June 11, 2026

The Mediterranean Supply Gap That Europe Cannot Afford to Ignore

Every major gas supply crisis in modern European history has shared one common characteristic: the warning signs were visible years before the disruption became acute. Declining field productivity, underinvestment cycles, and the slow erosion of export surpluses by domestic consumption are not sudden events. They are structural processes that accumulate over decades before the consequences become unavoidable. Understanding Algeria's current upstream predicament requires exactly this kind of long-cycle thinking, because the forces shaping its export capacity today were set in motion well before the current European energy emergency brought North African gas back into strategic focus.

Algeria gas production problems are not a single failure but a compounding of geological, regulatory, and demographic pressures that have been building simultaneously, each one accelerating the effect of the others. Furthermore, these pressures intersect directly with the broader LNG supply outlook that European policymakers are scrambling to recalibrate.

When big ASX news breaks, our subscribers know first

The Geological Reality Underneath Algeria's Resource Wealth

Algeria holds estimated total recoverable gas resources of between 2.5 and 3.4 trillion cubic metres, placing it among the most resource-endowed nations outside the Middle East and Russia. That geological inheritance is real and significant. The challenge is that the infrastructure and field development translating those resources into exportable volumes is anchored to a production base that is ageing rapidly.

The Hassi R'Mel field, which has been the cornerstone of Algerian gas output since the early 1960s, illustrates this problem with striking clarity. After more than six decades of continuous production, the field's original resource base of approximately 3 trillion cubic metres has been depleted to roughly 20% of its former volume. Output peaked in the mid-1990s, and the trajectory since then has been one of managed decline rather than growth. Satellite field tie-ins and nearby development programmes have partially offset this trajectory, but they cannot fully compensate for the fundamental exhaustion of what was once one of the world's great gas accumulations.

A closely parallel decline pattern is visible at Hassi Messaoud, Algeria's dominant oil field. The simultaneous maturity of both flagship assets points to a basin-wide phenomenon rather than isolated reservoir-level challenges. This is a critically important distinction for investors and policymakers assessing Algeria's long-term supply credentials: the problem is not confined to a single field that can be remediated through targeted intervention. It is a structural characteristic of Algeria's entire producing heartland.

What Gas Reinjection Demands Reveal About True Export Capacity

One dimension of Algeria's production constraints that rarely appears in headline statistics is the reinjection obligation. A meaningful portion of Algeria's gross gas output is not available for export or domestic sale because it must be pumped back into oil reservoirs to maintain formation pressure and sustain associated crude production. As oil fields age and natural reservoir pressure declines, the proportion of produced gas redirected to reinjection can increase, creating an invisible ceiling on commercially available volumes that is entirely separate from the production figures reported publicly.

This dynamic means that gross output statistics systematically overstate the gas actually available for export, and it compounds as the wider producing basin matures.

The 14-Year Policy Freeze and Its Lasting Upstream Consequences

Between 2005 and 2019, Algeria maintained a regulatory framework that prohibited production-sharing contracts and service agreements for natural gas assets, while simultaneously requiring that Sonatrach, the national oil company, hold a minimum 51% equity stake in all upstream ventures. This combination of restrictions effectively closed Algeria's upstream sector to meaningful foreign participation during a 14-year window that proved to be critical.

The timing was particularly damaging. The supply additions from discoveries made during the exploration activity of the 1980s and 1990s were beginning to plateau precisely when this investment freeze took hold. Without fresh capital flowing into development drilling and new field tie-ins, the production base had no replacement source of growth. The 2019 hydrocarbons law reform removed the mandatory equity floor and broadened the range of permissible contract structures, but legislative changes cannot retroactively compress the development cycle.

A gas field discovery does not become a producing asset overnight. From licence award to first commercial gas typically requires between seven and ten years of appraisal, engineering, drilling, and infrastructure commissioning. This means the investment drought of 2005 to 2019 will continue to suppress Algerian production capacity well into the late 2020s, regardless of how aggressively new capital is deployed today.

Daily gas output rose from approximately 278 million cubic metres per day in 2021 to 287 million cubic metres per day in 2023, but analysts widely regard that 2023 figure as a production ceiling rather than a launchpad for sustained growth. The incremental gains from satellite field expansions and enhanced recovery programmes at mature assets appear to have been largely exhausted. Consequently, natural gas price trends across global markets are increasingly reflecting this structural supply unease.

