July 15, 2026

The Structural Paradox at the Heart of Asia's Bauxite Economy

When geologists assess a mineral province, reserve size is typically treated as the foundational metric of future supply potential. Yet across Asia's bauxite landscape, this assumption consistently fails. The nations sitting on the continent's largest bauxite deposits are not the nations extracting the most ore. Instead, the Asia bauxite supply chain is organised around industrial throughput capacity, capital deployment, and downstream integration rather than geological endowment alone.

This structural paradox is not a temporary market anomaly. It is a deeply embedded feature of how bauxite flows through Asia, and understanding it requires looking beyond resource maps toward the industrial logic that transforms ore deposits into refined alumina and ultimately into aluminium metal. Furthermore, shifts in bauxite and alumina markets are increasingly influencing how supply chains are structured across the region.

When big ASX news breaks, our subscribers know first

Reserve Distribution vs. Extraction Reality: Asia's Defining Imbalance

Global bauxite production estimates place total reserves at between 29 and 30 billion tonnes, yet annual extraction runs at roughly 480 million tonnes per year, representing only 1.6 to 1.7% of the total reserve base. Asia accounts for approximately 18% of global reserves, yet the geographic distribution of those reserves bears little relationship to the region's production hierarchy.

The following snapshot illustrates just how disconnected reserve size is from actual extraction activity across Asia's key bauxite-holding nations:

| Country | Estimated Reserves | Share of Global Reserves | Current Production Role |

|---|---|---|---|

| Vietnam | 3.1 billion tonnes | ~10.7% | Very low extraction rate |

| Indonesia | 3.0 billion tonnes | ~10.3% | Shifted toward domestic alumina refining post-2023 export ban |

| China | 0.71 billion tonnes | ~2.4% | Dominant regional producer and consumer |

| India | 0.65 billion tonnes | ~2.2% | Growing domestic processor with export potential |

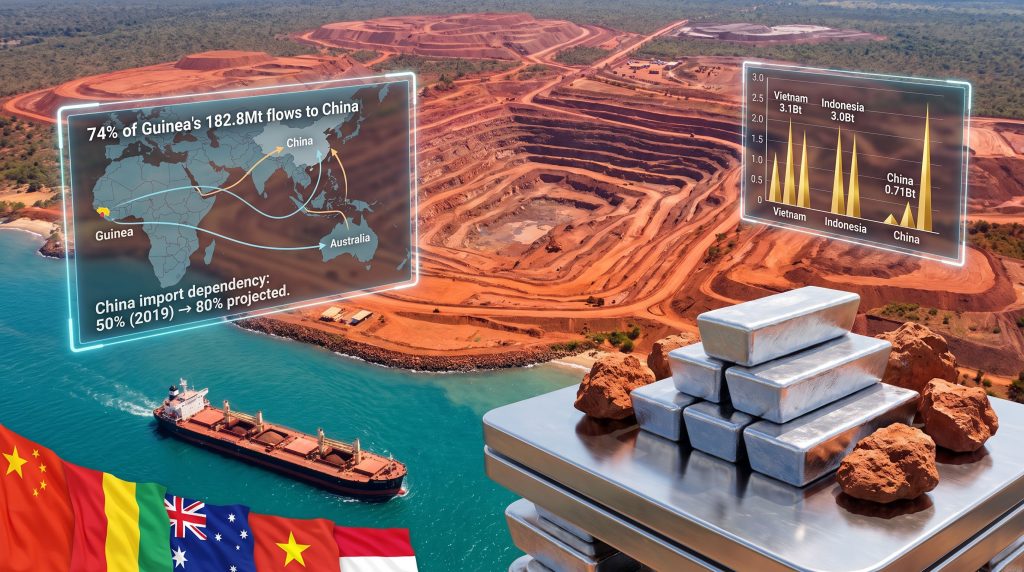

Vietnam holds the largest reserve base in Asia at 3.1 billion tonnes, yet its extraction rate remains marginal. China, by contrast, holds just 0.71 billion tonnes of domestic reserves but functions as the region's dominant driver of both production and consumption. This inversion is the central structural feature of the Asia bauxite supply chain.

The countries controlling the most bauxite in the ground are not the ones controlling the flow of ore through the market. Production leadership in Asia is determined by processing capacity, not geological wealth.

