June 20, 2026

When Geopolitics Rewrites the Energy Map

Few forces reshape global energy investment patterns as decisively as the sudden disruption of a major supply corridor. History shows that when critical chokepoints come under pressure, capital flows rapidly toward stable, pipeline-connected alternatives. That dynamic is now playing out in real time across North African energy markets, and Algeria sits directly at its centre.

The near-closure of the Strait of Hormuz to most tanker traffic, a consequence of the ongoing Iran war, has placed enormous pressure on the roughly one-fifth of global oil and gas supplies that normally transit this critical waterway. For European energy importers already managing post-pandemic supply volatility, this disruption has fundamentally altered procurement priorities and accelerated the search for geographically stable, infrastructure-ready alternatives. Algeria, with its direct pipeline connections to both Italy and Spain, has emerged as one of the clearest beneficiaries of this structural shift.

Understanding the Algeria oil and gas bid round across 7 fields requires viewing it not as a routine tender event, but as the opening move in a longer strategic sequence designed to capitalise on both geopolitical timing and genuine geological opportunity.

When big ASX news breaks, our subscribers know first

Algeria's Strategic Position in a Disrupted Energy World

North Africa Fills the Gap Left by Middle East Uncertainty

Europe sourced roughly 10 percent of its gas imports from North Africa in the most recent annual period, and Algeria's role within that share is disproportionately significant given its dual pipeline connectivity to Italy and Spain. By mid-2025, Algeria had established itself as the fourth-largest LNG supplier to the European Union, a ranking that reflects both infrastructure investment and supply reliability over time. The LNG supply outlook for North Africa has consequently attracted significant institutional attention from European buyers.

Pipeline-delivered gas carries a different risk profile than LNG. It does not depend on floating storage, regasification terminals, or the availability of liquefaction capacity at the point of origin. When Middle East LNG exporters face operational disruptions, pipeline-connected suppliers gain a structural reliability premium that goes beyond simple price competition. Algeria's geographic positioning means that European buyers currently navigating the consequences of Hormuz disruptions have an immediate, operational alternative available.

ALNAFT president Samir Bekhti has noted that the prevailing geopolitical situation has directly stimulated investment demand in Algeria's hydrocarbons sector, citing the country's stable location and proximity to European energy consumers as key factors driving international interest. This is not merely a marketing position. It reflects a genuine supply security calculus that European energy ministries are applying with increasing urgency. Furthermore, European gas prices have added another layer of complexity to procurement decisions across the continent.

Why Algeria's OPEC Membership Adds a Layer of Strategic Complexity

Algeria's participation in OPEC introduces a dimension that is sometimes overlooked in purely commercial analyses of its bid round. The broader OPEC market influence on production quota dynamics means that exploration investment today does not automatically translate into immediate production increases. Any capacity expansion Algeria achieves through new exploration awards must ultimately be managed within the broader OPEC framework.

This creates an interesting strategic tension. Algeria is aggressively attracting exploration capital while operating within a collective production management structure. Foreign operators entering the country should factor in that discovered resources may face a longer pathway to full production ramp-up than purely commercial geology would suggest. The 2030 tender pipeline addresses this by staging capacity development over a multi-year horizon, which is consistent with OPEC quota management timelines.

