June 22, 2026

The Metal That Builds the Future Is Being Defined Right Now in Shanghai

Every decade or so, a single material finds itself at the intersection of every major industrial megatrend simultaneously. In the 2020s, that material is aluminium. Lightweight enough to decarbonise transport, infinitely recyclable enough to satisfy circular economy mandates, and conductive enough to wire the clean energy grid, aluminium has quietly become one of the most strategically significant materials of the energy transition era. Yet understanding where this industry is heading requires more than reading price charts or production data. It requires being in the room where the decisions are made, and in July 2026, that room is in Shanghai.

Aluminium China 2026 returns for its 21st edition at a moment when the forces reshaping the global aluminium market are accelerating simultaneously across multiple fronts. For producers, processors, technology developers, and investors alike, the event represents one of the most concentrated opportunities to read the direction of a market that influences supply chains on every continent.

When big ASX news breaks, our subscribers know first

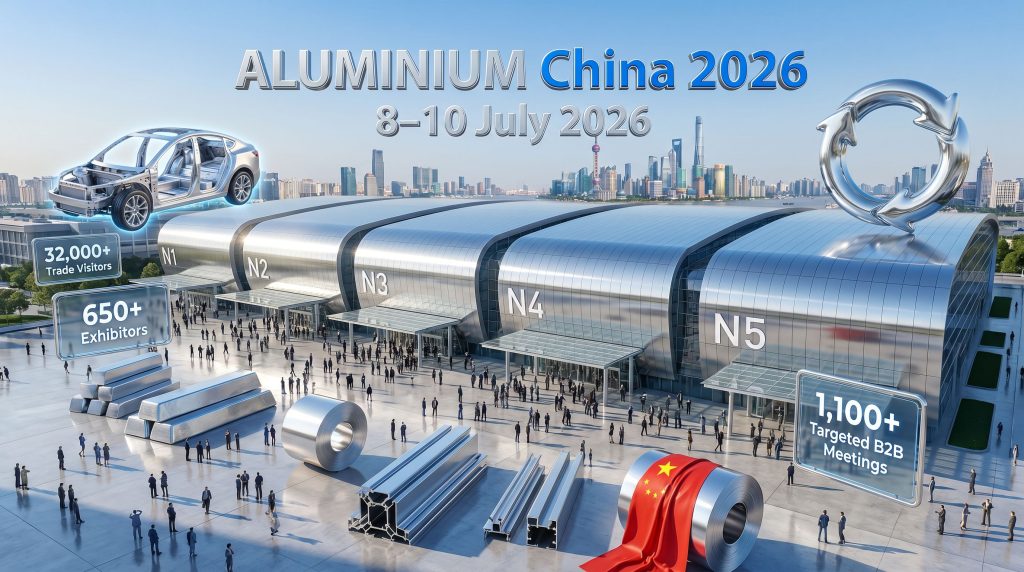

Event Snapshot: Aluminium China 2026 at a Glance

Before examining what drives the significance of this event, it is worth establishing the facts of its scope and structure.

| Detail | Information |

|---|---|

| Full Name | ALUMINIUM China 2026 |

| Dates | 8 to 10 July 2026 |

| Venue | Halls N1 to N5, Shanghai New International Expo Centre (SNIEC) |

| Organiser | RX China |

| Edition | 21st Annual |

| Expected Exhibitors | 650+ |

| Expected Trade Visitors and Delegations | 32,000+ |

| Targeted B2B Meetings | 1,100+ |

These figures alone place Aluminium China 2026 among the most significant industry gatherings in the global metals calendar. However, the numbers only partially explain why this event commands attention far beyond Asia's borders.

Why China Sits at the Centre of the Global Aluminium System

The Structural Reality of Chinese Dominance

China's position in global aluminium markets is not simply a matter of scale. It is a matter of structural centrality. The country accounts for the majority of global primary aluminium production and consumes a comparable share of global output, meaning that decisions made within China's policy, energy, and manufacturing ecosystems transmit directly into international price benchmarks, scrap flows, and downstream supply availability.

When Chinese smelters adjust output in response to energy cost pressures or environmental compliance requirements, spot markets in Europe, North America, and Southeast Asia feel the effect within weeks. When Chinese downstream manufacturers adopt new aluminium alloy specifications for electric vehicles or construction applications, those specifications frequently become de facto global standards as supply chains align around the dominant volume buyer.

