July 15, 2026

The Strategic Reframing of a Common Metal

For most of industrial history, aluminium occupied a peculiar position in the global materials hierarchy. It was everywhere, yet taken for granted. Abundant in the Earth's crust, lightweight, corrosion-resistant, and endlessly recyclable, it powered aircraft fuselages, beverage cans, and kitchen foil without attracting the geopolitical anxiety typically reserved for gold, uranium, or rare earth elements. That era of comfortable abundance is now giving way to something more complex, as the case for aluminium as a critical mineral gains formal recognition across major economies.

The convergence of clean energy targets, electrified transport mandates, and defence modernisation programs has forced governments across the world's largest economies to reconsider what the word critical actually means when applied to industrial materials. The answer, increasingly, has little to do with geological scarcity.

When big ASX news breaks, our subscribers know first

What "Critical" Really Means When Applied to Aluminium

Scarcity Is the Wrong Framework

The conventional assumption is that critical minerals are rare minerals. Cobalt, lithium, and rare earth elements are frequently discussed in terms of geological concentration and limited reserve bases. Aluminium shatters this logic entirely. It is the third most abundant element in the Earth's crust, comprising roughly 8% of crustal mass, and bauxite deposits exist across multiple continents. There is no shortage of the raw material.

What triggers critical status, as defined by modern policy frameworks, is not scarcity but consequence. Specifically, the economic, industrial, and national security consequences of supply disruption. Aluminium's classification rests on three compounding vulnerabilities:

- Its functional irreplaceability across defence, aerospace, automotive, and energy infrastructure

- The geographic concentration of its refining and smelting capacity

- The absence of domestic strategic reserves in major consuming nations

"A metal can be geologically common and strategically critical at the same time. The risk is not running out of bauxite; it is the inability to convert that bauxite into usable aluminium at scale, quickly enough, when geopolitical pressure demands it."

This distinction reshapes the entire policy conversation. Criticality, in its modern definition, is a function of supply chain architecture, not mineral abundance. Furthermore, understanding the broader critical minerals demand picture helps contextualise why aluminium now sits alongside lithium and cobalt in strategic policy frameworks.

How Major Economies Have Formally Recognised Aluminium's Strategic Role

The United States: Building a National Security Case

The U.S. formally included aluminium on both its 2022 and 2025 Critical Minerals Lists, a recognition that the metal's supply chain carries systemic risk for American industrial and defence capacity. More specifically, the Department of Energy designated aluminium within its Electric Eighteen framework, a set of materials deemed essential to the clean energy technology transition.

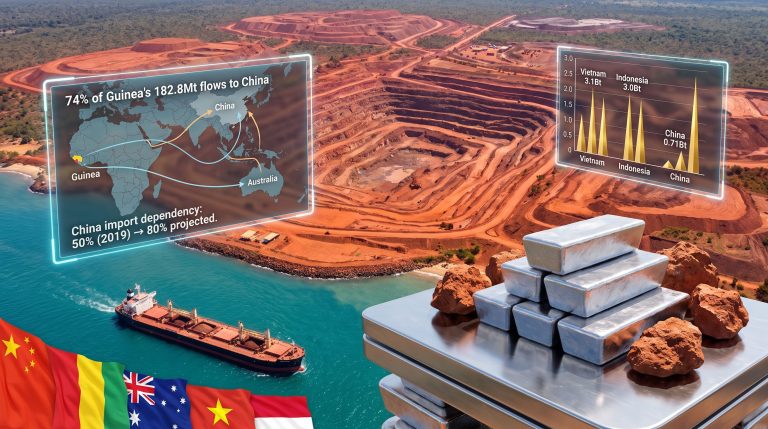

The numbers underlying this designation are striking. The U.S. aluminium sector generates USD 228 billion in total economic impact, equivalent to approximately 1% of gross domestic product, and supports around 400,000 jobs across smelting, fabrication, and downstream manufacturing. Yet despite this domestic footprint, the United States imports roughly 61% of its aluminium requirements and maintains no strategic stockpile of the metal. That combination of economic dependency and supply exposure is precisely the risk profile that critical mineral designations are designed to flag.

However, US aluminium tariffs add a further layer of complexity, as measures designed to protect domestic producers can simultaneously constrain supply availability for downstream manufacturers.

