June 25, 2026

The Forgotten Bottleneck: Why Alumina Is the Real Vulnerability in America's Metal Economy

Most conversations about US aluminium independence focus on smelting capacity. How many furnaces are running, how much primary metal is being cast, and whether domestic output can meet the demands of aerospace manufacturers, defence contractors, and electric vehicle platforms. But this framing misses the deeper structural problem entirely. Before a single ingot of aluminium can be produced in the United States, the country must first secure a supply of smelter-grade alumina, the refined white powder that feeds every electrolytic reduction cell in every primary smelting facility on earth.

This is the bottleneck that almost never appears in policy headlines, and it is precisely why the evolving Brimstone and Century Aluminum US aluminium supply chain strategy is drawing attention from industry analysts, materials security planners, and industrial investors alike.

Understanding why this matters requires a brief detour into how aluminium is actually made.

When big ASX news breaks, our subscribers know first

How the Aluminium Supply Chain Actually Works

Primary aluminium production operates across three distinct industrial stages, and each one introduces its own geographic and geopolitical exposure.

- Bauxite mining extracts the raw ore, predominantly from tropical deposits in Guinea, Australia, Brazil, and Indonesia.

- Alumina refining converts bauxite into smelter-grade aluminium oxide (Al₂O₃) using the Bayer process, a chemically intensive operation requiring caustic soda, high-pressure digesters, and significant thermal energy.

- Primary smelting uses electrolytic reduction (the Hall-Heroult process) to convert alumina into metallic aluminium, consuming enormous quantities of electricity in the process.

The United States has historically participated meaningfully only at stage three. There are no economically viable bauxite deposits within US borders, meaning that every tonne of domestically smelted aluminium has always depended on imported raw materials at stages one and two. Furthermore, with China currently controlling approximately 60% of global alumina and aluminium output, according to Mining Technology, and the US producing less than one-sixth of the aluminium it consumes domestically, the exposure is not theoretical. It is structural, entrenched, and growing more consequential as geopolitical friction intensifies.

Smelter-grade alumina typically must meet tight chemical specifications, including aluminium oxide purity levels generally above 98.5%, with controlled levels of silica, iron oxide, and sodium content. These quality thresholds are non-negotiable for modern electrolytic reduction cells, meaning not just any refined material will serve as a functional feedstock.

What the Brimstone-Century Aluminum MOU Actually Represents

In June 2026, Brimstone and Century Aluminum formalised a memorandum of understanding with the stated objective of creating the first fully domestic mine-to-metal aluminium supply chain in US history. The structure of the agreement is straightforward in concept but extraordinary in ambition.

| Agreement Component | Detail |

|---|---|

| Partnership Type | Memorandum of Understanding (MOU) |

| Alumina Supplier | Brimstone |

| Alumina Buyer | Century Aluminum |

| Target Product | Smelter-grade alumina |

| Supply Chain Goal | First fully domestic US mine-to-metal aluminium chain |

| Announced | June 2026 |

Brimstone will supply smelter-grade alumina from its planned US-based production facility, with the material destined for Century's existing and expanding smelting operations. What distinguishes this from conventional alumina supply contracts is the feedstock itself. Brimstone does not intend to process imported bauxite. Instead, the company is developing a production pathway built entirely around calcium silicate rocks, a class of geological material that exists in abundance across the continental United States.

This distinction is not a minor technical footnote. It is the entire premise of the supply chain independence claim.

Brimstone's Rock Refinery: Rethinking Where Alumina Comes From

The Bayer Process and Its Geographic Constraints

The conventional Bayer process has dominated alumina production for over a century. Developed in 1887 by Austrian chemist Karl Bayer, the method dissolves aluminium-bearing minerals from bauxite using hot sodium hydroxide solution under pressure, separates the resulting aluminate liquor from impurities, and then precipitates and calcines aluminium hydroxide into the final oxide product. The process works extremely well for bauxite, but bauxite is geologically concentrated in tropical and subtropical laterite environments. The continental US simply does not have it in commercially exploitable form. In addition, global bauxite production remains heavily concentrated in a handful of countries, further amplifying America's feedstock vulnerability.

Calcium Silicate Rocks as an Alternative Feedstock

Brimstone's approach inverts this geographic constraint. Rather than processing bauxite, the company extracts alumina from calcium silicate rocks, a lithologically diverse category that includes materials like anorthosite, nepheline syenite, and related igneous or metamorphic rock types. These formations are geologically widespread across North America, and critically, they do not require tropical weathering conditions to form.

