June 11, 2026

When Inventory Becomes the Enemy of Recovery

Commodity markets have a well-documented habit of building surplus faster than they can destroy it. The mechanics are straightforward: production cycles run on multi-year capex commitments, while demand responds to shorter economic rhythms. When those two cycles fall out of sync, the result is inventory accumulation that can persist long after the original cause of oversupply has begun to correct. Understanding this dynamic is essential to interpreting where the nickel market stands today, and why a growing nickel stock overhang is complicating what many had hoped would be a clean recovery narrative.

When big ASX news breaks, our subscribers know first

What Is a Nickel Stock Overhang and Why Does It Matter?

Defining the Mechanism Behind the Price Ceiling

In commodity market terminology, a stock overhang is not simply a surplus. It describes a condition where accumulated inventories across exchange-registered warehouses and supply chains exceed the market's near-term capacity to absorb them through productive consumption. The distinction matters because it frames the problem as one of time as much as volume.

A structural surplus refers to the broader imbalance between annual production and consumption. A stock overhang is its physical manifestation: metal already refined, warehoused, and available for immediate delivery. When traders and end-users know that readily available supply is sitting in exchange warehouses, the urgency to bid for spot metal evaporates. This is precisely why elevated exchange inventory functions as a price ceiling, not merely a lagging indicator.

Exchange-registered warehouse stocks are among the most transparent real-time signals of physical market imbalance. Rising inventory at the LME or ShFE tells the market that supply is outpacing absorption, and that signal is factored into forward pricing almost immediately.

Nickel's overhang differs from those seen in other base metals because of the geographic and product complexity involved. The metal trades across multiple product forms, including Class I refined nickel, nickel pig iron (NPI), nickel matte, and mixed hydroxide precipitate (MHP), each serving different end markets and carrying different price dynamics. Surplus in one product class can cascade into discounts across others, amplifying the pressure on producers throughout the supply chain. Furthermore, understanding the Indonesian nickel price trends provides important context for how this cascade effect materialises in practice.

How Large Is the Current Nickel Inventory Buildup?

A Multi-Year High That the Market Cannot Ignore

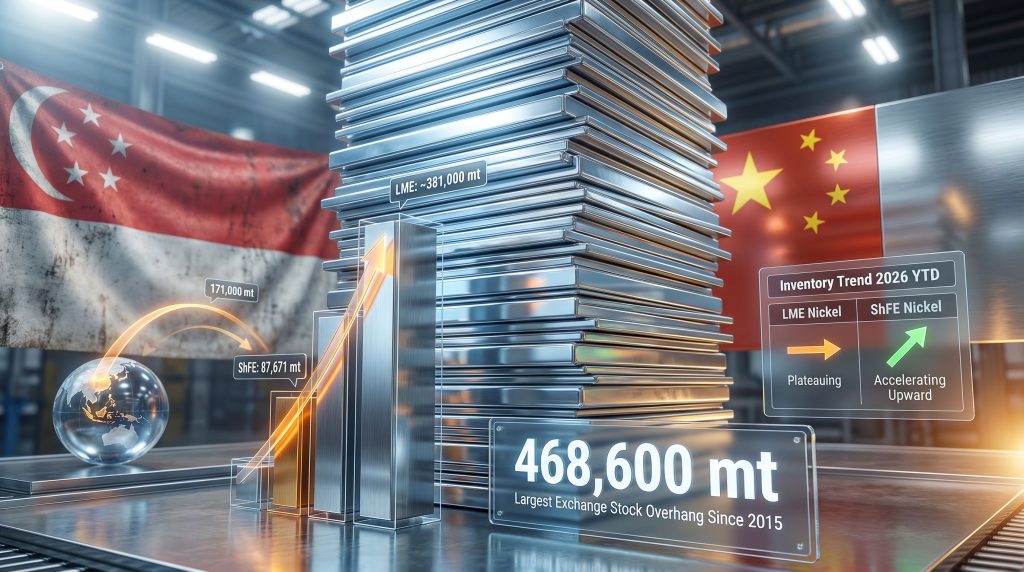

Combined inventories across the London Metal Exchange (LME) and the Shanghai Futures Exchange (ShFE) reached 468,600 metric tons as of mid-2026. To contextualise that figure: it represents approximately six weeks of total global nickel consumption and constitutes the largest nickel stock overhang recorded since 2015, according to Reuters market analysis.