The European Union: Industrial Sovereignty Through Formal Classification

The EU took a structured legislative approach, formally incorporating aluminium into its Critical Raw Materials Act, enacted in July 2023. This framework sets benchmarks for domestic extraction, processing, and recycling capacity across a list of materials deemed essential to European industrial and green transition objectives. For aluminium, the classification reflects concerns about European dependence on imported primary metal and the risk that trade disruptions could constrain both manufacturing output and renewable energy deployment timelines.

The EU's approach differs from the U.S. model in emphasis. Where Washington focuses on defence capability and import exposure, Brussels frames criticality primarily through the lens of industrial sovereignty and the ability to meet binding decarbonisation commitments without external supply vulnerability. In addition, Europe's critical minerals supply chain strategy reflects growing urgency around reducing dependence on geopolitically sensitive import corridors.

The United Kingdom: A First-Time Designation With Significant Weighting

Perhaps the most notable recent development in formal aluminium classification occurred in the March 2025 UK National Critical Minerals Assessment, where aluminium appeared for the first time on the country's official critical minerals register. Importantly, the UK did not simply include aluminium as a footnote; it ranked the metal among the top five critical minerals by national consumption value, positioning it alongside lithium and cobalt in strategic importance.

The economic rationale for this classification is clear. The UK aluminium industry contributes approximately GBP 2.97 billion in Gross Value Added and directly supports around 37,000 jobs. These figures do not capture the full multiplier effect across aerospace, construction, packaging, and automotive supply chains that depend on stable aluminium supply.

Canada: Export Powerhouse Meets Strategic Dependency

Canada occupies a structurally unusual position in the global aluminium system. It is one of the world's leading primary aluminium producers, with Quebec serving as the productive backbone of the industry due to abundant hydropower resources that enable low-carbon smelting. Canadian primary aluminium exports are valued at approximately USD 10 billion annually, supporting more than 11,000 direct industry jobs.

Yet export strength does not eliminate strategic vulnerability. Canada's critical minerals framework acknowledges that dependence on specific trade corridors and downstream processing capacity in other jurisdictions creates risks that need to be actively managed. The tension between being a major producer and maintaining domestic industrial resilience is a recurring theme in Canadian minerals strategy.

NATO: Where Mineral Policy Meets Military Alliance

One dimension of aluminium's critical status that receives less public attention is its inclusion on NATO's Critical Materials List. Military alliances are now active participants in shaping how member nations classify and prioritise strategic materials. Aluminium's role in aerospace structures, armoured vehicle components, naval architecture, and missile systems makes it a defence input that NATO members are expected to treat with the same seriousness as fuel reserves or weapons stockpiles.

| Economy | Designation Framework | Year | Primary Driver |

|---|---|---|---|

| United States | Critical Minerals Lists + DOE Electric Eighteen | 2022, 2025 | Defence capacity and energy transition |

| European Union | Critical Raw Materials Act | July 2023 | Industrial sovereignty and decarbonisation |

| United Kingdom | National Critical Minerals Assessment | March 2025 | Consumption value and supply chain risk |

| Canada | Critical Minerals Strategy | Ongoing | Export strength and domestic resilience |

| NATO | Critical Materials List | Ongoing | Defence capability across member states |

The Energy Transition Argument: Why Demand Is Only Moving in One Direction

Solar Photovoltaics: Aluminium's Largest Renewable Consumer

The clean energy transition has fundamentally altered aluminium's demand profile. Solar photovoltaic infrastructure alone consumes approximately 8 million tonnes of aluminium per year, making it the single largest renewable energy application for the metal. Aluminium satisfies more than 85% of structural component demand in photovoltaic systems, including panel frames, mounting structures, and inverter housings.

The scale relationship between solar deployment and aluminium demand is direct and quantifiable: every 1 GW of solar capacity installed requires between 10,000 and 20,000 tonnes of aluminium. As governments accelerate renewable energy targets measured in hundreds of gigawatts, the volume implications for aluminium supply are substantial.

"Why is aluminium considered critical for solar energy? Aluminium provides the structural integrity of photovoltaic systems, accounts for the majority of component weight, and is functionally non-substitutable in most framing and mounting applications. At current solar deployment rates, annual demand from this sector alone justifies strategic material designation."

Electric Vehicles: A Structural Demand Multiplier

Each electric vehicle manufactured incorporates an average of 205 kg of aluminium, used across battery enclosures, chassis components, heat management systems, and body panels. Unlike internal combustion vehicles, EV design places a premium on weight reduction because battery mass directly affects driving range. This lightweighting imperative makes aluminium functionally irreplaceable in EV architecture at current technology levels.