Furthermore, this is why attending Aluminium China 2026 carries a qualitatively different intelligence value compared with relying on secondary data sources. Direct exposure to what exhibitors are prioritising, what technologies are drawing floor traffic, and what themes dominate the conference programme provides a forward-looking read on industry direction that no report can fully replicate. The top aluminium companies operating globally are invariably present, making the event an essential gathering point for the sector's most influential players.

Key Macro Trends Driving the 2026 Industry Agenda

| Trend Category | Key Driver | Global Relevance |

|---|---|---|

| Lightweight Transportation | EV adoption and fuel efficiency targets | High across automotive OEMs globally |

| Sustainable Packaging | Circular economy regulations | High across consumer goods and FMCG sectors |

| Recycled Aluminium | Carbon reduction commitments | Critical for decarbonisation strategies |

| Advanced Processing | Manufacturing and Industry 4.0 innovation | Medium-High for competitive differentiation |

| Non-Ferrous Integration | Multi-metal supply chain convergence | Growing across industrial diversification |

2026 as an Inflection Point

Several forces converge to make the 2026 edition of the exhibition particularly consequential. Electric vehicle adoption is moving from early-majority to mass-market penetration across key economies, dramatically increasing aluminium demand intensity per vehicle produced. Regulatory frameworks around carbon border adjustments and extended producer responsibility are making recycled aluminium content a commercial necessity rather than a voluntary commitment.

The clean energy buildout, spanning solar panels, grid infrastructure, and battery storage systems, continues to absorb aluminium at volumes that were not part of most demand forecasting models a decade ago. In addition, US aluminium tariffs are reshaping trade flows globally, adding further urgency to understanding how supply chains are realigning in response to geopolitical pressures.

The compounding effect of simultaneous demand growth across multiple clean technology sectors creates a structural, multi-decade tailwind for aluminium that fundamentally changes how the metal should be assessed within any long-term industrial or investment framework.

What Aluminium China 2026 Actually Covers

Exhibition Floor: A Value Chain in Physical Form

Spanning five halls at the SNIEC, the exhibition floor at Aluminium China 2026 maps the full aluminium value chain from primary production through to finished applications. Confirmed participating companies include ALUMEX PLC, Alumall Material and Machine Co. Ltd, Anhui Shenchang Aluminum Group Co. Ltd, China Hongqiao Group Limited, Foshan Davos Aluminum Extrusions Co. Ltd, Shandong Mingda Shengchang Aluminum Group Co. Ltd, Jagannath Company, and Anhui Yubo Aluminum Materials Co. Ltd, among many others.

The geographic representation spans Chinese domestic producers alongside participants from South Asia and Southeast Asia, reflecting the increasingly regional character of aluminium supply chains. What is particularly notable about the exhibition's physical architecture is that it reflects an important industry shift: aluminium is no longer positioned primarily as a commodity. The exhibition's thematic coverage increasingly emphasises engineered performance, whether that is high-strength alloys for aerospace applications, precision extrusion profiles for EV battery enclosures, or surface treatment technologies that extend product life cycles and reduce lifecycle carbon footprints.

Co-Located Events Creating a Multi-Metal Ecosystem

Running concurrently with Aluminium China 2026 at SNIEC are four complementary exhibitions that collectively transform the venue into one of Asia's most significant non-ferrous metals industry gatherings:

- Lightweight Asia 2026: Advanced materials and weight-reduction technologies across transport and industrial sectors

- Copper China 2026: Non-ferrous metals convergence covering copper supply chains and applications

- Magnesium China 2026: Lightweight alloy applications with particular relevance to aerospace and automotive

- Shanghai International Metal Recycling Expo 2026: Circular economy and secondary metals processing

For international delegations managing travel budgets, this co-location structure materially improves the return on investment of attendance. A procurement specialist sourcing across aluminium, copper, and magnesium for an EV platform can cover all three material categories within a single three-day visit.

Conference Programme and Knowledge Exchange

Beyond the exhibition floor, the structured conference programme provides a forum for the industry's most pressing strategic conversations. The 2026 International Forum on Non-ferrous Metal Recycling and Sustainable Development is a centrepiece of this programme, with panel sessions covering recycling innovation, circular economy practices, and sustainable growth pathways across non-ferrous metals. A notable panel discussion is scheduled for 15:40 to 16:10 on 9 July 2026, bringing together industry experts to address these themes in depth.

