial substitution pathways for some minor metals applications. However, the processing challenges associated with minor metals mean that straightforward substitution remains elusive across most applications:

- Silicon carbide (SiC) offers a partial alternative to GaN in certain power electronics applications, but SiC cannot replicate GaN's performance characteristics across all relevant frequency and efficiency ranges

- Germanium recycling from end-of-life fibre optic cables and infrared optical systems is technically feasible but requires specialised processing infrastructure that does not yet exist at scale

- Tantalum recovery from electronic waste currently operates well below its theoretical potential, with actual recovery rates representing a small fraction of contained tantalum in the end-of-life electronics stream

- Strategic stockpiling by semiconductor manufacturers has emerged as a near-term mitigation strategy, but it does not address the underlying supply-demand imbalance and may accelerate near-term price pressure

Emerging Non-Chinese Supply Projects

Exploration and development activity for gallium and germanium resources outside China is advancing in Canada, Germany, and Australia. Tantalum diversification projects in Australia, Brazil, and Canada are attracting investor attention as the supply concentration risk becomes more widely appreciated. These projects represent meaningful long-term supply diversification potential, but the development timelines to production are measured in years, not months.

The next major ASX story will hit our subscribers first

Sector-by-Sector Impact: Who Faces the Most Acute Exposure

AI Hardware Manufacturers and Hyperscale Operators

The cost implications of minor metals price inflation are beginning to filter into GPU manufacturing economics. Gallium arsenide and germanium supply constraints are not yet creating production bottlenecks at major chip manufacturers, but procurement teams are operating with heightened awareness of supply chain fragility. Data centre operators face exposure through optical component cost increases, where germanium and InP pricing directly affects the economics of high-speed interconnect infrastructure deployment.

Consumer Electronics: Competing for the Same Supply Pool

A dynamic that receives insufficient attention is the direct competition between AI data centre demand and consumer electronics manufacturing for the same minor metal supply pools. Gallium and indium are consumed in both LED lighting systems and smartphone display components, meaning that AI infrastructure expansion does not operate in a separate market. Procurement pressure from hyperscale operators consequently competes directly with consumer device manufacturers for available supply, potentially affecting both pricing and allocation.

The Energy Transition Intersection: A Compounding Demand Dynamic

Perhaps the most consequential longer-term dynamic is the convergence of AI infrastructure demand and energy transition hardware deployment on the same minor metals. GaN power electronics are being deployed simultaneously in EV fast-charging infrastructure and AI data centre power systems, meaning that two of the most capital-intensive buildout programmes in the global economy are drawing on the same gallium supply base. Germanium faces analogous cross-sector pressure from solar cell manufacturers operating concentrated photovoltaic systems.

This convergence represents a genuinely novel demand dynamic. As noted by the World Economic Forum, previous commodity super cycles were typically driven by a single dominant demand source. The simultaneous scaling of AI infrastructure and energy transition hardware creates compounding pressure that historical supply models were not designed to capture.

Frequently Asked Questions: AI Demand and Minor Metals Supply Chains

What minor metals are most exposed to AI demand growth?

Gallium, germanium, indium phosphide, and tantalum are the four most directly exposed minor metals to AI infrastructure expansion. Each serves a distinct hardware function: gallium in power electronics, germanium and indium phosphide in optical data transfer systems, and tantalum in capacitors and chip fabrication processes.

Why can't supply simply increase to meet AI-driven demand?

Gallium and germanium are produced as by-products of aluminium and zinc refining, respectively. Their supply volumes are governed by the production economics of those primary metals, not by gallium or germanium pricing. New processing capacity requires 5-10 year development timelines, and refining expertise outside China is severely limited.

How do China's export controls affect global minor metals availability?

China's licensing requirements for gallium and germanium exports, introduced from mid-2023 onward, create uncertainty around supply predictability for Western manufacturers. Licensing approval timelines and approval rates introduce a risk premium into pricing and complicate long-term procurement planning.

Is there a risk of minor metals shortages disrupting AI development timelines?

In the near term (2025-2027), the most acute supply risk is for tantalum, given ongoing instability in the DRC alongside multi-sector demand growth. Gallium faces significant medium-term risk as the projected 85% demand increase by 2033 encounters a supply base that cannot expand at equivalent speed. Germanium's 37% projected demand increase by 2033 is compounded by China's own growing domestic consumption.

What is the difference between minor metals and rare earth elements?

Minor metals are a broad category defined by low annual production volumes, highly specialised end uses, and limited substitution options. Rare earth elements (REEs) are a specific subset of the periodic table — the lanthanide series plus scandium and yttrium — with distinct geological occurrence patterns and processing requirements. Both categories face AI demand for minor metals supply chain prices pressure, but through different hardware applications: REEs primarily in permanent magnets for motors and cooling systems, minor metals in semiconductor and optical components.

Key Takeaways: A Supply Chain at a Structural Turning Point

The convergence of AI infrastructure expansion, energy transition hardware deployment, and geopolitical supply concentration is creating a fundamentally new operating environment for minor metals markets. The key conclusions for procurement teams, investors, and policymakers are:

- Demand growth is structural, not cyclical. Projections of +85% for gallium and +37% for germanium by 2033 reflect permanent changes in technology hardware architecture, not temporary demand spikes.

- Supply cannot respond to price signals alone. The by-product production constraint for gallium and germanium means that price increases will not resolve supply shortfalls on commercially useful timescales.

- Geopolitical risk is concentrated and persistent. China's dominant position in gallium and germanium refining, combined with DRC instability for tantalum, creates supply vulnerabilities that policy responses are addressing but cannot eliminate in the near term.

- Market opacity amplifies procurement risk. Without exchange-traded pricing, procurement teams operating without specialist market intelligence are navigating minor metals markets with limited visibility into true price levels and supply availability.

- Proactive supply chain strategy is no longer optional. Geographic diversification of supplier relationships, long-term contracting, substitution research investment, and recycling infrastructure development are necessary responses to a supply environment that will remain structurally tight for years.

This article is intended for informational purposes only and does not constitute financial or investment advice. Demand projections and price forecasts referenced are forward-looking estimates subject to significant uncertainty. Readers should conduct independent analysis before making procurement or investment decisions based on minor metals market dynamics.

Want to Track ASX Discoveries in the Minerals Powering AI Infrastructure?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including the critical and minor metals at the centre of the AI supply chain — turning complex geological data into actionable investment insights. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin a 14-day free trial to position yourself ahead of the market.