June 23, 2026

The Structural Risk That Makes Canada's Pacific Oil Play So Compelling

Energy import dependency is one of the most persistently underappreciated vulnerabilities in modern industrial economies. For nations that consume far more energy than they produce, the architecture of supply chains matters as much as the price of the commodity itself. Single-corridor dependencies, where the bulk of imports flow through one region via one chokepoint, create fragility that no hedging mechanism can fully resolve. It is precisely this structural fragility that is now reshaping crude oil trade flows across the Pacific, and positioning Alberta talks with Japan on Canadian crude imports as one of the more strategically significant bilateral energy conversations currently underway.

When big ASX news breaks, our subscribers know first

Japan's 95% Problem: A National Security Liability Hidden in Plain Sight

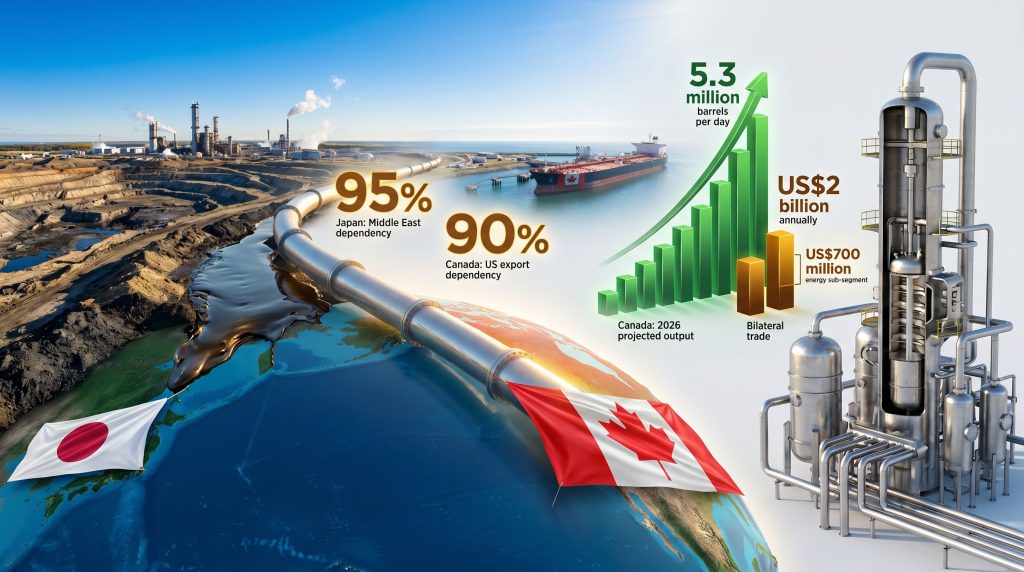

Japan's energy import profile contains a figure that should unsettle any supply chain analyst: approximately 95% of its crude oil imports originate from the Middle East. This concentration has persisted for decades, underpinned by the geographic convenience of Gulf producers, established long-term contracts, and the historical compatibility of Middle Eastern light, low-sulfur crude grades with Japan's refinery configurations.

However, the cost of that convenience is now becoming visible. The Strait of Hormuz, through which a substantial portion of global seaborne oil must pass, represents a single physical chokepoint whose disruption could sever Japan's primary supply artery within days. Understanding current crude oil market dynamics helps clarify why the Iran conflict's impact on Hormuz flows has brought renewed urgency to what was previously treated as a theoretical risk.

Beyond Hormuz, Japan's exposure is compounded by shipping lane risks through the South China Sea, creating a second layer of strategic vulnerability on the same primary supply route. For a resource-scarce economy that imports virtually all of its energy needs, this is not merely an economic issue. It is a national security liability that successive Japanese governments have acknowledged but struggled to structurally resolve.

For resource-scarce nations, energy security is defined by three intersecting pillars: supply diversity, price stability, and logistics resilience. Japan currently scores poorly on the first, and that deficiency undermines the other two.