The Algeria Bid 2026: Structural Details Every Investor Needs to Understand

Governance, Authority, and Timeline

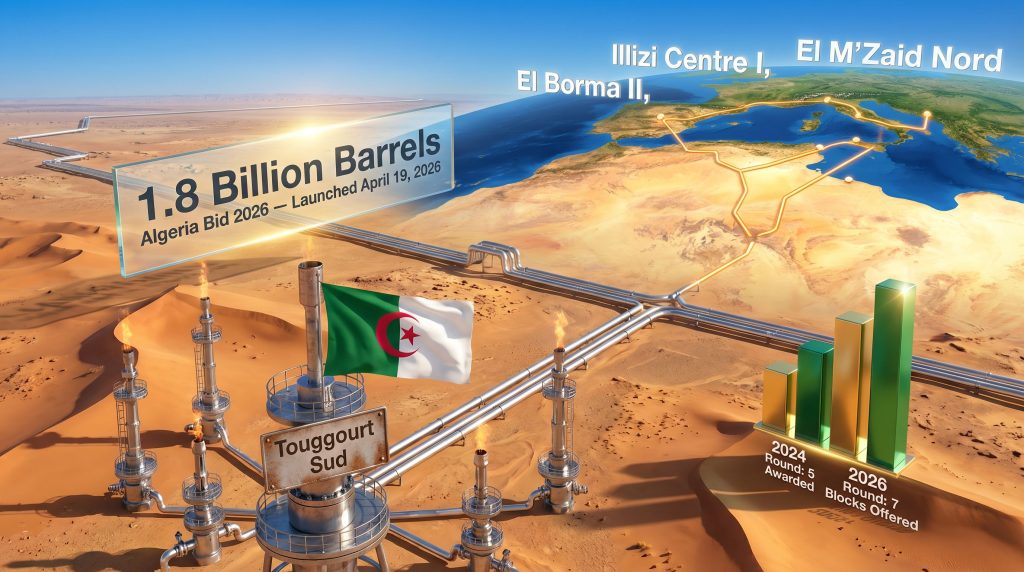

The Algeria Bid 2026 was formally launched on April 19, 2026, by ALNAFT, which operates under the authority of Algeria's Ministry of Hydrocarbons and Mines. ALNAFT functions as the technical and regulatory body responsible for evaluating exploration acreage and managing the bid process, while the Ministry sets the broader policy framework within which contracts are structured.

Algerian Minister of Hydrocarbons and Mines Mohamed Arkab has articulated the national rationale clearly: attracting foreign investment, facilitating technology transfer, and expanding exploration and production activity in response to rapidly shifting geopolitical and energy market conditions. These are not aspirational statements. They reflect policy commitments embedded in the 2030 hydrocarbon strategy that underpins this and future tender rounds.

The critical commercial timeline is structured as follows:

| Milestone | Date |

|---|---|

| Bid Round Launch | April 19, 2026 |

| Bid Submission Deadline | November 26, 2026 |

| Contract Award and Signing Target | January 31, 2027 |

The bid-to-contract window of under ten months is deliberately compact. This reflects institutional urgency shaped by the recognition that geopolitical windows of opportunity are not permanent. If Middle East supply routes stabilise, the investment premium currently attached to Algerian acreage will compress.

Contract Structures Available to Foreign Bidders

Two distinct contract frameworks govern the seven blocks, and the choice of structure materially affects how foreign operators should model their economic exposure:

| Contract Type | Number of Blocks | Key Feature |

|---|---|---|

| Production-Sharing Agreement | 6 blocks | Foreign partner shares output with Sonatrach under negotiated split |

| Participation Contract | 1 block | Sonatrach holds a minimum 51% equity stake |

The participation contract deserves particular attention from legal and financial due diligence teams. A minimum 51% Sonatrach equity requirement fundamentally constrains foreign operator control over development decisions, cost recovery mechanisms, and exit optionality. Operators familiar with production-sharing environments in other MENA jurisdictions will need to assess how Algeria's specific fiscal and regulatory terms compare before committing capital.

Disclosure: This article contains analysis of exploration-stage resource estimates and investment structures. None of the information contained herein constitutes financial advice. Investors should conduct independent due diligence and seek professional guidance before making any investment decisions.

Mapping the Seven Blocks: Basin Geology and Geographic Context

Southern Algeria's Proven Hydrocarbon Provinces

The seven blocks are distributed across Algeria's southern hydrocarbon basins, each with its own geological character and development history. What unites them is their position adjacent to mature, producing petroleum systems, a factor that materially reduces the binary exploration risk that defines frontier acreage. According to Reuters reporting on the bid round launch, Algeria's decision to open these blocks signals a decisive push to grow its international upstream partnerships.

| Block Name | Administrative Region | Primary Basin |

|---|---|---|

| El Borma II | Ouargla | Berkine / Oued Mya |

| El M'Zaid Nord | Ouargla | Berkine |

| Illizi Centre I | Illizi | Illizi |

| Est Bordj Omar Driss I | Illizi | Illizi |

| El Hadjira III | Touggourt | Oued Mya |

| Touggourt Sud | Touggourt | Oued Mya |

| El Benoud Est | El Bayadh | Benoud / Amguid |

Why Proximity to Proven Production Systems Matters

There is a geological principle that seasoned exploration geologists apply consistently: a new block adjacent to a producing field benefits from what is called a proven petroleum system. This means the source rock has demonstrably generated hydrocarbons, migration pathways exist, and trap structures have been validated by nearby production. The remaining question is trap-specific, not system-level, and this significantly narrows the risk profile.