The composition of that inventory pile is changing in ways that carry their own significance.

| Exchange | Inventory Level | Trend Direction | Notable Context |

|---|---|---|---|

| LME (incl. off-warrant) | ~381,000 mt (peak) | Plateauing / slight decline | Peaked after 9 consecutive months of growth |

| Shanghai Futures Exchange | 87,671 mt | Accelerating upward | Highest level since 2017 |

| Combined Total | 468,600 mt | Elevated | Largest since 2015 |

LME stocks accumulated for nine consecutive months between mid-2025 and early 2026, peaking just below the 400,000 metric ton threshold before edging approximately 20,000 tons lower. While this marginal decline has been interpreted by some as a signal that Western inventory accumulation is approaching exhaustion, the picture in Shanghai tells a different story. ShFE nickel stocks have nearly doubled since the start of 2026, reaching levels not seen since 2017, with no discernible seasonal moderation around the Chinese New Year period, which is typically associated with a temporary slowdown in industrial activity.

This eastward migration of surplus refined nickel is one of the more significant structural developments in the market. It reflects a shift in where excess supply is being absorbed, or more accurately, where it is being parked.

Why Did the Nickel Surplus Build So Aggressively?

Indonesia's Production Machine and the Four-Year Oversupply Cycle

The root cause of the current nickel stock overhang traces back to Indonesia's dramatic expansion of nickel processing infrastructure, financed predominantly by Chinese capital. Over a four-year period, Indonesia's output of Class II nickel products, primarily NPI for stainless steel and increasingly MHP for battery precursors, flooded global supply chains at a pace that demand simply could not match. The Indonesian nickel industry's growth challenges have been a defining feature of this structural oversupply period.

This was not a gradual build. Indonesian production scaled at a rate that overwhelmed the market's ability to price in the supply increase. The result was a compression of margins across the entire downstream chain, from NPI producers to Class I refined nickel smelters operating in higher-cost Western jurisdictions.

What makes this particularly complex from a market structure perspective is the product form cascade. When NPI prices collapse, stainless steel mills substitute away from Class I refined nickel, which then accumulates in exchange warehouses. When MHP discounts widen, battery precursor producers delay purchase commitments, extending the inventory overhang further up the chain. The surplus is therefore self-reinforcing across product categories.

Sulfur Constraints: A Lesser-Known Production Bottleneck

One factor not widely discussed in mainstream coverage is the role of sulfur availability as a constraint on Indonesian nickel processing. Converting nickel ore into certain intermediate products, particularly nickel matte and high-pressure acid leach (HPAL) outputs such as MHP, requires significant quantities of sulfuric acid. Indonesia's domestic sulfur supply infrastructure has struggled to keep pace with the rapid expansion of smelter capacity, creating a potential processing bottleneck that could curtail output independently of government quota decisions.

Government-imposed mining restrictions in Indonesia may further constrain ore availability in 2026, but the critical question for the global nickel market is not when Indonesian mine output falls — it is how long it takes for that upstream reduction to flow through refinery throughput and ultimately reach exchange-registered refined metal stocks. That transmission lag, potentially 12 to 18 months in some processing configurations, is a central reason why analysts expect the rebalancing process to be drawn out rather than sharp.

What Is Driving China's Nickel Import Surge?

