July 27, 2026

The Dual Regulatory Shock Rewriting Aluminium's Competitive Map

For most of the past century, aluminium producers competed on a relatively familiar set of variables: energy costs, bauxite access, smelting efficiency, and proximity to end markets. Trade policy existed as background noise, occasionally disruptive but rarely structural. That era is ending. The simultaneous arrival of carbon border pricing and an increasingly fragmented tariff landscape is fundamentally altering how aluminium is priced, sourced, and traded across the globe.

Businesses that continue to treat these as compliance footnotes are making a strategic miscalculation with long-term consequences. Understanding how aluminium CBAM and tariffs interact, where they diverge, and why each demands a separate strategic response is now foundational knowledge for anyone operating across the aluminium value chain.

When big ASX news breaks, our subscribers know first

What CBAM Actually Is, and Why Aluminium Is Particularly Exposed

The EU's Carbon Border Adjustment Mechanism is not a tariff. This distinction matters more than most industry participants currently appreciate. While a tariff is a customs duty applied to the commercial value of imported goods, CBAM is a carbon price applied to the embedded emissions of those goods. The economic effect can be equivalent, but the strategic response is entirely different.

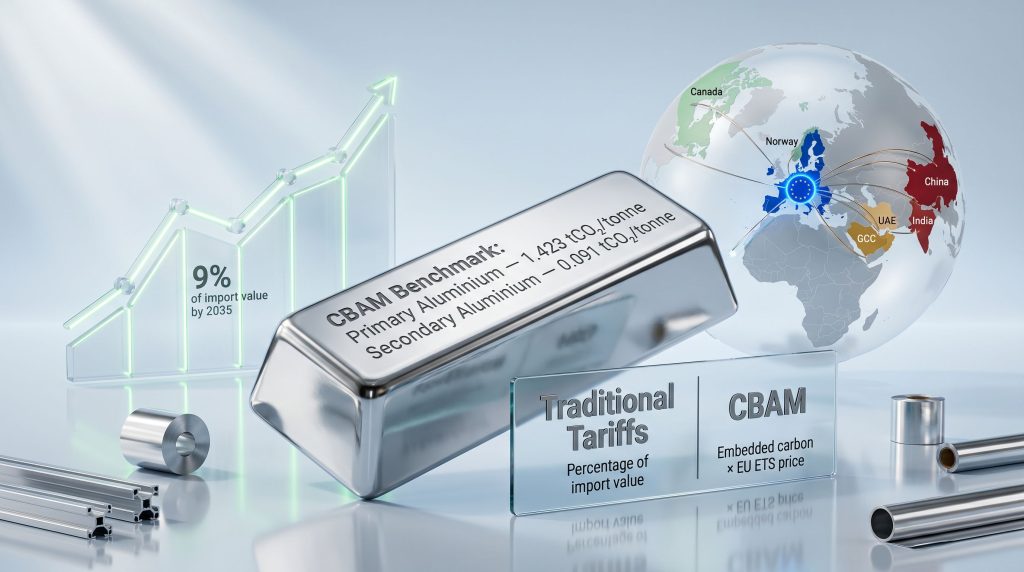

Aluminium sits within the first cohort of CBAM-covered sectors, alongside steel, cement, fertilisers, electricity, and hydrogen. The transitional reporting phase ran from October 2023 onward, but full financial liability commences in 2026, at which point importers must surrender CBAM certificates corresponding to the carbon price gap between the exporting country and the EU Emissions Trading System (ETS).

The Benchmark Numbers That Will Define Market Access

The EU has established product-specific carbon benchmarks that serve as the reference point for CBAM liability calculations. These figures carry significant commercial weight:

| Product Category | CBAM Benchmark (tCO₂ per tonne) |

|---|---|

| Primary Aluminium | 1.423 |

| Secondary (Recycled) Aluminium | 0.091 |

The gap between these two figures is not incremental — it is transformative. A 15-fold differential in carbon benchmark intensity between primary and secondary aluminium means the recycled metal segment enjoys a structural competitive advantage that will only grow as CBAM costs escalate toward their full magnitude.

Critically, these benchmarks are not static. As EU ETS carbon prices evolve and CBAM's free allocation phase-out progresses, the financial liability attached to each tonne of carbon above these benchmarks will increase. Producers and importers planning only for today's carbon price are underestimating their future exposure. Furthermore, the aluminium and alumina markets are already beginning to price in this longer-term trajectory.