CRU Group projects that aluminium demand originating from electric vehicle production could approach 10 million tonnes per year by 2030. When combined with solar demand and grid infrastructure requirements, the cumulative picture is one of structural, multi-decade demand growth that existing supply chains were not designed to service at this scale.

Grid Infrastructure, Wind Energy, and Construction

Beyond solar and EVs, aluminium's role in transmission infrastructure accounts for roughly 12% of total global demand. Aluminium conductors are standard in overhead power lines due to their combination of electrical conductivity, low weight, and corrosion resistance. Expanding electricity grids to support both renewable generation and EV charging networks amplifies this demand vector independently of solar and automotive growth.

Construction remains the single largest end-use sector for aluminium globally, representing approximately 25% of total consumption. Wind turbine nacelles, tower components, and offshore structure applications add further renewable energy demand to this already dominant segment.

Aluminium's Critical Status Compared to Other Strategic Minerals

| Mineral | Physical Scarcity | Supply Chain Risk | Energy Transition Role | Recyclability |

|---|---|---|---|---|

| Aluminium | Low (abundant crust) | High (import dependency, concentrated processing) | Very High | Infinite |

| Lithium | Moderate | High (geographic concentration) | Very High | Limited |

| Cobalt | Moderate | Very High (DRC concentration) | High | Partial |

| Rare Earths | Low to Moderate | Very High (Chinese processing dominance) | High | Very Limited |

Aluminium's risk profile is structurally distinct from every other metal on this list. Its criticality is not geological but logistical, geopolitical, and infrastructural. The concern is not the availability of bauxite; it is the capacity to refine alumina and smelt primary aluminium within secure supply chains when trade relationships become adversarial. Consequently, top aluminium producers are increasingly being assessed not just on output volumes but on the resilience and geographic diversity of their supply chains.

The Green Energy Paradox: A High-Emission Metal Building a Low-Emission World

The Carbon Contradiction

Primary aluminium smelting is one of the most energy-intensive industrial processes in existence. When powered by fossil fuel electricity, it produces significant greenhouse gas emissions per tonne of output, creating a genuine paradox: the metal most needed to build clean energy infrastructure is itself a source of industrial carbon emissions during production.

This tension is not theoretical. It is a material consideration in procurement decisions made by renewable energy developers, EV manufacturers, and government infrastructure programs that operate under binding emissions accounting frameworks. According to research from RUSI, aluminium's dual role as both an emissions-intensive industry and an enabler of the clean energy transition makes it one of the most strategically complex materials of the current decade.

Low-Carbon Aluminium as a Policy and Market Response

The policy response has focused on two pathways:

- Hydropower-smelted aluminium, produced in countries like Canada and Norway where smelters are powered by renewable electricity, significantly reduces the carbon intensity of primary production. This material now commands a price premium in markets where buyers face emissions obligations.

- Mandated procurement specifications increasingly require low-carbon aluminium certifications for public infrastructure projects, creating a regulatory market signal that is reshaping sourcing decisions across Europe and North America.

Recycling as a Supply Security Mechanism

Secondary aluminium production, derived from recycled scrap, requires approximately 5% of the energy needed to produce primary metal from bauxite. This energy efficiency advantage makes recycling not just an environmental preference but a genuine strategic supply tool.

Domestic recycling programs reduce import dependency, are insulated from geopolitical disruptions in bauxite supply chains, and produce metal that meets the carbon intensity requirements of green procurement frameworks. Furthermore, mining decarbonisation strategies increasingly incorporate secondary production as a core lever for reducing both emissions and supply chain exposure simultaneously.

The next major ASX story will hit our subscribers first

Supply Chain Vulnerabilities That Underpin Critical Classification

Upstream Concentration in the Bauxite and Alumina Stages

The aluminium supply chain runs from bauxite mining through alumina refining to primary smelting, and concentration risk exists at each stage. Bauxite production is dominated by Guinea, Australia, and China, with Guinea holding the world's largest reserves. Alumina refining and primary smelting capacity has increasingly concentrated in China, which accounts for more than half of global primary aluminium output.

This concentration means that trade disruptions, export restrictions, or diplomatic deterioration involving a small number of producing nations can propagate rapidly through the entire downstream aluminium supply chain of consuming economies.

The Absence of Strategic Stockpiles

Unlike petroleum, which is managed through strategic reserves in most developed economies, aluminium has no equivalent buffer in the United States or most European nations. The U.S. imports 61% of its aluminium with no strategic reserve to draw on in the event of supply disruption. This structural absence amplifies the strategic risk that formal critical mineral designation is intended to address.

