July 19, 2026

Algeria's energy sector transformation represents a critical juncture where declining production meets unprecedented European demand for alternative suppliers. The declining natural gas output, down 7% to 98.3 billion cubic meters in 2024, creates immediate investment imperatives precisely when energy transition challenges across developed markets elevate demand for reliable hydrocarbon sources. Furthermore, the Algeria oil and gas licensing round 2026 emerges as a strategic response to bridge substantial production gaps while positioning the nation as Europe's preferred alternative supplier during a period of heightened energy security concerns.

Current Market Position and Strategic Context

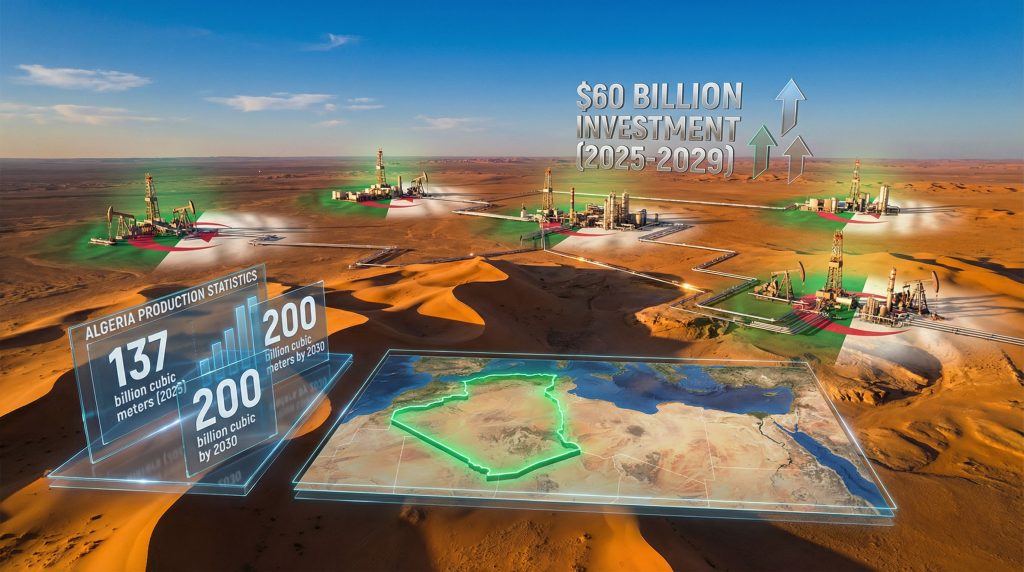

Algeria's position within North Africa's energy hierarchy reflects both substantial resource advantages and structural challenges that define investment attractiveness. The nation maintains proven natural gas reserves of approximately 159 trillion cubic feet, establishing it as one of Africa's most significant hydrocarbon endowments. Current annual gas production reaches 137 billion cubic meters in 2025, providing baseline metrics for evaluating expansion potential within regional and global supply chains.

The country's strategic geographic positioning creates substantial export advantages through established pipeline infrastructure connecting North African production centres to European consumption markets. The Transmediterranean Pipeline and Maghreb-Europe Pipeline systems collectively transport Algerian gas to Spain, Italy, and France, providing competitive advantages over frontier producers lacking developed export corridors.

However, production trends reveal concerning trajectories that underscore the urgency of Algeria's 2026 licensing initiative. Natural gas output declined 7% to 98.3 billion cubic meters in 2024, creating immediate imperatives for new field development precisely when European energy markets demonstrate heightened demand for alternative supply sources following geopolitical disruptions to traditional providers.

The intersection of production deficits with favourable market conditions positions Algeria's upcoming licensing round as a critical inflection point. Moreover, trade war market impact considerations further emphasise the importance of diversified energy partnerships. European energy security concerns, particularly following supply chain disruptions, have elevated demand for reliable North African suppliers, creating optimal timing for attracting international investment capital to aging hydrocarbon infrastructure.

When big ASX news breaks, our subscribers know first

Economic Drivers Shaping Investment Strategy

The fundamental economics driving Algeria's 2026 licensing strategy centre on bridging substantial production gaps while capitalising on favourable global market conditions. Current production targets establish aggressive expansion parameters: increasing annual gas production from 137 billion cubic meters in 2025 to 200 billion cubic meters by 2030, representing a 46% growth requirement over five years.

This production expansion translates to average annual growth requirements of approximately 8.8% year-over-year, demanding sustained capital investment and operational excellence across multiple project phases. The associated investment commitment of $60 billion for 2025-2029 represents one of North Africa's largest energy sector capital deployment programmes, encompassing exploration, development, infrastructure modernisation, and processing facility enhancements.