Domestic Demand: The Export Surplus Is Being Consumed from Within

| Metric | Estimated Figure |

|---|---|

| Algeria's domestic gas consumption (2025) | ~57 billion m³/year |

| Share of national output consumed domestically | More than 50% |

| Hydrocarbon contribution to GDP | ~10–12% |

| Hydrocarbon share of total export revenues | More than 90% |

Algeria consumed approximately 57 billion cubic metres of gas domestically in 2025, absorbing more than half of national production. The structural driver behind this consumption level is a heavily subsidised domestic energy pricing regime that makes gas artificially cheap across residential, industrial, and power generation sectors. Subsidised pricing removes the market signal that would otherwise encourage efficiency and demand moderation, creating a politically entrenched overconsumption pattern that is exceptionally difficult to reverse.

The power sector dynamic is particularly important and underappreciated in most external assessments of Algeria's export capacity. Algeria's electricity grid is almost entirely gas-fired, meaning that population growth, urbanisation, and rising living standards translate mechanically into higher gas demand with no diversification pathway to reduce that conversion. As the population continues growing and air conditioning penetration rises across a country with a predominantly hot climate, power sector gas demand will increase structurally.

The fiscal dimension makes this more than an energy planning problem. With hydrocarbons accounting for more than 90% of Algeria's total export revenues, the compression of exportable gas volumes by rising domestic consumption creates an immediate and direct threat to government finances. Lower export income reduces the capital available to Sonatrach for upstream reinvestment, which in turn constrains the future production growth that would be needed to restore export capacity. This is a self-reinforcing negative feedback loop with no easy exit. Indeed, energy export challenges of this nature are not unique to Algeria, as other resource-dependent economies face similarly difficult structural tradeoffs.

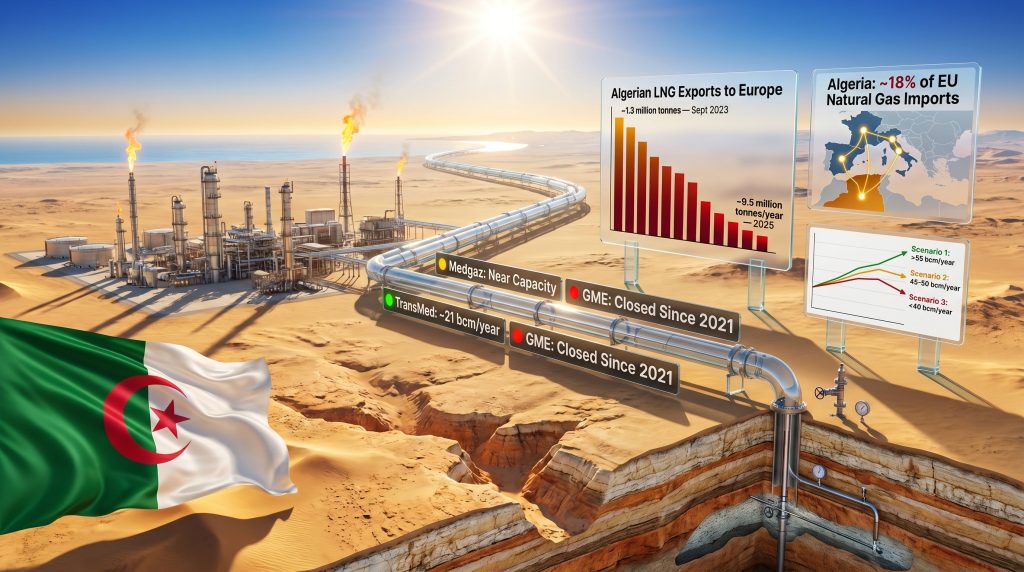

Pipeline Routes and LNG Infrastructure: Where the Real Bottleneck Sits

| Pipeline Route | Design Capacity | Approximate Recent Throughput | Status |

|---|---|---|---|

| TransMed (Tunisia to Italy) | ~32–35 billion m³/year | ~21 billion m³/year | Operational, underutilised |

| Medgaz (direct to Spain) | ~10–10.5 billion m³/year | Near capacity | Expansion talks initiated March 2026 |

| GME (Morocco–Spain) | ~8–10 billion m³/year | Zero | Closed since November 2021 |

The closure of the Gazoduc Maghreb-Europe pipeline in November 2021 removed approximately 8 to 10 billion cubic metres per year of export pathway capacity. Algeria declined to renew the transit agreement with Morocco following a deterioration in bilateral diplomatic relations, and the export corridor has remained closed since. This was not simply a political inconvenience: it represented a permanent reduction in Algeria's export routing flexibility that has not been compensated by capacity additions elsewhere.

TransMed is technically capable of moving significantly more gas than it currently carries, but increasing throughput depends on upstream availability rather than pipeline infrastructure. Medgaz, which runs directly from the Algerian coast to Almeria in Spain, is operating close to its nameplate capacity, and expansion discussions initiated in early 2026 to add approximately 1 billion cubic metres per year indicate European demand pull, though any physical capacity addition will require several years to engineer and commission.