The feedstock for Brimstone's planned operations comes from the Dolese Bros. Co. Roosevelt Quarry in Oklahoma, an existing quarry operation, which removes the need to establish greenfield mining infrastructure from scratch.

The Multi-Product Advantage: Alumina, Cement, and SCM From a Single Rock

Perhaps the most commercially significant aspect of Brimstone's process is what it produces alongside alumina. The same calcium silicate feedstock that yields smelter-grade aluminium oxide simultaneously generates portland cement clinker and supplementary cementitious materials (SCM). This multi-product output fundamentally changes the unit economics of the operation.

Unlike the Bayer process, which is purpose-built for alumina extraction alone, Brimstone's rock refinery model distributes capital and operating costs across three commercially valuable product streams. This has the potential to make domestic alumina production cost-competitive with imported material even before any supply chain risk premium is applied.

How does this compare directly to the established method?

| Process Variable | Bayer Process (Conventional) | Brimstone Rock Refinery |

|---|---|---|

| Primary Feedstock | Tropical bauxite (imported) | Calcium silicate rock (US-sourced) |

| Energy Profile | High energy intensity | Designed for lower carbon footprint |

| Co-Products | Alumina only | Alumina + cement + SCM |

| Feedstock Availability in US | None economically viable | Abundant domestically |

| Geopolitical Exposure | High (tropical supply regions) | Minimal |

Project Development Timeline: Demonstration to Industrial Scale

Brimstone's commercialisation pathway follows a staged approach, which is standard for novel process technologies seeking to demonstrate viability before committing to full industrial capital expenditure.

Key milestones as currently targeted:

- 2028: Commercial demonstration plant in Reno, Nevada, scheduled to become operational

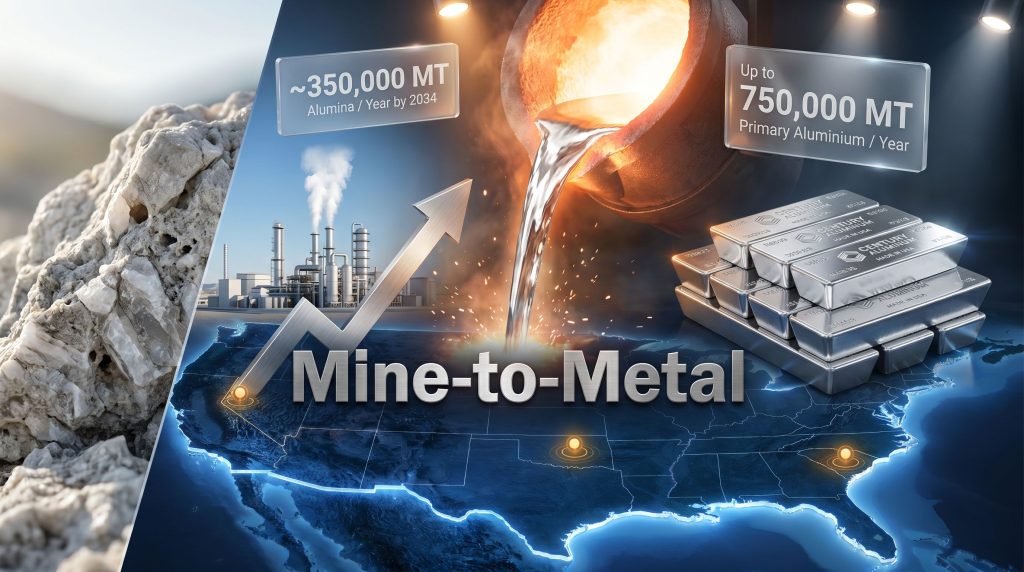

- 2034: Industrial-scale facility targeted for completion, with approximately 350,000 metric tonnes per annum of smelter-grade alumina capacity

To support this trajectory, Brimstone has received a US Department of Energy award of up to $189 million, with $8.7 million already finalised to advance site selection, engineering, and pre-commercial development work. This federal funding reflects broader policy interest in domestic critical materials supply chains, though it is worth noting that government funding awards do not guarantee commercial outcomes, and the technology remains in a demonstration phase with full industrial viability yet to be proven at scale.