Production Gap Analysis and Market Opportunity

The production shortfall results from multiple structural factors that create both challenges and opportunities for international investors. Declining output from mature fields in established basins like Berkine and Hassi Messaoud, combined with limited new field development over the past 15 years due to capital constraints, necessitates comprehensive field replacement and enhancement programmes.

Average decline rates in mature Algerian fields range from 5-8% annually without intervention, requiring continuous replacement drilling and enhanced recovery initiatives. This technical reality creates sustained demand for advanced extraction technologies and specialised operational expertise that international operators can provide through partnership arrangements.

The European Union's REPowerEU initiative, launched in response to energy security concerns, explicitly targeted diversification away from traditional suppliers, positioning North African producers as strategic partners. Furthermore, recent oil price crash insights demonstrate how geopolitical tensions can rapidly reshape global energy markets. European natural gas demand, projected at approximately 400 billion cubic metres annually through 2030, creates sustained market conditions supporting Algerian export expansion.

Investment Requirements and Infrastructure Modernisation

Beyond exploration and production activities, the licensing round represents comprehensive infrastructure modernisation requiring capital deployment across transportation networks, processing facilities, and export terminals. Algeria's existing infrastructure, developed primarily during the 1970s and 1980s, requires substantial upgrades to accommodate increased production volumes and modern efficiency standards.

The country's production infrastructure includes major processing facilities at Arzew and Skikda, which liquefy natural gas for export and process crude oil for domestic consumption and international markets. These facilities have operated continuously for decades, creating opportunities for technological modernisation and capacity expansion through international partnerships.

Geological Basin Investment Returns Analysis

The Algeria oil and gas licensing round 2026 encompasses 24 onshore blocks distributed across five major geological provinces, each presenting distinct risk-return profiles for international investors. This portfolio distribution reflects strategic positioning to offer diversified opportunities across geological systems with varying technical complexity and commercial potential.

Berkine Basin Characteristics and Commercial Advantages

The Berkine Basin represents one of Africa's most prolific petroleum systems, having produced over 2 billion barrels of crude oil and gas equivalent since commercial development began in the 1950s. Current producing fields include Hassi Messaoud (crude oil), Hassi Rmel (natural gas), and Tin Fouyad (crude oil and gas), demonstrating sustained commercial productivity over multiple decades.

The basin's production infrastructure advantage is substantial, with approximately 60-70% of Algeria's crude oil production deriving from this geological province. Established processing and export systems eliminate infrastructure development delays that characterise frontier exploration areas, enabling immediate revenue generation potential for new field development projects.

Key Berkine Basin Advantages:

- Established production infrastructure reducing development timelines

- Proven commercial discoveries with documented reserve estimates

- Lower exploration risk profile based on extensive geological data

- Immediate revenue generation potential through existing pipeline networks

- Skilled workforce availability and operational support systems

Illizi Basin Unconventional Resource Opportunities

The Illizi Basin, located in southeastern Algeria, contains significant unconventional gas resources with tight sandstone formations holding substantial in-place gas volumes estimated at 200+ trillion cubic feet. The basin's most prominent development, the In Amenas field (joint venture with BP and Statoil), produces approximately 110,000 barrels of oil equivalent daily, demonstrating commercial viability of complex projects.

Advanced seismic data acquired over multiple vintages provides high-quality subsurface images necessary for well placement optimisation and reserve estimation. The basin's proximity to the Trans-Mediterranean Pipeline and existing processing infrastructure at In Salah reduces development timelines and capital requirements compared to greenfield frontier areas.

Illizi Basin Technical Characteristics:

- Primary reservoirs: Lower porosity (8-12%) requiring stimulation technologies

- Permeability: 0.1-10 millidarcies necessitating advanced completion designs

- Resource potential: Substantial tight gas formations with proven productivity

- Infrastructure: Established pipeline connections and processing facilities

- Technology requirements: Horizontal drilling and hydraulic fracturing expertise

Western and Northern Basin Frontier Prospects

Western basins, including Berkine Basin extensions and separate systems like the Murzuq Basin (straddling Algeria-Libya border areas), represent higher-risk frontier exploration territories with limited drilling history. Success rates in analogous North African frontier basins range from 15-25%, compared to 40-60% in established basins, requiring higher risk-adjusted return expectations.