Why China Dominates Output Despite Holding Less Than 3% of Regional Reserves

Industrial Infrastructure as the True Determinant of Supply Power

China's bauxite production dominance is not a geological story. It is an industrial capacity story. With an estimated 225 million tonnes of annual alumina refining capacity, China has constructed the world's largest downstream processing infrastructure for the aluminium supply chain. The consequence of this scale is a structural import dependency that grows more pronounced each year.

Industry projections indicate that China could import as much as 80% of its bauxite requirements in the near term, a dramatic escalation from approximately 50% in 2019. This trajectory reflects the fundamental mismatch between China's domestic reserve base of 0.71 billion tonnes and the industrial appetite of its alumina refining sector. Consequently, China's industrial demand for raw materials continues to reshape global supply flows across multiple commodity categories.

Several forces reinforce this dependency:

- Domestic bauxite grades in China have declined over decades of intensive mining, reducing the efficiency and economics of local extraction

- The rapid expansion of alumina refining capacity in provinces such as Shanxi, Guizhou, and Guangxi has outpaced any feasible increase in domestic ore supply

- China's aluminium smelting sector, the world's largest, continues to consume finished alumina at volumes that demand consistent seaborne ore imports

The Quality Dimension: Why Chinese Domestic Ore Falls Short

One factor often overlooked in conventional market analysis is the diaspore-dominated mineralogy of Chinese bauxite. Unlike the gibbsite-rich deposits found in Guinea, Australia, and much of West Africa, Chinese domestic ore is predominantly diasporic, requiring higher processing temperatures and more energy-intensive refining conditions. This mineralogical distinction creates a cost disadvantage that makes imported gibbsitic bauxite economically attractive even when domestic ore is technically available.

Gibbsite-dominant ores dissolve more readily under the Bayer process, the industry-standard refining method, at lower temperatures and pressures. This translates directly into lower energy consumption per tonne of alumina produced. For Chinese alumina refiners operating at scale, preferring high-grade West African or Australian gibbsitic ore over lower-quality domestic diasporic material is a commercially rational decision, not merely a supply gap response. For a broader view of how bauxite moves through the supply chain, the transformation from raw ore to finished aluminium involves several capital-intensive processing stages.

Guinea: The Critical Chokepoint in Asia's Bauxite Supply Architecture

How a West African Nation Became the Backbone of Asian Aluminium Production

Guinea's emergence as the anchor of the Asia bauxite supply chain represents one of the more consequential supply chain realignments in recent commodity history. The country holds an estimated 7.4 billion tonnes of bauxite reserves, making it the single largest reserve holder globally. Crucially, Guinean bauxite is predominantly gibbsitic, high-grade, and located in deposits accessible to large-scale open-cut mining operations.

In 2025, Guinea exported approximately 182.8 million tonnes of bauxite, with an estimated 74% of that volume directed toward Chinese buyers. Chinese-backed consortiums are estimated to control around 70% of Guinea's bauxite import flows into China, reflecting a degree of upstream vertical integration that few other commodity supply chains can match.

This integration was not accidental. Over the preceding decade, Chinese capital financed port infrastructure, rail corridors, and mine development across Guinea's Boké region, effectively constructing a dedicated export corridor calibrated to Chinese refinery specifications. The result is a supply chain architecture that is highly efficient under stable conditions but structurally concentrated in ways that introduce significant systemic risk.

Why Guinea's Dominance Is Both an Asset and a Vulnerability

The concentration of Chinese bauxite procurement in a single nation exposes the entire supply chain to several interconnected risks:

- Political instability risk: Guinea has experienced repeated changes in government, with military-led transitions creating periodic uncertainty around mining concession frameworks and export levy structures

- Infrastructure dependency risk: The rail and port systems that move ore from the interior to the coast are critical single points of failure; any prolonged disruption would immediately constrain seaborne supply

- Pricing leverage risk: As Guinea's strategic importance to Chinese refiners grows, the Guinean state retains increasing leverage to renegotiate export royalties and local content requirements

Australia's Role: Reliable Supply with Concentrated Exposure

Australia functions as China's second-largest bauxite supplier and provides a meaningful degree of supply diversification relative to Guinea. However, Australia's bauxite trade profile carries its own concentration risk from the opposite direction.

