June 23, 2026

The Geology of Dominance: Why Guinea's Bauxite Controls the Aluminium World's Future

When commodity analysts discuss supply concentration risk, they typically point to oil markets, rare earth elements, or lithium. Yet one of the most structurally significant supply dependencies in modern industrial manufacturing exists in a material most people have never heard of: metallurgical bauxite. The aluminium supply chain runs entirely on it, and a single West African nation now commands a position within that chain that rivals the leverage OPEC once exercised over petroleum markets at its most influential.

Understanding why Guinea bauxite dominance and aluminium supply have become inseparable concepts requires examining not just production statistics, but the geological qualities, governance choices, and geopolitical pressures that have converged to produce one of the most consequential supply chain transformations of the current decade.

When big ASX news breaks, our subscribers know first

The Geological Foundation: Why Guinea's Ore Is Different

Bauxite is technically the third most abundant element compound in the Earth's crust, yet this geological abundance is profoundly misleading as an investment or industrial signal. The critical distinction is between bauxite that exists and bauxite that is commercially viable for alumina refining.

Most bauxite deposits globally carry elevated silica content, which creates substantial processing inefficiencies in the Bayer refining process. High silica ore consumes disproportionate quantities of caustic soda during alumina extraction, drives up energy inputs, and reduces refinery throughput — all of which add cost at every stage downstream.

Guinea's bauxite is geologically exceptional precisely because it is naturally low in reactive silica. This characteristic is not a marginal quality advantage; it is a fundamental processing cost differential that alumina refiners price directly into their procurement decisions. When a Chinese refinery operator weighs Guinean ore against lower-grade alternatives, the economics of ore quality translate immediately into operating margin. This is why Guinea's rise has not simply been a volume story but a quality displacement story.

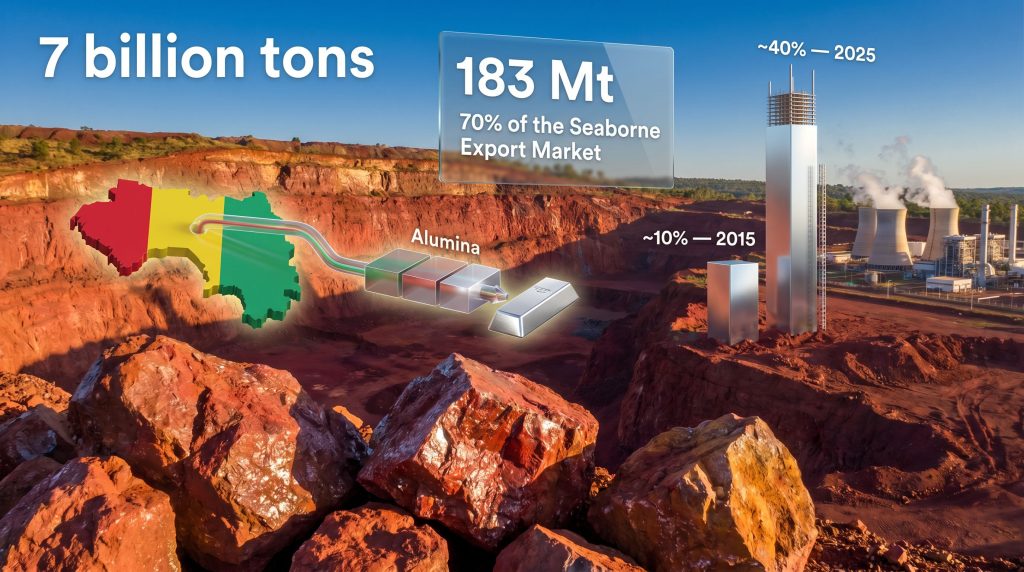

The country holds an estimated 7.4 billion tons of metallurgical-grade bauxite reserves, the largest proven deposit of its kind on Earth. Combined with the ore's quality characteristics, this reserve base gives Guinea a form of geological market power that cannot be replicated by competitor nations through capital investment alone. You cannot build better geology. For context on how this fits into global bauxite production, Guinea's position is truly unmatched among producing nations.