How Country of Origin Shapes CBAM Liability

One of the less-discussed dimensions of CBAM is that default emissions values differ significantly by country of origin and production method. This creates an unequal competitive playing field that is reshaping sourcing decisions in real time.

| Region / Origin | Carbon Intensity Profile | CBAM Exposure Level | Tariff Risk Profile |

|---|---|---|---|

| China | High (coal-dominated grid) | Very High | Elevated |

| India | High (coal-dominated grid) | High | Moderate to High |

| UAE | Moderate to High | Moderate-High | Moderate |

| Russia | Variable (hydro + fossil mix) | Moderate | Very High |

| Canada | Low (hydro-dominated) | Low | Low to Moderate |

| Norway / Iceland | Very Low (renewable) | Very Low | Low (EEA alignment) |

| GCC (excl. UAE) | Moderate | Moderate | Moderate |

Countries relying on coal-dominated electricity grids for smelting operations face materially higher CBAM default values, while hydro-powered producers in Canada, Norway, and Iceland are positioned as structural beneficiaries of the emerging carbon pricing regime. The grid intensity of a producing nation is now, effectively, a trade competitiveness variable.

The Financial Scale of CBAM: Projections Through 2035

Quantifying CBAM's cost impact requires distinguishing between the near-term ramp-up phase and the longer-term trajectory. In the early years, free ETS allocations partially offset liability for EU domestic producers. As those allocations are phased out in parallel with CBAM's maturation, the cost curve steepens considerably.

Market analysis projects that CBAM costs for aluminium imports could average approximately 9% of import value by 2035, with the impact concentrated in high-carbon supply chains and specific product categories. This is not a marginal adjustment. At that magnitude, CBAM operates with economic force comparable to a significant tariff shock, despite being a fundamentally different policy instrument.

The cost transmission does not remain contained at the raw material level. Tariff and CBAM-driven input cost increases flow progressively through semi-fabricated products, components, and finished goods. Industries characterised by thin operating margins — including automotive components, packaging, and construction profiles — face amplified exposure as carbon-adjusted aluminium costs rise through the supply chain.

As Roman Borisov, Regional Sales Director of RUSAL, has noted, competitive dynamics in the aluminium sector are shifting away from pure cost optimisation toward verified carbon performance, traceability, and compliance readiness as the defining commercial variables. (Source: AL Circle ALuminium LeaderSpeak 2026 e-Magazine)

Tariffs vs. CBAM: Two Instruments, Two Strategic Responses

The risk of conflating aluminium CBAM and tariffs is that it leads to the wrong mitigation strategies. Companies that treat CBAM as simply another trade barrier may over-invest in origin-switching and under-invest in the emissions verification infrastructure that actually determines their carbon liability.

| Dimension | Traditional Tariffs | CBAM |

|---|---|---|

| Policy Basis | Trade policy / customs duty | Environmental / carbon pricing |

| Calculation Method | Percentage of import value | Embedded carbon × EU ETS price |

| Affected Variable | All imports of a product | Imports with above-benchmark carbon intensity |

| Revenue Destination | Government customs revenue | EU carbon market mechanism |

| WTO Compatibility | Governed by WTO rules | Designed to comply with WTO non-discrimination principles |

| Strategic Response | Sourcing diversification, FTAs | Decarbonisation, emissions verification |

Tariffs create incentives for geographic supply chain diversification. CBAM creates incentives for production decarbonisation and investment in verifiable emissions measurement. A business facing both simultaneously requires an integrated strategy that addresses each instrument on its own terms. In addition, US aluminium tariffs are compounding this challenge by adding further pressure on supply chain decisions for producers exporting to multiple markets simultaneously.

Giovanni Magarotto, CEO and Managing Partner of T.T. Tomorrow Technology, has observed that tariffs on aluminium and related materials are increasing costs across the entire value chain, affecting raw material prices, production expenses, and the final competitiveness of end products. (Source: AL Circle ALuminium LeaderSpeak 2026 e-Magazine)

Tariff-driven supply chain restructuring is also producing longer-term capital allocation effects. The uncertainty itself, independent of the actual tariff level, discourages long-term investment commitments and accelerates the move toward regionalised supply networks. As Göksal Güngör, General Manager of Assan Alüminyum, has highlighted, evolving tariff structures are reinforcing the strategic logic of regionalisation and operational flexibility across the global aluminium trade. (Source: AL Circle ALuminium LeaderSpeak 2026 e-Magazine)

The Unresolved Design Tensions Inside CBAM

CBAM's framework contains several contested areas that have significant commercial implications for aluminium producers and importers. These are not minor technical details; they are structural questions whose resolution will materially affect competitive positioning.