Approximately 98% of Australian bauxite exports flow to Chinese buyers, meaning that while Australia diversifies China's supplier base, China effectively constitutes Australia's entire bauxite export market. The bilateral trade reached a value of approximately $1.5 billion in 2022, making it a material revenue stream for Australian mining operations in Western Australia and Queensland.

Australian bauxite, drawn primarily from the Darling Range and Cape York Peninsula deposits, is gibbsitic and well-suited to Chinese refinery configurations. However, Australia's geographic distance from Chinese ports adds freight costs that West African suppliers, particularly in Guinea, can undercut on a delivered basis during periods of shipping rate volatility. The performance of the leading bauxite mines in both countries continues to shape the competitive dynamics of seaborne ore pricing.

Indonesia's Strategic Pivot: From Ore Exporter to Regional Alumina Competitor

Indonesia's decision to ban raw bauxite exports in 2023 fundamentally altered the trade flow dynamics across the Asia bauxite supply chain. Prior to the ban, Indonesia was a significant seaborne ore supplier, particularly to Chinese refineries. The restriction was designed to capture more value domestically by incentivising investment in Indonesian alumina refining capacity. However, as analysis of Indonesia's aluminium ambitions highlights, building sufficient domestic bauxite supply to match refinery expansion has proven a considerable challenge.

The structural impact of this shift is significant:

| Metric | Pre-2023 (Ore Exporter) | Post-2023 (Alumina Focus) |

|---|---|---|

| Primary Export Product | Raw bauxite ore | Refined alumina |

| Contribution to Seaborne Ore Supply | High | Significantly reduced |

| Regional Competitive Effect | Minimal | Increasing alumina market competition |

| Strategic Alignment | Volume-driven extraction | Value-added domestic processing |

The downstream consequence of Indonesia's policy is a gradual increase in regional alumina supply competition as Indonesian refining capacity comes online. This places Indonesian alumina in direct competition with Chinese-refined product in third-party markets, adding a new dimension of competitive pressure to Asia's aluminium value chain.

The next major ASX story will hit our subscribers first

Vietnam's Dormant Giant: 3.1 Billion Tonnes Waiting for a Trigger

Vietnam's position in the Asia bauxite supply chain is defined by what has not happened rather than what has. The country holds the largest reserve base in Asia at 3.1 billion tonnes, concentrated in the Central Highlands provinces of Dak Nong and Lam Dong, yet extraction remains at a fraction of its theoretical potential.

Several structural barriers explain this inertia:

- Infrastructure deficit: The Central Highlands are landlocked relative to deep-water port access, requiring substantial investment in road or rail corridors to make large-scale export economics viable

- Environmental sensitivities: Bauxite mining in the Central Highlands intersects with highland forest ecosystems and indigenous community land rights, creating regulatory and social licence complexity

- Processing-first policy orientation: Vietnamese industrial policy has historically favoured developing domestic alumina refining capacity before scaling raw ore exports, mirroring the Indonesian model

- Capital access constraints: The scale of investment required to develop a world-class bauxite-to-port corridor has exceeded the appetite of both domestic Vietnamese capital and most international mining majors

For Vietnam to transition from reserve holder to meaningful Asia bauxite supply chain participant, it would require a convergence of infrastructure investment, regulatory clarity, and sufficiently elevated long-term bauxite prices to justify the capital commitment.

India's Emerging Dual Role: Consumer and Potential Regional Exporter

India's 0.65 billion tonnes of bauxite reserves are geographically concentrated in Odisha and Andhra Pradesh, with additional deposits in Gujarat, Maharashtra, and Jharkhand. The key operators shaping India's position in the regional supply chain are NALCO, a public sector undertaking with integrated mining-to-smelting operations, and Vedanta, which operates across multiple points of the aluminium value chain.

India's bauxite economics are shaped by a protective regulatory framework that has historically restricted raw ore exports to preserve domestic refinery feedstock. This policy stance positions India primarily as a domestic consumer rather than a regional exporter, though rising Indian aluminium demand and planned capacity expansions suggest the country's influence on Asian bauxite trade flows will grow through the 2030s.