From Peripheral Supplier to Seaborne Market Anchor

The speed of Guinea's production ascent is without parallel in modern mining history. Consider the trajectory across a single decade:

| Metric | 2015 | 2023 | 2025 |

|---|---|---|---|

| Guinea's global output share | ~10% | ~35% | ~40% |

| Guinea's seaborne export share | ~20% | ~55% | ~70% |

| Chinese imports from Guinea | 334,000 t | ~80 Mt | 149 Mt |

| Guinea's annual export volume | ~40 Mt | ~130 Mt | 183 Mt |

By 2023, Guinea had surpassed Australia as the world's largest bauxite producer, a milestone driven almost entirely by Chinese-backed capital deployment into Guinean mining infrastructure. Australian bauxite, while abundant, generally carries higher silica levels and faces longer shipping distances to Chinese refineries than Guinean material, creating a quality and logistics disadvantage that Chinese procurement strategies have steadily priced in over time.

By 2025, Guinea controlled approximately 40% of global bauxite output and an estimated 70% of the seaborne export market. These figures represent a concentration of market influence that fundamentally alters how supply disruptions, policy changes, and pricing dynamics propagate through the entire aluminium value chain. Furthermore, the major aluminium mining companies operating in this space have had to fundamentally recalibrate their sourcing and investment strategies in response.

"The critical insight often missed by generalist investors is that Guinea's market dominance was not built through price competition or political maneuvering. It was built on geological reality, cost economics, and the compounding effect of Chinese capital entering a jurisdiction with genuinely superior ore."

The Oversupply Paradox: Volume Without Discipline

Guinea's export volume surged 25% year-on-year in 2025, reaching 183 million metric tons and flooding the seaborne market with a quantity of ore that far outpaced incremental demand from alumina refiners. The predictable consequence was severe price compression: bauxite prices declined by approximately 50% over the course of 2025 and into early 2026.

This dynamic illustrates a counterintuitive principle that recurs throughout commodity market history. Dominant suppliers that expand volume without production discipline tend to destroy the very pricing power their resource endowment should theoretically confer. Guinea's geological monopoly is a genuine and durable competitive advantage, but producing into a falling price environment simply transfers economic value from Guinea's government and citizens to downstream aluminium manufacturers in China and elsewhere.

The parallel with other resource-rich developing nations is direct and instructive:

| Country | Resource | Production Problem | Control Mechanism Adopted |

|---|---|---|---|

| Indonesia | Nickel | Rapid volume expansion, price collapse | Mining and export quotas, processing mandate |

| DR Congo | Cobalt | Volume-driven price destruction | Export quota system (with significant disruption) |

| Guinea | Bauxite | 25% YoY export surge, 50% price decline | Combined mining and export quota framework (proposed) |

All three nations face the same structural tension: extractive sectors that outpaced governance frameworks, producing conditions in which the nation bearing the environmental and social costs of mining captures an ever-shrinking share of the downstream economic value. Indeed, Indonesia's nickel strategy provides perhaps the most directly applicable policy playbook for Guinea's policymakers to study.

Three Strategic Scenarios for Guinea's Response

Scenario One: The Quota Stabilisation Model

Guinea's government is evaluating a combined mining and export quota framework designed to close what insiders describe as the gap between permitted extraction volumes and actual shipment volumes. Under this approach, operators would be prevented from exporting bauxite in excess of their licensed production allocations, effectively capping the supply overhang that produced 2025's price collapse.

The calibration challenge is significant. Guinea's exports represent 74% of China's total bauxite import volume, meaning that poorly designed restrictions carry the potential to generate acute supply disruptions in Chinese alumina refining, with cascading consequences for aluminium metal production and pricing globally. Conakry's policymakers are acutely aware of the distinction between the Indonesian model, which achieved a relatively controlled market transition, and the Congolese cobalt experience, which generated considerable disruption and investor uncertainty.

Scenario Two: The Value Chain Ascent Model

The more strategically ambitious pathway involves replicating Indonesia's industrialisation trajectory by mandating or incentivising domestic alumina refining before bauxite export. Indonesia imposed an outright bauxite export ban in 2023 to force mining companies to build processing capacity onshore, successfully redirecting significant industrial investment into the country.

Guinea's government has established a target of five to six additional operational alumina refineries with combined processing capacity of approximately 7 million tons per year by 2030. Achieving this would fundamentally redefine what Guinea exports, shifting from low-value unprocessed ore to alumina, the intermediate product that commands substantially higher per-ton margins in global trade.

What makes this scenario particularly notable is the difference between bauxite and alumina as traded commodities. Alumina typically sells for roughly four to five times the per-ton value of raw bauxite, meaning that even partial success in the processing transition would dramatically improve Guinea's revenue capture per unit of geological resource consumed. According to Reuters' analysis of Guinea's bauxite ambitions, this value-chain shift could meaningfully reshape the entire aluminium supply structure by the end of the decade.