The Scrap Processing Arbitrage Risk

Under current CBAM methodology, remelted scrap aluminium is assigned very low or near-zero embedded emissions. While this is technically defensible, it creates a potential regulatory arbitrage pathway. Non-EU producers could theoretically route production through scrap-based processing to minimise CBAM liability, even where the environmental integrity of that route is questionable.

EU-based secondary producers, who have invested in genuine low-carbon recycling infrastructure, are most exposed to this design risk. Greenwashing via CBAM loopholes is an acknowledged concern among industry stakeholders, and if CBAM's scrap treatment methodology is not tightened before full implementation, it could inadvertently disadvantage the producers it was partly designed to protect.

The Indirect Emissions Controversy

Aluminium smelting is extraordinarily electricity-intensive, making Scope 2 emissions — those generated by power consumption rather than direct combustion — a dominant variable in any producer's carbon footprint. Whether and how CBAM accounts for indirect emissions remains one of the regulation's most commercially significant unresolved questions.

Excluding indirect emissions understates the true carbon cost of aluminium from coal-grid producers. Including them creates measurement and verification complexity. Josef Nierling, CEO of Porsche Consulting Italy, has pointed out that while most producers can estimate aggregate Scope 1 and Scope 2 emissions, CBAM demands far greater granularity — specifically plant-level and product-specific data that meets EU monitoring and reporting verification standards. (Source: AL Circle ALuminium LeaderSpeak 2026 e-Magazine) Most producers are not yet operating at that level of data infrastructure.

Free Allocation Phase-Out Sequencing

European Aluminium's Director General Paul Voss has been direct on this point: carbon leakage protection must remain effective throughout the transition, and free ETS allocations should not be phased out for aluminium until CBAM has been fully proven to provide equivalent protection. (Source: AL Circle ALuminium LeaderSpeak 2026 e-Magazine)

The concern is not theoretical. If free allocations are withdrawn before CBAM is demonstrably functional as a carbon leakage shield, EU producers could face a period of unprotected competitive disadvantage against non-EU imports that have not yet been brought into full CBAM compliance. Consequently, European raw materials policy is increasingly being shaped by these very concerns around supply security and competitive integrity.

Secondary Aluminium's Structural Advantage Under Carbon Pricing

The environmental physics of aluminium recycling translate directly into CBAM competitiveness. Secondary aluminium production requires approximately 95% less energy than primary smelting from bauxite. This is not a marginal efficiency gain; it is a fundamental difference in production economics that CBAM's benchmark structure now monetises.

The 15x differential between the primary benchmark (1.423 tCO₂/tonne) and the secondary benchmark (0.091 tCO₂/tonne) will generate an increasingly significant landed cost advantage for scrap-based producers as the EU ETS carbon price rises. EU-based recyclers, already competing on proximity to markets and lower logistics costs, gain an additional structural advantage that grows in proportion to the carbon price.

For downstream manufacturers, this reshapes procurement strategy. Long-term supply agreements with verified secondary aluminium producers are not merely a sustainability gesture; they are a CBAM liability management tool.

The next major ASX story will hit our subscribers first

How Sustainability Credentials Are Becoming a Commercial Differentiator

The connection between carbon performance and market access is no longer aspirational. As Daniel Lim, Sales and Marketing Director of ALCOM, has noted, sustainability and compliance are becoming central to customer procurement decisions, particularly among OEMs serving European, North American, and developed Asian markets. (Source: AL Circle ALuminium LeaderSpeak 2026 e-Magazine)

This dynamic creates a bifurcating market. Producers with robust, third-party-verified emissions data and demonstrably low carbon footprints can access premium procurement channels. Those without face not only CBAM cost exposure but also the risk of exclusion from customer approved-supplier lists where carbon credentials are now a baseline requirement.

Furthermore, the question of green metals pricing is becoming increasingly relevant here, as verified low-carbon aluminium begins to command differentiated pricing across key buyer segments. The investment case for emissions traceability infrastructure is therefore twofold:

- Immediate CBAM liability reduction: Verified actual emissions below default values directly reduce certificate surrender obligations from 2026 onward.