India's domestic aluminium consumption is expanding across infrastructure, automotive, and packaging sectors, creating sustained demand growth that will require either increased domestic bauxite extraction or, eventually, seaborne imports. Such an outcome would introduce India as a meaningful demand participant in the same seaborne markets that China currently dominates.

The Three Supply Chain Risk Vectors Investors Must Understand

Risk Vector 1: Policy Volatility Across Supplier Nations

Regulatory change has proven to be a faster and more disruptive force in the Asia bauxite supply chain than geological depletion. Furthermore, understanding commodity price impacts is essential for investors navigating supply chains where policy shifts can rapidly alter market fundamentals. Key policy risks currently in play include:

- Guinea's evolving export levy and royalty structures, which directly affect the landed cost of ore at Chinese refineries

- Indonesia's 2023 raw ore export prohibition, which removed a significant seaborne supply source

- Malaysia's environmental processing moratoriums, which have periodically curtailed bauxite extraction in Pahang state despite the country holding material reserve potential

Risk Vector 2: Logistical Bottlenecks in Maritime Bulk Shipping

Bauxite is a high-volume, low-value-per-tonne commodity. Its economics are acutely sensitive to bulk shipping freight rates, port congestion, and vessel availability. The Boké corridor in Guinea and the Port of Kamsar handle enormous throughput volumes, and any infrastructure disruption translates directly into supply shortfalls at Chinese refinery gates within weeks.

Risk Vector 3: Demand Concentration in a Single Market

Asia-Pacific accounted for 54.44% of global bauxite volume in 2025. When Chinese industrial output contracts, slows, or shifts, the effect on global bauxite demand is immediate and material. No other buyer in the global system has the purchasing scale to absorb displaced Chinese demand in the near term.

The structural concentration of both supply and demand in the China-Guinea axis represents the most consequential systemic risk in the global bauxite market today. Diversification is underway, but the pace of change is slower than the pace of risk accumulation.

Procurement Strategies: How Chinese Alumina Producers Are Managing Supply Security

Major Chinese alumina producers have developed a layered procurement architecture that balances supply security against capital efficiency:

| Procurement Strategy | Key Advantage | Key Risk |

|---|---|---|

| Vertical integration via equity mine ownership | Maximum supply certainty and cost control | Capital-intensive; exposed to host-country sovereign risk |

| Long-term off-take agreements | Volume assurance for buyers; revenue certainty for miners | Price inflexibility during market downturns |

| Spot market purchasing | Flexibility and ability to capture price dips | High vulnerability to supply shocks and price spikes |

Chinese producers operating in Guinea under equity ownership structures benefit from priority ore access and the ability to align ore specifications with specific refinery configurations. However, these positions also expose them to political risk in a jurisdiction that has demonstrated willingness to renegotiate mining terms, a factor that multi-year off-take agreements partially mitigate by introducing contractual certainty at the cost of pricing flexibility.

Geographic Diversification: China's Effort to Reduce Single-Source Dependency

Awareness of Guinea-concentration risk has driven systematic efforts to develop alternative bauxite sources. Emerging supplier nations entering China's procurement orbit include:

- Ghana: Growing export volumes with established port infrastructure and high-grade gibbsitic deposits

- Laos: Early-stage development with geographic proximity reducing freight costs relative to West African alternatives

- Turkey: Moderate reserve base with established trade relationships

- Malaysia: Intermittent supplier subject to environmental extraction moratoriums

Southeast Asia as a whole holds close to 20 billion tonnes of bauxite reserves across its constituent nations, suggesting that the region's long-term contribution to the Asia bauxite supply chain remains structurally underweighted relative to its geological potential. The primary constraint is not the ore; it is the combination of infrastructure, policy frameworks, and capital willing to develop it.

Three Scenarios for Asia's Bauxite Trade Architecture Through 2036

Scenario 1: Guinea Consolidation. Guinea maintains its dominant position as Chinese infrastructure investment deepens integration. Supply concentration risk intensifies, but operational efficiency improves. This scenario is most likely under conditions of political stability in Guinea and continued Chinese industrial aluminium demand growth.

Scenario 2: Southeast Asian Activation. Vietnam, Laos, and broader ASEAN producers develop extraction and export infrastructure, redistributing seaborne supply flows across multiple origin points. This scenario requires significant capital commitment and policy reform in Vietnam specifically, and is more likely as a medium-to-long-term outcome than an immediate market shift.