Scenario Three: The Enforcement Precedent Model

The seizure of mining assets from Emirates Global Aluminium following its failure to deliver on committed refinery development obligations has introduced a new dimension to Guinea's regulatory posture. This enforcement action functions as a credible signal to all operating companies that processing commitments carry genuine consequences, fundamentally altering the risk calculation for operators who might otherwise treat refinery development pledges as negotiable.

Whether this enforcement posture attracts or deters foreign capital depends heavily on how consistently it is applied and how clearly the investment rules are communicated in advance.

China's Structural Dependency and Its Strategic Response

China's aluminium sector faces a dependency on Guinean bauxite that has no near-term solution. Domestic Chinese bauxite reserves, while historically substantial, have been progressively depleted through decades of intensive extraction. The ore that remains is substantially lower in quality than Guinean material. Simultaneously, China's aluminium smelting capacity expanded dramatically across the 2000s and 2010s, requiring a proportional build-out in alumina refining infrastructure that Chinese domestic ore supply cannot support.

The scale of this dependency is difficult to overstate. Chinese imports of Guinean bauxite grew from 334,000 tons in 2015 to 149 million tons in 2025, a transformation of import dependence that occurred within a single decade. In 2025, Guinea accounted for 74% of all bauxite entering China. Consequently, China's raw material demand patterns across multiple commodities underscore just how structurally exposed the country's industrial base has become.

Anticipating Guinea's regulatory tightening, Chinese buyers accelerated import volumes ahead of any quota implementation. Monthly imports from Guinea reached a record 18 million tons in March 2026, reflecting deliberate inventory accumulation designed to buffer against potential supply restrictions. Precautionary stockpiling provides short-term insulation but cannot resolve the underlying structural condition.

China's more durable strategic response is being expressed through direct investment in Guinean processing capacity. Chalco, China's state-owned aluminium producer, committed to constructing a 1.2-million-ton-per-year alumina refinery within Guinea at a cost of approximately $1 billion, its first major overseas downstream aluminium investment. This represents a significant strategic shift: rather than resisting Guinea's value-chain ambitions, China's state sector is positioning itself to operate within, and therefore shape, the transition to in-country processing.

Chalco's commitment is the third Chinese-backed alumina refinery project announced in Guinea within a compressed timeframe, suggesting a coordinated recognition within China's state industrial complex that Guinea's processing transition is structurally inevitable.

The next major ASX story will hit our subscribers first

Guinea's Existing Refining Base and the Infrastructure Gap

Against the ambition of 7 million tons of annual alumina capacity by 2030, Guinea's current refining infrastructure represents a very modest foundation. The country's sole operational refinery is the Friguia facility, with an origin story spanning multiple decades and ownership structures:

- Constructed in the 1960s under French ownership through aluminium producer Pechiney.

- Subsequently acquired by U.S. producer Reynolds Metals.

- Held by Russia's Rusal since 2008, which has operated it through periods of significant disruption.

- The plant was entirely non-operational from 2012 to 2018 and currently operates below its nameplate capacity of 650,000 tons per year.

Reaching 7 million tons of annual alumina output by 2030 from this base requires an unprecedented acceleration of greenfield and brownfield refining investment within an eight-to-ten year window. Even optimistic scenarios suggest the 2030 target is highly ambitious, though the direction of travel is unambiguous.

The West African Alumina Corridor: A Regional Transformation

Guinea's industrial ambitions are not developing in isolation. A broader West African value-chain transition is underway that could reshape the regional geography of aluminium production:

- Nigeria has committed to a $1.3 billion alumina refinery investment in partnership with the Africa Finance Corporation (AFC), a pan-African development finance institution.

- Ghana is advancing refinery development under the auspices of the Ghana Integrated Aluminium Development Corporation, a state vehicle established specifically to develop the country's bauxite resources into processed aluminium products.

The convergence of these national programmes creates the conditions for a genuine West African alumina processing cluster. If it materialises at scale, the structural consequences for global aluminium supply chains are threefold:

- The seaborne bauxite market contracts as West African nations export processed alumina instead of raw ore, reducing the volume of unrefined bauxite moving through global shipping lanes.

- The global alumina export market expands as West African alumina enters trade flows at scale, introducing new competitive dynamics into a market currently dominated by Australian producers and Chinese state refineries.