The Berkine Basin, which hosts El Borma II and El M'Zaid Nord, is one of Algeria's most prolific conventional oil provinces, with decades of multi-operator production history. The Illizi Basin similarly carries extensive subsurface datasets accumulated from years of Sonatrach and partner operations. Incoming bidders in these basins are not working with blank geological maps.

They have access to regional seismic, well data, and production history from adjacent fields, tools that materially reduce subsurface uncertainty and allow more confident resource estimates and economic modelling. The Oued Mya Basin, hosting El Hadjira III and Touggourt Sud, has a long production track record and benefits from relatively well-understood stratigraphy. El Benoud Est in the Benoud/Amguid Basin represents the least mature geological setting among the seven, which introduces somewhat higher exploration uncertainty, but also potentially higher upside if structural traps in that basin prove productive.

Resource Scale: What 1.8 Billion Barrels Actually Means

Combined Resource Potential Across All Seven Fields

ALNAFT president Samir Bekhti confirmed that the combined estimated resources across the seven blocks exceed 1.8 billion barrels of oil and 8.63 billion cubic metres of natural gas. These figures place the Algeria oil and gas bid round across 7 fields among the more consequential exploration tenders to emerge from the MENA region in recent years. In addition, the geopolitical risk landscape across the broader region has made stable, proven jurisdictions like Algeria increasingly attractive to international capital.

Critical Distinction: These figures represent exploration-stage resource estimates, not certified reserves. Under standard petroleum resource classification systems, such as the SPE-PRMS framework, resources at this stage carry geological risking that must be applied before arriving at economically recoverable volumes. Investors should apply probability-weighted adjustments, typically differentiated by probability of discovery and probability of development, before using these figures in financial models.

Standout Resource Highlights

| Block | Estimated Oil Resource | Strategic Note |

|---|---|---|

| Touggourt Sud | 576+ million barrels | Largest single oil resource in the round |

| El M'Zaid Nord | Approximately 100 million barrels | Proximity to active Berkine production infrastructure |

| Remaining 5 Blocks | Combined hundreds of millions of barrels | Significant gas co-production potential across the portfolio |

Touggourt Sud's 576-plus million barrel oil resource estimate is particularly notable. For context, oil discoveries of this scale are genuinely rare at the global level. Even after applying standard exploration risking factors, a probability-weighted resource in this range would represent a material discovery by any international benchmark. The Oued Mya Basin setting provides geological comfort that the petroleum system required to charge such a structure is demonstrably active in the region.

The 8.63 billion cubic metres of gas resource across the portfolio adds a dimension that is especially valuable given current European gas pricing dynamics. Gas co-production from oil-focused blocks can meaningfully improve overall field economics, and Algeria's existing LNG infrastructure and pipeline export routes provide multiple monetisation pathways for any discovered gas volumes.

Algeria's 2030 Hydrocarbon Vision: The Bid Round in Strategic Context

A Multi-Year Tender Sequence, Not a One-Off Event

One of the most strategically important facts about the Algeria Bid 2026 that receives insufficient attention in commercial coverage is that it is explicitly positioned as one component of a sequential tender series running through 2030. This distinction matters enormously for how international operators should evaluate their entry strategy.

A single bid round presents a take-it-or-leave-it decision. A multi-round pipeline creates optionality. Operators who do not win blocks in this round can position themselves for subsequent tenders, potentially with better geological data derived from early discoveries made by winning bidders. Conversely, first-movers who secure acreage in high-quality basins in this round gain a data and infrastructure advantage over later entrants.