Scenario 3: Policy Fragmentation. Multiple simultaneous export restrictions across key supplier nations accelerate the economics of alumina refining onshoring in consuming countries, reducing raw ore trade volumes globally. Indonesia's trajectory provides the existing template for this scenario.

Rising Indian aluminium demand introduces a fourth variable: as India's consumption base expands, its demand for bauxite feedstock could eventually redirect seaborne ore flows that currently terminate in China toward Indian refinery gates, subtly rebalancing the Asia bauxite supply chain's demand axis.

Frequently Asked Questions: Asia Bauxite Supply Chain

Which country holds the largest bauxite reserves in Asia?

Vietnam leads Asia's reserve base with 3.1 billion tonnes, representing approximately 10.7% of global bauxite reserves. Indonesia follows closely with 3.0 billion tonnes.

Why does China import bauxite despite being a major aluminium producer?

China's domestic reserve base of 0.71 billion tonnes is insufficient to supply its 225 million tonnes of annual alumina refining capacity. Additionally, domestic Chinese ore is predominantly diasporic, requiring more energy-intensive processing than the gibbsitic ores available from Guinea and Australia, creating both a volume gap and a quality-cost incentive to import.

What impact did Indonesia's 2023 export ban have on bauxite trade flows?

The ban removed Indonesia as a meaningful seaborne raw ore supplier, tightening global bauxite supply and redirecting Indonesian industrial focus toward domestic alumina production. This modestly supported bauxite prices and accelerated Chinese efforts to secure alternative ore sources.

How does Guinea fit into Asia's bauxite supply chain?

Guinea is the dominant seaborne bauxite supplier globally, exporting approximately 182.8 million tonnes in 2025, with 74% directed to China. Chinese-backed consortiums control an estimated 70% of Guinea's bauxite export flows to China.

What are the biggest risks facing Asia's bauxite supply chain today?

The three primary risk vectors are policy volatility in key supplier nations, logistical bottlenecks in high-volume maritime bulk shipping, and extreme demand concentration in China, which accounts for the majority of Asia-Pacific's 54.44% share of global bauxite volume.

Is Vietnam likely to become a major bauxite exporter in the future?

Vietnam has the geological foundation to become a significant exporter, but infrastructure constraints, environmental regulatory complexity, and a policy preference for domestic processing over raw ore exports mean this transition is unlikely in the short term. A ten-to-fifteen-year development horizon is a more realistic expectation, contingent on sustained capital investment.

Key Takeaways: Asia's Bauxite Supply Chain at a Glance

- Reserve size does not equal production leadership: Vietnam and Indonesia hold the most reserves, but China drives extraction and consumption through industrial infrastructure scale

- Chinese import dependency is accelerating: Projected to reach 80% of bauxite requirements, up from approximately 50% in 2019, driven by both volume shortfall and ore quality economics

- Guinea is the structural chokepoint: Approximately 74% of Guinea's 182.8 million tonne 2025 export volume flows to China, creating a bilateral concentration risk for the entire global supply chain

- Ore mineralogy shapes procurement decisions: The preference for gibbsitic over diasporic ore is a commercially significant driver of China's import behaviour that is underappreciated in mainstream market commentary

- Policy risk is moving faster than geology: Export bans, levy restructuring, and environmental moratoriums are reshaping Asia's bauxite trade architecture more rapidly than resource depletion

- Diversification is progressing but incomplete: Ghana, Laos, Turkey, and Malaysia are entering China's procurement consideration set, but Guinea and Australia remain structurally dominant in the near term

Disclaimer: This article contains forward-looking statements, scenario projections, and market forecasts based on available industry data and analytical frameworks. These projections involve inherent uncertainty and should not be construed as investment advice. Readers are encouraged to conduct independent due diligence before making financial or commercial decisions based on any content herein. Market conditions, trade policies, and reserve estimates are subject to change.

Want to Track ASX Mineral Discoveries Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, transforming complex commodity data across more than 30 minerals — including bauxite-adjacent opportunities — into clear, actionable insights for both short-term traders and long-term investors. Explore historic examples of major mineral discoveries and their market returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the next significant ASX announcement.