Northern basins, proximate to Mediterranean coastal areas, offer deepwater exploration opportunities requiring substantial capital investment and extended development timelines. Successful discoveries in comparable Mediterranean geological systems offshore Libya and Tunisia have demonstrated commercial viability of similar plays, though technical complexity and capital requirements exceed onshore conventional developments.

Fiscal Framework and Regional Competitiveness

Algeria's fiscal regime operates through production sharing agreements (PSAs) that divide economic value between the government and operators through cost recovery mechanisms and profit-sharing percentages. The Algeria oil and gas licensing round 2026 framework must balance government revenue objectives with investor return requirements while maintaining competitiveness against regional alternatives.

Additionally, the broader context of tariffs impact analysis suggests that trade policies can significantly affect international investment flows, making stable fiscal frameworks even more critical for attracting capital.

Comparative Regional Analysis

Algeria's Current Fiscal Structure:

- Signature bonuses: Variable based on acreage quality and competition

- Cost recovery: Approximately 50-60% of capital costs recoverable

- Profit oil splits: Typically 80-85% government, 15-20% operator

- Regulatory framework: Established legal structure with foreign investment provisions

Regional Competitor Comparison:

| Country | Cost Recovery % | Profit Oil Split (Gov/Op) | Signature Bonus Range |

|---|---|---|---|

| Algeria | 50-60% | 80-85% / 15-20% | Variable by block |

| Egypt | 70-80% | 70-75% / 25-30% | $15-50 million |

| Libya | 60-70% | 65-75% / 25-35% | $100+ million |

| Mauritania | 60-70% | 75-80% / 20-25% | $200-500 million |

Egypt's modified PSA framework generally offers operators marginally more favourable economics through higher cost recovery provisions and improved profit oil allocations. Libya, despite offering competitive signature bonuses exceeding $100 million for premier acreage, faces substantial political risk premia that increase cost of capital requirements.

Mauritania's emerging deepwater petroleum regime targets major international operators through substantial signature bonuses ranging $200-500 million for frontier deepwater blocks, though higher technical and geopolitical risks offset fiscal advantages for many investors.

Investment Decision Framework Considerations

The relationship between fiscal terms and investment decisions operates through project return calculations where higher government take reduces investor returns, affecting internal rate of return (IRR) calculations typically ranging 15-25% for competitive international oil and gas projects.

Algeria's fiscal framework must demonstrate stability and consistency over multiple licensing cycles to maintain investor confidence. The successful previous round, which attracted companies of various nationalities across five development areas with combined commitments exceeding $553 million, provides evidence of institutional capacity to manage complex international partnerships.

Technology Transfer and Enhanced Recovery Integration

The Algeria oil and gas licensing round 2026 emphasises enhanced oil recovery (EOR) and improved oil recovery (IOR) projects, indicating strategic focus on maximising returns from existing discoveries rather than purely greenfield exploration. This approach requires advanced technological capabilities and operational expertise that international partners can provide through collaborative arrangements.

Advanced Recovery Technologies and Economic Impact

Technology-Driven Value Creation Opportunities:

- Unconventional gas development: Horizontal drilling and hydraulic fracturing techniques for tight formations

- Digital reservoir management: Advanced monitoring and optimisation systems for mature field development

- Carbon capture and storage: Integration with environmental compliance and enhanced recovery applications

- Advanced drilling technologies: Extended-reach drilling and multilateral completions for complex reservoirs

The Hassi Rmel field, a giant natural gas accumulation discovered in 1956, has produced over 6 trillion cubic feet of gas while maintaining average production rates of 25-30 billion cubic metres annually. The field's longevity demonstrates both resource quality and the potential for technological enhancement to extend productive life and optimise recovery factors.

Operational Excellence and Knowledge Transfer

International operators bring specialised expertise in project management, safety protocols, and environmental compliance that complement Algeria's technical workforce and existing operational capabilities. The In Amenas field's successful development, achieving 110,000 barrels of oil equivalent daily through advanced well completion designs and subsurface monitoring systems, illustrates both technical complexity and viability of collaborative approaches.

Technology transfer extends beyond extraction techniques to encompass digital infrastructure, data management systems, and predictive maintenance protocols that enhance operational efficiency and reduce long-term operating costs across portfolio developments.

Natural Gas as Transition Fuel Economics

Algeria's strategic positioning of natural gas as a bridge fuel during global energy transition capitalises on its lower carbon intensity compared to coal and oil while renewable energy infrastructure scales globally. This market positioning creates sustained demand drivers supporting long-term investment viability beyond traditional hydrocarbon cycles.