- Commercial access preservation: Verified data enables participation in procurement processes where carbon performance is a qualifying criterion rather than a differentiating factor.

Strategic Priorities Across the Policy Transition Timeline

The 2025 to 2035 period represents a compressed window in which aluminium businesses must build the operational and commercial infrastructure to compete in a carbon-priced trading environment. The strategic priorities are distinct across three phases:

Near-Term (2025–2027):

- Complete the transition from CBAM reporting to full financial liability compliance before the 2026 deadline.

- Invest in plant-level emissions measurement capable of producing product-specific, verifiable data that meets EU monitoring rules.

- Audit existing supply chains to quantify CBAM exposure by origin, product category, and carbon intensity profile.

Medium-Term (2027–2030):

- Develop verified low-carbon supplier partnerships that lock in CBAM-advantaged landed costs through long-term offtake structures.

- Engage actively with CBAM regulatory consultation processes, particularly on unresolved design questions around scrap treatment and indirect emissions.

- Integrate carbon pricing scenarios into capital allocation and sourcing strategy modelling.

Long-Term (2030–2035):

- As CBAM costs approach tariff-equivalent magnitudes, businesses without decarbonised supply chains face compounding structural cost disadvantage.

- The industry's competitive hierarchy will be determined increasingly by carbon performance and traceability capability rather than production cost alone.

- Integrated management of both tariff exposure and CBAM liability — rather than siloed compliance functions — will characterise the most resilient operators.

However, competitive positioning under aluminium CBAM and tariffs will ultimately depend on how well businesses combine strategic foresight with operational investment. The leading aluminium producers are already moving to embed carbon performance and traceability into their core commercial strategies, recognising that the regulatory environment rewards preparation rather than reaction.

The aluminium businesses best positioned for the post-2026 environment are those investing now in verified emissions data, low-carbon supply partnerships, and integrated trade-and-carbon risk management — not those treating each policy change as a separate compliance event.

Frequently Asked Questions: Aluminium CBAM and Tariffs

When does full CBAM financial liability begin for aluminium?

Full financial liability under CBAM commences from 2026, following the transitional reporting-only phase that began in October 2023. Importers will be required to surrender CBAM certificates corresponding to the carbon price gap between the country of origin and the EU ETS carbon price. The EU's official CBAM guidance provides detailed compliance information for importers navigating these requirements.

Can exporters use actual emissions data instead of CBAM default values?

Yes. Exporters who provide verified actual emissions data can reduce their CBAM liability below the applicable default values. This creates a direct financial incentive for producers with lower-than-benchmark carbon intensity to invest in measurement infrastructure and third-party verification.

Do US tariffs and EU CBAM interact?

They operate as entirely separate and independent policy instruments. US aluminium tariffs are conventional import duties applied at the border, while CBAM is a carbon price on embedded emissions applied to EU-bound trade. Exporters serving both markets may face exposure to both simultaneously.

Which producers benefit most from CBAM?

Producers powered by renewable energy sources, particularly hydroelectric power, carry embedded carbon intensity well below CBAM benchmark levels. Canadian, Norwegian, and Icelandic smelters are among the clearest structural beneficiaries as CBAM costs widen the landed cost gap between clean and carbon-intensive supply.

What is the scrap loophole risk in CBAM?

Current CBAM methodology assigns very low embedded emissions to aluminium produced from remelted scrap. Critics argue this could incentivise non-EU producers to route production through scrap-based processes to minimise CBAM liability, potentially distorting competition with EU secondary producers who have made genuine investments in low-carbon recycling. Industry observers note that steel and aluminium supply chains more broadly are grappling with how CBAM cost burdens will be absorbed and passed through across the value chain.

Disclaimer: This article contains forward-looking projections and market estimates sourced from third-party analysis. These projections are subject to change based on regulatory developments, carbon price movements, and evolving trade policy. Nothing in this article constitutes financial or investment advice. Readers should conduct independent analysis and seek professional guidance before making business or investment decisions based on CBAM or tariff-related cost projections.

Want to Stay Ahead of ASX Mineral Discoveries Reshaping Global Commodity Supply Chains?

As regulatory shifts like CBAM and evolving tariff structures redefine which commodities attract capital and where they are sourced, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex data across 30+ commodities into actionable insights for investors at every level. Start your 14-day free trial at Discovery Alert today, or explore the historic returns major discoveries have delivered to understand why timing your entry matters.