The Counterintuitive Two-Way Trade Flow

China's nickel trade data for 2025 presents one of the more analytically puzzling pictures in recent commodity market history. According to World Bureau of Metal Statistics data, China imported 231,000 metric tons of refined nickel in 2025, the highest annual volume in four years. Over the same period, Chinese producers exported a record 171,000 metric tons, predominantly to LME-registered warehouses across Asia.

Importing and exporting refined nickel at scale simultaneously makes no conventional commercial sense unless one of those flows is being driven by something other than industrial demand. The most credible explanation, and one supported by analysis from Macquarie's commodities research team, is that a meaningful portion of China's import volumes in 2025 reflected government strategic stockpiling activity.

Macquarie's analysts estimated that government stockpile managers absorbed approximately 150,000 metric tons of nickel during 2025, with further strategic purchasing anticipated through 2026. China has a long-established policy of accumulating critical mineral reserves during periods of depressed pricing. Nickel's classification as a critical mineral by most major economies makes it a natural candidate for this type of reserve-building activity.

The 2026 Import Acceleration

The trend has intensified in 2026. Refined nickel imports into China surged 56% year-on-year during the January to April period, reaching 94,000 metric tons, while exports over the same window collapsed to just 9,400 metric tons. The net effect is a sharp domestic inventory build, which explains why ShFE stocks are climbing while LME stocks begin to plateau.

Strategic stockpiling absorbs spot supply without translating into productive consumption. This means government reserve-building can mask the true state of industrial demand, making it significantly harder for market participants to read the underlying supply-demand balance accurately.

This distinction between strategic absorption and genuine demand is critical for investors attempting to time a nickel price recovery. When government buying eventually slows or ceases, the inventory that was absorbed will not have generated downstream consumption, meaning the market will face the same fundamental imbalance when strategic buying normalises. In addition, the broader battery metals investment landscape adds further complexity to how investors should interpret these demand signals.

How Are Western Supply Disruptions Affecting the Overhang Equation?

Two Production Hits That Haven't Been Enough

The Western nickel supply chain has absorbed two significant and largely unexpected production disruptions in 2026, neither of which has been sufficient to meaningfully offset the structural surplus generated by Indonesian and Chinese-integrated capacity.

Ambatovy, Madagascar: The Ambatovy nickel operation was suspended in February 2026 following cyclone damage to critical infrastructure. The operation produced approximately 28,000 metric tons of finished nickel products in 2024 and is transitioning under new ownership led by a consortium with significant commodity trading experience. A return to production was anticipated by end of June 2026, though operational readiness timelines carry inherent uncertainty.

Sherritt International, Fort Saskatchewan: Sherritt International suspended direct participation in its Cuban mining joint venture following an escalation of US sanctions targeting Cuba. The Fort Saskatchewan refinery in Alberta depends on Cuban ore feed, and the company warned that its raw materials inventory was expected to last only to mid-June 2026. Sherritt had previously guided for 26,000 to 28,000 metric tons of finished nickel production in 2026, an outlook now carrying material uncertainty. The company has signed a term sheet to sell a majority stake in its Canadian nickel business to Gillon Capital, signalling a potential ownership restructure.

Combined, these disruptions put approximately 54,000 to 56,000 metric tons of annualised Western production at risk. In isolation, this is a meaningful volume. In the context of a global market carrying a 468,600 metric ton exchange inventory overhang, it is insufficient to trigger systemic rebalancing.

Why Western Disruptions Are Structurally Insufficient

The geometry of the global nickel market has changed fundamentally over the past decade. Indonesia and Chinese-integrated smelter networks now account for a dominant share of global refined output. Western producers, even collectively, no longer have the scale to swing the market through production interruptions alone.

What Western disruptions can do is slow the rate of LME inventory accumulation at the margin. Warrant cancellations and load-out rates at LME warehouses have picked up in recent weeks, suggesting some tightening of the physical market in the West. However, this represents localised logistics activity rather than evidence of a structural demand recovery.