The Reno demonstration plant serves a dual function: validating process chemistry at commercial throughput rates and generating the performance data needed to underwrite financing for the much larger industrial facility. For a process that diverges significantly from established Bayer chemistry, this verification step is not optional. It is the critical gating event for everything that follows.

Century Aluminum's Expanding Domestic Smelting Footprint

The demand side of the Brimstone and Century Aluminum US aluminium supply chain equation is equally significant. Century Aluminum is one of the largest primary aluminium producers in the United States, and its recent investment decisions indicate a deliberate expansion of domestic smelting capacity at a scale not seen in this country for decades. Indeed, leading aluminium mining companies are watching this expansion closely as it signals a broader shift in the domestic production landscape.

| Century Aluminum Expansion Initiative | Location | Capacity / Investment |

|---|---|---|

| Mt. Holly Facility Restart | South Carolina | $50 million investment |

| New Primary Smelter (JV with Emirates Global Aluminium) | Inola, Oklahoma | Up to 750,000 mt/year (or 500,000 mt high-purity) |

| Alumina Supply Agreement (Brimstone MOU) | US domestic | ~350,000 mt/year alumina feedstock |

The restart of the Mt. Holly facility in South Carolina, representing a $50 million recommitment to a previously idle asset, signals that Century is not simply talking about domestic capacity, it is funding it. More significantly, the joint venture with Emirates Global Aluminium (EGA) to construct a new primary production plant in Inola, Oklahoma, would, if fully executed, represent the first new US primary aluminium smelter built since 1980. With a potential capacity of up to 750,000 metric tonnes per year of primary aluminium, or 500,000 tonnes of high-purity product depending on configuration, the Oklahoma facility would fundamentally alter the scale of US smelting capability.

It is this Oklahoma smelter ambition that makes the Brimstone MOU so strategically coherent. A 750,000 tonne smelter requires a substantial and reliable alumina supply. Brimstone's targeted 350,000 tonne annual output would cover a meaningful portion of that demand from a fully domestic source. This mirrors a similar strategic logic seen in the Alcoa joint venture model, where securing reliable domestic inputs has become a central feature of modern aluminium investment planning.

The next major ASX story will hit our subscribers first

The Numbers Behind US Aluminium Import Dependency

To appreciate why the Brimstone and Century Aluminum US aluminium supply chain initiative is attracting so much attention, it helps to frame the scale of the gap it is attempting to close. The policy context has, furthermore, been sharpened considerably by recent US aluminium tariffs, which have intensified pressure on domestic producers to reduce their reliance on foreign material inputs.

By the Numbers:

- China controls approximately 60% of global alumina and aluminium production

- The US produces less than one-sixth of the aluminium it consumes domestically

- Brimstone's industrial plant could deliver ~350,000 metric tonnes of domestic alumina annually from 2034

- The new Century-EGA Oklahoma smelter could produce up to 750,000 metric tonnes of primary aluminium per year

For sectors like defence manufacturing, aerospace, and power transmission infrastructure, where supply chain provenance is increasingly a procurement and security requirement rather than a preference, the difference between imported and domestically sourced material is not merely a cost variable. It is a risk management variable.

Aluminium is used in fighter aircraft airframes, missile components, satellite structures, electrical transmission cables, and the battery enclosures of electric vehicles. Each of these applications represents a scenario where disruption of the upstream supply chain, whether through trade action, geopolitical instability, or logistics failure, creates consequences well beyond commodity price volatility.

Brimstone's Broader Industrial Ambitions

The commercial logic of Brimstone's model extends well beyond the aluminium sector. The company is actively in discussions with customers and partners across cement, steel, and other critical minerals markets. This diversification reflects an important characteristic of the rock refinery process: the same calcium silicate chemistry that yields alumina also produces materials that are directly relevant to the construction and steelmaking industries.

For investors and analysts evaluating this story, this multi-market positioning matters. If alumina demand growth is slower than projected, or if the demonstration plant requires additional development cycles, the cement and SCM revenue streams provide an alternative commercial pathway that does not depend on the aluminium market trajectory. This is an unusual characteristic for an alumina producer and one that reduces the binary risk profile typically associated with single-commodity process technology companies.

Additionally, the broader expansion of Brimstone's partner and customer discussions suggests the company is deliberately building a diversified industrial platform rather than a narrow aluminium input supplier. However, whether that ambition can be executed within the stated timelines remains to be demonstrated. The aluminium operations repowering underway at major facilities elsewhere offers a useful parallel for how large-scale industrial transformation in this sector unfolds in practice.