Algeria's LNG position tells a revealing story about the upstream constraint. The country operates two export hubs at Arzew and Bethioua in the west, with combined nameplate liquefaction capacity of approximately 20.8 million tonnes per year, alongside the Skikda terminal in the east at roughly 4.5 million tonnes per year. Following Europe's post-Russia energy realignment, Algerian LNG surged to a single-month record of approximately 1.3 million tonnes in September 2023, representing a roughly 60% increase over the preceding monthly average of around 900,000 tonnes. By 2025, however, annual LNG exports to Europe had retreated to approximately 9.5 million tonnes, representing around 6% of European LNG imports and down roughly 2 million tonnes year-on-year.

The critical analytical point here is that the liquefaction terminals themselves are not the constraint. They carry unused capacity. The production shortfall sits upstream, at the wellhead, where insufficient gas is being delivered to the terminals to sustain peak throughput. This distinction matters enormously for assessing what investment in new fields could realistically achieve.

Algeria's Strategic Weight in European Gas Supply

As of 2025, Algeria supplies approximately 18% of total EU natural gas imports, ranking second only to Norway. This positioning gives Algiers genuine strategic leverage in European supply security discussions, particularly with its two primary customers. However, European gas prices and the associated gas price pressure on importers add further complexity to what might otherwise appear to be a straightforward supplier-buyer relationship.

-

Italy receives roughly 20 to 23 billion cubic metres per year from Algeria, covering approximately 30% of its total gas needs. Italy's structural dependence on Algerian supply makes it the most directly exposed European economy to any sustained reduction in Algerian output.

-

Spain sources approximately 25% of its gas imports from Algeria, though the diplomatic relationship between the two countries introduces a layer of political complexity that Italy does not face to the same degree.

-

France and Turkey are significant LNG buyers, with Turkey having absorbed close to a quarter of total Algerian LNG shipments during peak export periods.

The concentration of this dependency creates a structural asymmetry that both parties have recognised. Europe needs Algeria to remain a reliable and growing supplier. Algeria needs the export revenue that European gas purchases generate. Yet the conditions that would allow Algeria to fulfil the European supply role are not guaranteed, and the three scenarios facing Algerian gas exports through 2030 diverge significantly depending on investment outcomes and domestic policy choices.

The next major ASX story will hit our subscribers first

The 2026 Bidding Round: Commercial Relevance and Its Limits

Algeria's national hydrocarbon resources agency ALNAFT launched seven onshore conventional blocks in mid-2026, with bid submissions and ratification scheduled for November. The combined resource estimate across the seven blocks is approximately 2.1 billion barrels of oil and 66.5 billion cubic metres of natural gas. Four of the seven blocks are positioned in the Illizi-Ghadames basin near the Libyan and Tunisian borders, a sub-basin with meaningfully better existing infrastructure connectivity compared to the south-western acreage that dominated the 2024 round.

This geographic shift is commercially significant. The 2024 round's gas-prone south-western blocks carried attractive resource estimates but demanded greenfield infrastructure construction that extended development timelines and capital requirements. The Illizi-Ghadames focus of the 2026 round allows operators to leverage existing processing facilities, pipelines, and support infrastructure, shortening the time from licence award to first commercial gas.

The investor landscape has broadened considerably since the 2019 legal reforms:

-

Eni produces approximately 140,000 barrels of oil equivalent per day in Algeria and signed a $1.35 billion production-sharing agreement at the Zemoul El Kbar perimeter, with reserves of approximately 415 million barrels of oil equivalent including 9.3 billion cubic metres of gas

-

TotalEnergies and QatarEnergy entered the Ahara licence jointly, each holding 24.5% with Total as operator

-

PTTEP of Thailand committed to the gas-oriented Reggane 2 project

-

Sinopec took Hassi Berkane North and is pursuing gas exploration at Guern El Guessa

-

Midad Energy of Saudi Arabia signed a $5.4 billion contract for the Illizi South block near the Libyan border

-

Chevron and ExxonMobil remain in ongoing discussions centred on unconventional and shale gas potential

The diversity of this investor group, spanning European majors, Gulf sovereign capital, Asian national oil companies, and American independents, reflects a genuine reassessment of Algeria as an upstream destination. The entry of Saudi and Chinese capital in particular suggests that the country's attractiveness extends beyond its proximity to European buyers.