The next major ASX story will hit our subscribers first

What Does the LME vs. ShFE Price Divergence Signal?

An Arbitrage Window That Isn't Closing

When Shanghai nickel prices trade at a persistent discount to London benchmarks, classical arbitrage theory predicts that Chinese producers will increase exports to LME warehouses to capture the price differential. This incentive currently exists. Yet export flows from China have collapsed, falling to just 9,400 metric tons in the first four months of 2026.

| Metric | LME Nickel | ShFE Nickel |

|---|---|---|

| Inventory trend (2026 YTD) | Plateauing after peak | Accelerating upward |

| Price performance (relative) | Outperforming | Underperforming |

| Export incentive signal | Arbitrage window open | Exports not materialising |

| Physical draw signals | Warrant cancellations rising | Inventory still building |

The failure of the arbitrage to close points to forces overriding commercial incentives. Government-directed stockpiling may be absorbing metal that would otherwise move to export channels. Domestic demand from Chinese stainless steel mills and battery precursor producers, while not robust, may be absorbing more spot supply than headline import figures suggest. Logistical and regulatory friction in moving refined nickel across jurisdictions may also be contributing.

For market observers, the persistence of this divergence is itself a signal. When price differentials between major exchanges fail to close through normal arbitrage mechanisms, it typically indicates that the market is operating under conditions that are not fully captured by standard supply-demand models. Consequently, nickel price momentum remains difficult to sustain in this environment, as structural forces continue to override conventional pricing signals.

How Long Could Nickel Market Rebalancing Take?

Scenario Pathways for Investors

The duration of the current nickel stock overhang will depend on the interaction of several variables, none of which are operating in isolation.

Scenario A: Accelerated Rebalancing (12 to 18 Months)

- Indonesian government mining quota restrictions tighten meaningfully and ahead of schedule

- Sulfur supply constraints curtail NPI and matte output at a scale that reaches refined metal markets within 12 months

- Western supply disruptions persist beyond initial estimates

- Chinese government strategic buying slows, reducing artificial demand support

- Outcome: Exchange inventories begin declining at 15,000 to 20,000 metric tons per month; price recovery gains momentum

Scenario B: Prolonged Overhang (24 to 36 Months)

- Indonesian output declines are modest and the transmission lag to refined markets is extended

- Chinese imports remain elevated while domestic inventory continues to build

- Western supply disruptions resolve faster than expected

- Strategic stockpiling continues to mask true industrial demand weakness

- Outcome: Exchange inventories remain above 300,000 metric tons; any price recovery is shallow and vulnerable to reversal

Most market analysts view Scenario B as the more probable near-term path. The six-week global consumption equivalent currently warehoused across exchanges means that even a meaningful demand acceleration would require a concurrent and sustained supply reduction to normalise inventory levels within a reasonable timeframe. Furthermore, the impact of tariff wars on global nickel markets adds an additional layer of uncertainty to both rebalancing scenarios.

What Does the Nickel Overhang Mean for Miners and Battery Producers?

Divergent Impacts Across the Supply Chain

The consequences of a prolonged nickel stock overhang are not uniform across market participants. The distributional effects vary significantly depending on cost structure, product form, and geographic exposure.

| Participant Type | Near-Term Impact | Long-Term Risk |

|---|---|---|

| Indonesian NPI producers | Low (low-cost base) | Regulatory and quota risk |

| Western Class I refiners | High (margin compression) | Closure and consolidation risk |

| Chinese integrated smelters | Moderate | Overcapacity self-correction |

| Battery material producers | Mixed (lower input costs) | Supply security risk |

| Stainless steel mills | Positive (lower feedstock costs) | Demand-driven |

For Western Class I producers, the combination of low spot prices and wide intermediate product discounts creates a structurally challenging operating environment. Junior and mid-tier miners with nickel exposure face heightened financing risk as equity markets discount recovery timelines further into the future. Major diversified miners with nickel divisions, such as BHP and Rio Tinto, can absorb margin pressure more readily, but nickel remains under strategic review at several large producers.