Trade Policy Amplification

Tariff regimes, including U.S. Section 232 national security measures applied to aluminium imports, interact with critical mineral designations in complex ways. Measures designed to protect domestic producers can simultaneously tighten supply availability for downstream manufacturers. Sanctions applied to Russian aluminium, a significant global supplier, demonstrated how quickly policy decisions can ripple through global pricing and availability.

The Aluminium Council of Australia has documented how formal critical mineral classification frameworks can, when properly implemented, help governments navigate these trade policy tensions by establishing clear strategic priorities that transcend short-term tariff considerations.

Frequently Asked Questions: Aluminium as a Critical Mineral

Is aluminium rare enough to qualify as a critical mineral?

No. Aluminium is geologically abundant, but criticality is determined by supply chain risk, economic dependency, and strategic indispensability, not physical scarcity. The case for aluminium as a critical mineral rests entirely on structural vulnerabilities in the conversion and distribution of the metal, not on any geological shortage of bauxite.

Which countries officially classify aluminium as critical?

The United States, European Union, United Kingdom, Canada, and NATO member states through respective frameworks have all formally recognised aluminium's critical status.

How much aluminium does a single electric vehicle contain?

An average electric vehicle incorporates approximately 205 kg of aluminium across its structural, thermal, and body components.

What makes aluminium irreplaceable in aerospace and defence?

Its strength-to-weight ratio, corrosion resistance, and machinability make it the default structural material in aircraft, naval vessels, and military vehicle platforms where weight directly affects operational performance.

How does aluminium recycling reduce supply chain risk?

Secondary production from scrap requires only around 5% of the energy of primary smelting, is geographically distributed, and reduces exposure to disruptions in bauxite and alumina supply chains concentrated in politically sensitive regions.

What is low-carbon aluminium?

Primary aluminium produced using renewable energy sources, particularly hydropower, generating significantly lower lifecycle carbon emissions than conventionally smelted metal, and increasingly specified in green procurement frameworks.

The Strategic Summary: A Permanent Reclassification, Not a Policy Trend

The designation of aluminium as a critical mineral across the United States, European Union, United Kingdom, Canada, and NATO represents something more durable than a policy response to a current geopolitical moment. It reflects a structural reassessment of how modern economies function and what they cannot operate without.

The demand forces driving this reassessment are not cyclical. Solar deployment, EV production, grid expansion, and defence modernisation are decade-long commitments with compounding aluminium requirements. The supply chain vulnerabilities that make those requirements difficult to guarantee are embedded in geography, infrastructure, and trade architecture that cannot be rapidly reconfigured.

| Strategic Dimension | Key Metric | Implication |

|---|---|---|

| U.S. Economic Impact | USD 228 billion / 400,000 jobs | Systemic economic dependency |

| Solar PV Demand | ~8 million tonnes per year | Renewable energy bottleneck risk |

| EV Demand Forecast | ~10 million tonnes per year by 2030 (CRU) | Structural demand acceleration |

| Aluminium Per EV | ~205 kg | Non-substitutable lightweighting role |

| U.S. Import Reliance | 61% with no strategic reserve | National security vulnerability |

| UK GVA Contribution | ~GBP 2.97 billion | Strategic industrial asset |

| Canada Export Value | USD 10 billion annually | Trade-critical commodity status |

| Recycling Energy Saving | ~95% less energy vs. primary | Circular economy security lever |

What the policy frameworks of major economies have collectively recognised is that aluminium's strategic value cannot be measured by geological abundance or commodity pricing alone. Its role sits at the intersection of defence capability, decarbonisation infrastructure, and industrial employment in ways that make supply disruption a systemic risk rather than a market inconvenience.

The reclassification of aluminium as a critical mineral is not a temporary designation awaiting revision. It is a structural acknowledgement that the metal underpinning modern industrial civilisation requires the same policy seriousness previously reserved for oil, rare earths, and advanced semiconductors.

Disclaimer: This article contains forward-looking demand projections and strategic assessments sourced from third-party research, including CRU Group forecasts. These projections involve assumptions that may not materialise. Readers should conduct independent research before making investment or business decisions based on any figures cited.

Want to Know When the Next Major ASX Mineral Discovery Hits the Market?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — including critical minerals like aluminium and its upstream inputs — so subscribers can act before the broader market reacts. Start your 14-day free trial today, or explore Discovery Alert's discoveries page to see how major mineral finds have historically generated substantial returns.