Scenario Projections: What Does Full Execution Look Like by 2034?

Any honest assessment of the Brimstone-Century partnership must acknowledge that a significant portion of the value proposition is forward-looking, and therefore subject to execution risk, capital market conditions, and technical uncertainties.

Three scenarios worth considering:

-

Full execution scenario: Brimstone's Reno demonstration plant validates the rock refinery process by 2028, the industrial-scale facility reaches its 350,000 tonne annual capacity by 2034, and the Century-EGA Oklahoma smelter comes online on schedule. In this scenario, the US achieves a genuinely sovereign primary aluminium production pathway for the first time in its industrial history.

-

Partial delivery scenario: The demonstration plant operates successfully but the industrial-scale facility faces financing delays or engineering challenges, pushing the 2034 target out by several years. Century's Mt. Holly and Oklahoma capacity still advances, but relies on international alumina sources during the gap period.

-

Geopolitical acceleration scenario: A significant disruption to alumina trade flows, whether through tariff escalation, export restrictions, or a logistics shock, accelerates the urgency of domestic alternatives and attracts additional capital and policy attention to projects like Brimstone's. This scenario could compress the timeline through prioritised investment rather than extend it.

Disclaimer: The scenarios above are speculative analytical frameworks and do not constitute investment advice or forecasts. The commercialisation of novel process technologies involves material technical, financial, and regulatory risks. Investors and stakeholders should conduct independent due diligence before drawing conclusions about likely outcomes.

Frequently Asked Questions: Brimstone and Century Aluminum US Aluminium Supply Chain

What did Brimstone and Century Aluminum agree to in their MOU?

The two companies signed a memorandum of understanding in June 2026, under which Brimstone will supply smelter-grade alumina from its planned US-based production facility to Century Aluminum for use in primary aluminium smelting.

What makes Brimstone's alumina production process different from conventional methods?

Rather than processing imported tropical bauxite using the Bayer process, Brimstone extracts alumina from calcium silicate rocks that are geologically abundant within the United States. The same process co-produces portland cement and supplementary cementitious materials.

When will Brimstone's alumina plant be operational?

The commercial demonstration plant in Reno, Nevada, is targeted for operational commencement in 2028. The full industrial-scale facility is targeted for completion by 2034.

How much alumina will Brimstone's industrial plant produce annually?

The industrial-scale facility is expected to have a production capacity of approximately 350,000 metric tonnes of smelter-grade alumina per year.

Why doesn't the US produce its own bauxite for aluminium smelting?

There are no economically viable bauxite deposits within the United States. Bauxite forms through deep tropical weathering processes that are absent in the continental US geological environment.

How much federal funding has Brimstone received from the US Department of Energy?

Brimstone has received a DOE award of up to $189 million, with $8.7 million already finalised to support site selection and early engineering work. The Reshorenow library has documented this milestone as a significant industrial breakthrough for US aluminium supply chain sovereignty.

What is the significance of the Oklahoma smelter joint venture with Emirates Global Aluminium?

The Century-EGA joint venture in Inola, Oklahoma, would, if completed, represent the first new US primary aluminium smelter constructed since 1980, with capacity of up to 750,000 metric tonnes of primary aluminium per year.

A Generational Opportunity With Generational Execution Risk

The Brimstone and Century Aluminum US aluminium supply chain initiative is, at its core, a bet on whether an entirely new process technology can reach industrial scale within a commercially and geopolitically relevant timeframe. The ambition is credible, the need is demonstrably real, and the commercial logic of the multi-product rock refinery model is genuinely novel.

What policymakers, procurement officers, and investors should watch between now and 2034 is not the announcements, but the execution metrics: demonstration plant throughput rates, alumina quality assurance data against smelter-grade specifications, capital commitment progress on the industrial facility, and Century's actual ramp-up trajectory at both Mt. Holly and Oklahoma.

The US has not built the full architecture of a sovereign aluminium supply chain in living memory. Consequently, whether the Brimstone-Century partnership represents the beginning of that construction, or a well-intentioned ambition that requires further development cycles, will be answered not in memoranda of understanding, but in metric tonnes of domestically produced, specification-grade alumina flowing to American smelting furnaces.

Want to Track the Next Major ASX Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, transforming complex mineral data into actionable insights across more than 30 commodities — giving subscribers an immediate edge on significant new discoveries. Explore historic examples of major mineral discoveries and their market returns, then start your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.