Algeria's stated three-pillar strategy underpinning the 2030 programme encompasses:

- Expanding production capacity to grow Algeria's absolute output position

- Managing rising domestic energy consumption driven by a population of approximately 47 million people with subsidised energy costs

- Growing export volumes to European markets, particularly through existing pipeline infrastructure to Italy and Spain

The domestic demand dimension is often underappreciated. Algeria's generous domestic energy subsidy regime means that internal consumption growth directly competes with exportable surplus. As the population expands and industrial activity grows, the volume of hydrocarbons available for export is subject to compression pressure from below. This creates a structural imperative to continuously replace and expand production capacity, not simply to grow export revenues, but to maintain them.

The Fiscal Architecture Behind the Strategy

Algeria's hydrocarbon sector is not merely economically important. It is the foundational pillar of government revenue, financing subsidy programmes and public expenditure across a country of nearly 47 million people. This level of fiscal dependency creates a political economy dynamic where hydrocarbon sector development is a matter of national budget stability, not just energy sector performance.

This fiscal imperative provides an important signal to investors about regulatory risk. While Algeria has historically adjusted fiscal terms in response to oil price cycles, as many hydrocarbon-dependent states do, the structural dependency on foreign investment and technology transfer creates strong institutional incentives to maintain competitive terms that continue to attract international operators. Consequently, the oil price geopolitics shaping global markets today are reinforcing Algeria's resolve to accelerate upstream development.

The next major ASX story will hit our subscribers first

Investor Risk and Opportunity Framework

Factors Attracting International Capital

- Relative geopolitical stability: Algeria's position outside the active conflict zone affecting Gulf supply routes creates a meaningful risk premium advantage for energy investors currently reassessing MENA exposure

- Proven basin geology: Berkine and Illizi basin blocks carry significantly reduced subsurface uncertainty compared to frontier acreage, supported by extensive existing well and seismic data

- Infrastructure adjacency: Existing processing, pipeline, and export infrastructure in producing basin areas reduces the greenfield capital expenditure required to bring new discoveries to production

- Defined commercial timeline: A bid-to-contract schedule of under ten months provides planning certainty that many competing jurisdictions do not offer

- European demand pull: Long-term gas supply relationships with Italy and Spain provide revenue visibility that supports project financing discussions

Risk Factors Requiring Rigorous Due Diligence

- Sonatrach partnership dynamics: Both contract structures require partnership with Algeria's national oil company. The participation contract structure, with its minimum 51% Sonatrach equity requirement, places particular constraints on foreign operator decision-making authority

- Exploration-stage resource estimates: The 1.8 billion barrel gross resource figure must be risk-weighted before it can support investment cases. Probability-of-discovery and probability-of-development factors will reduce net investable volumes materially

- Domestic consumption growth: Rising internal demand from a growing, subsidy-supported population creates medium-term export surplus compression risk that operators modelling long-duration production profiles should incorporate

- Fiscal term evolution: Algeria, like other hydrocarbon-dependent states, has historically revised contract terms as price cycles shift. Full legal review of specific contract terms is essential before commitment

- OPEC quota constraints: Production growth from new discoveries operates within OPEC collective management frameworks, potentially extending the timeline from discovery to full production ramp-up

Investment Perspective: The Algeria Bid 2026 offers a relatively conventional-risk entry point for international operators seeking exposure to proven basin geology with European export optionality. However, the Sonatrach partnership requirement and exploration-stage resource classifications demand rigorous modelling before capital allocation decisions can be responsibly made. This analysis is educational in nature and does not constitute investment advice.

Algeria's Position Within the Broader MENA Energy Investment Landscape

North Africa as a Structural Beneficiary of Gulf Supply Disruption

The competitive dynamics of MENA energy investment are being visibly reshaped by the Strait of Hormuz situation. Middle East producers that historically commanded investment capital based on proven reservoir size and low production costs now carry elevated geopolitical risk premiums that are altering the calculus for risk-adjusted returns.