However, even an optimistic 2026 round outcome cannot solve Algeria's near-term export pressure. Given that upstream development cycles typically require seven to ten years from licence award to first commercial gas, the 2026 round's production contribution will not be felt before the early-to-mid 2030s. The export capacity question for the late 2020s depends entirely on fields already in or approaching development. The IEA's Algeria energy profile underscores this timeline challenge, noting that exploration success alone cannot resolve structural production gaps within short windows.

Three Conditions That Must Align for Algeria to Preserve Its Export Position

-

Capital deployment must be rapid and technically credible. Attracting licence awards is the beginning of the process, not the outcome. Operators must move from award to development drilling within two to three years to compress timelines.

-

Domestic demand growth must be structurally addressed. Without meaningful energy pricing reform or efficiency improvements, rising internal consumption will continue absorbing new production increments before they reach export markets.

-

Infrastructure development in underdeveloped gas provinces must accelerate. Gas-rich acreage in remote basins without pipeline connections and processing infrastructure cannot contribute to export volumes regardless of how favourable the contractual terms are.

The shale gas dimension adds another layer of long-term optionality. Algeria holds technically recoverable shale gas volumes that some estimates place among the largest in Africa, and Europe's interest in Algerian shale has grown considerably since the Russian supply disruptions. However, unconventional development faces substantial domestic political resistance, water availability constraints in desert environments, and technical complexity that makes meaningful commercial production unlikely within a five-year horizon. Discussions with American majors around unconventional potential represent a structural possibility for the 2030s rather than a near-term production solution.

FAQ: Algeria Gas Production Problems

Why is Algeria experiencing gas production problems despite holding large reserves?

Large total resource estimates do not translate automatically into deliverable production. Algeria's primary producing fields have been operating for six decades and are now deeply mature. The absence of sufficient new field development to replace declining volumes, compounded by a 14-year period of restricted foreign investment from 2005 to 2019, has left the active production base structurally weakened relative to the country's resource endowment.

How does domestic consumption affect Algeria's export capacity?

Algeria consumed approximately 57 billion cubic metres domestically in 2025, absorbing more than half of national gas output. Heavily subsidised energy prices drive systematic overconsumption across power generation, industry, and residential sectors. Every additional cubic metre consumed domestically reduces the volume available for pipeline exports or LNG cargo loading.

What is Algeria's current share of EU gas imports?

Algeria accounts for approximately 18% of total EU natural gas imports as of 2025, ranking second only to Norway.

Why did Algeria close the Morocco-Spain gas pipeline?

The Gazoduc Maghreb-Europe pipeline was shut in November 2021 when Algeria declined to renew the transit agreement with Morocco following a deterioration in bilateral diplomatic relations. The closure removed approximately 8 to 10 billion cubic metres per year of export pathway capacity that has not been replaced.

Can Algeria's LNG terminals increase output to compensate for pipeline constraints?

Algeria's liquefaction terminals at Arzew, Bethioua, and Skikda have unused nameplate capacity. The bottleneck is not terminal infrastructure but upstream gas availability. Insufficient gas is reaching the terminals from producing fields to sustain peak throughput.

Summary: Key Data Points on Algeria's Gas Production Challenges

| Indicator | Figure |

|---|---|

| Total recoverable gas resources (estimated) | 2.5–3.4 trillion m³ |

| Hassi R'Mel remaining resource (approx.) | ~20% of original 3 trillion m³ base |

| Daily production (2023 peak) | ~287 million m³/day |

| Domestic gas consumption (2025) | ~57 billion m³/year |

| Share of output consumed domestically | More than 50% |

| EU import share (2025) | ~18% |

| Italy's reliance on Algerian gas | ~30% of national supply |

| Spain's reliance on Algerian gas | ~25% of gas imports |

| LNG export peak (September 2023) | ~1.3 million tonnes/month |

| LNG exports to Europe (2025) | ~9.5 million tonnes/year |

| 2026 round resource estimate | 2.1bn barrels oil + 66.5bn m³ gas |

Algeria gas production problems, in summary, represent a convergence of geological maturity, policy-induced underinvestment, and structural domestic demand growth that no single intervention can resolve. The country's strategic importance to European supply security is beyond question, but its ability to sustain, let alone expand, its export role through the late 2020s remains genuinely uncertain.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or energy trading advice. All production figures, resource estimates, and scenario projections involve inherent uncertainty and should not be relied upon as guarantees of future performance. Readers should conduct independent due diligence before making any investment or commercial decisions based on the information contained herein.

Want to Stay Ahead of the Next Major Resource Discovery?

While Algeria's structural supply constraints reshape European energy markets, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex resource data into actionable investment insights — explore the historic returns major discoveries have generated and begin your 14-day free trial to position yourself ahead of the broader market.