What "Supply Diversity" Actually Requires in Practice

Diversification is not achieved by simply purchasing a few spot cargoes from an alternative origin. It requires:

- Compatible refinery infrastructure capable of processing different crude grades

- Long-term contracted supply arrangements that create predictable volume flows

- Competitive delivered-cost economics relative to incumbent suppliers

- Reliable export logistics from the alternative origin to Japanese ports

Japan currently falls short on multiple criteria when it comes to Canadian crude, which is precisely why the current Alberta-Japan dialogue is focused on structural enablement rather than simple barrel-trading.

Why Alberta's Oil Sands Crude Cannot Simply Replace Middle Eastern Barrels

Understanding the technical barrier to Alberta-Japan crude trade requires a brief examination of refinery chemistry. Alberta's oil sands produce heavy, high-sulfur crude, typically characterised by high viscosity, elevated API gravity challenges, and significant sulfur content. These properties place it in a fundamentally different processing category than the light, low-sulfur grades that flow from Saudi Arabia, Kuwait, and the UAE.

Japanese refineries have been engineered and optimised over decades to process lighter, sweeter grades. The critical piece of hardware that bridges this gap is a coker unit (also known as a delayed coker), a thermal cracking process that breaks down the heaviest fractions of high-sulfur crude into lighter, more commercially valuable products including diesel, jet fuel, and petroleum coke.

Without coking capacity, a Japanese refinery attempting to process large volumes of Alberta oil sands crude would face:

- Significant yield degradation on high-value distillate products

- Accumulation of heavy residual fractions with limited commercial outlets

- Potential damage to downstream processing units not designed for high-metal-content feedstocks

- Uncompetitive economics compared to purpose-configured Middle Eastern grade processing

This infrastructure gap is not a minor logistical inconvenience. Furthermore, it is the central technical barrier that Alberta's current proposal is specifically designed to address.

Alberta's Two-Pathway Proposal: Coker Investment and Crude Blending

Alberta Energy Minister Brian Jean's discussions in Japan have centred on two distinct structural solutions to the refinery compatibility problem. Each carries different risk profiles, capital requirements, and timelines. Reuters reporting on Alberta's Japanese refinery investment ambitions provides additional context on the scope of these conversations.

| Pathway | Mechanism | Capital Requirement | Implementation Speed | Key Risk |

|---|---|---|---|---|

| Coker Unit Co-Investment | Alberta co-funds coker construction at Japanese refinery | High | Slower (years) | Political complexity of subnational foreign infrastructure investment |

| Heavy-Light Crude Blending | Blend Alberta heavy crude with synthetic lighter oil to match Japanese specs | Lower | Faster | Blending economics must compete with Middle Eastern delivered cost |

| Phased Incremental Offtake | Gradual Trans Mountain cargo growth while domestic upgrades proceed | Minimal near-term | Very slow | Insufficient volume growth to justify long-term commitment |

The coker unit co-investment pathway would represent an unprecedented move for Alberta: the province's first-ever direct investment in foreign energy processing infrastructure. This is not simply a supply negotiation. It is a proposal to reshape the hardware conditions that would make sustained Japanese crude imports commercially viable over a generational timeframe.

The blending pathway offers a lower-capital alternative, but introduces its own complexity. Producing a consistent, specification-compliant blended crude product requires reliable access to lighter synthetic components, precise blending ratios calibrated to specific Japanese refinery configurations, and economics that remain competitive against Middle Eastern grades on a full delivered-cost basis, including freight from Alberta to Pacific tidewater and onwards to Japan.

Alberta is not simply offering Japan another crude supplier. It is offering to participate in the infrastructure transformation that would make Canadian crude a structurally viable alternative, not just an occasional spot purchase.

Canada's Mirror Problem: 90% Export Dependency on a Single Customer

The symmetry between Japan's supply concentration and Canada's export concentration is striking. While Japan sources ~95% of its crude from the Middle East, Canada directs approximately 90% of its crude exports southbound to the United States via pipeline. Both nations are structurally overexposed to a single trade corridor.