B2B Matchmaking: Structured Commercialisation

One of the most underappreciated features of major industry exhibitions is the structured matchmaking component. Aluminium China 2026's programme targets more than 1,100 curated B2B meetings, connecting buyers, suppliers, and technology partners through a pre-scheduled system that removes the randomness of traditional exhibition networking.

For companies entering new markets or seeking to diversify their supplier base, these structured sessions compress months of relationship-building into a concentrated three-day window. Factory visit components add further depth for procurement decision-makers and technology evaluators who require operational verification rather than catalogue-level familiarity.

The Four Thematic Pillars of Aluminium China 2026

Pillar 1: Recycling and the Circular Economy

Perhaps no single theme defines the contemporary aluminium industry more than the transition from linear to circular production models. The energy mathematics of secondary aluminium production are compelling: producing aluminium from recycled scrap requires approximately 5% of the energy needed to produce primary aluminium from bauxite, according to the International Aluminium Institute. This energy intensity differential translates directly into carbon reduction potential at a scale that makes recycled aluminium content one of the most cost-effective decarbonisation tools available to downstream manufacturers.

China's investment in recycling infrastructure has expanded rapidly, and the implications extend beyond domestic production economics. As China battery recycling capabilities evolve alongside aluminium scrap processing, the convergence of these circular economy investments is reshaping how secondary materials flow through global supply chains. Furthermore, as Chinese recycling capacity grows, it influences global scrap flows, affects international scrap pricing, and changes the availability of secondary material for manufacturers in other regions.

Pillar 2: Innovation in Downstream Processing

The aluminium processing sector is undergoing a technology-driven transformation that is only partially visible from commodity market data. Advanced alloy development, including high-strength series 7xxx alloys for aerospace and automotive structural applications, precision extrusion technologies capable of producing complex hollow profiles in a single pass, and digital manufacturing integration enabling real-time quality control, are all reshaping what aluminium can do as an engineered material.

Industry 4.0 integration within aluminium processing facilities is enabling continuous process optimisation that reduces both energy consumption and scrap rates simultaneously, improving the economics of precision manufacturing in ways that commodity-focused analysis consistently underestimates.

Pillar 3: Lightweight Transportation and EV Demand

The electric vehicle sector represents one of the most structurally significant demand growth vectors for aluminium in the coming decade. Battery electric vehicles typically contain significantly more aluminium than their internal combustion engine equivalents, driven by requirements for lightweight battery enclosures, body-in-white structures, heat management systems, and chassis components.

Estimates from industry bodies suggest that aluminium content per battery electric vehicle can reach 250 kilograms or more, compared with approximately 150 kilograms for a conventional vehicle, representing a demand intensity uplift that compounds as EV penetration rates rise. Chinese EV manufacturers including BYD, CATL supply chain participants, and a growing cohort of emerging OEMs are actively influencing global aluminium specification standards as their combined production volumes create gravitational pull in the supplier ecosystem.

Pillar 4: Global Collaboration and Market Access

For companies operating outside China's domestic market, Aluminium China 2026 provides a market access mechanism that is difficult to replicate through any other channel. Identifying emerging Chinese technology suppliers, understanding application development trends before they reach Western markets, and building direct relationships with producers in the world's largest aluminium ecosystem all carry commercial value that, compounding over years of participation, is substantial.

Consequently, the China metals market dynamics that play out across steel and iron ore are increasingly mirrored in aluminium, reinforcing why direct engagement through events like this one has become indispensable for globally active industry participants.

Two Decades of Growth: How the Exhibition Has Evolved

The trajectory from the first edition of Aluminium China to its 21st represents something more than incremental growth in exhibitor counts and visitor numbers. It mirrors China's own industrial transformation over the same period: from a country known primarily for high-volume, cost-competitive commodity production, to a sophisticated industrial ecosystem increasingly defined by value-added manufacturing, materials innovation, and sustainability integration.

The increasing weight of recycling and circular economy content within the programme is particularly instructive. Content categories that were marginal in early editions now anchor the conference programme, reflecting both the maturation of China's regulatory environment and the global alignment of industrial strategy around sustainability commitments. For instance, the Gladstone aluminium repowering initiative by Rio Tinto illustrates how global producers are investing heavily in decarbonisation, a trend that finds direct expression in the exhibition's growing sustainability focus.