- Chinese domestic alumina refineries face competitive pressure from the very suppliers that currently provide their primary raw material input, creating a novel and uncomfortable competitive dynamic within China's aluminium industrial ecosystem.

The Critical Constraint: Energy Infrastructure

One factor that significantly differentiates Guinea's industrialisation pathway from Indonesia's is energy. Indonesia possesses abundant domestic coal-fired generation capacity, which powered both the alumina refining and aluminium smelting components of its industrialisation strategy. Guinea does not currently possess the energy infrastructure required to sustain large-scale industrial alumina processing at the volumes its 2030 targets imply.

This energy gap is not an insurmountable obstacle, but it does impose a sequencing constraint on Guinea's ambitions. Near-to-medium term targets are realistically capped at the alumina production stage. Full aluminium smelting within Guinea's borders remains a longer-horizon possibility contingent on material investment in hydroelectric or other generation capacity. Guinea's significant hydropower potential remains largely undeveloped, and bridging that gap will be central to any meaningful aluminium smelting ambition. However, the broader energy transition demand for aluminium globally means that the incentive to resolve this infrastructure constraint has rarely been greater.

"Investors and analysts who treat Guinea's aluminium ambitions as a near-term smelting story are likely misreading the timeline. The realistic near-term prize is alumina processing, and even that requires significant energy infrastructure investment to achieve at the targeted scale."

Frequently Asked Questions

Why does Guinea's low-silica bauxite command a quality premium?

The Bayer process used to refine bauxite into alumina is chemically sensitive to reactive silica content. High-silica ore requires substantially more caustic soda per ton of alumina produced, drives up processing costs, and reduces refinery efficiency. Guinea's naturally low-silica ore delivers meaningful per-ton cost advantages to alumina refiners, which is reflected in procurement preferences and pricing. As Al Circle's detailed overview of Guinea's bauxite journey illustrates, this quality advantage has been recognised by the industry for decades.

What distinguishes bauxite from alumina in trade terms?

Bauxite is the raw ore extracted at the mine. Alumina, or aluminium oxide, is the refined intermediate produced through the Bayer process and sold to aluminium smelters. Alumina typically commands four to five times the per-ton value of raw bauxite, making the transition from bauxite exporter to alumina exporter economically transformative for a producing nation.

Could Guinea replicate Indonesia's full export ban model?

Guinea is studying the Indonesian model carefully but faces different constraints, particularly in energy infrastructure and the scale of China's existing dependency. An outright export ban risks generating acute supply disruptions that rebound on Guinea through investment withdrawal and diplomatic pressure. A calibrated quota system with processing incentives is considered more appropriate to Guinea's specific circumstances.

How exposed is the global aluminium market to Guinea supply disruption?

Significantly. Guinea bauxite dominance and aluminium supply are now so deeply intertwined that the country accounts for approximately 40% of global bauxite production and 70% of the seaborne export market. Any material supply disruption in Guinea would propagate through alumina refining capacity globally, affecting aluminium metal production and pricing within a matter of months.

Projected Milestones and the Long-Term Outlook

| Timeline | Development | Strategic Significance |

|---|---|---|

| 2023 | Guinea surpasses Australia in bauxite output | Market dominance established |

| 2025 | 183 Mt exports; 74% of China's imports | Peak raw material dependency confirmed |

| 2026 | Chalco refinery commitment; quota framework development | Processing transition begins |

| 2030 | Target: 7 Mt/yr alumina refining capacity | West African alumina hub potential |

The trajectory Guinea is pursuing represents one of the most significant potential restructurings of the global aluminium supply chain since Chinese smelting capacity emerged as the dominant force in global metal production during the early 2000s. Whether it succeeds will depend on the quality of governance decisions made in Conakry over the next several years, the pace of energy infrastructure development, and the willingness of international capital to commit to long-duration projects in a regulatory environment that is still being defined.

What is not in question is the geological foundation. Guinea bauxite dominance and aluminium supply dynamics are now structurally linked in ways that will shape commodity markets for decades to come. The remaining question is whether Conakry can translate geological advantage into durable industrial value, completing a transition that has historically proven far more difficult in practice than in strategic planning documents.

This article contains forward-looking analysis and projections based on publicly available information. Commodity markets, regulatory environments, and geopolitical conditions are subject to rapid change. Nothing in this article constitutes financial advice. Readers should conduct independent research before making investment decisions.

Want To Identify the Next Major ASX Mineral Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex geological and commodity data into actionable investment insights for traders and long-term investors alike. Explore historic examples of discovery-driven returns and begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.