For Canada, the urgency of diversification has been amplified by US trade policy uncertainty under the Trump administration. Consequently, trade wars and oil prices have become increasingly intertwined concerns for Canadian energy policymakers. As the world's fourth-largest oil producer, with 2026 output projected to surpass the record 5.3 million barrels per day achieved in 2025, Canada's production trajectory is outpacing the pace of demand diversification.

The Trans Mountain Expansion: The Infrastructure That Changed the Equation

The completion of the Trans Mountain pipeline expansion in 2024 fundamentally altered Canada's ability to route oil sands crude to Pacific tidewater. Now operating at full capacity, Trans Mountain provides the physical logistics backbone for any Canada-to-Asia crude export strategy.

The commercial proof of concept is already visible: China has emerged as the leading Asian buyer of Canadian crude transported via Trans Mountain. This demonstrates that Alberta oil sands crude can compete effectively in Asian markets when the refinery infrastructure on the receiving end is appropriately configured. China's refineries, which include substantial coking capacity, can process heavy Canadian crude efficiently.

Japan's situation differs. Eneos Holdings, Japan's largest refining company, has purchased Trans Mountain crude on only a limited basis, acquiring two cargoes totalling approximately 800,000 barrels (comprising shipments of roughly 250,000 and 550,000 barrels respectively). These volumes are negligible relative to Japan's annual crude import requirements, but they validate that Trans Mountain crude can physically reach Japanese ports. The constraint is not logistics. It is refinery compatibility.

The Institutional Architecture Driving the Negotiation

The discussions initiated by Minister Jean in Japan span both government agencies and private sector participants, indicating that this is being treated as a structured bilateral framework rather than an ad hoc commercial conversation.

Key institutional stakeholders include:

- Japan Organization for Metals and Energy Security (JOGMEC): Japan's state-backed resource security agency, responsible for evaluating long-term supply arrangements. Alberta and JOGMEC have signed a Memorandum of Understanding covering cooperation on oil, natural gas, and carbon capture.

- Japan Bank for International Cooperation (JBIC): A government-aligned financial institution whose involvement in any project would signal formal state-level commitment to the financing framework.

- Ministry of Economy, Trade and Industry (METI): The primary policy authority over Japan's energy procurement strategy. Its engagement indicates the discussions have risen above purely commercial levels.

- Private sector participants: Jean's meetings also encompassed Japanese refiners, steelmakers, and energy traders, reflecting the reality that any commercial arrangement ultimately requires private sector buy-in to function.

The MOU with JOGMEC is the most concrete institutional output to date. However, it is important to note that no binding supply agreements have been finalised, and discussions remain at an early stage. The bilateral trade relationship between Alberta and Japan already exceeds US$2 billion annually, with energy exports accounting for approximately US$700 million of that total, providing an established commercial foundation for deeper engagement.

The next major ASX story will hit our subscribers first

The Pipeline Ambition Behind the Japan Diplomacy

Alberta's engagement with Japanese buyers serves a purpose that extends beyond the bilateral relationship itself. Securing credible Asian demand commitments is a precondition for building the commercial and financial case for a proposed new one-million-barrels-per-day oil export pipeline to Canada's west coast, a project that no private company has yet committed to constructing.

In this context, Mark Carney's vision for transforming Canada into an energy superpower aligns closely with Alberta's Pacific export ambitions. Alberta has committed to releasing its formal pipeline proposal by July 1, 2026. The strategic logic is straightforward: private sector investors and financiers require demonstrated demand on the receiving end of a multi-billion-dollar pipeline investment.

A long-term crude supply arrangement with Japanese buyers, particularly one anchored by infrastructure co-investment, could function as an anchor demand signal capable of transforming a politically driven infrastructure ambition into a commercially bankable project. Without that demand signal, the pipeline proposal risks remaining a policy aspiration. With it, the economics shift toward viability.