The next major ASX story will hit our subscribers first

Who Should Attend and Why

Attendance Value by Stakeholder Type

| Stakeholder Type | Primary Value Proposition | Key Activities |

|---|---|---|

| Primary Producers | Market intelligence, buyer access | Industry forums, B2B matchmaking |

| Downstream Processors | Technology sourcing, supplier diversification | Exhibition floor, factory visits |

| Technology Providers | Market entry, product demonstration | Exhibition showcasing, panel discussions |

| Traders and Distributors | Price discovery, relationship building | B2B meetings, networking sessions |

| End-Users (Automotive, Packaging, Construction) | Supply chain mapping, specification updates | Technical conferences, supplier meetings |

| Investors and Analysts | Sector intelligence, deal flow identification | Forums, executive panel discussions |

The Intelligence Advantage of Direct Market Access

There is a meaningful difference between reading about China's aluminium market and being physically present within it. Exhibition participation patterns, the categories of technology attracting the heaviest floor traffic, and the themes commanding the most engaged conference audiences all function as leading indicators of where capital allocation, technology adoption, and regulatory focus are heading.

Historical exhibition cycles suggest that themes which dominate the conference programme at major industry events frequently precede shifts in M&A activity, joint venture formation, and technology licensing by 12 to 24 months. For investors and analysts, this makes Aluminium China 2026 a forward indicator as much as a networking opportunity.

Frequently Asked Questions: Aluminium China 2026

When and where does Aluminium China 2026 take place?

The event runs from 8 to 10 July 2026 at the Shanghai New International Expo Centre (SNIEC), across Halls N1 through N5 in Shanghai, China.

Who organises Aluminium China 2026?

The event is organised by RX China, a major trade exhibition organiser with extensive operations across industrial sectors in the Asia-Pacific region.

How large is the expected attendance?

Organisers anticipate more than 650 exhibitors and approximately 32,000 trade visitors and delegations across the three-day programme.

What industries are covered?

The exhibition spans primary production, extrusion and rolling, casting, surface treatment, recycling, and end-user applications across automotive, construction, packaging, aerospace, and consumer electronics.

What events run alongside Aluminium China 2026?

Four co-located exhibitions run concurrently: Lightweight Asia 2026, Copper China 2026, Magnesium China 2026, and the Shanghai International Metal Recycling Expo 2026.

Is there a structured B2B programme?

Yes. Organisers facilitate more than 1,100 targeted B2B meetings through a pre-scheduled matchmaking system, alongside factory visits for procurement and technology evaluation purposes.

Reading Aluminium China 2026 as a Market Signal

For global market participants, the deeper value of tracking Aluminium China 2026 lies in what the event's thematic emphasis reveals about the industry's medium-term trajectory. The concentration of programme content on recycling infrastructure, lightweight transportation applications, and sustainability frameworks is not coincidental. It reflects the convergence of regulatory pressure, technology economics, and end-user demand signals that are collectively redirecting capital flows within the aluminium sector.

Aluminium's role as a critical enabler material across solar energy infrastructure, EV supply chains, and grid modernisation means that demand projections extending through 2030 and beyond must account for simultaneous growth vectors that were historically independent. The compounding effect of these multiple demand streams, each with its own growth trajectory, means that the structural case for aluminium differs materially from historical commodity cycles driven by a single dominant end-use.

Investors and industry participants who treat aluminium purely through the lens of its historical commodity behaviour risk misreading a structural shift that the 2026 programme at Aluminium China makes visible in concrete, operational terms.

Disclaimer: This article contains forward-looking statements and projections regarding market trends, demand growth, and industry developments. These represent current assessments based on available information and industry analysis, and are subject to change. Nothing in this article constitutes financial advice or a recommendation to buy or sell any securities or commodities. Readers should conduct their own independent research before making any investment decisions.

Readers seeking additional context on global aluminium market developments, trade fair programming, and industry intelligence can explore related coverage available through AL Circle, which provides ongoing reporting across the aluminium value chain, and the Aluminium Journal, which offers in-depth editorial analysis of the exhibition's significance within the broader industry landscape.

Want to Know Which ASX Mineral Discoveries Could Benefit From Aluminium's Structural Boom?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries hit the ASX, turning complex geological announcements across more than 30 commodities into clear, actionable insights for both traders and long-term investors. Explore historic discoveries and the substantial returns they have generated, then begin your 14-day free trial to position yourself ahead of the broader market.