Algeria, Libya, and Egypt are all competing for a share of the European-focused energy investment capital that is being repositioned away from Gulf exposure. Among these three, Algeria's pipeline infrastructure to both Italy and Spain provides a qualitative infrastructure advantage that neither Libya nor Egypt can fully replicate at current capacity levels. For further technical detail on the seven blocks and Algeria's strategic investment case, ALNAFT's official bid round documentation provides a comprehensive overview of terms and geological data.

| Competitive Factor | Algeria | Comparable MENA Producers |

|---|---|---|

| Proximity to European markets | High, pipeline-connected | Low to Medium |

| Geopolitical risk profile | Low to Medium | High in Gulf states |

| Exploration upside | Significant in underdeveloped basins | Moderate in mature fields |

| Infrastructure readiness | Medium to High | Variable |

| LNG export capacity | Growing | Established in Qatar and UAE |

A Note on Speculative Scenarios Worth Monitoring

Several analytical threads in the current environment warrant careful watching without overstating their certainty.

If the Strait of Hormuz situation extends beyond twelve to eighteen months, European energy buyers may shift from spot-market solutions to long-term contract frameworks anchored on North African supply, fundamentally changing the revenue visibility available to operators in Algeria's bid round blocks. This is speculative but operationally plausible given current trajectory.

Separately, Algeria's parallel engagement with major international operators across both offshore and shale gas domains, if these discussions progress to formal agreements, could signal a step-change in the country's exploration ambition that goes well beyond the seven-block conventional onshore round currently on offer.

Frequently Asked Questions: Algeria Oil and Gas Bid Round Across 7 Fields

What is the Algeria Bid 2026?

The Algeria Bid 2026 is an international oil and gas exploration tender launched by ALNAFT on April 19, 2026, offering seven exploration blocks across Algeria's proven southern hydrocarbon basins. It forms part of a sequential tender strategy running through 2030, aimed at attracting foreign investment, expanding production capacity, and growing export volumes to European markets.

How many blocks are available and where are they located?

Seven exploration blocks are on offer, spanning the Berkine, Illizi, Oued Mya, Benoud, and Amguid basins in southern Algeria across the administrative regions of Ouargla, Illizi, Touggourt, and El Bayadh.

What are the combined resource estimates?

ALNAFT has confirmed that the seven blocks collectively hold estimated resources exceeding 1.8 billion barrels of oil and 8.63 billion cubic metres of natural gas. These are exploration-stage resource estimates, not certified reserves, and should be risk-weighted for investment purposes.

What contract structures are available?

Six of the seven blocks are structured as production-sharing agreements with Sonatrach. One block is offered under a participation contract structure requiring Sonatrach to hold a minimum 51% equity interest.

When must bids be submitted?

The bid submission deadline is November 26, 2026, with contract awards and signings targeted for completion by January 31, 2027.

Why does Algeria's bid round matter for European energy security?

Algeria is pipeline-connected to both Italy and Spain and was the EU's fourth-largest LNG supplier by mid-2025. With Middle East supply routes under pressure from the Iran war and associated Hormuz disruptions, Algeria's stable supply corridor has become a structurally important component of European energy security planning.

Is this part of a larger strategy?

The Algeria Bid 2026 is explicitly one component of a sequential series of exploration tenders planned through 2030, making it the opening phase of a multi-year hydrocarbon acceleration programme rather than a standalone tender event.

Key Takeaways

- The Algeria oil and gas bid round across 7 fields offers access to a combined resource base exceeding 1.8 billion barrels of oil and 8.63 billion cubic metres of natural gas across proven southern Algerian basins

- Geopolitical timing is central to the bid round's commercial logic, with Hormuz disruptions elevating the strategic value of Algeria's stable, pipeline-connected supply corridor

- Touggourt Sud alone carries an estimated resource of more than 576 million barrels, making it one of the most significant individual exploration opportunities in the round

- The bid-to-contract timeline of under ten months reflects institutional urgency and provides planning certainty for international operators

- Algeria's 2030 tender pipeline positions this round as the first step in a structured, multi-year exploration acceleration programme

- Sonatrach partnership requirements and the exploration-stage nature of resource estimates are the two most important risk factors requiring detailed commercial and legal analysis before investment decisions are made

This article is intended for informational and educational purposes only. It does not constitute financial, legal, or investment advice. Resource estimates referenced are exploration-stage figures sourced from ALNAFT and reported by Arab News (April 20, 2026) and carry inherent geological and commercial uncertainty. Readers should conduct independent research and seek qualified professional advice before making any investment decisions.

Want to Stay Ahead of the Next Major Resource Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex resource data into actionable investment insights — explore the historic returns major discoveries have generated and begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.