The battery supply chain faces a more nuanced picture. MHP and nickel sulfate producers contend with ongoing pricing pressure as the overhang suppresses feedstock premiums. EV battery manufacturers benefit from lower input costs in the near term. However, the long-term risk is more concerning: if sustained low prices force Western nickel capacity into permanent closure, the supply security of battery-grade material becomes structurally compromised, concentrating supply chain dependency in Indonesian and Chinese-integrated networks. For those evaluating ASX nickel stock value, these structural risks are increasingly being priced into equity valuations across the sector.

FAQ: Understanding the Nickel Stock Overhang

What is a nickel stock overhang in simple terms?

A nickel stock overhang describes a situation where the volume of refined nickel held in exchange warehouses and broader supply chains significantly exceeds what the market can absorb in the near term. This excess supply acts as a ceiling on prices because traders know physical metal is readily available, reducing their willingness to pay a premium for spot delivery.

How does exchange inventory affect nickel prices?

Elevated LME or ShFE warehouse stocks signal to the market that physical supply is abundant. This reduces urgency to bid for spot metal, depressing cash prices and weighing on forward curves. Conversely, a sustained decline in exchange inventory signals tightening supply and typically supports price appreciation over time.

Why is the nickel overhang concentrating in China right now?

China's domestic smelter capacity, built on Indonesian raw material inputs, continues to produce refined nickel at scale. Simultaneously, import volumes have remained high, partly driven by strategic government stockpiling. The combination of domestic production and elevated imports is outpacing Chinese industrial consumption, causing inventory to accumulate at ShFE warehouses at an accelerating rate.

Could Western supply disruptions resolve the overhang quickly?

This is unlikely in isolation. While the Ambatovy suspension and Sherritt's feed supply crisis remove a meaningful volume of Western production from the market, the global surplus is primarily driven by Indonesian and Chinese-integrated capacity, which remains largely intact. Western disruptions may slow LME inventory accumulation at the margin but are insufficient to trigger systemic rebalancing on their own.

What would need to happen for nickel prices to recover strongly?

A durable recovery would likely require a combination of factors: a measurable decline in Indonesian output flowing through to refined metal markets, a slowdown in Chinese strategic stockpiling, a reduction in ShFE inventory, and a recovery in global stainless steel and battery demand sufficient to absorb the existing surplus. Most analysts view this as a multi-year process rather than a near-term event.

Key Takeaways for Market Participants

- 468,600 metric tons of combined exchange inventory represents the largest nickel stock overhang since 2015, equivalent to approximately six weeks of global consumption

- The surplus is migrating eastward, with ShFE stocks nearly doubling in 2026 as LME inventories plateau

- China's 56% year-on-year import surge in January to April 2026, combined with strategic stockpiling dynamics, is masking the true state of industrial demand

- Western production disruptions representing roughly 54,000 to 56,000 metric tons of annualised output are insufficient to offset the structural surplus on their own

- The failure of the LME-ShFE arbitrage to close through normal commercial mechanisms points to government-directed activity overriding market incentives

- Market rebalancing is expected to be a slow, multi-year process, with refined metal markets lagging upstream output adjustments by a significant transmission delay

- The overhang creates asymmetric risk for Western producers and battery supply chain participants, while providing a near-term cost benefit for stainless steel consumers

This article is intended for informational purposes only and does not constitute financial advice. Commodity markets involve significant risk, and all projections and scenario analyses discussed represent analytical frameworks rather than guaranteed outcomes. Readers should conduct their own due diligence before making investment decisions.

Want to Track the Next Major ASX Mineral Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, cutting through complex commodity data to surface actionable opportunities the moment they are announced — explore historic discoveries and their returns to understand what early positioning can mean, then begin your 14-day free trial at Discovery Alert to gain a market-leading edge.