Canada vs. the Middle East: Competing on a Different Value Proposition

Middle Eastern crude exporters hold structural advantages in the Japanese market that cannot be easily replicated: geographic proximity, deeply established refinery compatibility, decades of contractual relationships, and the logistics familiarity of well-worn shipping lanes.

Canadian crude cannot compete on these dimensions. What it can offer is fundamentally different:

- Geopolitical diversification away from a conflict-prone region with demonstrated chokepoint vulnerabilities

- Supply chain resilience through a politically stable, democratic exporting nation with a strong rule-of-law framework

- Alignment with democratic trading partner preferences that are increasingly relevant in a fragmenting global trade environment

- Growing production capacity with a clear trajectory toward higher output volumes through the remainder of the decade

In addition, Australia's resource and energy export challenges offer a useful parallel for understanding the structural pressures facing commodity-exporting nations in an increasingly fragmented trade environment. China's emergence as the dominant Trans Mountain buyer demonstrates that these advantages can translate into commercial reality when the infrastructure conditions are right.

Japan's potential entry into the Canadian crude market, even at initially modest volumes, would validate the Trans Mountain corridor as a genuinely multi-buyer, multi-destination export route, reducing Canada's dependence on any single Asian customer and reinforcing the commercial case for further Pacific export infrastructure investment. Alberta's approach to cutting US reliance by developing Japanese partnerships illustrates precisely how this diversification logic plays out in practice.

Disclaimer: This article contains forward-looking statements regarding oil production projections, pipeline proposals, and bilateral trade negotiations. These involve significant uncertainties and should not be interpreted as guarantees of future outcomes. Readers should conduct independent analysis before making any investment or policy-related decisions based on information contained herein.

Frequently Asked Questions: Alberta Talks With Japan on Canadian Crude Imports

What is Alberta proposing to Japan regarding crude oil?

Alberta is exploring co-funding the construction of a coker unit at one or more Japanese refineries, which would allow those facilities to efficiently process heavy, high-sulfur Alberta oil sands crude. A secondary option involves developing a blended crude product that combines Alberta heavy crude with lighter synthetic oil to create a grade compatible with existing Japanese refinery configurations.

Why can't Japan simply purchase Canadian crude without infrastructure changes?

Alberta oil sands crude is chemically incompatible with most Japanese refinery configurations, which are optimised for lighter, lower-sulfur Middle Eastern grades. Without coking capacity or a compatible blended feedstock, processing Alberta crude in Japanese refineries would result in poor yields, residual fraction accumulation, and uncompetitive economics.

How much Canadian crude does Japan currently import?

Japanese imports of Canadian crude remain minimal. Eneos Holdings has purchased two Trans Mountain cargoes totalling approximately 800,000 barrels, representing a negligible share of Japan's annual crude import requirements.

What is the Trans Mountain pipeline's role in this strategy?

Completed in 2024 and operating at full capacity, the Trans Mountain pipeline expansion provides the physical infrastructure to move Alberta crude westward to Pacific tidewater, enabling export to Asian markets including Japan. Furthermore, understanding crude oil price trends through 2025 helps contextualise why the economics of this corridor are gaining renewed attention.

What is the current status of the Alberta-Japan negotiations?

Discussions are at an early stage. Alberta Energy Minister Brian Jean conducted in-person meetings in Japan with officials from JOGMEC, JBIC, METI, and private sector refiners and traders. A Memorandum of Understanding between Alberta and JOGMEC has been signed, confirming that Alberta talks with Japan on Canadian crude imports have progressed beyond initial exploratory dialogue. No binding supply agreements have been finalised.

How large is Canada's oil production?

Canada is the world's fourth-largest oil producer. Output in 2026 is projected to surpass the record 5.3 million barrels per day achieved in 2025, driven primarily by continued oil sands expansion in Alberta.

Want to Track the Next Big Resource Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across more than 30 commodities — delivering actionable insights to subscribers ahead of the broader market. Explore historic examples of exceptional discovery returns and begin your 14-day free trial at Discovery Alert to position yourself at the leading edge of resource investment opportunities.