Market Positioning Analysis and Demand Sustainability

Strategic Market Advantages:

- European Union's REPowerEU plan creates sustained import demand through 2035

- LNG export potential to Asian markets experiencing continued economic growth

- Domestic industrial development opportunities in petrochemical and fertiliser sectors

- Power generation applications during renewable energy transition phases

European natural gas demand, while declining from peak levels, maintains substantial volumes through the transition period as renewable energy systems require backup generation capacity and industrial applications continue requiring gas feedstocks. Similarly, Saudi exploration licenses demonstrate how regional competitors are positioning themselves strategically in global energy markets. Algeria's proximity to European markets through existing pipeline infrastructure provides cost advantages over distant LNG suppliers.

The country's potential for petrochemical sector expansion creates domestic value-added opportunities that extend beyond commodity exports. Natural gas serves as both energy source and chemical feedstock for fertiliser production, plastics manufacturing, and other industrial applications with sustained global demand profiles.

The next major ASX story will hit our subscribers first

Investment Structures and Partnership Models

The Algeria oil and gas licensing round 2026 framework must accommodate diverse investor profiles while ensuring optimal risk distribution and technology transfer benefits. Partnership models require careful structuring to balance government revenue objectives, operator return requirements, and operational efficiency considerations.

What Are the Optimal Investment Structure Options?

Recommended Partnership Models:

- Production sharing agreements: Competitive terms balancing government revenue and operator returns

- Joint venture arrangements: Partnerships with Sonatrach providing local expertise and market access

- Service contract models: Specialised technical expertise for specific operational challenges

- Risk-service contracts: Exploration activities with graduated payment structures based on success metrics

The previous licensing round's success in attracting major international companies including TotalEnergies, Eni, and Sinopec demonstrates Algeria's capacity to structure competitive terms. These operators collectively committed over $553 million in investments across five development areas, indicating substantial confidence in fiscal stability and operational conditions.

Risk Distribution and Financial Optimisation

Effective partnership structures distribute geological, technical, commercial, and regulatory risks according to each party's comparative advantages and risk tolerance. International operators typically assume technical and operational risks while government entities retain resource ownership and long-term revenue streams.

Risk Mitigation Strategies:

- Diversified portfolio approaches across multiple geological basins

- Phased development programmes allowing gradual capital deployment

- Comprehensive insurance coverage for political and operational risks

- Flexible operational planning accommodating market volatility

Project Development Timelines and Investment Horizons

Investment decision-making for the Algeria oil and gas licensing round 2026 requires clear understanding of development timelines and cash flow profiles across different project types. The licensing framework extends from current nomination processes through anticipated bid submission deadlines, with successful projects requiring 3-7 years for initial production depending on technical complexity and infrastructure requirements.

Development Phase Economics and Milestone Planning

Project Development Timeline Framework:

- Nomination period: Through January 31, 2026

- Bid round launch: Early 2026 (anticipated based on government statements)

- License award: Mid-2026 (projected following evaluation processes)

- First production: 2029-2032 (estimated based on project complexity)

The timeline variation reflects different project characteristics: existing field development and infill drilling programmes can achieve first production within 2-4 years, while frontier exploration discoveries require 5-8 years for initial production. Unconventional resource developments typically fall within 3-5 years depending on infrastructure availability and completion complexity.

Cash Flow Projections and Financial Planning

Successful project economics require careful cash flow modelling incorporating exploration costs, development capital expenditure, operational expenses, and revenue profiles over project lifespans typically extending 15-25 years for major developments. Algeria's established infrastructure and experienced workforce reduce certain cost categories while geological complexity and regulatory requirements influence others.

The $60 billion investment programme for 2025-2029 provides context for sector-wide capital deployment expectations, with individual projects ranging from $500 million to $5 billion depending on scope and technical requirements. These investment levels require long-term financial commitments and sustained operational focus that favour experienced international operators with proven technical capabilities.

Algeria's 2026 oil and gas licensing round represents a transformative opportunity within North African energy markets, where established resource endowments meet evolving global demand patterns and technological advancement capabilities. The intersection of production necessity, favourable market conditions, and institutional capacity creates optimal conditions for international investment partnerships that can deliver sustained economic benefits while supporting regional energy security objectives.

This analysis is based on publicly available information and industry assessments. Investment decisions should incorporate comprehensive due diligence, professional advice, and consideration of individual risk tolerance and investment objectives. Hydrocarbon exploration and development involve substantial risks including geological uncertainty, commodity price volatility, and regulatory changes.

Ready to Capitalise on North African Energy Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant mineral and energy discoveries across global markets, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Begin your 14-day free trial today and secure your market-leading advantage in emerging resource sectors.